For many individuals, the dream of owning a car is synonymous with freedom, convenience, and a significant milestone in personal independence. However, achieving this dream often involves navigating the world of auto financing, and one term frequently encountered is “car note.” Far more than just a casual phrase, understanding “what’s a car note” is fundamental to responsible vehicle ownership and sound personal finance. In its simplest form, a car note refers to the monthly payment you make towards an auto loan, or more broadly, the loan agreement itself that finances the purchase of a vehicle. It represents a contractual obligation to repay a borrowed sum, plus interest, over a predetermined period.

A car note is often one of the largest recurring expenses in a household budget, second only to housing for many. Its implications extend beyond the mere act of paying a bill; it impacts your credit score, dictates your disposable income, and influences your overall financial stability. Diving into the intricacies of car notes empowers consumers to make informed decisions, secure favorable terms, and ultimately manage their finances with greater confidence and control. This article will deconstruct the car note, guiding you through its components, the acquisition process, effective management strategies, and its broader financial implications, all within the strict confines of the Money niche.

Deconstructing the Car Note: The Basics of Auto Loans

To truly grasp what a car note entails, it’s essential to understand the fundamental mechanics of an auto loan. At its core, an auto loan is a secured loan, meaning the car itself acts as collateral. If you fail to make payments, the lender has the right to repossess the vehicle to recover their losses. This structure is common in large purchases and impacts both the lender’s risk and the borrower’s responsibilities.

The Anatomy of a Car Loan: Principal, Interest, Term

Every car loan is comprised of three primary components that dictate the size and duration of your car note:

- Principal: This is the initial amount of money you borrow to purchase the car. It is the actual price of the vehicle, less any down payment or trade-in value. The higher the principal, the larger your monthly payments will generally be, assuming all other factors remain constant. Managing the principal starts with negotiating a good vehicle price and making a substantial down payment.

- Interest: This is the cost of borrowing money from the lender, expressed as an annual percentage rate (APR). It’s the profit margin for the lender and a significant factor in your total repayment amount. A higher interest rate means a larger portion of your monthly payment goes towards interest, especially in the early stages of the loan. Factors like your credit score, the loan term, and market conditions heavily influence the interest rate you’re offered.

- Term: Also known as the loan duration, this is the length of time, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months), over which you agree to repay the loan. A longer term generally results in lower monthly payments, making the car more “affordable” on a month-to-month basis. However, a longer term also means you’ll pay more in total interest over the life of the loan and the car will depreciate further before it’s paid off, potentially leading to a situation where you owe more than the car is worth (being “upside down” or having negative equity). Conversely, a shorter term leads to higher monthly payments but less total interest paid and quicker equity build-up.

Fixed vs. Variable Interest Rates

While less common for standard auto loans, understanding the difference between fixed and variable rates is crucial for any borrower. Most car loans come with a fixed interest rate, meaning the APR remains constant for the entire duration of the loan. This provides stability and predictability, as your monthly principal and interest payment will not change. You know exactly what to expect each month, making budgeting simpler.

Variable interest rates, on the other hand, fluctuate with market indices. While rare for new car purchases, some exotic or specialized financing options might offer them. A variable rate could mean your monthly payment changes, sometimes significantly, making financial planning more challenging. For the vast majority of car buyers, a fixed-rate loan is the standard and preferred option due to its predictable nature.

Key Players in the Car Note Process: Borrower, Lender, Dealership

The journey to securing a car note involves several key participants, each with a distinct role:

- The Borrower: This is you, the individual taking out the loan to purchase the vehicle. Your financial history, creditworthiness, and ability to repay will be scrutinized by lenders.

- The Lender: This is the financial institution providing the funds for the loan. Lenders can be banks, credit unions, or the financing arm of car manufacturers (e.g., Toyota Financial Services, Ford Credit). They assess risk, set interest rates, and dictate loan terms.

- The Dealership: While primarily focused on selling you a car, dealerships often facilitate the loan process. They act as intermediaries, presenting your loan application to various lenders and often adding their own markup to the interest rate offered by the lender (known as dealer reserve). Understanding this dynamic is crucial for effective negotiation.

Navigating the Car Note Process: From Application to Ownership

Securing a car note is not just about signing on the dotted line; it’s a process that begins long before you even step foot on a car lot. Strategic planning and informed decision-making can save you thousands of dollars over the life of your loan.

Pre-Approval vs. Dealership Financing

One of the most powerful tools a car buyer has is loan pre-approval. This involves applying for an auto loan with a bank or credit union before you start shopping for a car.

- Pre-Approval: When you’re pre-approved, a lender provides you with a firm offer for a loan amount and interest rate, typically valid for a certain period (e.g., 30 days). This gives you several advantages:

- Knowing Your Budget: You know exactly how much you can afford, preventing you from falling in love with a car outside your financial reach.

- Negotiation Power: You walk into the dealership as a cash buyer, in essence. The dealer knows you already have financing, which allows you to focus solely on negotiating the car’s price, rather than being swayed by financing schemes. It also provides a benchmark against which to compare any financing offers the dealership might present.

- Reduced Stress: Separating the car negotiation from the loan negotiation simplifies the process and reduces pressure.

- Dealership Financing: While convenient, relying solely on dealership financing can sometimes lead to less favorable terms. Dealerships often have relationships with multiple lenders and can offer various financing options. However, they may also mark up the interest rate to earn a profit. While they can sometimes beat your pre-approval rate, it’s always best to have an outside offer as leverage.

Understanding the Loan Agreement and Fine Print

The auto loan agreement is a legally binding contract, and understanding every clause is paramount. Before signing, carefully review:

- Interest Rate (APR): Confirm it matches what you were offered.

- Loan Term: Ensure the number of months is correct.

- Total Amount Financed: This includes the car’s price, taxes, fees, and any add-ons (like extended warranties or GAP insurance).

- Monthly Payment: Verify the figure.

- Prepayment Penalties: Check if there are any fees for paying off the loan early. Most standard auto loans do not have these, but it’s crucial to confirm.

- Late Payment Penalties: Understand the charges for missed or late payments.

- Other Fees: Look out for administrative fees, document fees, or other charges that might be added to the loan amount.

Never feel rushed or pressured to sign. If you don’t understand something, ask for clarification or take the document home to review it more thoroughly.

The Impact of Credit Score on Your Car Note

Your credit score is arguably the single most influential factor in determining the interest rate you qualify for on a car note. Lenders use your credit score (e.g., FICO score) as a primary indicator of your creditworthiness and the likelihood that you’ll repay the loan.

- Excellent Credit (780+): You’ll typically qualify for the lowest available interest rates, often advertised as “prime” rates, saving you significant money over the loan term.

- Good Credit (670-779): You’ll still get competitive rates, but they might be slightly higher than those with excellent credit.

- Fair Credit (580-669): Expect higher interest rates, as lenders perceive a greater risk.

- Poor Credit (Below 580): Securing a loan can be challenging, and if approved, the interest rates will be very high, potentially making the car unaffordable in the long run.

Before applying for a car note, it’s wise to check your credit report and score. If your score is not ideal, consider taking steps to improve it, such as paying down existing debts or correcting errors on your credit report, before seeking financing. Even a slight improvement in your credit score can translate to thousands of dollars saved in interest.

Down Payments and Trade-Ins

Making a substantial down payment or leveraging a trade-in vehicle can significantly impact your car note.

- Down Payment: This is the initial cash payment you make towards the purchase price of the car. A larger down payment reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also helps build equity in the car faster, reducing the risk of being upside down on the loan. Financial advisors often recommend a down payment of at least 10-20% for new cars and 5-10% for used cars.

- Trade-In: If you have an existing vehicle you wish to sell, trading it in at the dealership allows its value to be applied directly against the price of the new car, effectively acting like a down payment. Ensure you research your trade-in’s value independently (e.g., Kelley Blue Book, Edmunds) before negotiating to ensure you receive a fair offer. In some cases, selling your old car privately might yield more cash than a trade-in, which you can then use as a down payment.

Managing Your Car Note: Strategies for Financial Wellness

Once you’ve secured your car note, the focus shifts to effective management. Responsible repayment not only keeps you in good standing with your lender but also positively impacts your broader financial health.

Making Payments On Time: Avoiding Penalties and Credit Damage

The most fundamental aspect of managing your car note is making your payments on time, every time.

- Impact on Credit Score: Payment history is the largest factor in your credit score (35%). Late payments (typically 30 days or more past due) are reported to credit bureaus and can severely damage your credit score, making it harder and more expensive to obtain future loans (mortgages, personal loans, credit cards).

- Late Fees: Lenders typically charge late fees for overdue payments, adding unnecessary costs to your debt.

- Default and Repossession: Consistent late payments or missed payments can lead to default on your loan, which empowers the lender to repossess your vehicle. This not only results in the loss of your car but also leaves a significant negative mark on your credit report.

To ensure timely payments, consider setting up automatic payments from your bank account or setting calendar reminders a few days before the due date.

Strategies for Early Loan Payoff

Paying off your car note earlier than scheduled can be a smart financial move, saving you a substantial amount in interest and freeing up your monthly cash flow.

- Extra Payments: Even small, consistent extra payments can make a big difference. For instance, paying an extra $50-100 each month, or making one extra full payment per year, can shave months off your loan term and hundreds of dollars off your total interest paid. You can achieve this by making bi-weekly payments (which results in 13 full payments per year) or simply adding an amount to your regular monthly payment.

- Lump Sum Payments: If you receive a bonus, tax refund, or any unexpected windfall, consider applying a portion directly to your loan principal. This immediately reduces the amount on which interest accrues.

- Refinancing: As discussed below, refinancing to a lower interest rate or shorter term can also accelerate your payoff.

Always confirm with your lender that extra payments are being applied directly to the principal and that there are no prepayment penalties.

Refinancing Your Car Note: When and Why

Refinancing an auto loan involves taking out a new loan to pay off your existing car note, usually with a new lender and new terms. This can be a highly effective strategy for financial optimization under certain circumstances:

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower APR, reducing your monthly payment and total interest paid.

- Improved Credit Score: If your credit wasn’t great when you first bought the car but has since improved, refinancing can get you a better rate.

- Changes in Financial Situation:

- To Lower Monthly Payments: If you’re struggling with high monthly payments, extending the loan term through refinancing can reduce your monthly burden (though you’ll pay more interest overall).

- To Shorten the Loan Term: If your financial situation has improved, you might refinance to a shorter term to pay off the car faster and save on interest, even if it means a higher monthly payment.

- Removing a Co-signer: If you initially needed a co-signer but now have strong enough credit to qualify on your own, refinancing can release the co-signer from their obligation.

Before refinancing, compare offers from multiple lenders, understand all associated fees, and calculate whether the savings outweigh the costs of the new loan.

What Happens if You Can’t Pay Your Car Note?

Facing difficulties in making your car payments is a stressful situation, but understanding the potential consequences and available options is crucial.

- Consequences:

- Late Fees: As mentioned, immediate charges.

- Credit Damage: Missed payments severely harm your credit score.

- Default: After a certain period (e.g., 60-90 days of missed payments), your loan will be considered in default.

- Repossession: The lender can legally repossess your car. This will negatively impact your credit for years and may result in additional fees (towing, storage) that you’re still liable for. Even after repossession, if the car is sold for less than what you owe, you could be responsible for the “deficiency balance.”

- Options:

- Contact Your Lender Immediately: Don’t wait until you’ve missed payments. Explain your situation. Lenders might offer options like deferment (postponing payments), forbearance (temporarily reducing payments), or a modified payment plan.

- Sell the Car: If you can’t afford the payments and the car is worth more than you owe, selling it yourself can prevent repossession and minimize credit damage.

- Voluntary Repossession: If you’re certain you can’t make payments, you can voluntarily surrender the vehicle. While still a negative credit event, it might reduce some fees associated with involuntary repossession.

- Budget Adjustment: Re-evaluate your entire budget to see if cuts can be made elsewhere to free up funds for your car payment.

The Broader Financial Implications of a Car Note

A car note is rarely an isolated financial commitment. It integrates with and impacts your overall financial health, necessitating a holistic view of your money management.

Budgeting for Your Car Note: Beyond the Monthly Payment

The car note itself is just one piece of the puzzle when it comes to the true cost of car ownership. Responsible budgeting demands consideration of all associated expenses:

- Insurance: This is a mandatory and often significant monthly cost. Rates vary widely based on your vehicle, driving record, location, and coverage type.

- Fuel: Daily commuting or frequent travel means a recurring expense at the gas pump or charging station.

- Maintenance and Repairs: Cars require regular oil changes, tire rotations, and occasional repairs. Budgeting for these unexpected costs is essential, especially as the car ages.

- Registration and Taxes: Annual vehicle registration fees and potential property taxes on your vehicle are also recurring expenses.

- Depreciation: While not a direct cash outflow, depreciation is the single largest cost of car ownership. A new car typically loses a significant portion of its value in the first few years. Understanding this helps you assess the long-term financial wisdom of your purchase.

When calculating whether you can afford a car, factor in all these elements, not just the car note. A common guideline is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net income.

Opportunity Cost and Debt Management

Every dollar spent on a car note is a dollar that cannot be used for other financial goals. This is the concept of opportunity cost. A large, long-term car note can:

- Delay Savings and Investments: Money tied up in car payments could otherwise be contributing to an emergency fund, retirement accounts, or other investment vehicles.

- Impede Other Debt Repayment: If you have high-interest debts like credit card balances, prioritizing a car note over these can be financially suboptimal.

- Affect Housing Decisions: A high car payment can impact your debt-to-income ratio, potentially making it harder to qualify for a mortgage or limiting the amount you can borrow for a home.

Responsible debt management involves balancing all your financial obligations and prioritizing where your money goes. For many, minimizing debt, including car debt, is a key component of building long-term wealth.

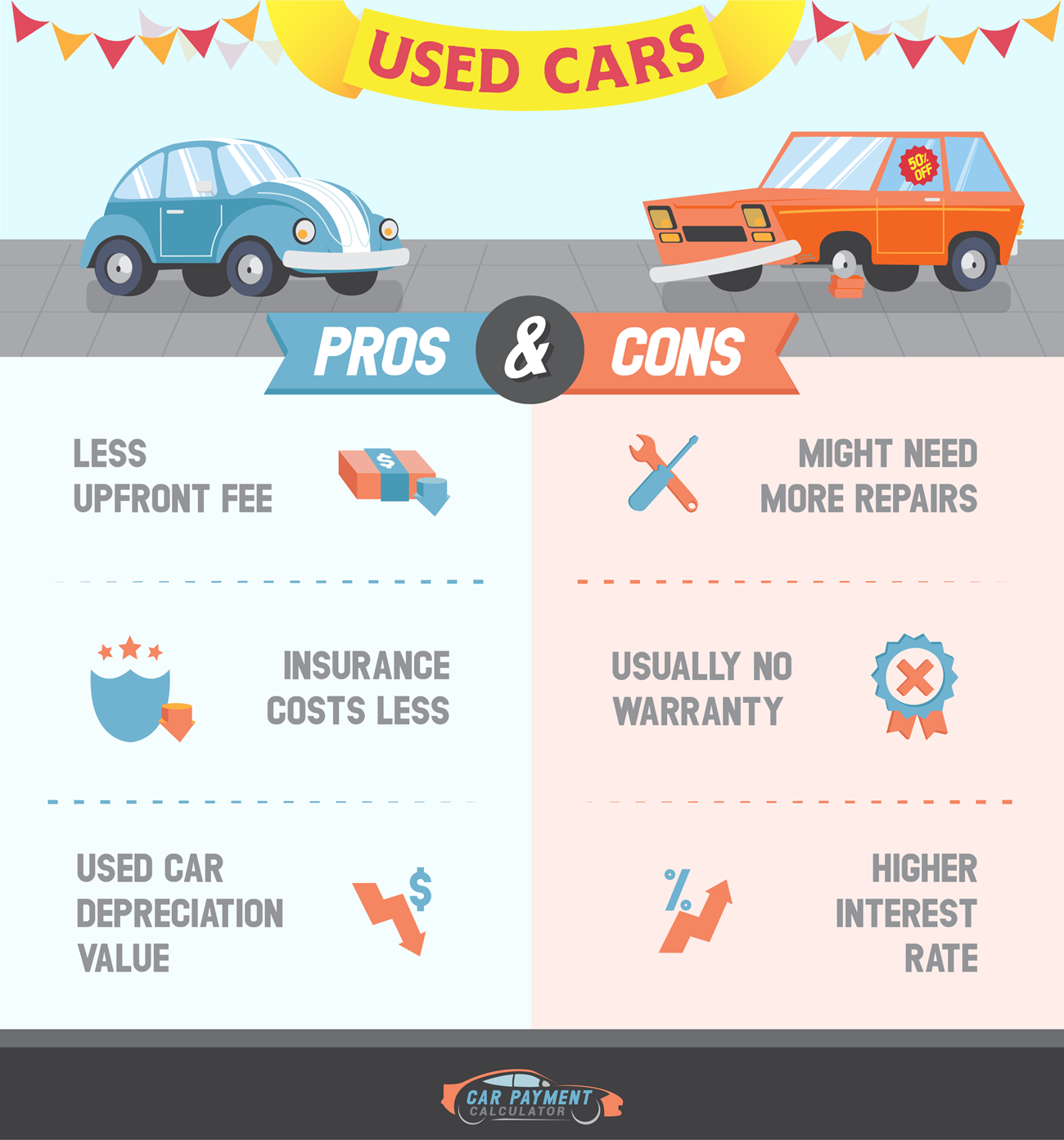

Weighing New vs. Used Cars: Car Note Considerations

The decision between buying a new or used car has profound implications for your car note and overall financial picture:

- New Cars:

- Pros: Latest technology, full warranty, no prior owner issues, often access to lower interest rates (especially through manufacturer incentives).

- Cons: Rapid depreciation (losing significant value the moment you drive it off the lot), higher purchase price leading to larger principal and potentially larger car notes.

- Used Cars:

- Pros: Significantly lower purchase price (avoiding the steepest depreciation), lower insurance costs, smaller principal meaning potentially lower car notes, greater value retention moving forward.

- Cons: Shorter or no warranty, potential for unforeseen mechanical issues, potentially higher interest rates (lenders may perceive used cars as higher risk), may not have the latest features.

For many budget-conscious buyers, a quality used car offers excellent value, allowing for a smaller car note and less total debt, freeing up funds for other financial priorities. The “sweet spot” is often a car that is a few years old (3-5 years), having absorbed the initial depreciation but still having plenty of life left.

Conclusion

Understanding “what’s a car note” is an essential lesson in personal finance. It’s not merely a recurring bill but a significant financial commitment with far-reaching implications for your budget, credit, and long-term financial goals. By thoroughly grasping the components of an auto loan, strategically navigating the application process, and diligently managing your payments, you can transform a potentially burdensome obligation into a manageable part of your financial landscape.

Empowering yourself with knowledge about interest rates, loan terms, credit scores, and the true cost of car ownership allows you to make decisions that align with your financial objectives. Whether you’re considering a new purchase or already making payments, a proactive and informed approach to your car note is a cornerstone of sound money management, paving the way for greater financial freedom and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.