In the intricate world of finance, where sophisticated instruments are crafted to meet diverse investor needs and issuer requirements, the concept of “tranches” stands as a cornerstone. Far from being a mere technical term, tranches represent a fundamental mechanism for segmenting risk, tailoring investment opportunities, and optimizing capital structures. Understanding tranches is crucial for anyone delving into structured finance, securitization, or even the broader dynamics of debt markets. This article will demystify tranches, exploring their definition, diverse applications, underlying mechanics, and their profound impact on financial markets.

The Fundamental Concept of Tranches

At its core, a tranche is a segment or slice of a larger financial transaction or debt offering. The term itself, derived from French, literally means “slice” or “portion,” perfectly encapsulating its role in breaking down a whole into manageable, distinct parts. While the concept might seem complex, its purpose is elegantly simple: to cater to a variety of investor preferences regarding risk, return, and maturity by dividing a homogeneous pool of assets or a single debt offering into different classes.

Defining a Tranche

Imagine a large pie that needs to be distributed among people with different appetites and dietary restrictions. Some might want a small, sweet slice, others a larger, savory one. In finance, a “tranche” works similarly. It’s a specific portion of a larger debt issue, investment fund, or structured financial product, distinguished by its unique characteristics. These characteristics commonly include:

- Risk Profile: Different tranches often carry varying levels of credit risk, with some being more protected against losses than others.

- Maturity: Tranches can have different repayment schedules or dates when the principal is due.

- Interest Rate/Yield: Reflecting their risk and maturity, tranches will offer different coupon rates or expected returns.

- Payment Priority: Crucially, tranches are often defined by their position in the payment waterfall, determining who gets paid first in the event of cash flow generation or default.

This segmentation allows issuers to attract a wider range of investors, from conservative institutions seeking low-risk, stable returns to aggressive hedge funds willing to take on higher risk for potentially greater rewards.

Origins and Etymology

The term “tranche” entered the financial lexicon predominantly from French, meaning “slice” or “portion.” Its usage in finance gained significant traction with the rise of structured finance, particularly in the mid-20th century, as financial engineers sought ways to manage and distribute risk more effectively. While the basic idea of segmenting debt isn’t new, the formalization and widespread application of tranches as a distinct financial instrument became prominent with the innovation of securitization.

Why Tranches Exist: Managing Risk and Investment Preferences

The existence of tranches is driven by fundamental economic principles: the desire to efficiently allocate capital and manage risk. Issuers, whether corporations or financial institutions, often need to raise large sums of capital. By structuring their offerings into tranches, they can:

- Broaden Investor Base: Different tranches appeal to different types of investors with varying risk appetites and investment mandates. A pension fund might only be interested in the safest, highest-rated tranche, while a hedge fund might target the riskier, higher-yielding junior tranches.

- Reduce Funding Costs: By segmenting risk, issuers can potentially achieve a lower blended cost of capital than they would with a single, undifferentiated offering. The senior tranches might receive a very high credit rating, attracting investors at lower interest rates, which helps offset the higher rates paid on riskier tranches.

- Tailor Product to Market Demand: Tranches allow for bespoke financial products that precisely match market demand for specific risk/return profiles, maturities, or credit qualities.

For investors, tranches offer:

- Diverse Risk/Return Options: Investors can choose a tranche that perfectly aligns with their investment strategy and risk tolerance, from conservative to aggressive.

- Diversification: Investing in tranches of a securitized pool can offer exposure to a diversified set of underlying assets that might otherwise be inaccessible or too granular to invest in individually.

- Enhanced Liquidity: Well-structured and rated tranches can offer better liquidity in secondary markets compared to direct investments in the underlying, often illiquid assets.

Tranches in Practice: Diverse Applications Across Finance

While the conceptual definition of a tranche is straightforward, its application in finance is incredibly varied, extending across numerous sophisticated financial instruments. From real estate to corporate debt, tranches are a critical component in structuring complex financial deals.

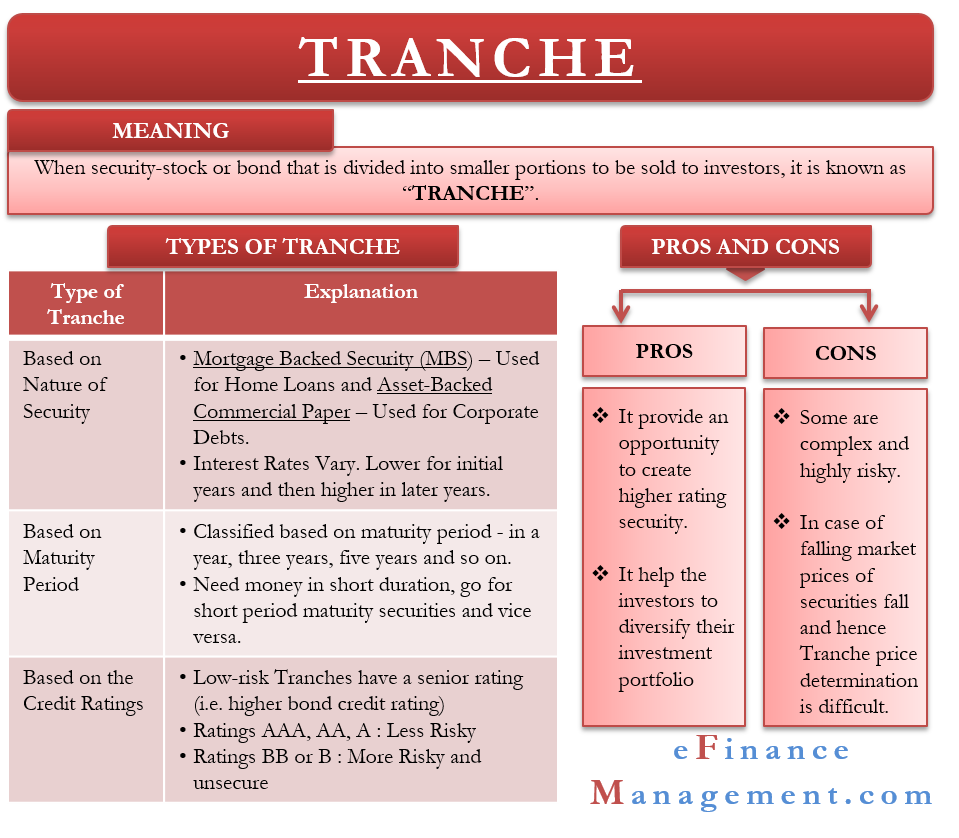

Securitization and Mortgage-Backed Securities (MBS)

Perhaps the most famous — or infamous — application of tranches is in securitization, particularly with Mortgage-Backed Securities (MBS). In an MBS, thousands of individual mortgage loans are pooled together. This large pool of future mortgage payments is then divided into various tranches.

- How it works: Investors in an MBS tranche receive payments derived from the principal and interest paid by homeowners. However, different tranches have different payment priorities. For example, a senior tranche might be paid first from the cash flows generated by the mortgages, making it less risky. Junior tranches would be paid later, after the senior tranches are satisfied, thus carrying more risk but offering potentially higher returns.

- Impact: This structure transformed the mortgage market, allowing banks to sell off mortgages, free up capital, and issue new loans. It also provided institutional investors with a new asset class linked to the housing market.

Collateralized Debt Obligations (CDOs) and Asset-Backed Securities (ABS)

Building on the MBS model, Collateralized Debt Obligations (CDOs) and other Asset-Backed Securities (ABS) represent a broader application of securitization using a wider range of underlying assets.

- CDOs: These pools can consist of corporate bonds, loans, other MBS tranches (known as CDO-squared), or even other structured products. Like MBS, CDOs are sliced into tranches, each with varying levels of risk and return depending on their seniority. CDOs gained significant notoriety during the 2008 financial crisis due to their complexity and the widespread defaults in their underlying assets.

- ABS: More generally, ABS can be backed by credit card receivables, auto loans, student loans, or equipment leases. The cash flows from these diverse assets are then used to pay investors in different tranches. These structures allow originators of consumer credit to offload risk and raise capital efficiently.

Corporate Debt and Loans

Tranches are not exclusive to securitization. They are also commonly used in corporate finance, particularly in syndicated loans and bond offerings.

- Syndicated Loans: When a company needs a very large loan, a group of banks (a syndicate) might provide the capital. This loan can be structured into different tranches, such as a “term loan A” (often with a shorter maturity and amortizing payments) and a “term loan B” (longer maturity, bullet payment, often held by institutional investors). There might also be a “revolving credit facility” tranche, which acts like a corporate credit card.

- Bond Offerings: Sometimes, a single corporate bond issuance might involve different tranches with varying maturities, coupon rates, or even different currencies, catering to distinct investor groups in different markets.

Structured Finance and Equity Offerings

Beyond debt, tranches can also be found in more specialized structured finance products and even, conceptually, in equity.

- Project Finance: Large infrastructure projects often use tranches to segment funding sources, with different tranches catering to senior lenders, mezzanine debt providers, and equity investors, each with their specific risk and return expectations.

- Preferred Stock: While technically equity, preferred stock can sometimes be seen as a tranche within a company’s capital structure, sitting between common equity and debt, offering fixed dividend payments but typically no voting rights.

Understanding Tranche Structures: Risk, Return, and Priority

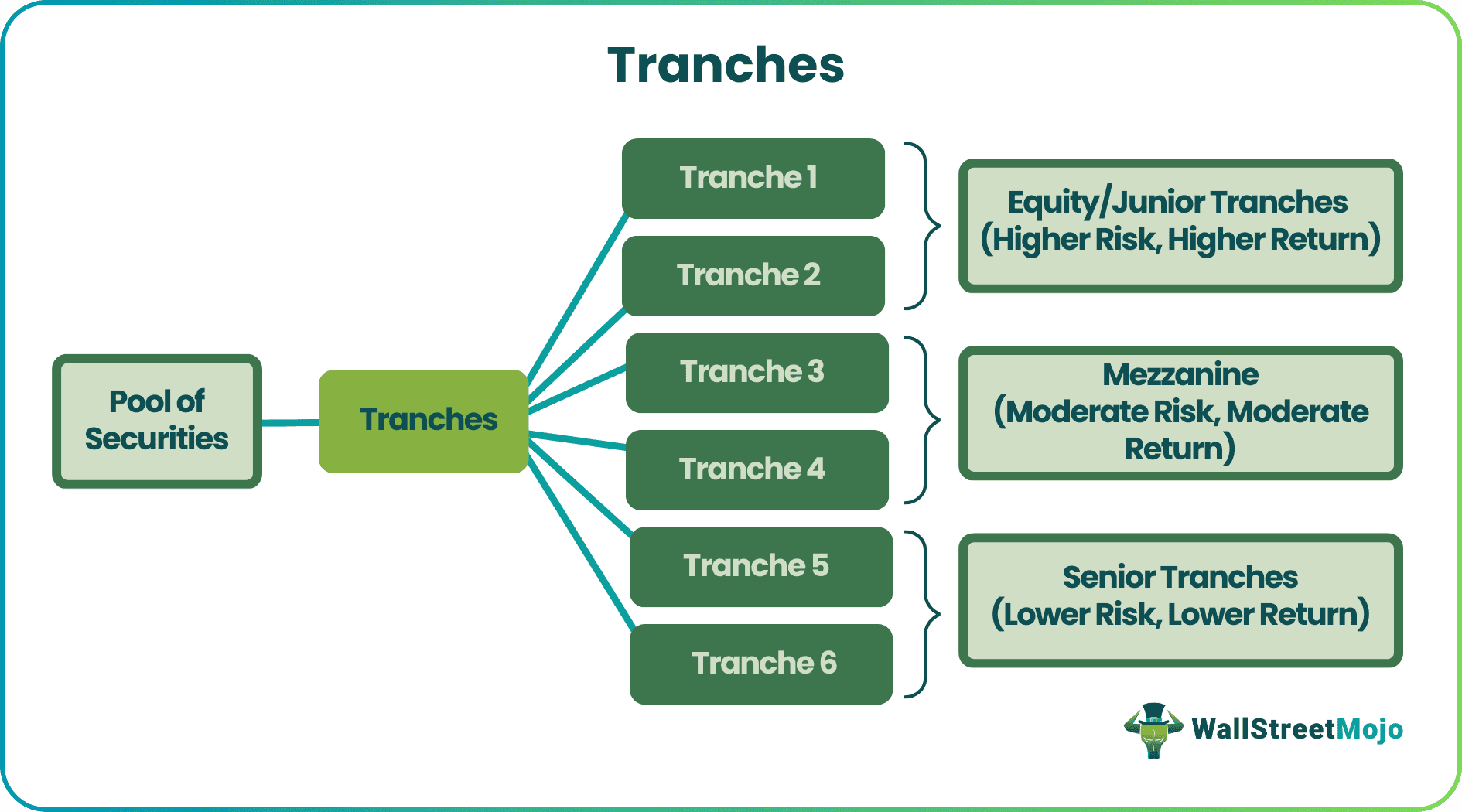

The defining characteristic of tranches lies in their hierarchical structure, often visualized as a “waterfall.” This structure dictates the order in which cash flows from the underlying assets are distributed and, critically, the order in which losses are absorbed. This priority directly translates into varying risk and return profiles for each tranche.

Senior Tranches: The First in Line

The senior tranche sits at the top of the payment waterfall. It is the safest and typically the largest portion of a structured financial product.

- Characteristics: Senior tranches are the first to receive principal and interest payments from the underlying assets. In the event of defaults in the underlying pool, the senior tranche is protected by the junior tranches, meaning losses must first deplete the junior tranches before impacting the senior tranche.

- Risk and Return: Due to their preferential payment position and greater protection, senior tranches carry the lowest credit risk within the structure. Consequently, they offer the lowest interest rates or yields, appealing to conservative investors such as pension funds, insurance companies, and banks that prioritize safety and stability. They often receive the highest credit ratings (e.g., AAA, AA).

Mezzanine Tranches: Bridging the Gap

Sitting below the senior tranche but above the equity or junior tranche, the mezzanine tranche represents an intermediate layer of risk and return.

- Characteristics: Mezzanine tranches are paid after the senior tranches are fully satisfied but before the junior tranches. They absorb losses only after the junior tranches have been wiped out.

- Risk and Return: These tranches carry moderate risk and offer higher yields than senior tranches to compensate investors for this increased risk. They appeal to investors with a balanced risk appetite who are willing to take on some additional risk for enhanced returns. Credit ratings for mezzanine tranches typically fall in the single-A or triple-B range.

Equity (Junior) Tranches: High Risk, High Reward

Also known as the “equity tranche,” “first-loss tranche,” or “residual tranche,” this is the riskiest and typically the smallest portion of the structure.

- Characteristics: The equity tranche is the last to receive payments from the cash flows but the first to absorb losses from defaults in the underlying assets. If the underlying assets perform poorly, the equity tranche is the first to suffer, potentially losing its entire investment.

- Risk and Return: This high-risk position means the equity tranche offers the highest potential returns if the underlying assets perform well. It attracts aggressive investors such as hedge funds and private equity firms who are comfortable with substantial risk in pursuit of outsized returns. Equity tranches are often unrated or carry very low speculative-grade ratings.

Waterfall Payments: How Cash Flows are Distributed

The “waterfall” is the literal mechanism by which cash flows generated by the underlying assets are distributed to the various tranches.

- Expenses First: Typically, the first money out of the pool goes to cover servicing fees, administrative costs, and trustee fees.

- Senior Tranche: After expenses, the senior tranche receives its scheduled principal and interest payments.

- Mezzanine Tranches: Once the senior tranche is paid, any remaining cash flow goes to pay the mezzanine tranches.

- Equity (Junior) Tranche: Finally, if there is still cash flow remaining after all other tranches are paid, it flows to the equity tranche.

This sequential payment mechanism is fundamental to understanding the risk allocation inherent in tranche structures. Any shortfall in the underlying asset cash flows will affect the lowest tranches first, cascading upwards if the losses are severe enough.

Advantages and Disadvantages of Tranches for Investors and Issuers

The innovative design of tranches offers significant benefits to both those who create them (issuers) and those who invest in them. However, like any complex financial instrument, tranches also come with inherent risks and have faced significant criticism, particularly in the wake of financial crises.

Benefits for Issuers: Access to Capital and Tailored Offerings

For financial institutions, corporations, and other entities needing to raise capital, tranches provide several compelling advantages:

- Efficient Capital Raising: By segmenting risk, issuers can tap into a broader investor base. This allows them to raise larger sums of capital than might be possible with a single, undifferentiated offering, as they can cater to a wider spectrum of risk appetites.

- Lower Overall Funding Costs: Attracting highly conservative investors to senior tranches at very low interest rates helps to offset the higher yields demanded by investors in riskier junior tranches. This blending can result in a lower average cost of capital for the issuer.

- Risk Transfer and Balance Sheet Management: Through securitization, issuers can move assets off their balance sheets, transferring the associated risks to investors. This frees up regulatory capital, enhances liquidity, and allows them to originate new loans or investments.

- Customization: Tranches allow issuers to create highly customized financial products that precisely meet the demands of specific market segments, optimizing the sale and pricing of their offerings.

Benefits for Investors: Diverse Risk/Return Profiles

Investors find tranches attractive for the flexibility and diversity they offer:

- Tailored Risk Exposure: Investors can select tranches that align perfectly with their specific risk tolerance and investment objectives, from very low-risk, stable income streams to high-risk, high-reward opportunities.

- Access to Diversified Asset Pools: Tranches in securitized products offer investors exposure to a diversified pool of underlying assets (e.g., thousands of mortgages or auto loans) that would be impractical or impossible to invest in individually.

- Potentially Higher Yields: For those willing to take on more risk, mezzanine and equity tranches can offer significantly higher yields compared to traditional corporate bonds or government securities, reflecting the compensation for first-loss exposure.

- Liquidity in Certain Tranches: Well-rated and widely traded senior tranches of securitized products can offer good liquidity in secondary markets, allowing investors to buy and sell relatively easily.

Risks and Criticisms: Complexity, Opacity, and Systemic Vulnerability

Despite their advantages, tranches have faced substantial criticism, especially after the 2008 global financial crisis.

- Complexity and Opacity: The primary drawback is their inherent complexity. Understanding the true risk profile of a tranche requires deep analysis of the underlying assets, the legal structure of the waterfall, and potential correlation risks. This complexity can lead to opacity, making it difficult for investors (and even regulators) to fully grasp the embedded risks.

- Reliance on Credit Rating Agencies: Investors heavily relied on credit rating agencies to assess the risk of tranches, particularly the highly-rated senior tranches. However, the models used by these agencies proved fallible, especially when the underlying assets (like subprime mortgages) deteriorated rapidly and unexpectedly.

- Systemic Risk: The widespread use and interconnectedness of structured products built with tranches (especially CDOs) meant that when the underlying housing market collapsed, the defaults cascaded rapidly through the financial system, leading to a systemic crisis. The failure of one part of the chain could trigger widespread losses due to counterparty risk and leveraged positions.

- Moral Hazard: Critics argue that securitization and tranches created a “moral hazard,” where originators of loans had less incentive to perform thorough due diligence because they could quickly sell off the loans to investors, transferring the risk.

The Role of Credit Rating Agencies

Credit rating agencies play a crucial role in the tranche ecosystem, assigning ratings (e.g., AAA, BBB, CCC) to different tranches based on their assessment of credit risk. These ratings are critical because many institutional investors are legally or internally restricted to investing only in tranches above a certain rating threshold (e.g., investment grade). The controversy surrounding these agencies during the 2008 crisis highlighted the challenges of rating complex, highly structured financial products, leading to calls for greater oversight and reform.

Regulatory Scrutiny and Evolution of Tranches

The profound impact of tranches on the 2008 financial crisis spurred significant regulatory reform and a re-evaluation of structured finance practices. The lessons learned have shaped how tranches are designed, rated, and traded today.

Lessons from the 2008 Financial Crisis

The crisis exposed several critical vulnerabilities related to tranches:

- Underestimation of Correlation Risk: Rating agencies and investors underestimated the degree to which various seemingly independent underlying assets (e.g., mortgages across different regions) could default simultaneously during a systemic downturn.

- The “Tranche of Tranches” Problem: CDOs of MBS (CDO-squared) created layers of complexity where even highly-rated tranches of these layered products proved highly vulnerable when the original underlying mortgages began to default en masse.

- Lack of Transparency: The complexity made it nearly impossible for many market participants to accurately price and manage the risks associated with these instruments, contributing to illiquidity and panic when the crisis hit.

- “Originate to Distribute” Model Flaws: The ease with which risk could be transferred through securitization, enabled by tranches, incentivized a focus on loan origination volume rather than loan quality for some institutions.

Dodd-Frank and Other Regulatory Reforms

In response to the crisis, governments and regulators worldwide implemented significant reforms aimed at increasing transparency, accountability, and stability in financial markets. In the United States, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 introduced several provisions directly impacting structured finance and tranches:

- Risk Retention (Skin in the Game): Dodd-Frank mandated that securitizers retain a portion of the credit risk of the assets they securitize (typically 5%), aligning their incentives with investors and ensuring they have “skin in the game.” This was intended to mitigate the moral hazard of the “originate-to-distribute” model.

- Increased Disclosure Requirements: Regulators imposed stricter disclosure requirements for structured products, aiming to provide investors with more comprehensive and understandable information about the underlying assets and the structure of tranches.

- Oversight of Credit Rating Agencies: The Act also aimed to improve the oversight and accountability of credit rating agencies, reducing their reliance on issuer-paid models and promoting greater transparency in their methodologies.

- Volcker Rule: While not directly about tranches, the Volcker Rule (part of Dodd-Frank) generally prohibited banks from engaging in proprietary trading or owning hedge funds and private equity funds, which had often been major players in the market for riskier tranches.

The Future of Tranches in Financial Markets

Despite the challenges and regulatory overhaul, tranches remain an indispensable tool in modern finance. They continue to serve the fundamental purpose of segmenting risk and matching investor preferences. The future of tranches likely involves:

- Greater Transparency and Standardization: Ongoing efforts to standardize the underlying assets and provide clearer, more accessible information about tranche structures will be crucial for rebuilding investor confidence.

- Evolution of Rating Methodologies: Credit rating agencies continue to refine their models, incorporating lessons from past crises and focusing more on stress testing and scenario analysis.

- Focused Application: While complex structured products like synthetic CDOs of CDOs might be less prevalent, tranches will continue to be vital in simpler, more transparent securitizations (like those backed by high-quality auto loans or student loans) and in corporate debt markets.

- Technological Advancement (FinTech): Emerging technologies like blockchain could potentially enhance transparency and efficiency in the tracking and trading of tranches, providing immutable records of ownership and cash flow distribution.

In conclusion, tranches are more than just financial jargon; they are the architectural beams of modern structured finance. They allow for the efficient allocation of capital and the precise tailoring of risk and reward profiles across various financial instruments. While the complexities and risks associated with tranches were dramatically exposed during the 2008 crisis, continuous innovation, coupled with robust regulatory frameworks, ensures their continued, albeit more cautious, role in the evolving landscape of global financial markets. Understanding “what are tranches” is therefore essential for comprehending the mechanics of capital formation, risk management, and investment opportunities in the 21st century financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.