When discussing the landscape of modern finance, few names carry as much weight or command as much respect as Vanguard. For the average investor, Vanguard is often synonymous with the “set it and forget it” philosophy of wealth building. But to understand what Vanguard truly is, one must look beyond the ticker symbols and account balances. Vanguard is more than just an asset management firm; it is a structural anomaly in the financial world that fundamentally changed how millions of people save for retirement, buy homes, and build generational wealth.

Founded in 1975 by John C. “Jack” Bogle, Vanguard has grown from a small experimental firm into one of the world’s largest investment companies, managing over $7 trillion in global assets. Its rise was fueled by a singular, disruptive idea: that the interests of the investment firm should be perfectly aligned with the interests of the investor.

The Revolutionary Structure of Vanguard

To understand Vanguard, you must first understand its unique corporate structure. Most investment firms are either publicly traded (like BlackRock) or privately owned by a small group of partners or a parent company. In these traditional models, the firm has two masters to serve: the clients who invest their money and the shareholders who want to see a profit from the firm’s operations. This often creates a conflict of interest, as higher fees for clients translate to higher profits for shareholders.

The Client-Owned Model

Vanguard operates on a completely different premise. The company is owned by its funds, and those funds, in turn, are owned by the clients who invest in them. In essence, if you own a share of a Vanguard mutual fund or ETF, you are a partial owner of the company itself. This “mutuality” is the bedrock of Vanguard’s identity. Because there are no outside shareholders demanding a cut of the profits, Vanguard can return those profits to its investors in the form of lower costs.

Why Low Costs are the Ultimate Growth Engine

In the world of personal finance, the “expense ratio” is the silent killer of wealth. A fee of 1% might sound small, but over 30 years, it can strip away hundreds of thousands of dollars from a portfolio due to the loss of compounding returns. Vanguard’s structural advantage allows it to keep its average expense ratio significantly lower than the industry average. While many active funds charge 0.50% to 1.00% or more, Vanguard’s most popular index funds often charge as little as 0.03%. This relentless focus on cost-cutting has forced the entire financial industry to lower their prices—a phenomenon often referred to as “The Vanguard Effect.”

Core Investment Offerings and Strategy

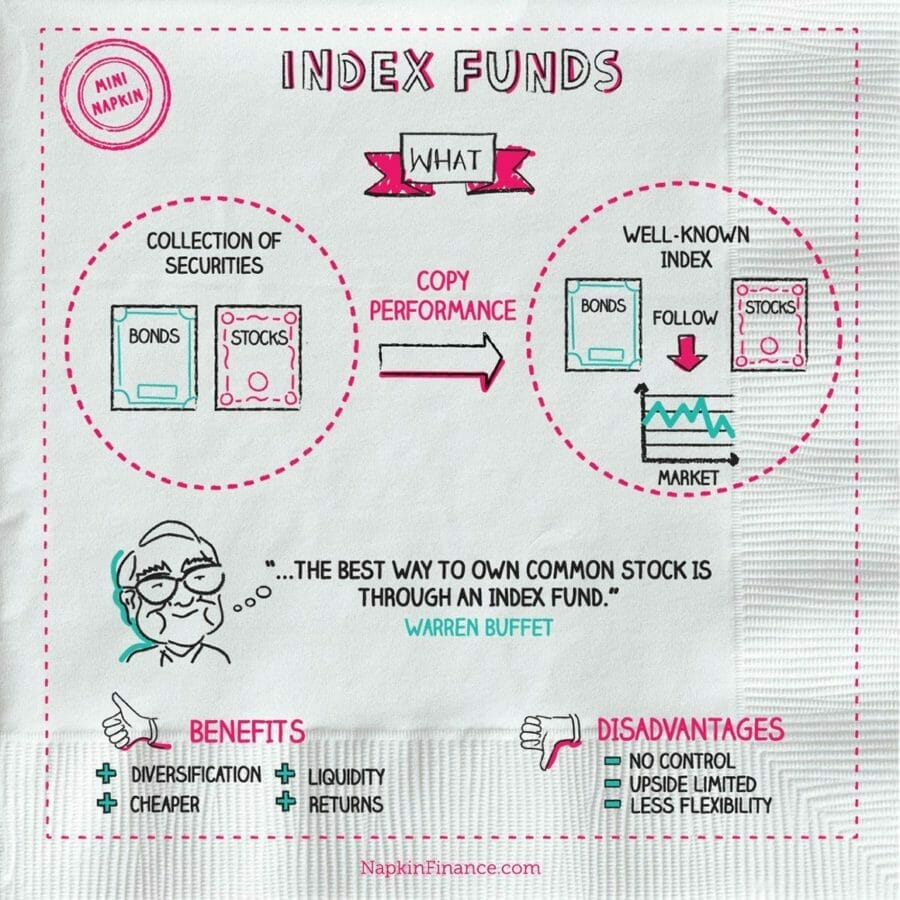

Vanguard is best known for being the pioneer of index fund investing. Before Bogle launched the First Index Investment Trust (now the Vanguard 500 Index Fund), the prevailing wisdom was that you had to hire an expensive “expert” to pick individual stocks and beat the market. Bogle argued that most experts fail to beat the market over the long term, especially after accounting for their high fees.

The Power of Index Funds and ETFs

An index fund is a type of mutual fund or Exchange-Traded Fund (ETF) designed to mimic the performance of a specific market benchmark, such as the S&P 500 or the Total Stock Market Index. Instead of trying to find the “next big thing,” a Vanguard index fund simply buys everything in the index. This provides instant diversification. By owning a single Vanguard ETF like VTI (Total Stock Market ETF), an investor gains exposure to thousands of U.S. companies, ranging from tech giants like Apple and Microsoft to smaller industrial firms.

Target Retirement Funds: The Ultimate “Hands-Off” Tool

For many investors, the most difficult part of “Money” management is knowing how to change their asset allocation as they get older. Vanguard popularized the Target Retirement Fund (or Target Date Fund). These funds are “funds of funds” that automatically adjust their holdings over time. When you are young, the fund is aggressive, holding mostly stocks. As you approach your target retirement year, the fund automatically shifts toward safer investments like bonds. This eliminates the emotional stress of rebalancing and ensures that investors don’t take on too much risk at the wrong time.

The Bogleheads Philosophy and Long-Term Success

The success of Vanguard is inextricably linked to a specific investment philosophy popularized by its founder and his followers, known as “Bogleheads.” This community emphasizes simplicity, frugality, and patience—traits that are often overlooked in a world of high-frequency trading and viral “meme stocks.”

Embracing Market Efficiency and Long-Term Thinking

The core of the Vanguard philosophy is the belief that the market is generally efficient. Rather than trying to time the market—guessing when it will go up or down—Vanguard encourages investors to “stay the course.” This means continuing to invest regardless of market volatility. History has shown that the biggest threat to an investor’s success isn’t a market crash; it is the investor’s own behavior. By providing low-cost, diversified tools, Vanguard makes it easier for individuals to resist the urge to trade impulsively and instead focus on long-term compounding.

Minimizing Taxes and Maximizing “Real” Returns

In the Money niche, it isn’t just about what you make; it’s about what you keep. Vanguard is highly regarded for its “tax-efficient” fund management. Because index funds trade less frequently than actively managed funds, they generate fewer capital gains distributions, which can trigger tax bills for investors. For those holding investments in taxable accounts, this efficiency can add a significant “hidden” return to their portfolio over several decades.

Modern Services: Vanguard in the Digital Age

While Vanguard was built on the back of paper ledgers and telephone orders, it has evolved into a modern financial powerhouse that offers more than just mutual funds. To stay competitive with fintech startups and traditional brokerages, Vanguard has expanded its suite of financial tools.

Personal Advisor Services and Hybrid Advice

Recognizing that some investors want more guidance than a simple index fund can provide, Vanguard launched its Personal Advisor Services (PAS). This is a “hybrid” model that combines sophisticated algorithms with human financial advisors. While traditional wealth managers might charge 1% or more of assets under management, Vanguard’s service is offered at a fraction of that cost. This makes professional financial planning accessible to the “mass affluent”—the middle-class families who have saved diligently but don’t have the multi-million dollar portfolios required by boutique private banks.

Digital Experience and the Modern Brokerage

In recent years, Vanguard has overhauled its digital interface to cater to a younger generation of investors. Through the Vanguard mobile app and website, users can trade stocks, ETFs, and options, often with zero commissions. While Vanguard’s platform is less “gamified” than apps like Robinhood—a deliberate choice to discourage frequent, risky trading—it provides all the necessary tools for a disciplined, long-term investor to manage their entire financial life in one place.

Is Vanguard Right for Your Financial Journey?

Choosing where to put your money is one of the most important decisions you will ever make. Vanguard is not necessarily the right choice for everyone, but it is the gold standard for a specific type of investor.

Best for Long-Term Wealth Builders

If your goal is to build wealth over decades for retirement, education, or financial independence, Vanguard is arguably the best platform in existence. Its culture is built around the idea of the “prudent investor.” It is not a place for day traders, speculators, or those looking to get rich quick. It is a place for people who understand that wealth is built through the slow, steady accumulation of assets and the rigorous minimization of costs.

Assessing the Trade-offs

No company is perfect. Some users find Vanguard’s customer service to be slower than that of premium competitors like Fidelity or Charles Schwab, especially during periods of high market volatility. Additionally, because Vanguard’s philosophy is so rooted in simplicity, investors looking for highly complex derivative products or “bleeding-edge” alternative investments might find the platform’s offerings too conservative.

However, for the vast majority of people, the “Money” problem isn’t a lack of complex products; it’s the presence of high fees and unnecessary risk. Vanguard solves these problems at their root. By making the investor the owner, Vanguard created a virtuous cycle where success for the company is defined by the success of its clients. In the high-stakes world of finance, that is a rare and powerful thing. Whether you are just starting your first job or are already enjoying retirement, understanding Vanguard is a critical step in mastering your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.