In the rapidly evolving landscape of personal finance, digital payment applications like Cash App have become indispensable tools for millions. They offer unparalleled convenience for sending, spending, and investing money, blurring the lines between traditional banking and modern technology. Yet, beneath the sleek interfaces and instant transactions lies a crucial question that often puzzles users: “What’s Cash App’s bank name?” Understanding the financial institutions that power these platforms isn’t just about curiosity; it’s fundamental to comprehending how your money is handled, the security measures in place, and how these innovative tools integrate into the broader financial system.

For a financial tool like Cash App, the concept of a single “bank name” can be a bit more complex than with a traditional checking account. Cash App, developed by Block, Inc. (formerly Square, Inc.), is a financial technology (fintech) company, not a bank itself. This distinction is vital. As a fintech, Cash App partners with established, federally insured banks to offer its services, ensuring that user funds are held securely and comply with banking regulations. Delving into these partnerships reveals the intricate mechanics that make your digital wallet function reliably within the robust framework of the U.S. financial system.

The Elusive Bank Identity: Unpacking Cash App’s Banking Partnerships

The question of Cash App’s bank name doesn’t have a single, straightforward answer because, as a fintech, it collaborates with multiple regulated financial institutions to provide its diverse range of services. This partnership model is common among challenger banks and digital wallets, allowing them to innovate rapidly while leveraging the regulatory compliance and infrastructure of traditional banks.

Identifying the Primary Banking Partners

For most users, particularly concerning direct deposits and the routing and account numbers associated with their Cash App account, two key banking partners typically emerge: Sutton Bank and Lincoln Savings Bank.

- Sutton Bank: Based in Attica, Ohio, Sutton Bank is a state-chartered bank that often serves as the issuing bank for Cash App’s debit cards (the “Cash Card”). When you receive a Cash Card, its association with Sutton Bank allows it to function within the Visa network, enabling you to spend your Cash App balance wherever Visa is accepted. For many standard Cash App accounts, especially those primarily used for peer-to-peer transfers and card spending, Sutton Bank plays a significant role in facilitating these transactions.

- Lincoln Savings Bank: Located in Reinbeck, Iowa, Lincoln Savings Bank is another crucial partner. This institution is frequently associated with the routing and account numbers provided to Cash App users for direct deposits. When you set up direct deposit to your Cash App account for paychecks or government benefits, the funds are routed through Lincoln Savings Bank before appearing in your Cash App balance. This partnership provides the underlying traditional banking infrastructure necessary for these fundamental financial transactions.

It’s important to note that the specific bank associated with your Cash App account can sometimes vary based on the service you’re using or even the timing, as fintech partnerships can evolve. However, Sutton Bank and Lincoln Savings Bank are the most commonly cited and directly relevant partners for the majority of Cash App users.

The Role of Multiple Banking Partners

The use of multiple banking partners isn’t a sign of obfuscation but rather a strategic operational choice. Each partner may specialize in different aspects of the financial services Cash App offers.

- Diverse Service Offerings: One bank might be better equipped to handle card issuance and transaction processing (like Sutton Bank for the Cash Card), while another might excel in managing ACH transfers and direct deposits (like Lincoln Savings Bank). This specialization allows Cash App to optimize its services and scale its operations efficiently.

- Regulatory Compliance: Partnering with multiple banks helps Cash App navigate the complex regulatory landscape. Each partner bank is a regulated entity, bringing its own compliance infrastructure to the table, which is essential for consumer protection and financial stability.

- Risk Management: Distributing financial operations across several partners can also be a form of risk management, ensuring redundancy and resilience in service delivery.

Ultimately, while Cash App acts as the user-facing interface, these banking partners provide the crucial, regulated financial plumbing that allows your money to move securely and legally within the banking system.

More Than Just a Bank Account: Understanding Cash App’s Financial Structure

To truly grasp what Cash App is and how it functions, it’s essential to understand that it operates as a fintech platform layered on top of traditional banking infrastructure, rather than being a bank in the conventional sense. This hybrid model offers unique advantages but also requires users to understand how their funds are managed.

Fintech vs. Traditional Banking: A Hybrid Model

Traditional banks operate under strict charters and regulations, directly holding customer deposits, issuing loans, and providing a full suite of financial services. Fintech companies like Cash App, on the other hand, leverage technology to deliver specific financial services, often more efficiently or conveniently, but they typically do not hold a banking charter themselves.

Cash App’s hybrid model means:

- Innovation at the Forefront: Cash App can rapidly develop and deploy new features, like instant transfers, Bitcoin trading, or stock investing, without the bureaucratic hurdles often faced by large traditional banks.

- Leveraging Existing Infrastructure: By partnering with FDIC-insured banks, Cash App provides users with the security and regulatory compliance of traditional banking without having to build and maintain an entire banking infrastructure from scratch. This allows Cash App to focus on user experience and digital features.

- Simplified Access: For many users, especially those underserved by traditional banking or seeking a more streamlined digital experience, Cash App offers an accessible gateway to financial services.

The Importance of a Routing Number and Account Number

For Cash App users, the most tangible evidence of its banking partnerships comes in the form of a routing number and an account number. These are the standard identifiers used in the U.S. banking system to facilitate electronic funds transfers (EFTs), such as direct deposits.

- Routing Number: This nine-digit code identifies the financial institution (the bank) responsible for receiving or sending a payment. When you use Cash App for direct deposit, the routing number provided will correspond to one of its partner banks, typically Lincoln Savings Bank.

- Account Number: This unique number identifies your specific account within that financial institution. While your Cash App balance is what you see in the app, the underlying account number provided for direct deposits links to an account managed by the partner bank, holding funds associated with your Cash App profile.

These numbers are crucial for integrating Cash App into your broader financial life, allowing employers to deposit your paycheck directly or government agencies to send benefits to your Cash App balance.

How Cash App Facilitates Direct Deposits and Withdrawals

The process of direct deposits and withdrawals through Cash App beautifully illustrates its hybrid financial structure:

- Direct Deposits: When an employer initiates a direct deposit to your Cash App account, they use the routing and account numbers provided by Cash App (which belong to a partner bank like Lincoln Savings Bank). The funds are sent to this partner bank. The partner bank then communicates with Cash App, which credits your Cash App balance, making the funds available to you within the app.

- Withdrawals/Spending: When you use your Cash Card, transfer funds to another bank account, or withdraw cash from an ATM, Cash App debits your in-app balance. The actual movement of funds through the traditional banking system is facilitated by its banking partners (e.g., Sutton Bank for Cash Card transactions, or ACH transfers processed through a partner bank for transfers out to external bank accounts).

This seamless operation gives users the impression of a bank account directly within Cash App, even though multiple entities are working behind the scenes.

Security, Regulations, and Your Money: What Knowing the Bank Means for Users

Understanding Cash App’s banking partners is not merely academic; it has direct implications for the security of your funds, regulatory protections, and how you manage your money effectively within the digital realm.

FDIC Insurance: Protecting Your Funds

One of the most significant benefits of Cash App partnering with traditional banks is the availability of FDIC (Federal Deposit Insurance Corporation) insurance. The FDIC is an independent agency of the U.S. government that protects bank depositors in the event of a bank failure.

- How it Applies: Because Cash App’s partner banks (like Sutton Bank and Lincoln Savings Bank) are FDIC-insured institutions, funds held by these banks for Cash App users are typically eligible for FDIC pass-through insurance up to the standard maximum deposit insurance amount ($250,000 per depositor, per insured bank, for each account ownership category).

- Important Nuance: It’s crucial to confirm how this insurance applies to your specific Cash App balance. While the underlying funds are held at an FDIC-insured bank, the exact nature of the relationship (e.g., if funds are held in a pooled account for multiple Cash App users) means you should always refer to Cash App’s official terms and conditions or contact their support for precise details on how your funds are protected. However, the general principle is that the funds held by the partner bank on your behalf are indeed covered.

This insurance provides a critical layer of security, assuring users that their money is protected even if one of the partner banks were to fail.

Regulatory Oversight and Consumer Protection

Cash App’s partnerships also bring it under the umbrella of banking regulations designed to protect consumers. While Cash App itself is regulated by various state money transmission laws, its banking partners are subject to oversight by federal and state banking authorities, including:

- OCC (Office of the Comptroller of the Currency): For national banks.

- State Banking Departments: For state-chartered banks.

- Federal Reserve: Oversees state-chartered banks that are members of the Federal Reserve System.

- CFPB (Consumer Financial Protection Bureau): Protects consumers in the financial marketplace.

This multi-layered regulatory environment ensures that operations like anti-money laundering (AML), know-your-customer (KYC) compliance, and other consumer protection measures are adhered to, adding legitimacy and security to your Cash App transactions.

Understanding Transaction Limits and Security Measures

While Cash App offers incredible flexibility, it also implements transaction limits and security measures, partly driven by regulatory requirements and partly by its own risk management strategies.

- Limits: Daily or weekly limits on sending, receiving, or withdrawing funds are common. These limits can often be increased by verifying your identity (providing your full name, date of birth, and the last four digits of your SSN), which is a KYC requirement mandated by banking regulations to prevent fraud and money laundering.

- Security: Cash App employs robust security features, including encryption, fraud detection technology, and the ability to enable security locks (PIN, fingerprint, or Face ID) for transactions. These measures, combined with the security protocols of its banking partners, work in tandem to protect your account and funds from unauthorized access.

Being aware of these limits and actively utilizing the available security features is crucial for responsible financial management within the Cash App ecosystem.

Optimizing Your Financial Experience with Cash App

Leveraging Cash App effectively as a financial tool goes beyond simply sending and receiving money. Understanding its underlying structure allows you to integrate it more strategically into your personal finance routine.

Setting Up Direct Deposit: A Step-by-Step Guide

Direct deposit is one of Cash App’s most powerful features, allowing you to receive paychecks, tax refunds, and government benefits directly into your account.

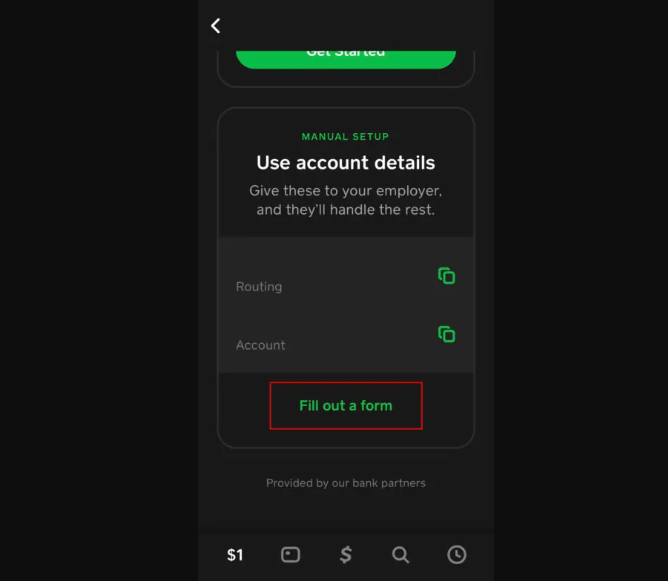

- Access Account & Routing Numbers: In the Cash App, tap the banking tab (the house icon). Scroll down and tap on “Direct Deposit.” You’ll find your Cash App routing number and account number.

- Provide to Payer: Give these details to your employer’s payroll department, government agency, or benefit provider. You might need to fill out a direct deposit form, which can often be found or printed directly from the Cash App.

- Confirm Deposit: Once set up, funds will typically arrive on your payday, often up to two days earlier than traditional bank deposits, depending on your employer’s payroll process.

Setting up direct deposit not only streamlines income receipt but also often unlocks higher transaction limits within the app.

Managing Your Cash App Balance and Transfers

Effectively managing your Cash App balance involves understanding its capabilities and limitations.

- Funding Your Account: Beyond direct deposit, you can add money to your Cash App balance by linking a debit card or bank account and initiating transfers, or by receiving money from other Cash App users.

- Spending Options: Use your Cash Card anywhere Visa debit cards are accepted, make online purchases, or send money to friends and family instantly.

- Transferring Out: You can transfer your Cash App balance to a linked bank account. Standard transfers are free but take 1-3 business days, while instant transfers incur a small fee but are available immediately.

- Investing: Cash App also allows you to buy and sell Bitcoin and invest in stocks, further diversifying its utility as a financial tool. These investment features operate under separate regulatory frameworks and are not typically covered by FDIC insurance.

Integrating Cash App into Your Personal Finance Strategy

For many, Cash App isn’t just a peer-to-peer payment app; it’s an integral part of their financial ecosystem.

- Budgeting: Use it for specific spending categories, like discretionary spending, separate from your primary bank account.

- Emergency Funds (Small Scale): For minor emergencies or immediate needs, its quick accessibility can be beneficial.

- Allowance Management: An excellent tool for managing allowances for family members or shared expenses with housemates.

- Financial Inclusion: For individuals who may not have traditional bank accounts, Cash App (with its direct deposit and Cash Card features) can serve as a vital entry point into the digital financial system.

By understanding how Cash App partners with banks and offers regulated services, users can make informed decisions about how to best incorporate this powerful tool into their overall personal finance strategy.

The Future of Digital Banking: Cash App’s Role in a Shifting Landscape

Cash App’s model of leveraging banking partnerships to deliver a seamless digital experience is indicative of a larger trend reshaping the financial industry. The distinction between “banks” and “fintechs” continues to evolve, promising a future of more integrated and user-centric financial services.

The Rise of Neobanks and Fintech Innovations

Cash App is part of a broader movement of neobanks and fintech companies that are challenging traditional banking models. These digital-first entities prioritize user experience, mobile accessibility, and innovative features, often at lower costs than incumbent banks. Their success hinges on understanding consumer needs and delivering solutions that leverage technology to overcome the limitations of legacy systems. The partnership model allows them to scale rapidly while adhering to necessary financial regulations.

Bridging the Gap: Traditional Banks and Digital Wallets

The ecosystem is not one of pure competition but often one of collaboration. Traditional banks are increasingly recognizing the value of fintech innovation, either by developing their own digital solutions or by partnering with successful fintechs. Digital wallets like Cash App are, in essence, bridging the gap between established financial infrastructure and the demand for instant, mobile-first financial interactions. They provide a vital conduit for moving money within and outside the traditional banking system.

What’s Next for Digital Payments and Financial Inclusion

The ongoing evolution promises further advancements in:

- Real-time Payments: Faster, more ubiquitous instant payment systems are becoming the norm, driven by consumer demand and technological capabilities.

- Embedded Finance: Financial services will become increasingly integrated into non-financial platforms and apps, making them almost invisible and seamlessly part of daily activities.

- Financial Inclusion: Digital wallets and fintechs are playing a critical role in bringing financial services to underserved populations globally, offering access to tools like direct deposit, digital payments, and micro-investing where traditional banking might be inaccessible or too costly.

In conclusion, while Cash App may not be a bank in the traditional sense, its deep partnerships with regulated institutions like Sutton Bank and Lincoln Savings Bank provide the robust financial backbone necessary for its innovative services. For users, understanding these relationships is key to appreciating the security, regulatory compliance, and strategic potential of this powerful digital financial tool within the ever-evolving landscape of personal finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.