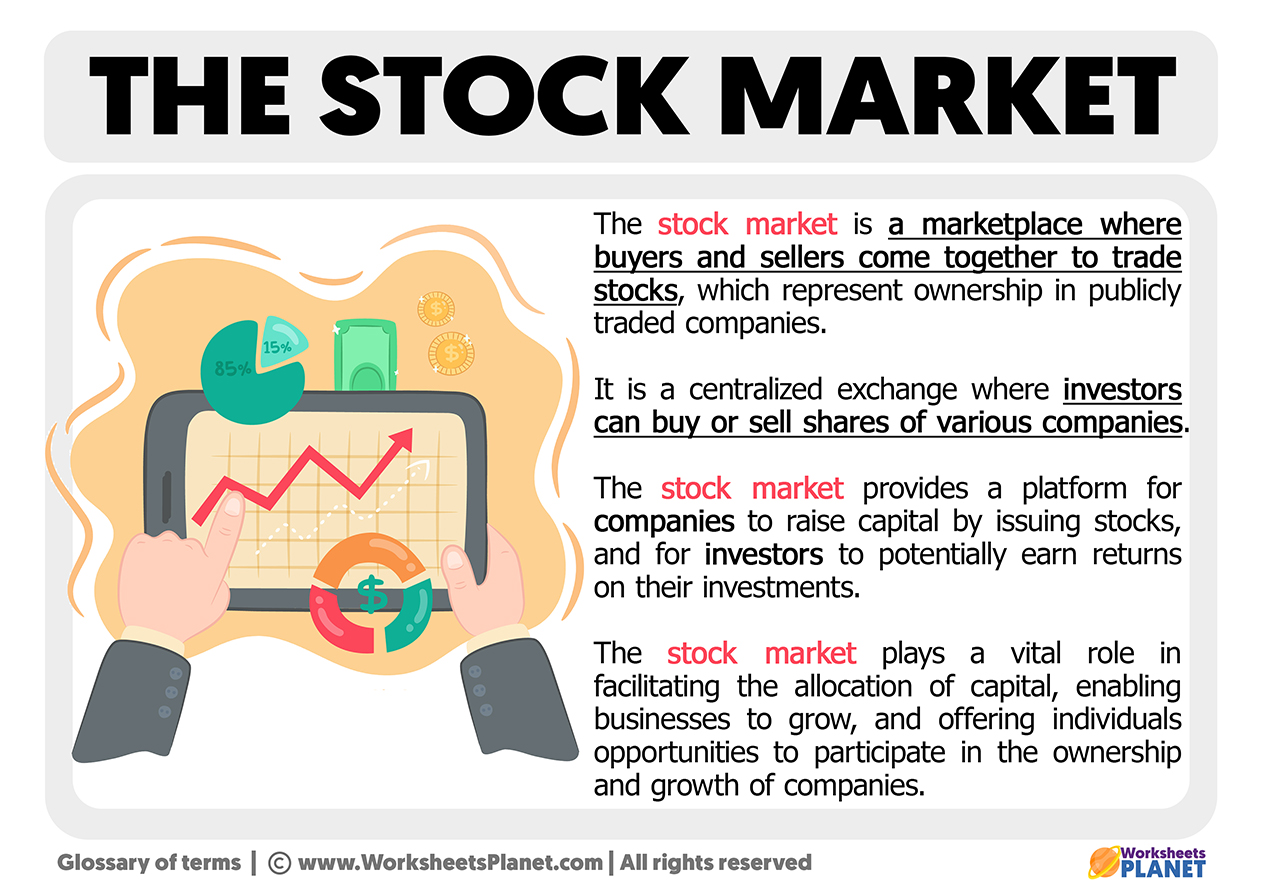

The question “what stock?” might seem simple, yet it unlocks a world of financial opportunity and complexity. For many, the stock market represents a daunting maze of jargon, charts, and unpredictable movements. For others, it’s a powerful engine for wealth creation, a gateway to financial independence, and a means to participate in the growth of innovative companies. This article aims to demystify the concept of stocks, providing a foundational understanding for aspiring investors and a fresh perspective for those looking to refine their strategies. We will explore what stocks are, why they are a vital component of long-term wealth building, and how to approach the market with confidence and informed decision-making.

The Foundation: Deconstructing “What Stock”

Before diving into the intricacies of investment strategies, it’s crucial to grasp the fundamental nature of a stock. Understanding this bedrock concept is the first step toward becoming a more knowledgeable and successful investor.

Defining a Stock: More Than Just a Piece of Paper

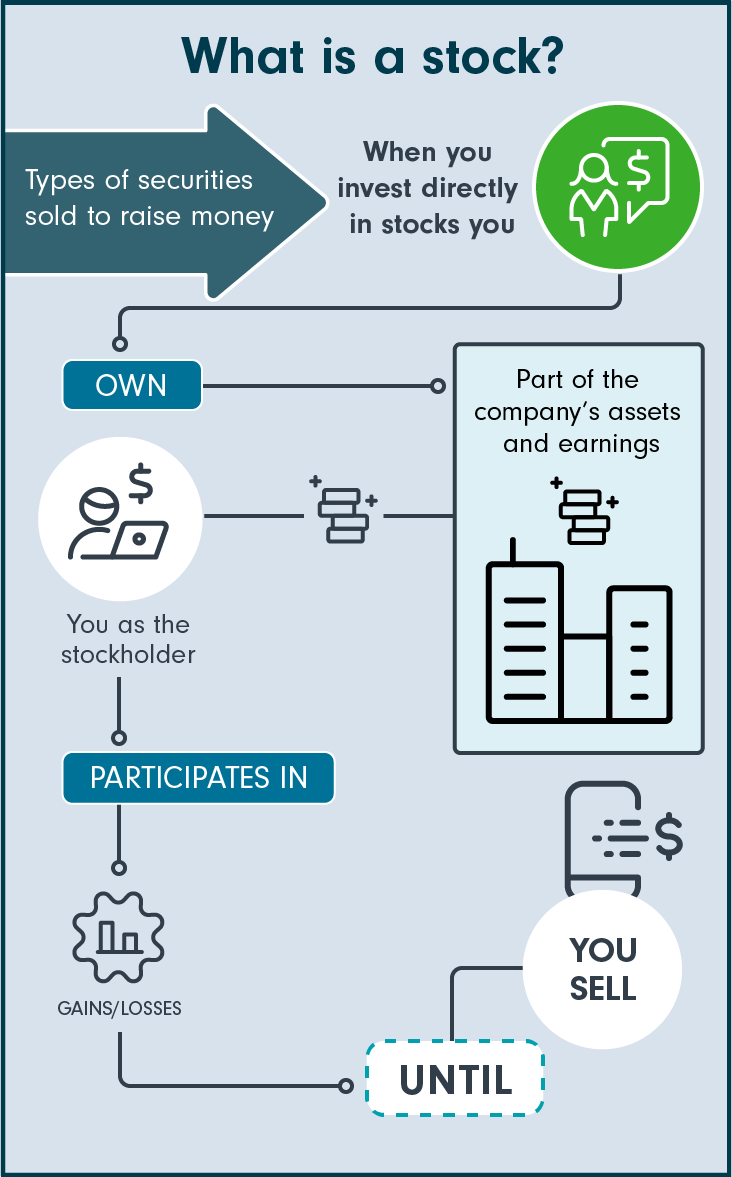

At its core, a stock (also known as equity or a share) represents a slice of ownership in a company. When you buy a stock, you become a part-owner, or shareholder, of the issuing company. This ownership stake, however small, grants you certain rights and a claim on a portion of the company’s assets and earnings. Unlike owning a physical asset like a house, owning a stock doesn’t give you direct control over the company’s daily operations or a right to walk into its offices and claim a desk. Instead, it provides a proportionate claim to residual earnings and, in most cases, voting rights on corporate matters.

The value of your stock fluctuates based on market demand, the company’s performance, its future prospects, and broader economic conditions. It’s important to remember that the price you pay for a stock today reflects the market’s collective assessment of all these factors.

Common vs. Preferred Shares: Knowing Your Rights

Not all stocks are created equal. Companies typically issue two main types of shares:

- Common Stock: This is the most prevalent type of stock. Common shareholders have voting rights on important corporate decisions, such as electing the board of directors, and typically have the potential for greater capital appreciation. However, they are last in line to receive payment if the company goes bankrupt (after bondholders and preferred shareholders).

- Preferred Stock: Preferred shares generally do not carry voting rights. However, they typically offer fixed dividend payments, often at a higher rate than common stock dividends, and preferred shareholders have priority over common shareholders in receiving payments if the company liquidates. This makes them less volatile than common stocks, appealing to income-focused investors who prioritize steady returns over capital gains potential or voting rights.

Understanding these distinctions is vital as they influence an investor’s potential returns, risks, and overall role within the company’s ownership structure.

Why Companies Go Public: Fueling Growth and Innovation

The process by which a privately held company first offers its shares to the public is called an Initial Public Offering (IPO). But why would a company choose to dilute its ownership and subject itself to intense public scrutiny?

Primarily, companies go public to raise capital. Selling shares to the public provides a significant influx of cash that can be used to fund expansion, research and development, pay down debt, or acquire other businesses. This capital infusion is often critical for scaling operations and maintaining competitive edge in fast-evolving markets.

Additionally, going public can increase a company’s visibility and prestige, making it easier to attract top talent and secure partnerships. It also provides liquidity for early investors and founders, allowing them to cash out a portion of their holdings. For investors, purchasing shares in a publicly traded company offers a chance to participate in its success and benefit from its future growth.

The Allure of Equities: Why Invest in Stocks?

Investing in stocks is a cornerstone of modern wealth management, attracting millions of people globally. While the allure is strong, it’s essential to understand both the opportunities and the inherent risks.

Capital Appreciation: The Power of Growth

One of the primary reasons investors buy stocks is for capital appreciation, which refers to the increase in the value of an asset over time. If you buy a stock for $50 and its market price rises to $75, you have realized a capital gain of $25 per share. Historically, the stock market has been one of the most effective vehicles for long-term wealth creation, outpacing inflation and other investment options over extended periods. This growth is driven by a company’s ability to innovate, expand its market share, increase profits, and effectively manage its operations. As the company grows, its perceived value increases, leading to a higher stock price.

Dividends: Regular Income Streams

Beyond capital appreciation, many companies distribute a portion of their profits to shareholders in the form of dividends. These are typically paid out quarterly, though some companies pay monthly or annually. Dividends provide a regular income stream to investors, which can be particularly appealing to retirees or those seeking supplemental income. While growth stocks (often younger, rapidly expanding companies) might reinvest all their earnings back into the business and pay no dividends, mature, stable companies in established industries are often reliable dividend payers. Reinvesting these dividends can also significantly boost your total returns over time through the power of compounding.

The Risks Involved: Understanding Volatility and Loss

It would be remiss to discuss stock investing without acknowledging the risks. The stock market is inherently volatile, meaning prices can fluctuate significantly and unpredictably. Economic downturns, geopolitical events, industry-specific challenges, or even negative company news can lead to sharp declines in stock prices. Unlike a savings account, there’s no guarantee that you will get back the principal amount you invested. The potential for capital loss is a real and ever-present factor.

Furthermore, individual stocks carry specific risks. A company’s management might make poor decisions, new competitors might emerge, or its products might become obsolete. These factors can erode its profitability and, consequently, its stock value. Prudent investors understand these risks and employ strategies to mitigate them, such as diversification and thorough research.

Long-Term Wealth Creation: Patience is a Virtue

Despite the short-term volatility, the stock market has consistently rewarded patient, long-term investors. Historically, periods of market decline have been followed by periods of recovery and growth. By investing for the long term (typically 5-10 years or more), investors can ride out market fluctuations and benefit from the compounding effect of returns. Compounding allows your earnings to generate further earnings, leading to exponential growth over time. This long-term perspective is crucial for harnessing the full potential of stock market investing.

Decoding the Market: Research and Analysis Essentials

Making informed investment decisions requires more than just gut feelings or following headlines. It demands a systematic approach to research and analysis. This involves digging into a company’s financials, understanding its industry, and evaluating its prospects.

Fundamental Analysis: Peering Into a Company’s Health

Fundamental analysis is the process of evaluating a security in an attempt to measure its intrinsic value, by examining related economic, financial, and other qualitative and quantitative factors. The goal is to determine if a stock is currently undervalued or overvalued by the market.

-

Key Financial Statements: At the heart of fundamental analysis are a company’s financial reports:

- Income Statement: Also known as the profit and loss (P&L) statement, it shows a company’s revenues, expenses, and profit (or loss) over a period (e.g., a quarter or a year). Key metrics here include revenue growth, gross profit, operating income, and net income (earnings).

- Balance Sheet: This provides a snapshot of a company’s financial health at a specific point in time, detailing its assets (what it owns), liabilities (what it owes), and shareholder equity (the owners’ claims). It helps assess solvency and liquidity.

- Cash Flow Statement: This statement tracks the actual cash coming into and going out of a company from its operating, investing, and financing activities. It’s crucial because profits reported on the income statement don’t always translate directly into cash in hand.

-

Key Ratios: Financial statements yield powerful insights when analyzed through various ratios:

- Price-to-Earnings (P/E) Ratio: Compares a company’s current share price to its earnings per share (EPS). A high P/E might indicate high growth expectations, while a low P/E might suggest undervaluation or a lack of growth prospects.

- Earnings Per Share (EPS): A company’s profit divided by the number of outstanding shares. Higher EPS generally indicates greater profitability.

- Debt-to-Equity Ratio: Measures a company’s financial leverage, indicating how much debt it uses to finance its assets relative to the value of shareholders’ equity. Lower ratios are generally preferred.

- Return on Equity (ROE): Measures the rate of return on the ownership interest (shareholders’ equity) of the common stock owners. A higher ROE indicates more efficient use of shareholder investments.

-

Industry and Economic Trends: A company does not operate in a vacuum. Its success is heavily influenced by the broader industry landscape, competitive pressures, technological advancements, and macroeconomic conditions (e.g., interest rates, inflation, GDP growth). Understanding these external factors is critical for assessing a company’s future prospects.

Technical Analysis: Interpreting Market Sentiment

While fundamental analysis focuses on a company’s intrinsic value, technical analysis attempts to predict future price movements based on past price and volume data. Technical analysts use charts, patterns, and indicators to identify trends and predict potential turning points. While valuable for short-term trading, a deep dive into technical analysis is beyond the scope of a foundational guide. For long-term investors, fundamental analysis typically holds greater weight.

Identifying Growth Sectors vs. Value Traps

Part of successful research is understanding where to look. Growth stocks are companies expected to grow at an above-average rate compared to the market. They often reinvest most of their earnings back into the business and pay little to no dividends. Value stocks are those that appear to trade at a lower price relative to their fundamentals (e.g., earnings, dividends, sales), suggesting they are undervalued by the market.

However, beware of value traps – stocks that appear cheap but are fundamentally flawed and continue to decline. Thorough due diligence is key to distinguishing genuine value from deceptive affordability.

Crafting Your Investment Strategy: Building a Resilient Portfolio

With a grasp of what stocks are and how to analyze them, the next step is to formulate a personal investment strategy. A well-constructed portfolio is resilient, diversified, and aligned with your financial goals and risk tolerance.

Defining Your Risk Tolerance: A Personal Assessment

Before making any investment, you must understand your risk tolerance – your psychological willingness and financial ability to take on risk. Are you comfortable with significant fluctuations in portfolio value for the potential of higher returns, or do you prioritize capital preservation and stable growth? Your age, income stability, existing savings, and time horizon (when you’d need the money) all play a role in determining this. Younger investors with a longer time horizon might afford to take on more risk, while those nearing retirement might opt for a more conservative approach.

Diversification: The Golden Rule of Investing

Diversification is arguably the most critical principle in investing. It means not putting all your eggs in one basket. By spreading your investments across various assets, industries, and geographies, you reduce the impact of any single investment performing poorly.

- Across Industries: Investing in a range of sectors (e.g., technology, healthcare, consumer staples, financials) ensures that if one industry faces headwinds, your entire portfolio isn’t jeopardized.

- Across Market Caps: Diversifying across large-cap (well-established, stable companies), mid-cap (growing companies), and small-cap (smaller, higher-growth potential but riskier companies) stocks can balance growth potential with stability.

- Beyond Stocks: True diversification often extends beyond just stocks to include other asset classes like bonds, real estate, and potentially alternative investments.

Investment Styles: Growth, Value, Income, or Blend?

Your risk tolerance and goals will largely dictate your investment style:

- Growth Investing: Focuses on companies with strong earnings growth potential, often regardless of their current valuation. These are typically fast-growing companies that reinvest profits and may not pay dividends.

- Value Investing: Seeks out companies whose intrinsic value is believed to be higher than their current market price. Value investors look for “bargains” and are patient, waiting for the market to recognize the true worth of their holdings.

- Income Investing: Prioritizes investments that provide regular income, primarily through dividends from stocks or interest from bonds. This style is often favored by retirees or those seeking supplemental cash flow.

- Blended Approach: Many investors adopt a combination, balancing growth potential with value and income considerations. This often proves to be a robust strategy.

The Power of Dollar-Cost Averaging: Mitigating Volatility

Dollar-cost averaging (DCA) is a strategy where an investor invests a fixed amount of money at regular intervals (e.g., $100 every month), regardless of the asset’s price. This approach automatically leads to buying more shares when prices are low and fewer shares when prices are high, effectively averaging out the purchase price over time. DCA reduces the risk of making a large investment at an unfavorable peak and removes the emotional component of trying to “time the market.”

Rebalancing Your Portfolio: Staying on Track

Over time, different investments in your portfolio will perform differently, causing your original asset allocation (e.g., 60% stocks, 40% bonds) to drift. Rebalancing involves periodically adjusting your portfolio back to its target allocation. This might mean selling some assets that have grown significantly and buying more of those that have underperformed, or simply redirecting new investments to underperforming segments. Rebalancing helps manage risk and ensures your portfolio remains aligned with your long-term goals.

From Theory to Practice: Executing Your Stock Investments

Once you’ve developed your strategy, the next step is to put it into action. This involves choosing a brokerage, understanding how to place trades, and continuously managing your investments.

Choosing a Brokerage: Features, Fees, and Services

To buy or sell stocks, you need a brokerage account. The choice of brokerage can significantly impact your investing experience due to variations in fees, platform features, research tools, and customer service.

- Traditional vs. Discount Brokers: Traditional full-service brokers offer personalized advice, financial planning, and a wide range of products, but typically charge higher fees or commissions. Discount brokers provide lower-cost (often commission-free) trades and robust self-service platforms, ideal for investors who prefer to manage their own portfolios.

- Robo-Advisors: These platforms use algorithms to build and manage diversified portfolios based on your risk tolerance and financial goals, often with very low fees. They are an excellent option for beginners or those who prefer a hands-off approach.

When choosing, consider factors like minimum investment requirements, commission structures (for stocks, ETFs, options), access to research and educational materials, ease of use of their trading platform (desktop and mobile), and customer support quality.

Placing Your First Trade: Market Orders vs. Limit Orders

When you’re ready to buy or sell, you’ll encounter different order types:

- Market Order: An instruction to buy or sell a security immediately at the best available current price. Market orders are executed quickly but offer no price guarantee – you might pay slightly more or receive slightly less than the last quoted price, especially for less liquid stocks.

- Limit Order: An instruction to buy or sell a security only at a specified price or better. A buy limit order will only execute at your specified price or lower, while a sell limit order will only execute at your specified price or higher. Limit orders give you more control over the price but may not execute if the market price never reaches your specified limit. For new investors, using limit orders can be a prudent way to ensure you don’t overpay.

Monitoring and Adjusting: The Active Investor’s Role

Investing is not a “set it and forget it” endeavor. While long-term investors aren’t day traders, regular monitoring of your portfolio and the broader economic landscape is crucial. Review your portfolio at least annually (or more frequently if market conditions change significantly) to ensure it still aligns with your goals and risk tolerance. Be prepared to adjust your strategy as your life circumstances evolve, or if a company’s fundamentals drastically change. This might involve rebalancing, selling underperforming assets, or taking advantage of new opportunities.

Taxation and Record-Keeping: Don’t Forget the Details

Finally, remember the tax implications of stock investing. Capital gains (profits from selling a stock) and dividends are subject to taxation. The tax rate can vary depending on whether it’s a short-term gain (held for less than a year) or a long-term gain (held for over a year), and your overall income bracket. Keep meticulous records of all your trades, including purchase dates, costs, sale dates, and proceeds. This will simplify tax season and help you track your overall performance accurately.

In conclusion, understanding “what stock” entails a journey from grasping basic definitions to mastering strategic execution. By diligently researching, diversifying wisely, and maintaining a long-term perspective, you can confidently navigate the stock market and unlock its immense potential for wealth creation. The journey of investing is continuous learning, but with a solid foundation, you are well-equipped to begin building your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.