Navigating the annual tax season is a cornerstone of responsible personal finance. Understanding when you can submit your taxes, along with the implications of timely or delayed filing, is crucial for financial planning, avoiding penalties, and maximizing any potential refunds. While the general tax season is widely recognized, the specific window for submission, critical dates, and strategic considerations for filers often require a deeper dive.

Understanding the Annual Tax Season Calendar

The Internal Revenue Service (IRS) sets a precise calendar for when taxpayers can submit their federal income tax returns each year. This calendar dictates the official opening and closing dates, as well as specific deadlines for various types of filers and payments.

The Official Opening and Closing Dates

Typically, the IRS begins accepting tax returns in late January. This opening allows a window of several weeks before the traditional filing deadline of April 15th. For example, in a given year, the IRS might announce that it will begin accepting and processing 2023 tax returns on January 29, 2024. This early start provides ample time for individuals and tax professionals to prepare and submit returns electronically or by mail. The primary deadline for most individual taxpayers to file federal income tax returns and pay any taxes owed is generally April 15th of each year. If April 15th falls on a weekend or holiday, the deadline is typically pushed to the next business day. For example, if April 15th is a Saturday, the deadline would shift to Monday, April 17th. This core deadline is non-negotiable for most, carrying significant financial consequences if missed without proper measures.

State Tax Deadlines

It’s vital to remember that federal tax deadlines do not always align perfectly with state income tax deadlines. Most states that levy an income tax will mirror the federal April 15th deadline. However, there are exceptions. Some states have earlier or later deadlines, and it’s imperative for taxpayers to verify the specific dates for their state of residence. For instance, some states might have an extended deadline for certain types of income or specific counties. Furthermore, some states do not have a state income tax at all, simplifying the process for residents there, but not absolving them of their federal obligations. Misunderstanding state-specific dates can lead to penalties from both federal and state tax authorities, underscoring the importance of localized financial diligence.

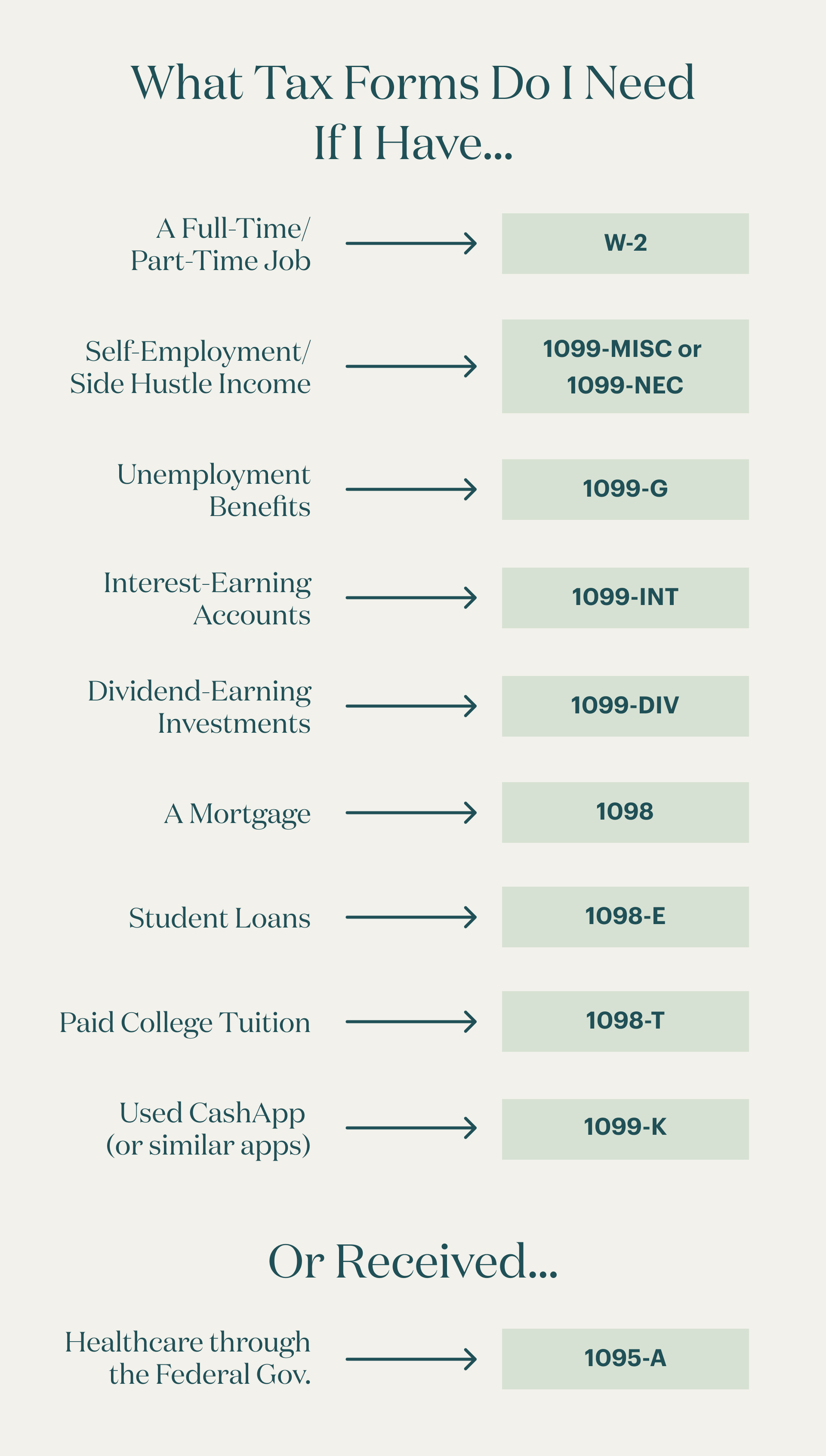

Key Documents You’ll Need to Gather

The efficiency and accuracy of your tax submission largely depend on the completeness and organization of your financial documents. Beginning the process of gathering these materials well before the filing window opens can alleviate stress and prevent errors.

Income Statements (W-2s, 1099s)

The foundation of any tax return is accurate reporting of income. For most employees, this means obtaining a Form W-2, Wage and Tax Statement, from each employer. Employers are required to send W-2s to employees by January 31st. These forms detail your annual wages and the amount of federal, state, and local taxes withheld.

For independent contractors, freelancers, or those with significant investment income, Form 1099 is crucial. There are several variations:

- Form 1099-NEC (Nonemployee Compensation) for self-employment income.

- Form 1099-MISC (Miscellaneous Income) for rental income, prizes, or certain other income.

- Form 1099-INT (Interest Income) for interest earned from banks or other financial institutions.

- Form 1099-DIV (Dividends and Distributions) for dividends and capital gain distributions from investments.

- Form 1099-B (Proceeds From Broker and Barter Exchange Transactions) for sales of stocks, bonds, or other securities.

- Form 1099-R (Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.) for retirement account distributions.

These forms are generally issued by January 31st or mid-February, depending on the type. Without accurate income reporting, the entire return can be compromised, leading to audits or penalties.

Deduction and Credit Supporting Documents

Beyond income, many taxpayers can reduce their tax liability through deductions and credits. Supporting documentation is essential to substantiate these claims. This includes:

- Mortgage Interest Statement (Form 1098): For homeowners deducting mortgage interest.

- Student Loan Interest Statement (Form 1098-E): For those deducting student loan interest.

- Records of Charitable Contributions: Receipts or acknowledgment letters for cash and non-cash donations.

- Medical Expense Records: Bills, receipts, and insurance statements for substantial out-of-pocket medical costs.

- Property Tax Statements: For those itemizing deductions.

- Childcare Expense Records: Including the provider’s EIN or Social Security number for claiming the Child and Dependent Care Credit.

- Educational Expense Statements (Form 1098-T): For claiming education credits like the American Opportunity Tax Credit or Lifetime Learning Credit.

Organizing these documents systematically throughout the year, perhaps in a dedicated digital or physical folder, streamlines the tax preparation process significantly.

Previous Year’s Tax Returns

Your prior year’s tax return is a valuable resource. It provides a blueprint of your income, deductions, and credits from the previous period, which can serve as a guide for the current year. It’s also necessary if you need to access specific carryovers, such as capital loss carryovers or net operating loss carryovers. Furthermore, if you’re using tax software for the first time or switching providers, your previous year’s Adjusted Gross Income (AGI) may be required for electronic filing validation. Keeping at least three years of past tax returns, along with all supporting documentation, is a prudent financial practice.

Early Bird vs. Last-Minute Filers: Pros and Cons

Taxpayers typically fall into one of two camps: those who file as soon as the window opens and those who wait until the eleventh hour. Both approaches have distinct financial implications.

Advantages of Early Filing

Filing your taxes early, especially if you anticipate a refund, is often a financially savvy move. The sooner you file, the sooner you receive your refund, which can be put to immediate use, such as paying down debt, boosting savings, or making investments. Early filing also offers peace of mind and reduces the stress associated with the looming deadline. Perhaps more importantly, it provides a buffer against potential issues. If there are errors, missing documents, or if you need to consult a tax professional, doing so early allows ample time to resolve these matters without incurring late penalties. Early filers are also often less susceptible to identity theft related to fraudulent tax filings, as a scammer cannot file a return under your name if you have already submitted a valid one.

Potential Downsides of Rushing

While early filing has benefits, rushing the process can be detrimental. Submitting your return before receiving all necessary documents (e.g., a late W-2 or a corrected 1099) will necessitate an amended return (Form 1040-X), which can be time-consuming and delay any refund or finalization of your tax liability. It’s crucial to ensure you have all information before hitting submit, even if that means waiting a few extra days or weeks into the filing period. Premature filing based on incomplete data is a common mistake that can create more work and potential financial headaches later on.

The Benefits of Strategic Timing

The most financially prudent approach often lies in a balanced strategy. Aim to gather all your documents by mid-February, giving yourself a few weeks to review, prepare, and double-check your return before the April 15th deadline. This allows for the benefits of early filing (peace of mind, quick refunds) without the risks of rushing. If you owe taxes, filing early allows you to know your obligation and plan your payment by April 15th, potentially avoiding interest or penalties. If you’re a complex filer or self-employed, using the early part of the tax season to consult with a financial advisor or tax professional can ensure accuracy and uncover all applicable deductions and credits, optimizing your financial outcome.

What Happens If You Can’t File on Time?

Life happens, and sometimes, despite best intentions, meeting the April 15th deadline isn’t feasible. Understanding your options and the consequences is crucial for managing your financial obligations effectively.

Requesting an Extension

If you need more time to prepare your federal income tax return, you can request an extension using Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. This grants you an automatic six-month extension to file, typically moving your deadline to October 15th. It’s important to understand that an extension to file is not an extension to pay. If you anticipate owing taxes, you must estimate your tax liability and pay any due taxes by the original April 15th deadline to avoid penalties and interest. Failure to pay by the original deadline, even with an extension to file, can still result in financial penalties. Many tax software programs and tax professionals can help you file for an extension quickly and easily.

Penalties for Late Filing vs. Late Payment

The IRS imposes different penalties for late filing and late payment, and it’s essential to distinguish between them.

- Failure to File Penalty: This is typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid taxes. If you file more than 60 days late, the minimum penalty is $485 (for 2024, indexed for inflation) or 100% of the tax due, whichever is smaller.

- Failure to Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25% of your unpaid taxes.

- Interest: In addition to penalties, the IRS charges interest on underpayments and unpaid taxes from the original due date until the payment date. The interest rate can change quarterly.

It’s possible to face both penalties simultaneously. However, if you have a valid extension to file and pay at least 90% of your tax liability by the original due date, the failure-to-pay penalty may not apply. If you are due a refund, there is no penalty for failing to file on time, but you risk losing your refund if you don’t file within three years.

Special Circumstances for Extensions

The IRS provides special filing extensions for certain taxpayers, often without needing to file Form 4868. These include:

- Members of the Military and Support Personnel in Combat Zones: They typically have an automatic extension to file and pay taxes, generally 180 days after leaving a combat zone.

- Taxpayers in Federally Declared Disaster Areas: The IRS may postpone tax deadlines for those affected by natural disasters. Information on specific relief is usually announced after a disaster declaration.

- U.S. Citizens and Resident Aliens Living and Working Abroad: If you live outside the U.S. and Puerto Rico, you generally get an automatic two-month extension to file, making your deadline June 15th. However, interest still applies from April 15th on any unpaid taxes.

Optimizing Your Tax Filing Process

Beyond meeting deadlines, strategically approaching your tax filing can lead to significant financial advantages. It’s an opportunity to review your financial health and plan for future tax efficiency.

Choosing the Right Filing Method (Software, Professional)

The method you choose for preparing and filing your taxes can greatly impact accuracy, cost, and peace of mind.

- Tax Software: Options like TurboTax, H&R Block, and TaxAct offer user-friendly interfaces that guide you through the process, often integrating with financial institutions to import data. This is cost-effective for straightforward returns and empowers you with direct control. Most software also offers e-filing directly with the IRS and state tax agencies.

- Professional Tax Preparer: For complex financial situations (e.g., self-employment with varied income streams, extensive investments, real estate transactions, or major life changes), a certified public accountant (CPA) or enrolled agent (EA) can be invaluable. Professionals can identify overlooked deductions, ensure compliance, and provide strategic advice, potentially saving you more than their fees.

- IRS Free File Program: For taxpayers whose Adjusted Gross Income (AGI) falls below a certain threshold (e.g., $79,000 for 2023 taxes), the IRS offers Free File, a partnership with tax software companies that provides free federal tax preparation and e-filing. This is a powerful financial tool for eligible individuals.

Planning for Next Year

Tax planning is an ongoing process, not just an annual event. As you prepare your current year’s return, take notes on what worked well, what challenges you faced, and any changes in your financial situation that might impact next year’s taxes.

- Adjust Withholding: If you received a large refund, it means you overpaid taxes throughout the year. While a refund feels good, it’s essentially an interest-free loan to the government. Consider adjusting your W-4 with your employer to have less tax withheld, increasing your take-home pay throughout the year, which you can then save or invest. Conversely, if you owed a significant amount, you might need to increase your withholding or make estimated tax payments.

- Tax-Advantaged Accounts: Plan contributions to 401(k)s, IRAs, Health Savings Accounts (HSAs), and 529 plans. These accounts offer significant tax benefits, reducing your taxable income now or providing tax-free growth later.

- Major Life Events: Anticipate how events like marriage, divorce, birth of a child, home purchase, or starting a business will affect your tax situation. Proactive planning can maximize benefits and avoid surprises.

Leveraging Financial Tools for Tax Prep

Modern financial tools can dramatically simplify tax preparation.

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), or Personal Capital can categorize spending throughout the year, making it easier to identify deductible expenses.

- Expense Trackers: For freelancers and small business owners, apps designed for expense tracking (e.g., QuickBooks Self-Employed, Expensify) can digitize receipts and generate reports that directly feed into tax software.

- Digital Record Keeping: Cloud storage services (Google Drive, Dropbox, OneDrive) allow you to securely store digital copies of all tax-related documents, making them accessible from anywhere and reducing the risk of loss.

- Investment Tracking Software: Tools that track capital gains and losses can be invaluable for investors, simplifying the complex calculations for Form 8949 and Schedule D.

By understanding the annual tax calendar, preparing meticulously, choosing an appropriate filing strategy, and leveraging modern financial tools, taxpayers can transform the often-dreaded tax season into a structured and financially empowering process. It’s not just about submitting a form; it’s about optimizing your financial health and ensuring compliance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.