In the world of finance, few terms carry as much weight as “total equity.” Whether you are an individual investor looking at a company’s balance sheet, a business owner trying to assess your firm’s value, or a homeowner tracking your personal net worth, total equity is the ultimate metric of financial health. At its core, equity represents what is truly “owned” after all obligations have been met. It is the residual interest in assets after deducting liabilities, serving as a critical barometer for solvency, stability, and growth potential.

Understanding total equity is not just an exercise for accountants; it is a fundamental skill for anyone looking to navigate the complexities of the modern economy. This guide will break down the components of total equity, explore its significance in corporate and personal finance, and provide actionable insights on how to build and leverage it for long-term wealth.

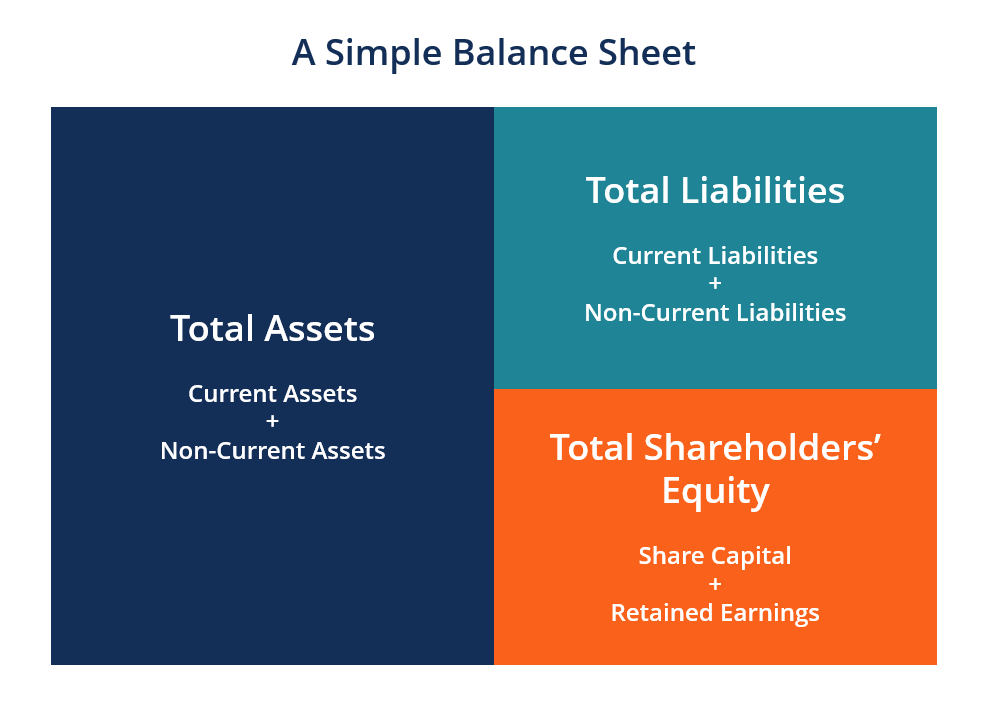

Defining Total Equity: The Core Equation of Net Worth

To understand total equity, one must first understand the fundamental accounting equation that governs every financial statement in the world: Assets = Liabilities + Equity. When we rearrange this formula to solve for equity, we get: Total Equity = Total Assets – Total Liabilities.

The Accounting Equation: Assets, Liabilities, and Equity

Assets are everything a person or business owns that has value—cash, real estate, inventory, equipment, and intellectual property. Liabilities are the obligations or debts owed to outside parties—loans, mortgages, accounts payable, and taxes. Total equity is what remains for the owners once all those debts are theoretically paid off.

In the context of a corporation, this is often referred to as “Shareholder’s Equity.” In the context of an individual, it is commonly known as “Net Worth.” Regardless of the terminology, the principle remains the same: equity represents the “book value” of ownership.

Why Total Equity Represents True Ownership

It is a common mistake to conflate high assets with high wealth. A company might possess $10 million in state-of-the-art machinery, but if it took $9.5 million in high-interest loans to acquire that machinery, the total equity is only $500,000.

Total equity serves as a “buffer” for a business. In times of financial distress, a healthy equity position ensures that a company can cover its losses without falling into insolvency. For investors, equity represents their claim on the company’s earnings and assets, providing a sense of security that the business has a solid foundation of internal funding.

The Components of Shareholder’s Equity

For a business, total equity is rarely a single number derived from a simple subtraction. Instead, it is composed of several distinct accounts that tell a story about where the company’s capital came from and how it has been managed over time.

Common and Preferred Stock

The most visible component of equity is the capital contributed by shareholders. Common stock represents the basic ownership interest in a corporation, usually providing voting rights and a claim on dividends. Preferred stock acts as a hybrid; it usually does not offer voting rights but gives holders a higher claim on assets and earnings (dividends) than common stockholders. When a company issues shares, the par value of those shares is recorded in the equity section of the balance sheet.

Retained Earnings: The Growth Engine

Perhaps the most important component of total equity is retained earnings. This is the cumulative amount of net income that a company has decided to keep rather than distribute to shareholders as dividends. Retained earnings represent the “engine” of a company’s internal growth. When a business is profitable and reinvests those profits into new projects, research, or debt reduction, its total equity increases. Conversely, consistent losses will erode retained earnings and can eventually lead to negative equity.

Treasury Stock and Additional Paid-in Capital

Other technical components include Additional Paid-in Capital (APIC), which reflects the amount investors paid over the par value of the stock. On the flip side, Treasury Stock refers to shares that the company has bought back from the open market. Treasury stock is a “contra-equity” account, meaning it actually reduces the total equity figure. Companies often buy back shares to increase the value of remaining shares or to improve financial ratios.

Analyzing Total Equity for Business Success

For business owners and investors, total equity is more than just a line item; it is a diagnostic tool used to measure performance and risk. By analyzing equity in relation to other financial figures, one can gain deep insights into a company’s operational efficiency.

Equity as a Metric for Solvency

Solvency refers to a company’s ability to meet its long-term obligations. A high level of total equity relative to debt suggests a solvent, stable company. Financial analysts often look at the Debt-to-Equity Ratio. A high ratio indicates that a company is financing its growth aggressively through debt, which can be risky if interest rates rise or revenues dip. A lower ratio suggests a more conservative, equity-funded approach, which is generally viewed as safer during economic downturns.

Return on Equity (ROE) and Performance Analysis

One of the most popular metrics for investors is Return on Equity (ROE). This is calculated by dividing net income by total equity. ROE measures how effectively a company’s management is using the shareholders’ capital to generate profit. An ROE of 15-20% is generally considered excellent. It tells the story of efficiency; if a company can generate high profits with a relatively small amount of equity, it is a sign of a high-moat, high-efficiency business.

Negative Total Equity: Red Flags and Risk Management

It is possible for a company to have negative total equity. This occurs when total liabilities exceed total assets. While this is often a sign of impending bankruptcy, it can also occur in specific scenarios, such as when a company takes on massive debt to fund a successful share buyback program or experiences temporary but significant accounting losses. However, for the average investor, negative equity is a major red flag that requires immediate and thorough investigation.

Total Equity in Personal Finance: Building Wealth

While “total equity” sounds like corporate jargon, it is the most vital concept in personal finance. In this context, we look at your personal balance sheet to determine your net worth.

Home Equity and Real Estate Assets

For most individuals, the largest contributor to their total equity is home equity. This is the difference between the fair market value of your home and the remaining balance on your mortgage. As you make monthly payments—specifically the portion that goes toward the principal—and as the property value appreciates, your equity grows. Home equity is a powerful financial tool, as it can be accessed through Home Equity Lines of Credit (HELOCs) or home equity loans to fund education, renovations, or other investments.

Net Worth Tracking for Personal Financial Freedom

Your “Total Personal Equity” or Net Worth is the ultimate scorecard of your financial life. It includes your bank accounts, retirement funds (401k, IRA), brokerage accounts, and physical assets, minus your student loans, credit card debt, and mortgages.

Tracking this number monthly or annually is essential for long-term planning. It allows you to see past the “noise” of your monthly salary and focus on whether you are actually accumulating value. True financial independence is reached when your total equity is large enough to generate sufficient passive income to cover your living expenses.

Strategies to Increase Total Equity Over Time

Building equity is a marathon, not a sprint. It requires a disciplined approach to both increasing assets and aggressively managing liabilities.

Debt Reduction and Liability Management

The fastest way to increase total equity is often to reduce liabilities. Every dollar of debt repaid is a dollar added to your equity. In a business context, this might mean refinancing high-interest debt to lower interest costs and using the savings to pay down principal. In personal finance, using strategies like the “debt snowball” or “debt avalanche” to eliminate consumer debt directly boosts your net worth, as it stops the “leakage” of interest payments that otherwise erode your wealth.

Asset Appreciation and Reinvestment

The second pillar of equity growth is the acquisition of appreciating assets. This involves moving capital from “depreciating assets” (like cars or gadgets) into “appreciating assets” (like stocks, real estate, or a business).

For a business, this means reinvesting profits into high-return projects rather than letting cash sit idle. For an individual, it means automating contributions to investment accounts. Over time, the power of compound interest turns small amounts of equity into substantial wealth. By consistently focusing on the equity side of the balance sheet—rather than just the income statement—you ensure that you are building a lasting financial legacy that can withstand market volatility and provide long-term security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.