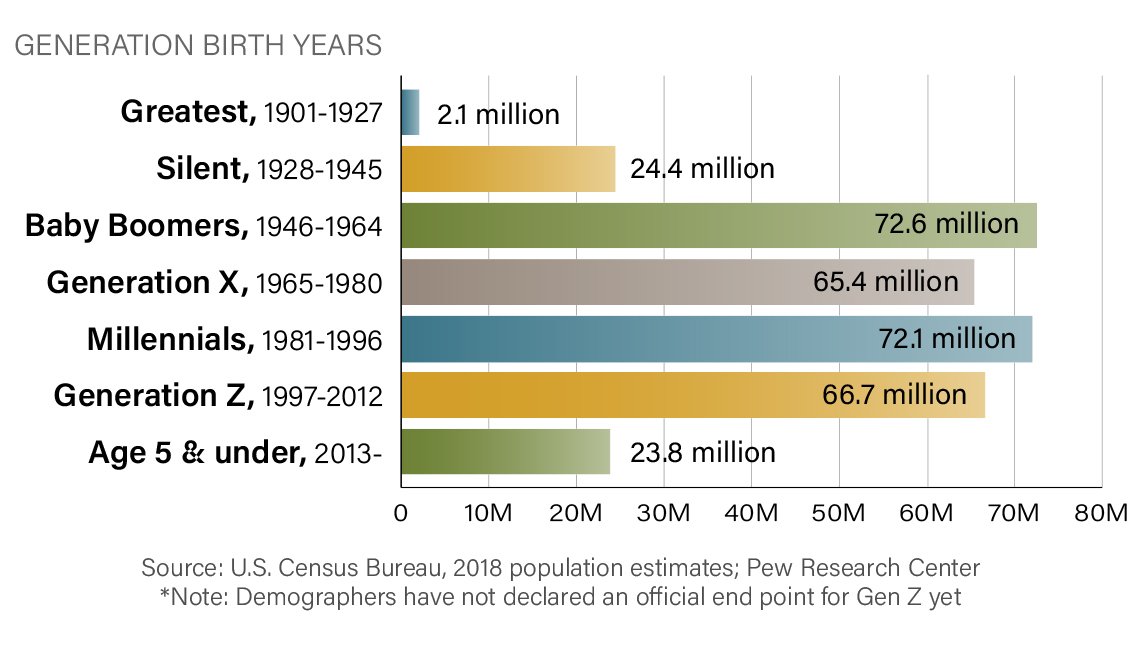

The question “what years are Gen X in?” is more than just a demographic inquiry; it’s a gateway to understanding a generation that has navigated immense societal and technological shifts. While the precise birth years can be debated, the common consensus places Generation X, often referred to as the “middle child” generation, as born roughly between the mid-1960s and the early 1980s. This cohort, sandwiched between the Baby Boomers and Millennials, has a unique perspective shaped by economic booms and busts, the rise of personal computing, and a growing skepticism towards traditional institutions.

From a financial perspective, Gen X occupies a fascinating and critical position. They are at a stage in their lives where they are balancing the responsibilities of supporting older generations and simultaneously preparing for their own retirement, all while navigating a complex and evolving economic landscape. Their financial behaviors, strategies, and challenges offer valuable insights into the broader dynamics of personal finance, investment, and the pursuit of financial independence in the 21st century. This article will delve into the financial realities of Generation X, exploring their investment habits, their approach to debt, their retirement planning strategies, and the financial tools they employ to secure their futures.

Gen X’s Financial Crucible: Navigating a Shifting Economic Landscape

Born during a period of significant economic transition, Gen X witnessed firsthand the impact of recessions, the dot-com bubble, and the Great Recession. This exposure has instilled in them a pragmatic and often cautious approach to financial management. Unlike their optimistic Boomer predecessors or their digitally native Millennial successors, Gen X often operates with a degree of skepticism, a trait that has profoundly shaped their financial decision-making.

The Shadow of Economic Uncertainty and its Impact on Risk Appetite

The formative years of many Gen Xers were marked by economic turbulence. From the oil crises of the 1970s to the S&L crisis of the late 1980s and early 1990s, they saw jobs disappear and investments falter. This consistent exposure to economic instability has, for many, cultivated a more risk-averse investment philosophy compared to earlier generations. While they may not shy away from investing altogether, their allocation often leans towards more stable, diversified portfolios. The memory of market crashes and subsequent prolonged recoveries has likely tempered a purely growth-focused approach, favoring a balance of capital preservation and steady appreciation.

This inherent caution can manifest in several ways. For instance, they might be more inclined to seek out traditional financial advisors rather than solely relying on do-it-yourself online platforms, valuing human expertise and a personalized approach. They may also exhibit a greater preference for tangible assets like real estate, which has historically been perceived as a more secure store of value, despite its own inherent volatilities. The emphasis often lies on building a solid foundation rather than chasing quick gains, a lesson learned through observing the financial fortunes of those around them.

The Rise of the “Latchkey Kid” Investor: Independence and Early Financial Exposure

The moniker “latchkey kid” for Gen X highlights a generation that often had more independence from a younger age. This autonomy extended to their early financial experiences. Many Gen Xers were exposed to the world of investing and personal finance at a time when it was becoming more accessible, albeit still less ubiquitous than today. The advent of discount brokerages and the increasing availability of financial information meant that Gen X had the opportunity to begin building wealth and understanding financial concepts earlier than many Boomers.

This early exposure has fostered a sense of self-reliance in their financial planning. While they may consult experts, they are also comfortable doing their own research and making informed decisions. This independence can be a significant advantage, allowing them to tailor their financial strategies to their specific needs and risk tolerance. They are less likely to blindly follow trends or advice, preferring to understand the rationale behind any financial recommendation. This can lead to more robust and personalized financial plans, but it also places a greater burden on them to acquire the necessary financial literacy. The ability to independently navigate the complexities of investment vehicles, tax implications, and market fluctuations is a hallmark of the financially savvy Gen X individual.

Gen X’s Debt Dilemma: The Mortgage Burden and the Credit Card Shadow

For Generation X, debt is a multifaceted issue, often characterized by the significant responsibility of homeownership and the persistent presence of consumer debt. This generation has grappled with the financial implications of major life decisions, including purchasing homes and managing the rising costs of raising families, all while navigating the allure and pitfalls of consumer credit.

The Mortgage as a Cornerstone and a Constraint

For many Gen Xers, the mortgage represents the largest single debt they will ever incur. It’s often viewed as a necessary step towards financial security and wealth building. They have generally embraced homeownership as a key financial goal, a tangible asset that offers stability and a potential hedge against inflation. However, this commitment also ties up a substantial portion of their income for decades, influencing their ability to save, invest, and spend in other areas.

The housing market’s fluctuations have directly impacted Gen X’s financial trajectory. Those who purchased during boom times may have seen significant equity growth, while others who bought at the peak before a downturn may still be grappling with underwater mortgages. The pressure to maintain mortgage payments can also limit their flexibility when it comes to career changes, relocation, or even taking on additional debt for other ventures. This makes strategic financial planning around mortgage repayment and refinancing crucial for this demographic. Furthermore, the increasing cost of housing in many regions means that for some Gen Xers, the dream of homeownership has become an even more significant financial undertaking, often requiring dual incomes and careful budgeting.

The Lingering Specter of Consumer Debt

Beyond the mortgage, Gen X has also contended with significant levels of consumer debt, particularly credit card debt. The increased accessibility of credit cards in their younger years, coupled with the pressures of consumerism, has led to a generation that understands the utility of plastic but also the dangers of accumulating high-interest balances. While some have successfully managed and paid down this debt, for others, it remains a persistent drain on their finances, hindering their ability to save for retirement or other significant goals.

The impact of credit card debt on Gen X’s financial health is profound. The high interest rates associated with these debts can make it difficult to make progress on principal repayment, leading to a cycle of debt accumulation. This can also negatively impact their credit scores, making it harder to secure favorable terms on future loans, such as mortgages or auto loans. The financial discipline required to manage credit responsibly is a lesson that many Gen Xers have learned, sometimes through hard experience. The ongoing effort to chip away at this debt, while simultaneously trying to save and invest, presents a unique financial challenge for this generation.

Gen X’s Retirement Reckoning: Bridging the Gap to Financial Independence

As Generation X approaches their prime earning years and begins to look towards retirement, a significant financial reckoning is underway. Having witnessed the changing landscape of pensions and the increasing reliance on individual savings, Gen X faces the daunting task of ensuring financial security in their later years. This generation is often characterized by a more independent approach to retirement planning, driven by necessity rather than solely by choice.

The Decline of Pensions and the Rise of the 401(k)

Unlike their Boomer predecessors who often benefited from defined-benefit pension plans, Gen X has largely had to rely on defined-contribution plans, most notably the 401(k). This shift places the onus of investment decisions and risk management squarely on the individual. The success of their retirement hinges on their ability to contribute consistently, make wise investment choices, and navigate market volatility over several decades.

The reliance on 401(k)s means that Gen Xers must be diligent in their savings habits. The temptation to dip into retirement funds for immediate needs, or the simple act of not contributing enough, can have a significant long-term impact on their retirement nest egg. Furthermore, the complexity of investment options within 401(k) plans can be overwhelming for some, leading to underperformance or overly conservative investment strategies that may not provide adequate growth. The financial literacy and ongoing engagement with their retirement accounts are therefore paramount for this generation.

The Balancing Act: Supporting Aging Parents and Planning for Their Own Future

A unique challenge faced by Generation X is the dual responsibility of potentially supporting aging parents while simultaneously preparing for their own retirement. This “sandwich generation” effect can put immense financial pressure on Gen X individuals. They may be providing financial assistance to their parents, helping with healthcare costs, or even providing direct care, all of which can divert funds that would otherwise be allocated to their own retirement savings.

This balancing act requires exceptional financial planning and prioritization. Gen Xers often find themselves needing to optimize every dollar, looking for ways to maximize savings, minimize expenses, and potentially explore additional income streams. The need to care for both ends of the generational spectrum can create a complex web of financial obligations that require careful management and foresight. The emotional and financial toll of this dual responsibility cannot be overstated, making proactive financial planning and open communication with both their children and their parents crucial for navigating this critical life stage.

Financial Tools and Strategies for the Gen X Investor

In their quest for financial security, Generation X employs a diverse range of financial tools and strategies, reflecting their pragmatic and often independent approach to money management. They are a generation that has embraced digital tools while still valuing traditional wisdom, creating a unique blend of modern financial practices.

Embracing Technology: Online Brokerages, Budgeting Apps, and Robo-Advisors

Gen X has been instrumental in the adoption of digital financial tools. They were among the first to embrace online banking and stock trading platforms, recognizing the efficiency and cost savings they offered. Today, many Gen Xers actively use budgeting apps to track their spending, manage their cash flow, and identify areas for potential savings. The rise of robo-advisors has also provided an accessible and often lower-cost entry point into diversified investing, appealing to their desire for smart, automated financial management.

These technological advancements have democratized access to financial tools, empowering Gen X to take a more hands-on approach to their wealth building. The ability to monitor their investments in real-time, set up automated savings transfers, and access a wealth of financial information at their fingertips has significantly changed the way they manage their money. This embrace of technology is a testament to their adaptability and their commitment to leveraging every available resource to achieve their financial goals.

The Enduring Value of Traditional Financial Advice and Diversification

Despite their comfort with digital tools, Gen X often recognizes the continued value of traditional financial advice. Many seek out fee-only financial planners or advisors who can offer objective guidance on complex financial decisions, such as retirement planning, estate planning, and tax optimization. The personalized insights and the human element of financial advice remain highly valued, especially when dealing with significant life events or complex financial situations.

Furthermore, diversification remains a cornerstone of Gen X’s investment strategy. They understand the importance of spreading their investments across different asset classes, industries, and geographies to mitigate risk. This may include a mix of stocks, bonds, real estate, and potentially alternative investments. Their approach is often characterized by a long-term perspective, focusing on building a resilient portfolio that can withstand market fluctuations and deliver consistent returns over time. This blend of modern technological tools and time-tested financial principles positions Generation X to navigate the complexities of personal finance with a degree of sophistication and resilience, ultimately aiming for a secure and financially independent future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.