The bedrock of economies worldwide, the small business represents far more than just a diminutive version of a corporate giant. It embodies entrepreneurship, fuels local communities, and serves as a vital engine for innovation and job creation. But what exactly defines a small business, and why is understanding its characteristics crucial for anyone looking to enter the entrepreneurial landscape, invest in local economies, or simply appreciate its profound impact? In the realm of money and finance, defining and understanding the small business is paramount for effective financial planning, investment strategies, and economic policy.

Defining the Small Business: More Than Just Size

While the term “small” might imply simplicity, the definition of a small business is multifaceted, often encompassing both quantitative and qualitative criteria. These definitions are crucial for various purposes, including access to funding, tax benefits, and regulatory compliance, making them a cornerstone of business finance.

Quantitative Metrics: The Numbers Game

The most straightforward way to define a small business involves numerical thresholds. These metrics often vary significantly by country, industry, and the specific agency providing the definition.

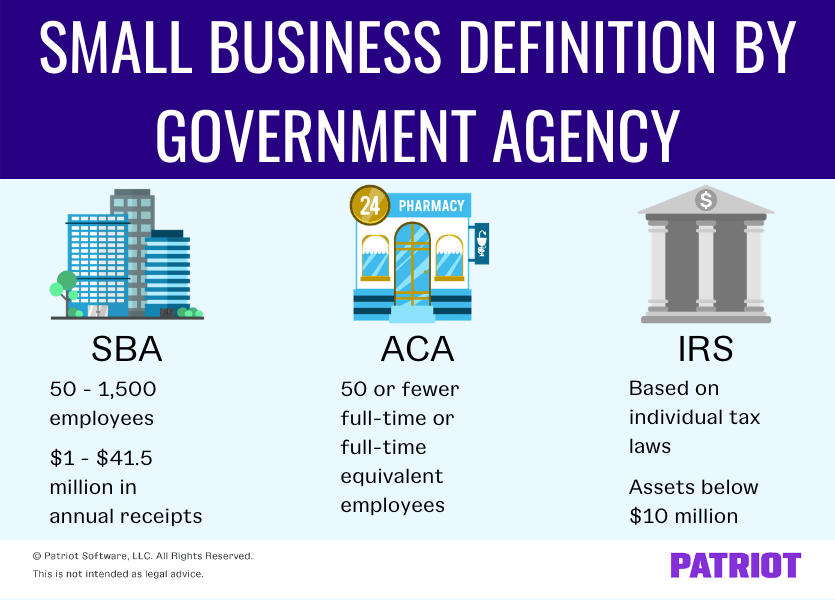

- Employee Count: This is perhaps the most common metric. In the United States, the U.S. Small Business Administration (SBA) often defines a small business as one with fewer than 500 employees, though this can range from 100 to 1,500 depending on the specific industry. In contrast, the European Union typically uses thresholds of fewer than 50 employees for a “small” enterprise and fewer than 250 for a “medium-sized” enterprise. These numbers directly impact a business’s operational costs, payroll management, and eligibility for certain financial programs.

- Annual Revenue/Turnover: Another critical financial metric, annual revenue, is frequently used. For instance, the SBA sets revenue thresholds that can vary widely by industry, from under $1 million for some agricultural businesses to over $40 million for certain manufacturing sectors. These revenue ceilings determine a business’s scale of operations and its ability to compete in specific markets, directly influencing its financial viability and potential for growth.

- Assets: Less commonly, the total value of a company’s assets might be used as a defining characteristic. This is particularly relevant in capital-intensive industries where significant equipment or property investments are required. However, for many service-based small businesses, asset value is a less indicative measure of “smallness.”

Qualitative Aspects: Beyond the Figures

Beyond mere numbers, qualitative characteristics offer a deeper understanding of what constitutes a small business, particularly from an operational and strategic finance perspective.

- Independent Ownership and Management: A hallmark of small businesses is that they are typically owned and operated by a single individual or a small group of individuals. Decision-making is often centralized, and the owners have direct involvement in daily operations. This contrasts sharply with larger corporations, which have diffused ownership and professional management structures. This independence often means greater agility and faster decision-making, which can be a financial advantage.

- Localized Operations: Many small businesses serve a local or regional market rather than having a national or international presence. While e-commerce has blurred these lines, the core customer base and supply chain for many remain geographically concentrated. This local focus can build strong community ties, but also limit market reach and potential for exponential financial growth.

- Limited Market Share: By definition, a small business typically holds a relatively small share of its overall market. It often operates in niche markets or competes on factors other than pure scale, such as specialized service, unique products, or personalized customer experiences. This can allow them to thrive without directly competing head-on with larger entities, but also means their revenue streams might be less diversified.

Diverse Structures of Small Businesses: Financial and Legal Implications

The legal and financial structure chosen for a small business has profound implications for liability, taxation, administrative burden, and fundraising capabilities. Understanding these differences is crucial for any aspiring entrepreneur or financial advisor.

Common Legal Structures

- Sole Proprietorship: This is the simplest and most common form, where the business is legally indistinguishable from its owner. All profits flow directly to the owner, but the owner also bears unlimited personal liability for business debts and obligations. From a financial perspective, it offers ease of setup and minimal ongoing costs, but exposes personal assets to business risks.

- Partnership: Involves two or more individuals who agree to share in the profits or losses of a business. General partnerships entail unlimited liability for all partners, while limited partnerships (LP) and limited liability partnerships (LLP) offer some protection for certain partners. Financially, partnerships allow for pooled resources and expertise but require careful consideration of profit-sharing and liability agreements.

- Limited Liability Company (LLC): An LLC combines the pass-through taxation benefits of a sole proprietorship or partnership with the limited liability protection of a corporation. Owners (members) are not personally responsible for the company’s debts. This hybrid structure is immensely popular for small businesses due to its balance of protection and financial flexibility.

- Corporation (S-Corp & C-Corp): A corporation is a separate legal entity from its owners (shareholders). C-corporations face “double taxation” (corporate profits taxed, and then dividends to shareholders taxed). S-corporations avoid double taxation by passing income and losses directly to shareholders’ personal income. Corporations offer the strongest liability protection and facilitate easier fundraising through stock issuance, but come with higher administrative costs and compliance burdens. The choice between S-Corp and C-Corp is a critical financial decision based on income levels and growth projections.

Business Models and Operating Styles

Small businesses also differentiate themselves through their operational models and how they generate income.

- Brick-and-Mortar: Traditional businesses with a physical storefront or office, relying on foot traffic and local clientele. These often entail significant upfront capital for rent, fit-out, and inventory, and ongoing operational costs.

- E-commerce: Businesses conducted entirely or primarily online, offering products or services through websites or digital platforms. Lower overheads for physical premises can make these financially appealing, with wider market reach but intense online competition.

- Franchises: A business model where an individual (franchisee) purchases the right to operate a business using the established brand, systems, and processes of another company (franchisor). This offers a proven business model and brand recognition but involves franchise fees, royalties, and adherence to strict operational guidelines, all of which are critical financial considerations.

- Service-Based Businesses: Offer intangible services rather than physical products (e.g., consulting, graphic design, cleaning services). These often have lower startup costs, relying more on expertise and intellectual capital, and often have higher profit margins per transaction.

The Economic and Financial Significance of Small Businesses

Small businesses are far from insignificant; they are indispensable to the global economy, acting as crucial drivers of financial health, job creation, and innovation.

Engine of Job Creation

Across developed economies, small businesses are responsible for the vast majority of net new jobs. They provide opportunities for diverse skill sets and are often more adaptable to local labor market needs than larger corporations. This job creation translates directly into economic stability, consumer spending power, and overall financial well-being for communities.

Incubators of Innovation and Competition

Small businesses are often at the forefront of innovation. Their agility, less bureaucratic structures, and closer connection to niche customer needs allow them to experiment with new products, services, and business models. This constant experimentation fosters competition, which benefits consumers through lower prices, higher quality goods, and a wider range of choices. From a financial perspective, small businesses often fill market gaps that large corporations might overlook, leading to new revenue streams and investment opportunities.

Pillars of Local Economies

Small businesses form the backbone of local economies. They source goods and services locally, keep money circulating within communities, and contribute to the unique character and vibrancy of neighborhoods. This localized economic activity generates tax revenue, supports local supply chains, and provides essential services that enhance the quality of life, all contributing to a robust local financial ecosystem. Investing in local small businesses is often seen as a direct investment in the community’s future.

Financial Management: The Lifeblood of Small Business Success

For any small business, robust financial management is not merely an administrative task; it is the absolute foundation for survival, growth, and long-term sustainability. Without sound financial practices, even the most innovative ideas can fail.

Access to Capital and Funding

One of the biggest financial challenges for small businesses is securing adequate capital.

- Bootstrapping: Many small businesses start by self-funding, using personal savings, credit cards, or early profits to finance operations. While it minimizes debt, it can limit growth potential.

- Loans: Traditional bank loans, lines of credit, and government-backed loans (like SBA loans in the U.S.) are primary sources of debt financing. Eligibility often depends on a solid business plan, collateral, and a good credit history.

- Grants: Certain industries or types of businesses may qualify for government or private grants, which do not need to be repaid. These are highly competitive but offer non-dilutive funding.

- Equity Financing: For high-growth potential businesses, seeking investment from angel investors or venture capitalists means giving up a share of ownership in exchange for capital. This is less common for traditional “small businesses” but can be transformative for scalable ventures.

- Crowdfunding: Platforms allow businesses to raise small amounts of capital from a large number of individuals, either as donations, pre-orders, or in exchange for equity.

Cash Flow Management and Budgeting

Effective management of cash flow – the money flowing in and out of the business – is critical. Many small businesses fail not due to a lack of profitability, but due to poor cash flow.

- Monitoring and Forecasting: Regularly tracking income and expenses, and accurately forecasting future cash inflows and outflows, allows businesses to anticipate shortages or surpluses.

- Expense Control: Maintaining tight control over operational expenses is paramount, particularly in the early stages.

- Accounts Receivable/Payable: Efficiently managing invoicing, collections, and vendor payments ensures a healthy cash balance.

- Budgeting: Developing and adhering to a comprehensive budget helps allocate resources effectively, prioritize spending, and track financial performance against goals.

Profitability and Pricing Strategies

Understanding profitability involves more than just revenue; it’s about the bottom line.

- Cost of Goods Sold (COGS): Accurately calculating the direct costs associated with producing goods or services.

- Operating Expenses: Managing indirect costs such as rent, utilities, salaries, and marketing.

- Pricing Strategy: Developing a pricing model that covers costs, generates a healthy profit margin, and remains competitive in the market. This often involves considering value-based pricing, cost-plus pricing, or competitive pricing.

- Break-Even Analysis: Determining the sales volume needed to cover all costs, a crucial step for setting targets and evaluating viability.

Navigating Challenges and Embracing Opportunities

Small businesses face a unique set of challenges but also possess inherent advantages that allow them to thrive in dynamic market conditions.

Key Financial Challenges

- Limited Resources: Scarcity of capital, personnel, and time can constrain growth and innovation.

- Market Volatility: Small businesses are often more susceptible to economic downturns, supply chain disruptions, and sudden shifts in consumer demand.

- Competition: Battling larger, more established players with greater financial muscle and marketing budgets.

- Regulatory Burden: Complying with taxes, labor laws, and industry-specific regulations can be disproportionately costly for smaller entities.

- Talent Acquisition: Attracting and retaining skilled employees can be challenging when competing with larger companies offering more extensive benefits.

Strategic Opportunities for Growth

- Niche Market Specialization: Excelling in a highly specific market segment where larger companies may not find it profitable to compete.

- Agility and Adaptability: The ability to pivot quickly in response to market changes or customer feedback, without layers of bureaucracy.

- Personalized Customer Service: Building strong, lasting relationships with customers through superior, tailored experiences.

- Leveraging Technology (Financially Smart Tech): Adopting cost-effective digital tools for accounting, marketing, inventory management, and e-commerce can level the playing field. These are not “tech trends” but rather “financial tools” that optimize operations and reduce costs.

- Community Engagement: Building a loyal local customer base through community involvement and strong local branding (from a financial and trust perspective).

Conclusion

The small business, in its myriad forms and functions, is a powerful force that underpins economic stability and progress. Far from a simple concept, it is a complex entity defined by quantitative metrics and qualitative characteristics, governed by crucial legal and financial structures, and driven by entrepreneurial spirit. From generating the majority of new jobs to fostering innovation and supporting local economies, its impact is undeniable.

For anyone involved in finance, investment, or entrepreneurship, understanding “what is the small business” is not merely an academic exercise. It is a fundamental requirement for making informed decisions, allocating resources effectively, and contributing to a resilient and prosperous economic future. The challenges are real, but the opportunities for financial success, personal fulfillment, and societal contribution remain boundless for those who master the art and science of operating a small business.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.