In the realm of personal finance, few acronyms carry as much weight—or cause as much confusion—as APR. Standing for Annual Percentage Rate, APR is the standard metric used to express the true cost of borrowing money. Whether you are applying for a credit card, financing a new vehicle, or signing the closing papers on a home mortgage, the APR attached to your loan will dictate your monthly payments and the total amount you repay over the life of the debt.

Determining what constitutes a “good” APR is not a one-size-fits-all answer. A rate that is considered excellent for a credit card would be predatory for a mortgage, and a competitive rate for an auto loan might be unattainable for someone with a developing credit history. To navigate the financial landscape effectively, one must understand the benchmarks for different financial products and the variables that influence the rates lenders offer.

Understanding the Fundamentals: What APR Really Means

Before assessing what makes a rate “good,” it is essential to define what an APR actually represents. Unlike a simple interest rate, the APR is designed to provide a more holistic view of the cost of credit. It includes the interest rate plus any additional fees or costs associated with the loan, such as origination fees, mortgage insurance, or points.

The Difference Between Interest Rate and APR

The interest rate is the percentage of the principal balance that the lender charges you for borrowing the funds. However, borrowing often involves “hidden” costs. For example, in a mortgage, you might pay closing costs or loan processing fees. The APR folds these costs back into the percentage, providing a standardized “shop-able” number. When comparing two loans, the one with the lower interest rate isn’t always the cheapest; the one with the lower APR generally is, as it accounts for the total expense.

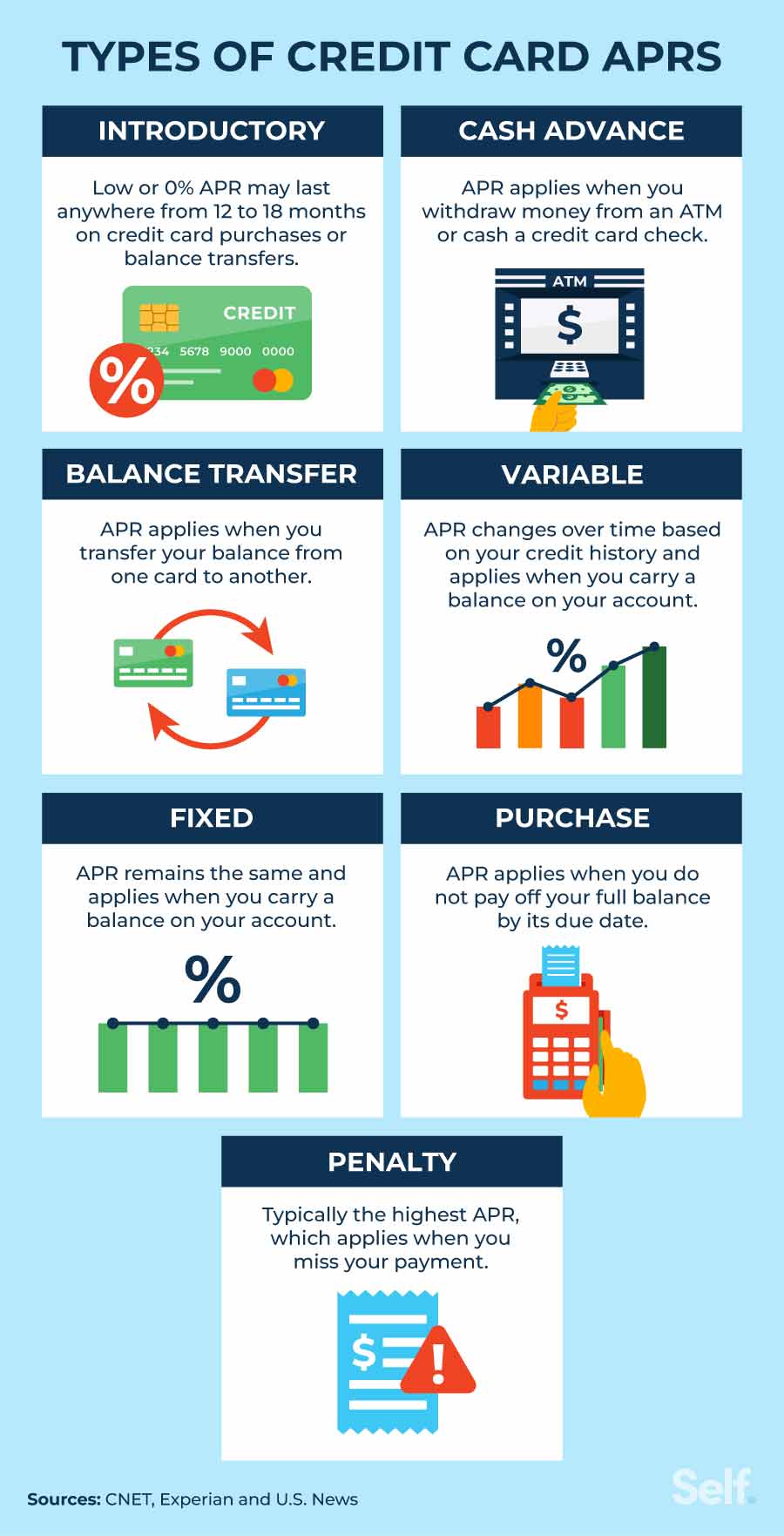

Fixed vs. Variable APR

Another critical distinction is whether the APR is fixed or variable. A fixed APR remains constant throughout the term of the loan, providing predictability for your budget. These are common in mortgages and personal loans. A variable APR, however, is tied to an index (such as the U.S. Prime Rate). When the index moves up or down based on Federal Reserve policy, your APR follows suit. Most credit cards utilize variable APRs, meaning your cost of debt can increase even if your financial behavior remains unchanged.

Nominal vs. Effective APR

While most consumers only deal with the nominal APR (the rate stated by the lender), it is worth noting the effective APR, which accounts for the effects of compounding interest. On credit cards, interest often compounds daily. While the APR is expressed annually, the actual interest you pay over a year might be slightly higher than the stated APR because of this compounding effect.

Benchmarking a “Good” APR Across Different Financial Products

Because different types of loans carry different levels of risk for the lender, a “good” APR varies significantly by category. To know if you are getting a fair deal, you must compare your offer against the current national averages and the specific product type.

Credit Card APRs

Credit cards typically have the highest APRs because they represent “unsecured” debt—there is no collateral (like a house or car) for the lender to seize if you default.

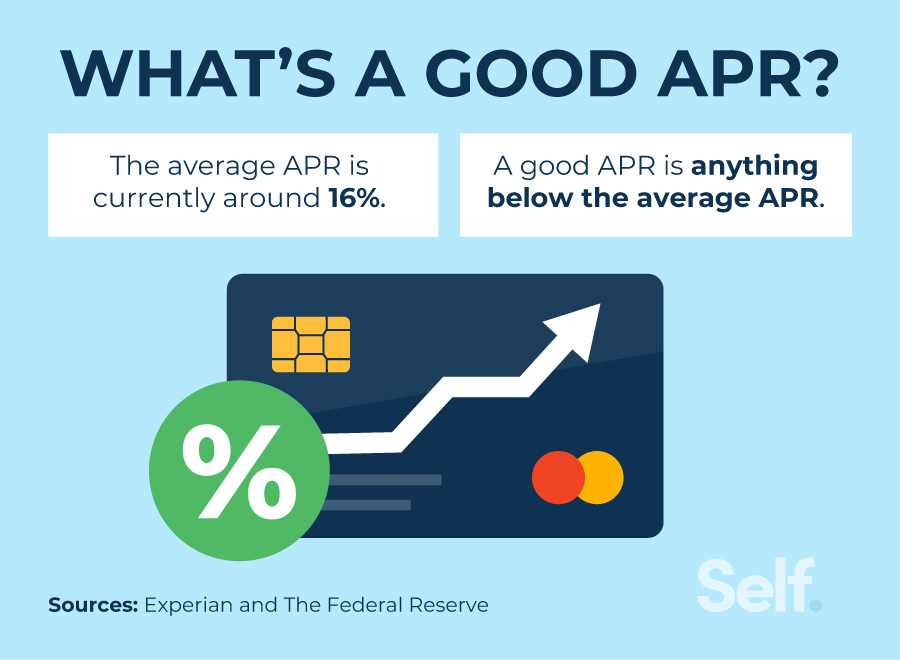

- Average Rate: As of mid-2024, the average credit card APR in the United States hovers between 21% and 25%.

- What is “Good”: An APR below 18% is generally considered good in the current economic climate. For those with excellent credit, “low-interest” cards might offer rates between 13% and 15%.

- The 0% Exception: The best possible APR is 0%. Many lenders offer introductory 0% APR periods for 12 to 21 months on new purchases or balance transfers. For a savvy consumer, this is the gold standard of “good.”

Mortgage Rates

Mortgages are secured by the property itself, making them lower risk for lenders and thus offering much lower APRs than credit cards.

- Current Climate: After a decade of historic lows, mortgage rates have climbed. A “good” rate today is vastly different from a “good” rate in 2021.

- What is “Good”: If the national average for a 30-year fixed mortgage is 7%, an APR of 6.5% to 6.75% would be considered excellent. Because mortgages involve hundreds of thousands of dollars, even a 0.25% difference in APR can save you tens of thousands of dollars over 30 years.

Auto Loans and Personal Loans

Auto loans are secured by the vehicle, while personal loans can be either secured or unsecured.

- Auto Loans: For a new car, a good APR for a borrower with excellent credit typically ranges from 5% to 8%. Used car rates are usually 1% to 3% higher.

- Personal Loans: These are often used for debt consolidation. A good APR here is anything significantly lower than the interest on the debt you are consolidating. Typically, rates between 8% and 12% are considered good for those with strong credit.

Factors That Influence Your Personal APR

Lenders do not hand out the same APR to everyone. They use a process called “risk-based pricing” to determine how much to charge you. Understanding these factors can help you predict what kind of rate you will be offered.

The Power of the Credit Score

Your credit score is the single most influential factor in determining your APR. It serves as a shorthand for your financial reliability.

- Excellent (740-850): Borrowers in this tier receive the “prime” rates—the lowest APRs advertised by banks.

- Good (670-739): Borrowers will likely be approved for most loans but may pay 1% to 3% more in interest than those in the excellent tier.

- Fair to Poor (Below 670): These borrowers are considered high-risk. They may face “subprime” rates, which can be double or triple the rates offered to prime borrowers.

Debt-to-Income Ratio (DTI)

Even if you have a perfect credit score, a lender may give you a higher APR (or deny your application) if you are already overleveraged. Your DTI is the percentage of your gross monthly income that goes toward paying debts. Lenders prefer a DTI below 36%. A high DTI signals to the lender that you might struggle to make payments, prompting them to charge a higher APR to compensate for that risk.

Economic Conditions and the Federal Reserve

The “Floor” of all APRs is set by the Federal Open Market Committee (FOMC). When the Federal Reserve raises the federal funds rate to combat inflation, the cost for banks to borrow money increases. To maintain their margins, banks pass these costs on to consumers. Therefore, a “good” APR is always relative to the current federal interest rate environment.

Strategies to Secure a Lower APR

If you find that the APRs you are being offered are higher than the “good” benchmarks, there are proactive steps you can take to lower your cost of borrowing.

Optimize Your Credit Profile

Before applying for a major loan, take six months to polish your credit report. Pay down existing credit card balances to lower your credit utilization ratio (ideally below 10%). Ensure there are no errors on your report. Even a 20-point bump in your score can move you into a different pricing tier, potentially saving you thousands in interest.

The Art of Shopping Around

Many consumers take the first loan offer they receive, often from their primary bank or a dealership. However, APRs can vary wildly between institutions. Online banks, credit unions, and local community banks often have different overhead costs and risk tolerances. For mortgages and auto loans, “rate shopping” within a 14-to-45-day window typically counts as a single inquiry on your credit report, allowing you to compare multiple offers without damaging your score.

Negotiation and Refinancing

For existing debt, the APR isn’t necessarily permanent. If your credit score has improved since you took out a loan, you can explore refinancing. This is particularly common with mortgages and auto loans. For credit cards, a simple phone call to the issuer requesting a lower rate can sometimes yield results, especially if you have a long history of on-time payments and have received better “pre-approved” offers from competitors.

Leveraging Collateral

If you are struggling to get a good APR on a personal loan, consider a secured loan. By backing the loan with a savings account, CD, or vehicle title, you reduce the lender’s risk, which almost always results in a lower APR compared to an unsecured signature loan.

Conclusion: The Long-Term Impact of a Good APR

Understanding “what’s a good APR” is more than an academic exercise; it is a fundamental pillar of wealth building. Every dollar you spend on interest is a dollar that isn’t being invested in your retirement, your education, or your home equity.

A “good” APR is ultimately one that aligns with the current market, rewards you for your financial discipline, and fits within a sustainable budget. By monitoring market trends, maintaining a robust credit score, and refusing to settle for the first offer on the table, you can minimize the cost of debt and maximize your financial freedom. In the world of personal finance, the APR is the price of admission for using someone else’s money—make sure you aren’t paying a premium.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.