The age-old question of how much of one’s income should be allocated to rent is more complex today than ever before. For decades, the conventional wisdom of the “30% rule” served as a guiding principle for individuals and financial institutions alike. However, in an era defined by rapid technological advancements, evolving economic landscapes, and a burgeoning digital economy, a one-size-fits-all answer feels increasingly outdated. Understanding the true percentage of your paycheck that should go to rent requires a holistic approach, blending traditional financial principles with modern tools, strategic income generation, and a keen awareness of personal financial goals and the unique demands of the current market.

This article delves into the nuances of rent affordability, examining the historical context, dissecting the factors that challenge traditional guidelines, and—crucially—exploring how technology and personal branding can empower individuals to make smarter, more sustainable housing decisions. From sophisticated financial planning apps to the power of a diversified income stream, we’ll navigate the path to not just affording rent, but strategically integrating it into a robust financial future.

The Evolving 30% Rule: A Modern Perspective on Rent-to-Income Ratios

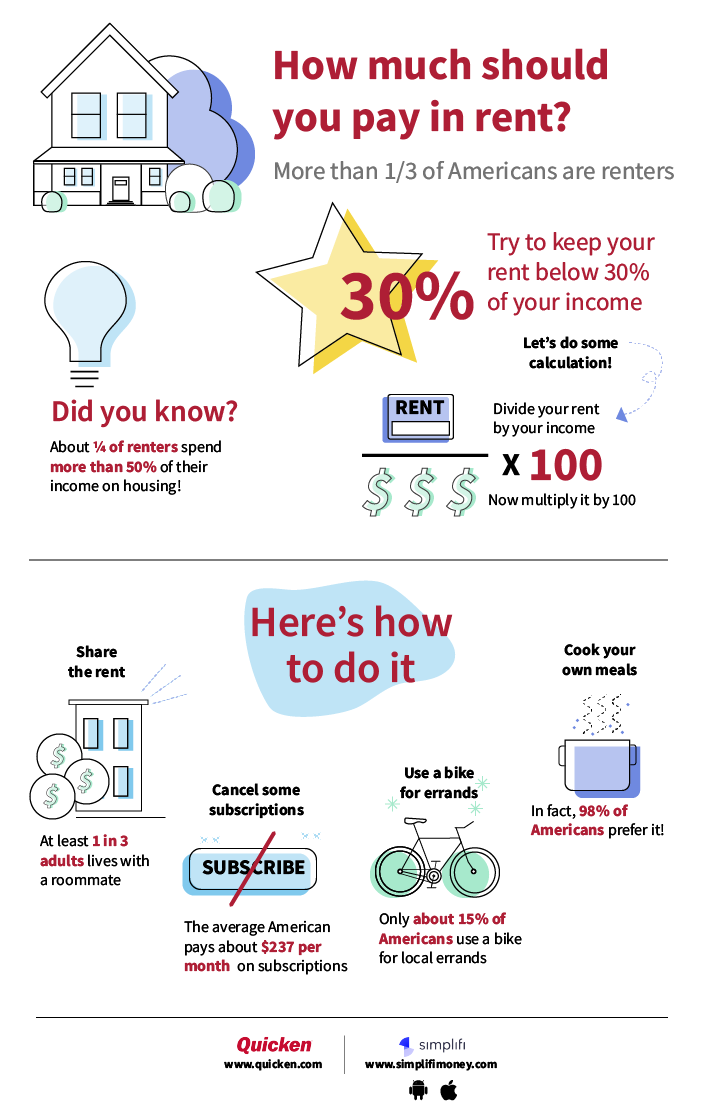

For generations, the “30% rule” has been the cornerstone of housing affordability advice. This guideline suggests that your gross monthly income should ideally cover no more than 30% of your rent, including utilities. While simple and easy to remember, its relevance in today’s dynamic economic climate is increasingly questioned.

Understanding the Traditional Benchmark

The 30% rule originated in the United States in the 1930s, initially as part of housing legislation designed to provide affordable public housing. It was later codified into law in 1981, setting the maximum amount a household could pay for rent to receive federal housing assistance. The logic behind it was straightforward: spending more than 30% of your income on housing would leave insufficient funds for other necessities like food, transportation, healthcare, and savings. For many years, it served as a practical benchmark for renters, landlords, and lenders to assess financial stability. If a renter’s income met this threshold, it was generally considered a green light for landlords, signaling a lower risk of default and indicating that the tenant possessed enough discretionary income to maintain their lifestyle.

Why the 30% Rule Falls Short Today

While historically significant, the 30% rule often fails to account for the multifaceted realities of modern personal finance. Several factors contribute to its diminishing utility:

- Stagnant Wages vs. Soaring Rents: In many urban and even suburban areas, rent prices have drastically outpaced wage growth. This disparity means that for a significant portion of the population, adhering to the 30% rule would necessitate living in undesirable locations, in substandard conditions, or simply isn’t an option without significant sacrifices.

- Varying Regional Economies: The cost of living varies wildly from one city or region to another. 30% of a high income in a low-cost area might be perfectly comfortable, but 30% of a modest income in an expensive metropolis like New York City, San Francisco, or London could easily be insufficient to secure even basic accommodation.

- Individual Financial Burdens: The rule doesn’t consider other significant financial obligations such as student loan debt, childcare costs, healthcare premiums, or transportation expenses, which can eat into a substantial portion of a paycheck before rent is even considered. A young professional with substantial student loan payments, for instance, might find the 30% rule unrealistic despite a decent salary.

- Inflation and Lifestyle Expectations: What constituted a comfortable lifestyle decades ago differs from today. The rise of subscription services, digital connectivity needs, and evolving consumer habits mean that discretionary income is often allocated differently.

Alternative Rent-to-Income Guidelines

Recognizing the limitations of the 30% rule, financial experts have proposed alternative budgeting frameworks that offer more flexibility and a realistic approach to housing affordability:

- The 50/30/20 Rule: This popular budget strategy suggests allocating 50% of your after-tax income to “needs” (including rent, utilities, groceries, transportation, essential insurance), 30% to “wants” (dining out, entertainment, hobbies, travel), and 20% to “savings and debt repayment.” Under this model, rent isn’t a standalone percentage but part of a broader “needs” category, allowing for a higher percentage if other needs are lower, or vice versa. This rule provides more flexibility, especially for those in high-cost-of-living areas, as it acknowledges that housing might take a larger slice of the “needs” pie.

- The 35-40% Rule (with caveats): In extremely high-cost-of-living areas, some financial advisors suggest that a rent-to-income ratio of up to 35-40% might be acceptable, provided that other expenses are kept exceptionally low, and there’s a clear plan for robust savings and debt reduction. This approach often requires significant lifestyle trade-offs and meticulous budgeting to ensure financial stability.

- Personalized Budgeting: Ultimately, the most effective approach is a personalized budget. This involves a detailed analysis of your unique income, expenses, financial goals, and priorities. What one person considers an acceptable rent burden, another might find unsustainable. The goal isn’t just to afford rent, but to ensure that your housing costs leave enough room for other essential expenses, savings, investments, and a reasonable quality of life.

Leveraging Technology and Digital Tools for Smarter Rent Decisions

In the digital age, technology is not just a convenience; it’s a powerful ally in managing personal finances and making informed decisions about housing. From sophisticated budgeting applications to data-driven market analysis, tech tools can demystify the complexities of rent affordability and empower users to optimize their housing budget.

Financial Planning Apps and Software

The modern financial landscape is awash with apps and software designed to streamline budgeting, track expenses, and provide insights into spending habits. These tools are indispensable for understanding how much you can truly afford for rent:

- Automated Expense Tracking: Apps like Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard link directly to your bank accounts and credit cards, automatically categorizing transactions. This provides a clear, real-time overview of your income versus expenses, highlighting where your money is actually going.

- Budgeting and Goal Setting: These platforms allow users to set specific budgets for various categories, including housing. They can send alerts when you’re nearing your limits, helping you stay on track. Some even feature goal-setting modules for saving a down payment or creating an emergency fund, making the rent decision part of a larger financial strategy.

- AI-Powered Insights: Advanced apps are now incorporating Artificial Intelligence (AI) to offer predictive insights. AI can analyze your spending patterns to identify potential overspending, suggest areas for saving, and even forecast your financial health, giving you a clearer picture of your capacity to handle a certain rent payment. For instance, an AI tool might suggest that while 35% of your income seems high for rent, your current spending on discretionary items is so low that it’s manageable.

- Digital Security: With these tools handling sensitive financial data, robust digital security features – including multi-factor authentication, encryption, and regular security audits – are paramount. Ensuring the safety of your financial information is a key consideration when choosing which apps to trust.

Data-Driven Rental Market Analysis

Gone are the days of aimlessly driving around neighborhoods looking for “For Rent” signs. The internet has revolutionized how renters find and evaluate properties, offering unprecedented access to market data:

- Online Rental Platforms: Websites and apps like Zillow, Trulia, Apartments.com, Rent.com, and local real estate agency portals provide comprehensive listings, complete with photos, virtual tours, floor plans, and amenity details. They allow users to filter searches by price, number of bedrooms, location, pet policy, and more, significantly narrowing down options.

- Market Trend Analysis: Many platforms offer tools to research historical rent prices, average costs in specific neighborhoods, and market trends. This data can help you determine if a particular listing is overpriced, underpriced, or fair market value. For instance, comparing the asking rent to the median rent for similar properties in the same zip code can provide strong negotiation leverage.

- AI for Predictive Analysis: The future of rental market analysis increasingly involves AI. AI algorithms can process vast amounts of data—including demographic shifts, economic indicators, public transport accessibility, and even local amenity ratings—to predict future rent trends and recommend neighborhoods that align with a renter’s budget and lifestyle preferences. This helps renters not just find a place today, but anticipate future affordability.

Digital Security and Smart Home Integration

While not directly related to the “percentage” of your paycheck, these tech aspects can indirectly influence the overall cost and value of your rental:

- Energy Management Systems: Smart thermostats (e.g., Nest, Ecobee) can optimize heating and cooling, potentially lowering utility bills, thus reducing the total housing cost. Many landlords are now integrating these into rental units.

- Smart Home Security: Digital door locks, video doorbells, and security cameras (with landlord permission) enhance safety and convenience, adding value to the rental experience.

- Digital Lease Management: Secure online portals for paying rent, submitting maintenance requests, and accessing lease documents streamline the rental process, reducing administrative hassle and improving transparency.

Building Your Financial Brand: Income Diversification and Personal Growth

Beyond simply budgeting your current income, a proactive approach to managing rent involves enhancing your earning potential and diversifying your income streams. In today’s economy, where personal brand and digital skills are increasingly valuable, individuals have unprecedented opportunities to bolster their financial standing, making rent a less daunting percentage of their overall financial picture.

The Gig Economy and Side Hustles

The rise of the gig economy, largely enabled by technology platforms, has democratized income generation. What was once seen as supplementary income for specific groups is now a mainstream strategy for many to meet financial goals, including comfortably affording rent:

- Online Freelancing Platforms: Websites like Upwork, Fiverr, Toptal, and Freelancer.com connect skilled individuals with clients seeking services in writing, graphic design, web development, digital marketing, virtual assistance, and more. These platforms allow individuals to monetize their skills outside of a traditional 9-to-5 job, directly increasing their take-home pay.

- Content Creation and Monetization: Platforms like YouTube, TikTok, Instagram, and personal blogs offer avenues for individuals to build an audience and generate income through advertising, sponsorships, merchandise sales, and direct audience support. A strong personal brand can translate into significant revenue streams, offsetting housing costs.

- On-Demand Services: Ride-sharing (Uber, Lyft), food delivery (DoorDash, Uber Eats), and other local service apps provide flexible opportunities to earn extra cash in your spare time. This additional income, even if modest, can be strategically allocated to rent, emergency savings, or debt reduction.

- Online Education and Consulting: If you possess specialized knowledge, platforms like Teachable, Thinkific, or even simple video conferencing tools allow you to create and sell online courses or offer consulting services, leveraging your expertise into profitable ventures.

Personal Branding as a Financial Asset

Your “personal brand” is no longer just for celebrities or entrepreneurs; it’s a critical asset for anyone looking to maximize their earning potential. A strong, authentic personal brand can open doors to higher-paying opportunities and more lucrative side hustles:

- Professional Reputation: A well-curated online presence (LinkedIn profile, professional website, industry-specific social media) showcasing your skills, achievements, and thought leadership can attract recruiters and potential clients, leading to better job offers or freelance gigs.

- Networking and Opportunities: Your brand helps you connect with like-minded professionals and industry leaders, leading to mentorship, collaboration, and referral opportunities that can directly impact your income.

- Credibility and Trust: A consistent and positive personal brand builds trust, making you a preferred candidate for employment or a sought-after freelancer. This credibility often translates into higher rates or salaries.

- Niche Expertise: By positioning yourself as an expert in a specific niche (e.g., AI ethics, sustainable tech, brand storytelling), you can command premium rates and attract projects that align with your passion, making work more enjoyable and profitable.

Strategic Career Development and Upskilling

Investing in your skills and career growth is one of the most effective long-term strategies for managing housing costs. Many in-demand skills today are tech-related, offering clear pathways to higher income:

- Continuous Learning: Online courses (Coursera, edX, Udemy), certifications (Google, AWS, Microsoft), and workshops allow individuals to acquire new skills or deepen existing ones in areas like data science, cybersecurity, software development, cloud computing, and digital marketing. These skills are highly valued and command higher salaries.

- Mentorship and Professional Communities: Engaging with mentors and participating in professional communities (both online and offline) provides invaluable insights, networking opportunities, and guidance for career advancement.

- Negotiation Skills: Learning to effectively negotiate salaries and benefits is crucial. Understanding your market value and confidently advocating for it can significantly increase your take-home pay, making any rent percentage feel more manageable.

- Adaptability: The job market is constantly evolving. Cultivating adaptability and a willingness to learn new technologies and methodologies ensures long-term career resilience and upward mobility.

Beyond the Percentage: A Holistic Approach to Housing Affordability

While a percentage rule provides a useful starting point, truly assessing housing affordability requires looking beyond the base rent payment. A holistic approach considers all associated costs, lifestyle choices, and how rent fits into your broader financial aspirations.

Total Housing Costs vs. Base Rent

The sticker price of rent often doesn’t tell the whole story. To understand the true cost of housing, you must factor in additional expenses:

- Utilities: Electricity, gas, water, and sewage can add hundreds of dollars to your monthly housing budget. Smart home technology and energy-efficient appliances can help mitigate these costs.

- Internet and Cable: In today’s connected world, reliable internet is a necessity, not a luxury. These services can be significant monthly expenses.

- Renter’s Insurance: While often inexpensive, renter’s insurance is crucial for protecting your belongings and providing liability coverage. It’s an essential, non-negotiable cost.

- Maintenance and Repair (for homeowners, but sometimes renters): While landlords typically cover major repairs, renters might incur costs for minor fixes or unexpected needs, especially in older properties.

- Commute Costs: The cheapest rent might be in an area far from your work, leading to high transportation costs (gas, public transport, car maintenance, ride-sharing) and lost time. Calculate the real cost of your commute before committing to a distant, cheaper rental.

The Impact of Location and Lifestyle

Your choice of location and desired lifestyle significantly influence rent affordability:

- Urban vs. Suburban vs. Rural: City living often comes with higher rents but may offer lower transportation costs, more job opportunities, and amenities. Suburban and rural areas might have cheaper rent but require a car and could mean longer commutes.

- Roommates vs. Solo Living: Sharing an apartment or house with roommates can drastically reduce individual rent payments, allowing you to live in a better area or save more money. The personal finance implications of living alone versus with others are substantial.

- Amenities and Building Type: A luxury apartment with a gym, pool, and concierge service will naturally cost more than a no-frills unit. Evaluate which amenities are truly important to you and which you can live without.

- Quality of Life: Sometimes, paying a slightly higher percentage for rent in a safe neighborhood with good schools, parks, or a vibrant community is a worthwhile investment in your overall well-being. This non-monetary value should be part of your consideration.

Future Planning and Financial Goals

Your rent decision should not be made in isolation; it must align with your long-term financial objectives:

- Saving for a Down Payment: If homeownership is a goal, allocating a higher percentage to savings and investments now might mean compromising on rent for a few years to build capital faster.

- Retirement Planning: Ensure your rent doesn’t prevent you from contributing adequately to your retirement accounts. The power of compound interest makes early and consistent contributions invaluable.

- Debt Repayment: High-interest debt (like credit card debt) can be a significant drain on your finances. Prioritizing debt repayment might mean choosing a more modest rental to free up funds for accelerated debt reduction.

- Investment Goals: Whether it’s investing in the stock market, starting a business, or pursuing further education, your rent should leave room for these growth-oriented endeavors. A lower rent percentage can enable greater investment capacity, which in turn fuels long-term wealth creation.

In conclusion, there is no definitive “what percent of paycheck should go to rent” that applies to everyone. While the 30% rule offers a historical reference, the modern renter must adopt a more sophisticated, personalized approach. By leveraging cutting-edge financial technology, strategically diversifying income through the gig economy and personal branding, and holistically evaluating all housing-related costs against long-term financial goals, individuals can navigate the complex housing market with confidence. The key is not just to find an affordable place, but to make a housing decision that empowers your entire financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.