Determining exactly how much of your paycheck should be directed toward savings is one of the most pivotal decisions you will make for your financial future. While the question seems simple, the answer is often layered with variables including your income level, geographic location, debt obligations, and long-term aspirations. In a world of rising costs and economic volatility, a structured approach to saving is no longer just a recommendation—it is a necessity for achieving peace of mind and building generational wealth.

This guide explores the foundational frameworks of personal finance, helps you identify your unique savings capacity, and provides actionable strategies to optimize your financial trajectory.

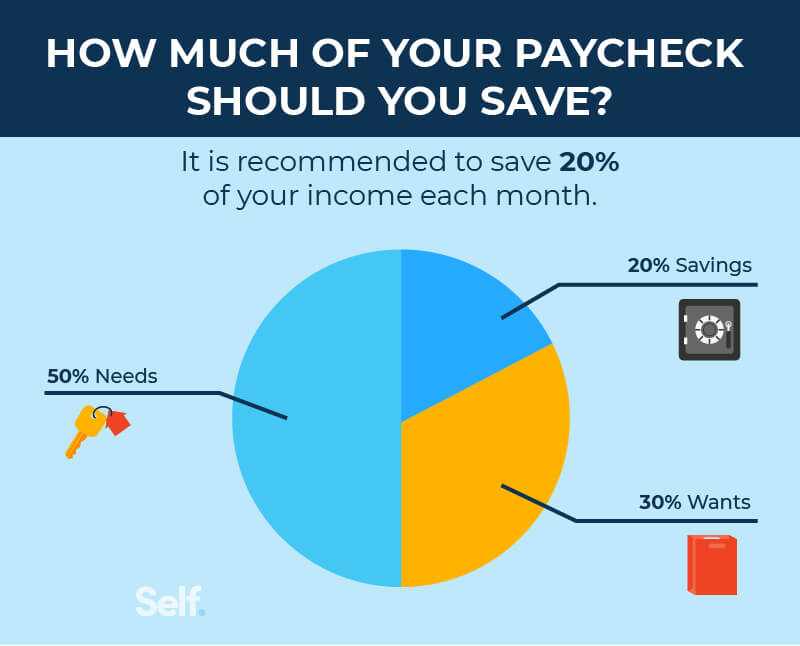

The Gold Standard: The 50/30/20 Rule

When beginning a financial journey, many experts point toward the 50/30/20 rule. Popularized by Senator Elizabeth Warren in her book All Your Worth, this framework offers a balanced approach to budgeting that ensures your future is funded while your present remains comfortable.

Understanding the 50% Needs

The first half of your after-tax income should be dedicated to “needs.” These are the non-negotiable expenses that keep your life functioning. This includes housing (rent or mortgage), utilities, groceries, transportation, insurance, and minimum debt payments. If your needs exceed 50% of your paycheck, it is a signal that you may be “house poor” or over-extended on lifestyle basics, which inevitably cannibalizes your ability to save.

Navigating the 30% Wants

The middle tier of the budget allows for “wants”—the lifestyle choices that provide enjoyment but are not strictly necessary for survival. This includes dining out, streaming subscriptions, travel, hobbies, and luxury purchases. The 50/30/20 rule acknowledges that a budget which is too restrictive often fails. By allocating 30% to your desires, you create a sustainable system where you don’t feel deprived, making it easier to stick to your long-term savings goals.

Committing the 20% to Savings

The final 20% is the engine of your financial growth. According to this rule, at least one-fifth of every paycheck should be funneled into savings, investments, and extra debt repayments (beyond the minimums). This includes contributions to retirement accounts like a 401(k) or IRA, building an emergency fund, and investing in brokerage accounts. If you can consistently hit this 20% mark, you are statistically likely to achieve financial independence far ahead of the average consumer.

Factors That Influence Your Personal Savings Rate

While 20% is an excellent benchmark, personal finance is personal for a reason. Your “ideal” savings percentage may fluctuate depending on your current life stage and economic environment.

Cost of Living and Geographic Realities

A person earning $70,000 in a rural area with low housing costs can easily save 30% or more of their income. Conversely, a professional earning the same amount in a metropolitan hub like New York or London might struggle to save 5% after paying for rent and transport. When calculating your savings goal, you must account for your “local inflation.” If you live in a high-cost area, you may need to be more aggressive about cutting “wants” to ensure your savings rate doesn’t drop to zero.

Career Stage and Earning Potential

Early in your career, your primary goal is often just to establish the habit of saving. If entry-level wages make 20% impossible, starting with 5% is better than zero. The “power of habit” ensures that as your salary increases through promotions or job-hopping, you can apply “percentage-based” thinking. Instead of increasing your lifestyle spending when you get a raise, you can direct the entirety of that raise into your savings, a concept known as avoiding “lifestyle creep.”

Debt Obligations and Interest Rates

The relationship between debt and savings is critical. If you carry high-interest debt, such as credit card balances with 20% APR, paying down that debt is mathematically equivalent to “saving” at a 20% guaranteed return. In this scenario, your paycheck should be heavily weighted toward debt elimination before you focus on building a large investment portfolio. However, low-interest debt, such as a 3% mortgage, should not discourage you from investing in the stock market, where historical returns may outpace the cost of the debt.

Building a Hierarchy of Financial Goals

Not all savings are created equal. To maximize the effectiveness of every dollar taken from your paycheck, you must prioritize where those funds go based on urgency and long-term utility.

The Emergency Fund: Your Financial Safety Net

Before you invest a single dollar in the stock market, you must establish an emergency fund. The standard recommendation is three to six months of essential living expenses. This fund serves as a buffer against job loss, medical emergencies, or unforeseen home repairs. Without this safety net, a single stroke of bad luck could force you into high-interest debt, undoing years of disciplined saving.

Retirement Contributions and Employer Matching

If your employer offers a 401(k) or similar retirement plan with a “match,” this is your first investment priority. An employer match is essentially a 100% return on your money before the market even moves. At a minimum, you should contribute enough of your paycheck to capture the full match. Failing to do so is leaving free money on the table and is one of the most common financial mistakes made by young professionals.

Saving for Large Purchases and Milestones

Once your emergency fund is set and your retirement is on track, you can begin “sinking funds” for specific goals. This might include a down payment for a home, a wedding, or a new vehicle. These funds should typically be kept in a High-Yield Savings Account (HYSA) rather than the stock market if you plan to use the money within the next three to five years, protecting your principal from short-term market volatility.

Psychological and Practical Strategies to Boost Savings

For many, the challenge isn’t the math—it’s the discipline. Human psychology is hardwired for instant gratification, making the act of saving for a distant future feel abstract and unrewarding.

The Power of Automation

The most effective way to ensure you save a specific portion of your paycheck is to remove the human element. Set up an automatic transfer that triggers the moment your direct deposit hits your account. By “hiding” the money from yourself, you adapt your spending habits to the remaining balance. If you never see the money in your checking account, you are far less likely to spend it on impulse purchases.

“Pay Yourself First” – The Mindset Shift

Most people spend their paycheck on bills, groceries, and entertainment, and then save “whatever is left over.” The problem is that, frequently, nothing is left over. The “Pay Yourself First” philosophy flips this script. You treat your savings like your most important bill. By allocating your 20% (or chosen percentage) first, you force yourself to be creative and disciplined with the remaining 80% to cover your expenses.

Rethinking Luxury and Consumerism

In a digital age fueled by social media, “Keeping up with the Joneses” has evolved into keeping up with influencers. High savings rates are often achieved not just by earning more, but by consciously choosing a simpler lifestyle. Evaluating purchases based on their “hours worked” equivalent can be a sobering and effective tool. If a $1,000 gadget represents 40 hours of your labor, is it truly worth a full week of your life?

Adjusting Your Strategy as Life Evolves

Your savings rate should not be a static number. It is a dynamic tool that should be recalibrated as your circumstances change.

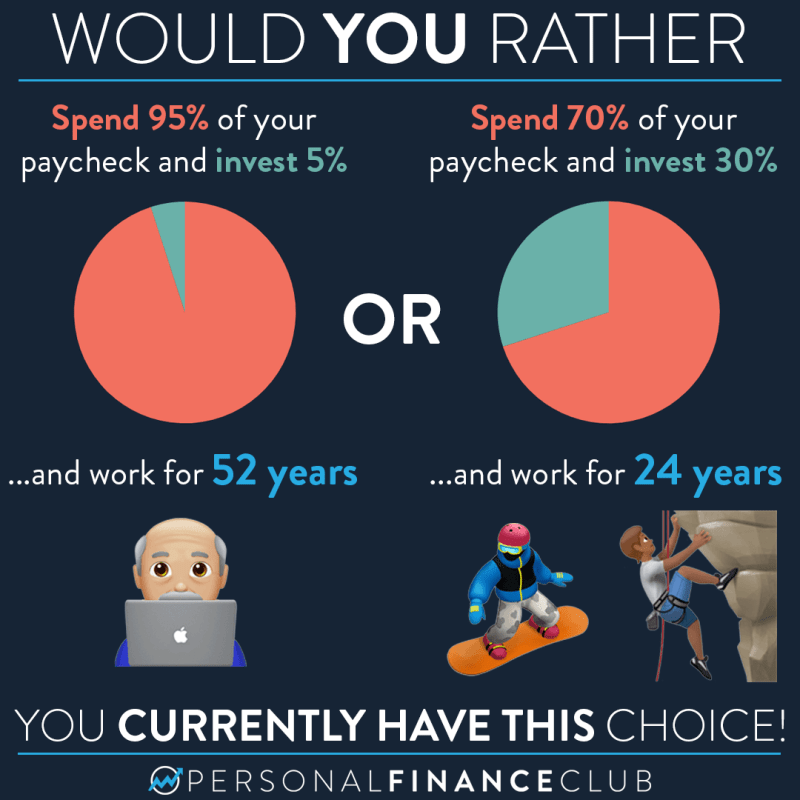

The Aggressive Savings Approach (FIRE Movement)

For those pursuing Financial Independence, Retire Early (FIRE), the 20% rule is often insufficient. Adherents to this movement frequently aim for savings rates of 50% to 70%. While this requires significant lifestyle sacrifices, it drastically shortens the timeline to retirement. If your goal is to exit the traditional workforce in your 30s or 40s, you must aggressively widen the gap between your income and your expenses.

Scaling Back During Lean Times

Life is unpredictable. There may be periods—such as during a career transition, a health crisis, or when expanding your family—where your savings rate must temporarily drop. The key is to remain intentional. Reducing your savings to 5% during a difficult year is a tactical adjustment; stopping entirely and losing the habit is a strategic failure. As soon as the “lean time” passes, the goal should be to return to your benchmark percentage immediately.

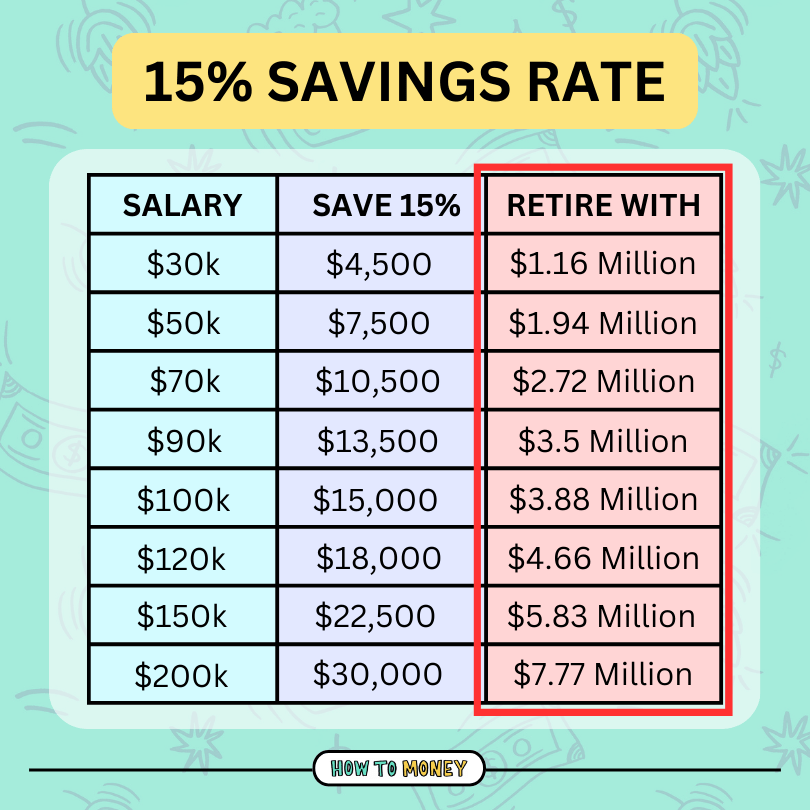

The Role of Compound Interest

The most compelling reason to save as much of your paycheck as possible as early as possible is compound interest. A dollar saved in your 20s is worth significantly more than a dollar saved in your 40s because it has more time to grow. Even a small increase in your savings rate—moving from 15% to 20%—can result in hundreds of thousands of dollars in additional wealth over a 30-year career.

Conclusion

There is no universal “perfect” number for how much of your paycheck should go to savings, but the 20% threshold remains the most robust target for the average earner. By prioritizing an emergency fund, maximizing employer benefits, and automating your contributions, you transform saving from a chore into a seamless part of your lifestyle. Ultimately, the portion of your paycheck you save today is the price you pay for the freedom you will enjoy tomorrow. Wealth is not built by what you earn, but by what you keep.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.