The escalating cost of higher education is one of the most significant financial hurdles facing modern families. As tuition rates consistently outpace inflation, the need for a strategic, tax-advantaged investment vehicle has never been more critical. Enter the 529 plan—a cornerstone of American personal finance designed specifically to help families navigate the complexities of funding education. Named after Section 529 of the Internal Revenue Code, these plans have evolved from simple college savings accounts into versatile financial tools that offer substantial tax benefits, flexibility, and a path toward long-term wealth preservation.

In this guide, we will explore the mechanics of 529 plans, their unique tax advantages, the impact of recent legislative changes, and how to integrate them into a broader financial strategy.

Understanding the Basics of a 529 Plan

At its core, a 529 plan is a state-sponsored investment account that allows savers to put away money for future education expenses. While these plans are authorized by federal law, they are administered by individual states, state agencies, or educational institutions. Understanding the distinction between the types of plans and how they function is the first step in maximizing their potential.

Definition and Purpose

A 529 plan is technically a “qualified tuition program.” Its primary purpose is to encourage families to save for the high costs of post-secondary education by offering incentives that traditional brokerage accounts or savings accounts cannot match. While they are most commonly associated with four-year universities, the scope of 529 plans has expanded significantly to include vocational schools, trade schools, and even certain international institutions.

Types of 529 Plans: Savings vs. Prepaid Tuition

There are two distinct varieties of 529 plans, each serving a different financial philosophy:

- Education Savings Plans: This is the most popular type. It functions similarly to a 401(k) or an IRA. You contribute after-tax dollars into an account, and those funds are invested in a portfolio of mutual funds, ETFs, or other investment vehicles. The account’s value fluctuates based on market performance.

- Prepaid Tuition Plans: These plans allow you to purchase credits or units at participating colleges and universities (usually public, in-state institutions) for future tuition and mandatory fees at current prices. This acts as a hedge against tuition inflation, though these plans are less common and often have more residency restrictions.

How 529 Plans Work in Practice

Anyone can open a 529 plan—parents, grandparents, or even individuals for their own future education. The person who opens the account is the “owner,” and the person for whom the funds are intended is the “beneficiary.” The owner maintains control over the account, including the ability to change the beneficiary or decide when and how the funds are distributed. This control is a vital feature for long-term financial planning.

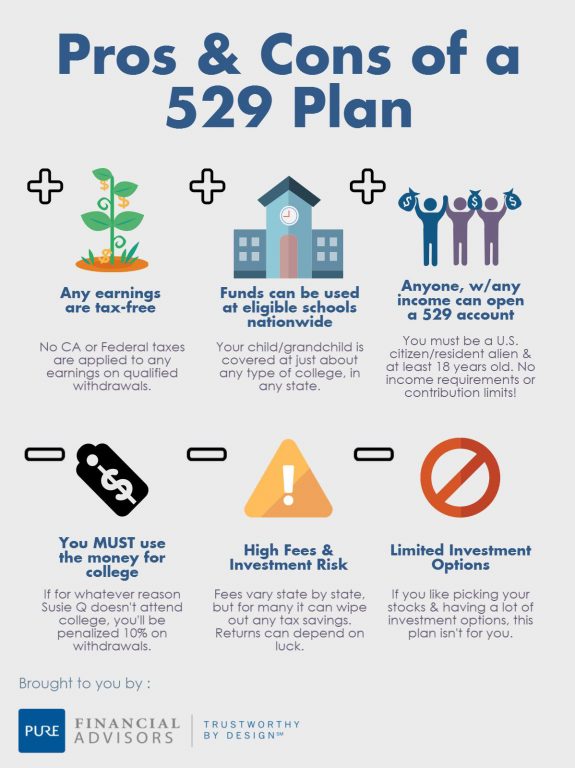

The Significant Tax Advantages of 529 Plans

The primary reason financial advisors recommend 529 plans over standard taxable brokerage accounts is the “triple threat” of tax benefits. By utilizing these plans, investors can significantly amplify their net returns over a long-term horizon.

Tax-Deferred Growth

In a standard brokerage account, you are subject to capital gains taxes and taxes on dividends or interest earned each year. Within a 529 plan, your investments grow tax-deferred. This means that every dollar earned through market appreciation is reinvested without being chipped away by the IRS. Over 18 years, the compounding effect of tax-deferred growth can lead to a substantially larger nest egg compared to a taxable account.

Tax-Free Withdrawals for Qualified Expenses

The most powerful feature of the 529 plan is that withdrawals are 100% tax-free at the federal level, provided the money is used for “qualified education expenses.” This includes tuition, fees, books, supplies, and equipment required for enrollment. For many students, room and board also qualify, provided the student is enrolled at least half-time. By avoiding taxes on both the principal and the gains at the point of withdrawal, families can effectively increase their purchasing power by 15% to 30%, depending on their tax bracket.

State Tax Incentives and Credits

Beyond federal benefits, many states offer their own incentives to encourage residents to use their state-sponsored plan. Depending on where you live, you may be eligible for a state income tax deduction or a tax credit based on your contributions. It is important to note that you can participate in any state’s 529 plan, but you usually only receive the state tax break if you contribute to your home state’s specific plan. For high-income earners in states like New York or Indiana, these deductions can provide immediate, tangible savings every tax year.

Eligibility, Contributions, and Limits

One of the misconceptions about 529 plans is that they are only for middle-class families. In reality, the high contribution limits and lack of income restrictions make them an excellent tool for high-net-worth individuals looking for estate planning solutions.

Who Can Open and Benefit from a 529?

There are no income limits for contributing to a 529 plan. Whether you earn $50,000 or $5,000,000 a year, you can open an account and reap the federal tax benefits. Furthermore, there is no age limit for the beneficiary. An adult can open a 529 plan for themselves to fund a mid-career MBA or a certification program.

Contribution Limits and “Superfunding”

529 plans do not have the restrictive annual contribution limits found in IRAs or 401(k)s. Instead, they have “aggregate limit” caps that vary by state, typically ranging from $235,000 to over $500,000 per beneficiary.

From a gift tax perspective, contributions are considered completed gifts. To help families jumpstart their savings, the IRS allows for “superfunding.” This allows a contributor to bundle five years’ worth of annual gift tax exclusions into a single year’s contribution. As of 2024, an individual could contribute up to $90,000 (or $180,000 for a married couple) in a single year without triggering the gift tax, provided they don’t give any more to that beneficiary for the next five years.

Flexibility in Changing Beneficiaries

What happens if the intended student decides not to go to college or receives a full scholarship? The 529 plan offers remarkable flexibility. The account owner can change the beneficiary to another “member of the family” without incurring taxes or penalties. This definition is broad, including siblings, cousins, parents, and even future grandchildren. This makes the 529 plan a powerful multi-generational wealth-transfer tool.

Qualified Expenses and SECURE Act 2.0 Updates

The utility of 529 plans has expanded through recent legislation, making them more versatile than ever before. It is no longer just a “college” fund; it is a comprehensive “education” fund.

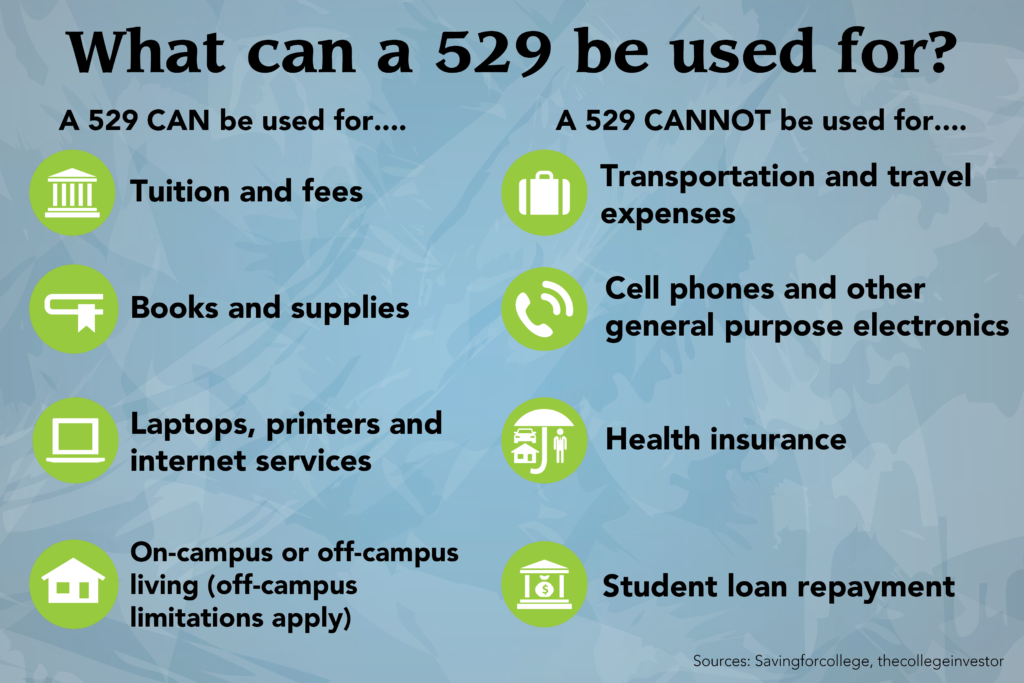

What Counts as a Qualified Education Expense?

To keep the tax-free status of withdrawals, the funds must be spent on qualified expenses. These include:

- Tuition and mandatory fees.

- Books, supplies, and equipment (including computers and internet access).

- Room and board (for students enrolled at least half-time).

- Special needs services for a beneficiary.

K-12 Tuition and Apprenticeship Programs

The Tax Cuts and Jobs Act of 2017 expanded 529 usage to include up to $10,000 per year per student for tuition at public, private, or religious K-12 schools. Additionally, the SECURE Act of 2019 expanded qualified expenses to include costs associated with registered apprenticeship programs and up to $10,000 (lifetime limit) to pay down principal or interest on qualified student loans.

The 529 to Roth IRA Rollover Provision

Perhaps the most significant change in recent years comes from the SECURE Act 2.0. Starting in 2024, account holders can roll over unused 529 funds into a Roth IRA for the beneficiary. This effectively eliminates the “fear of overfunding.” There are specific rules: the account must have been open for at least 15 years, and there are annual and lifetime limits ($35,000 lifetime cap). This provision ensures that if a child doesn’t use the money for school, it can still serve as a powerful foundation for their retirement.

Choosing and Managing Your 529 Plan

Selecting the right plan requires a balance of evaluating tax breaks, fees, and investment quality. Because you are not restricted to your own state’s plan, the entire national market is available to you.

Factors to Consider When Selecting a Plan

When comparing plans, look first at your home state’s tax benefits. If your state offers a significant deduction, it is usually best to stay local. However, if you live in a state with no income tax (like Texas or Florida) or a state that doesn’t offer a deduction, you should look for “Direct-Sold” plans with the lowest possible expense ratios. States like Utah (my529) and Nevada (Vanguard) are frequently cited for their low costs and high-quality underlying funds.

Investment Options: Age-Based vs. Static Portfolios

Most 529 plans offer “Age-Based” investment options. Much like a Target Date Fund in a 401(k), these portfolios are aggressive (heavy on stocks) when the child is young and automatically become more conservative (heavy on bonds and cash) as the child approaches college age. This “set it and forget it” approach is ideal for most parents. Alternatively, “Static” portfolios allow you to maintain a specific asset allocation regardless of the child’s age.

What Happens if the Beneficiary Doesn’t Go to College?

If the funds are not used for qualified expenses and are not rolled over into a Roth IRA or transferred to another family member, you can still withdraw the money. However, you will owe federal income tax on the earnings portion of the withdrawal, plus a 10% penalty. The principal (your original contributions) is never taxed or penalized upon withdrawal because it was made with after-tax dollars.

In conclusion, a 529 plan is one of the most effective personal finance tools available for building long-term educational security. By combining significant tax savings with flexible management options and recent legislative enhancements, it provides a robust framework for families to invest in the most valuable asset of all: the future of their children. Whether you are just starting a family or looking to optimize a multi-generational estate plan, the 529 plan offers a clear, tax-advantaged path to meeting the rising costs of education.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.