Mortgage rates are far more than just a percentage; they are the bedrock upon which homeownership is built, dictating affordability, influencing housing market trends, and impacting the broader economy. For prospective homebuyers, a seemingly small fluctuation in rates can translate into thousands of dollars over the life of a loan, significantly altering monthly payments and purchasing power. For current homeowners, understanding these rates is crucial for refinancing decisions, equity management, and financial planning. Navigating the complex world of mortgage rates requires a keen understanding of their mechanics, the forces that drive them, and their profound implications for personal finance.

Decoding Mortgage Rates: More Than Just a Number

At its core, a mortgage rate is the interest charged by a lender for a home loan, expressed as an annual percentage of the outstanding loan balance. It’s the cost of borrowing money to purchase a property, and it profoundly impacts the total cost of homeownership. This rate is not static; it constantly shifts, responding to a myriad of economic indicators and market forces.

The Basics: What is a Mortgage Rate?

When you take out a mortgage, you’re borrowing a substantial sum of money over an extended period, typically 15 or 30 years. The mortgage rate determines how much extra you’ll pay the lender on top of the principal amount borrowed. A higher rate means higher monthly payments and a greater total cost over the loan’s lifetime. Conversely, a lower rate makes homeownership more accessible and affordable. It’s crucial to distinguish between the nominal interest rate and the Annual Percentage Rate (APR). While the interest rate reflects the cost of borrowing, the APR includes not only the interest rate but also other fees associated with the loan, such as origination fees, discount points, and private mortgage insurance (PMI) if applicable. The APR provides a more comprehensive measure of the true cost of credit.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The two primary types of mortgage rates offer distinct advantages and risks:

- Fixed-Rate Mortgages (FRMs): As the name suggests, the interest rate on a fixed-rate mortgage remains constant for the entire duration of the loan. This provides unparalleled predictability in monthly payments, making budgeting straightforward. Borrowers choosing FRMs are shielded from potential rate increases in the future but will not benefit if market rates fall unless they refinance. This stability is highly attractive to those who value financial certainty, especially in volatile economic environments or when rates are relatively low.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an interest rate that changes periodically after an initial fixed-rate period. Common ARM structures include 5/1, 7/1, or 10/1 ARMs, where the first number indicates the length of the fixed-rate period in years, and the second number denotes how often the rate adjusts thereafter (typically annually). After the initial fixed period, the rate adjusts up or down based on a predetermined index (like the Secured Overnight Financing Rate – SOFR) plus a margin set by the lender. ARMs typically offer lower initial interest rates compared to FRMs, making them appealing for borrowers who plan to sell or refinance before the fixed period ends, or those who anticipate future income growth. However, they carry the risk of significantly higher payments if rates rise. Most ARMs have caps on how much the rate can increase or decrease per adjustment period and over the life of the loan, providing some level of protection.

Key Influencers on Mortgage Rate Movements

Mortgage rates are not set arbitrarily; they are dynamic reflections of complex macroeconomic forces. Understanding these influences is paramount for predicting potential shifts and making informed decisions.

The Federal Reserve and Monetary Policy

While the Federal Reserve does not directly set mortgage rates, its actions profoundly impact them. The Fed influences short-term interest rates through the federal funds rate, which affects banks’ borrowing costs. When the Fed raises its benchmark rate to combat inflation, it generally pushes up other interest rates, including those on mortgages. Conversely, a rate cut or quantitative easing policies designed to stimulate the economy tend to lower mortgage rates. Investors closely watch the Fed’s announcements and projections, as they provide critical signals about future rate trajectories.

Inflation Expectations

Inflation is a primary driver of interest rates across the board, including mortgages. Lenders need to ensure that the return on their loans outpaces the rate at which money loses its purchasing power. If inflation is expected to rise, lenders will demand higher interest rates to compensate for the diminished value of future principal and interest payments. Therefore, strong inflationary pressures typically lead to higher mortgage rates, while expectations of low inflation can help keep rates down.

The 10-Year Treasury Yield

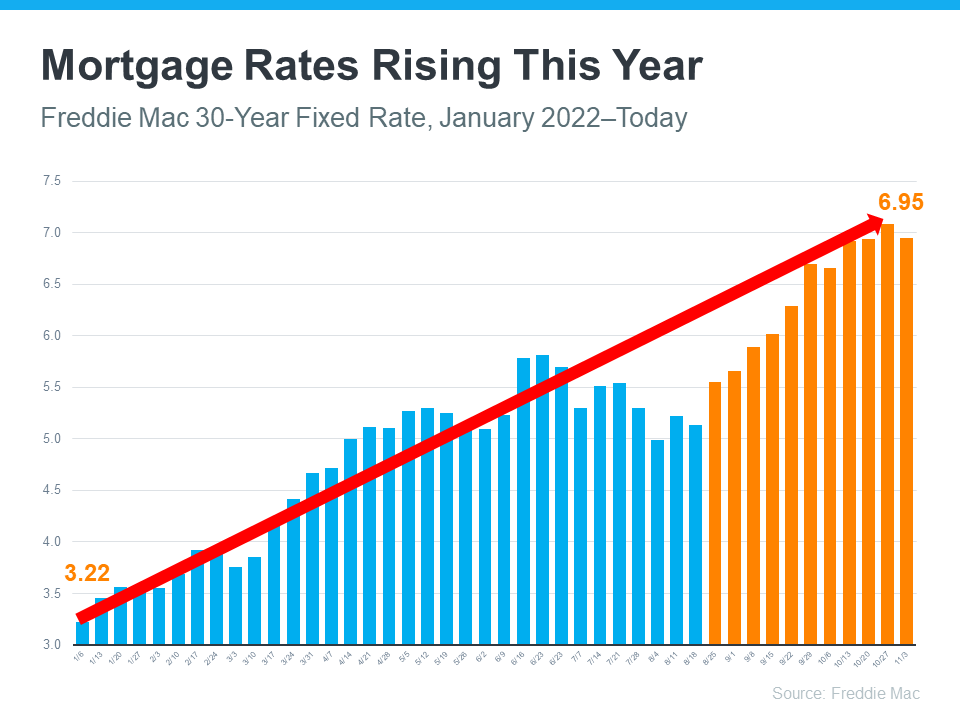

The yield on the 10-year U.S. Treasury bond is a crucial benchmark for fixed-rate mortgages. While not directly correlated, mortgage rates generally move in the same direction as the 10-year Treasury yield. This is because both are long-term fixed-income investments, and investors compare their relative attractiveness. When demand for Treasuries is high (pushing yields down), mortgage rates tend to follow suit. Conversely, when investors sell Treasuries (driving yields up), mortgage rates often rise. Factors like government borrowing, geopolitical events, and global economic sentiment all play a role in shaping Treasury yields.

Economic Growth and Employment Data

A strong economy, characterized by robust GDP growth and low unemployment, often signals higher inflation and potential interest rate hikes from the Federal Reserve. This environment typically leads to higher mortgage rates. Conversely, economic slowdowns or recessions often prompt the Fed to lower rates to stimulate borrowing and investment, which can lead to reduced mortgage rates. Employment reports, consumer confidence indices, and manufacturing data are all closely watched economic indicators that can sway market sentiment and, consequently, mortgage rates.

Lender-Specific Factors and Borrower Profile

Beyond macroeconomic trends, individual lenders and specific borrower characteristics also influence the mortgage rate offered. Lenders have varying overhead costs, profit margins, and risk assessments. Shopping around with multiple lenders is critical to finding the best rate. Furthermore, a borrower’s financial health plays a significant role. Factors like credit score, debt-to-income ratio, loan-to-value (LTV) ratio (the amount borrowed compared to the home’s appraised value), and loan type (e.g., FHA, VA, conventional) all impact the perceived risk to the lender and, by extension, the interest rate offered. A higher credit score and a lower debt-to-income ratio generally qualify borrowers for more favorable rates.

The Tangible Impact of Mortgage Rates

The ebb and flow of mortgage rates have far-reaching consequences, affecting everything from individual household budgets to the overall vitality of the housing market.

Affordability for Homebuyers

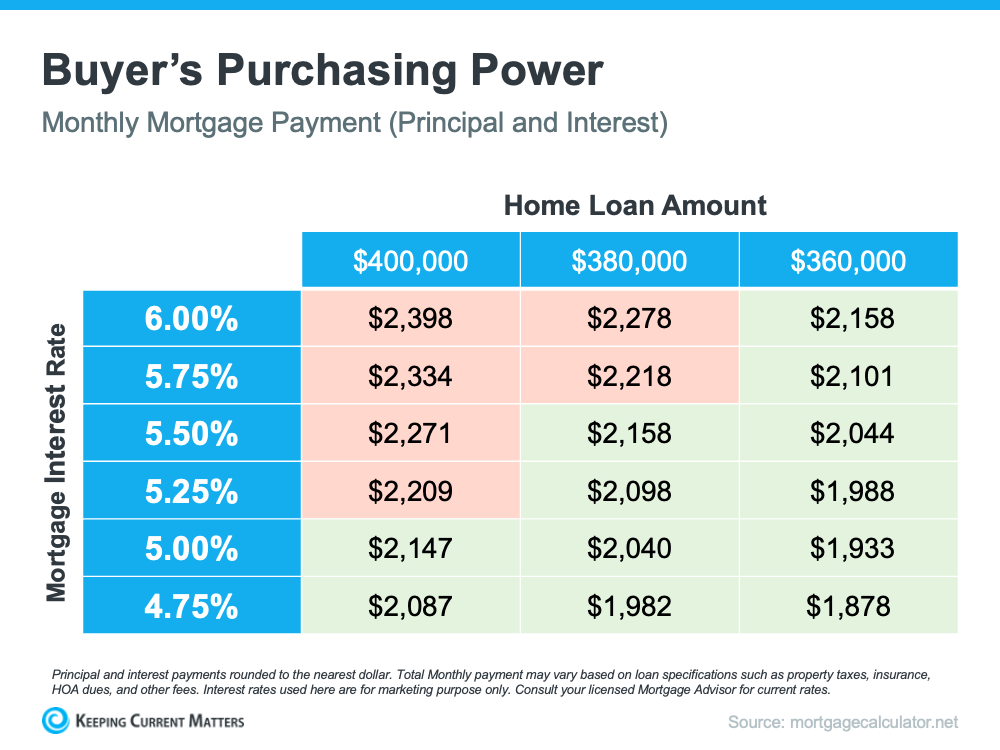

Even a quarter-point change in mortgage rates can significantly impact a homebuyer’s monthly payment and the total cost of a loan over 30 years. When rates rise, the purchasing power of homebuyers diminishes, as the same monthly payment can afford a smaller loan amount. This can price out a segment of potential buyers or force them to consider less expensive properties or save for a larger down payment. Conversely, falling rates make homeownership more accessible, reducing monthly costs and allowing buyers to qualify for larger loans or more desirable homes.

Refinancing Opportunities for Homeowners

Existing homeowners are keenly attuned to mortgage rate movements, primarily for refinancing opportunities. When market rates drop significantly below their current mortgage rate, refinancing can be an attractive option. Refinancing allows homeowners to secure a lower interest rate, which can substantially reduce monthly payments, decrease the total interest paid over the life of the loan, or shorten the loan term. It can also be used to tap into home equity for renovations or debt consolidation, though this involves taking on more debt. However, refinancing comes with closing costs, so homeowners must calculate whether the savings outweigh these upfront expenses.

Impact on Housing Market Dynamics

Mortgage rates are a primary determinant of housing market activity. When rates are low, demand for homes typically surges, as financing becomes more affordable. This increased demand, especially coupled with limited inventory, can drive up home prices. Conversely, rising rates can cool down a hot housing market, as higher borrowing costs reduce demand, potentially leading to fewer sales and a deceleration in price appreciation. Developers and builders also monitor rates closely, as they influence their ability to secure financing for new projects and the ultimate affordability of homes for their customers.

Navigating the Current Rate Environment

Understanding the factors influencing mortgage rates is only half the battle; knowing how to strategically navigate the prevailing rate environment is equally crucial for securing the best possible terms.

The Importance of Shopping Around

One of the most impactful steps a borrower can take is to shop around with multiple lenders. Different banks, credit unions, and mortgage brokers will offer varying rates and terms based on their risk assessment, overheads, and current promotions. Obtaining quotes from at least three to five lenders within a short timeframe (typically 14-45 days to avoid multiple hard inquiries impacting your credit score significantly) allows for direct comparison and negotiation. This simple act can save thousands of dollars over the loan’s life.

Locking Your Rate

Once you’ve received an attractive rate offer, consider a rate lock. A rate lock is a guarantee from the lender that the interest rate offered will be honored for a specified period, typically 30 to 60 days, while your loan application is processed. This protects you from rate increases if market rates rise before your closing. However, if rates fall during your lock period, you might miss out on even lower rates unless your lender offers a “float-down” option, which allows you to secure a lower rate if it drops below a certain threshold.

Improving Your Financial Profile

Before applying for a mortgage, take steps to strengthen your financial standing. A higher credit score (generally above 740 for the best rates) indicates a lower risk to lenders, translating into more favorable interest rates. Reducing existing debt, increasing your down payment, and ensuring a stable income history can also improve your overall borrower profile and lead to better loan terms. Even minor improvements can significantly impact the rate you qualify for.

Considering Rate Buydowns and Points

In certain market conditions, borrowers might consider paying “discount points” to lower their interest rate. One discount point typically costs 1% of the loan amount and can reduce the interest rate by a fraction of a percentage. This is essentially prepaying interest to secure a lower long-term rate. The decision to buy down a rate depends on how long you plan to stay in the home; if you anticipate selling or refinancing within a few years, the cost of the points might not be recouped. Conversely, for long-term homeowners, buydowns can lead to substantial savings.

Looking Ahead: Future Mortgage Rate Outlook

Predicting future mortgage rates with certainty is impossible, as they are influenced by an intricate web of global and domestic economic factors. However, understanding the current economic landscape and expert consensus can help individuals anticipate potential shifts and plan accordingly.

Economic Projections and Expert Consensus

Market analysts and economists continuously monitor indicators such as inflation trends, Federal Reserve policy statements, employment data, and global economic stability to project future rate movements. Generally, if inflation remains elevated or the economy shows unexpected resilience, the Fed may maintain a hawkish stance, potentially leading to higher or sustained rates. Conversely, signs of a cooling economy or a successful reduction in inflation might prompt the Fed to consider easing monetary policy, which could push mortgage rates downward. Geopolitical events and supply chain disruptions also have the potential to introduce volatility.

Preparing for Volatility

Given the inherent unpredictability of financial markets, borrowers and homeowners should prepare for potential volatility. For those contemplating a home purchase, understanding the “what-if” scenarios for different rate environments is crucial. For current homeowners, regularly reviewing mortgage statements and staying informed about market rates can help identify potential refinancing opportunities or signal the need to accelerate principal payments if rates are expected to rise. Engaging with a trusted financial advisor or mortgage professional can provide personalized insights and strategies tailored to individual financial goals and risk tolerance, ensuring that decisions are well-informed regardless of market fluctuations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.