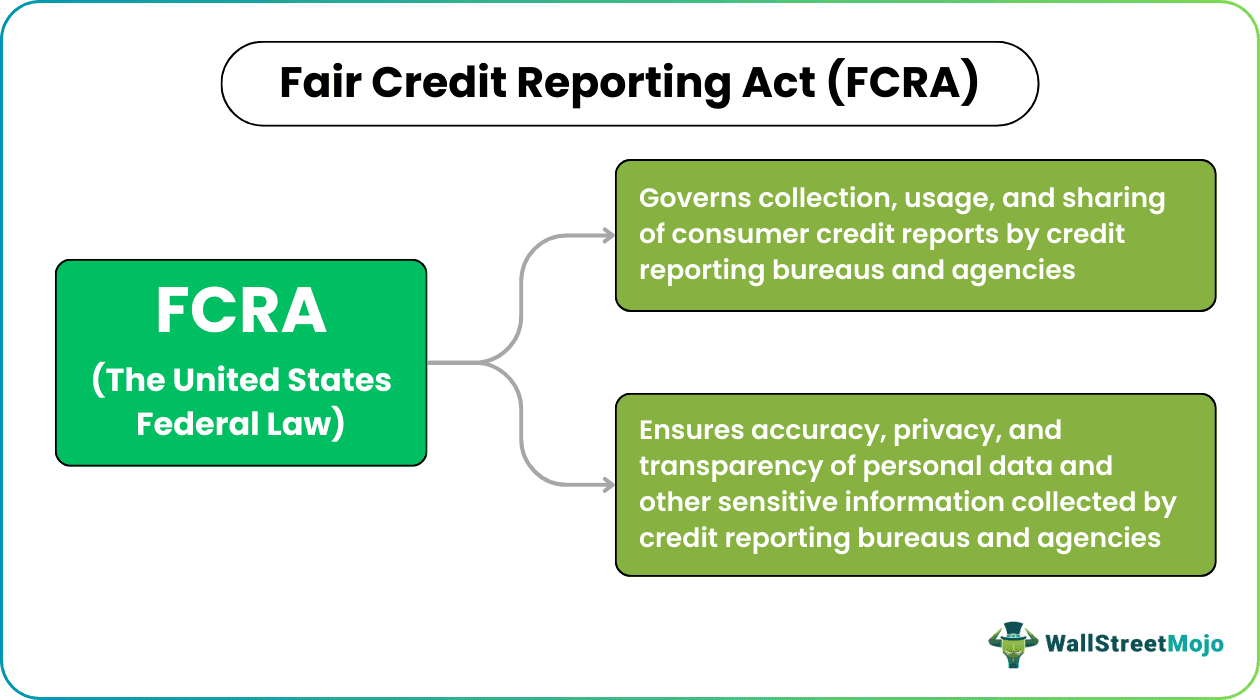

In the intricate world of personal finance, where access to credit dictates everything from purchasing a home to securing a job, understanding the bedrock principles that govern this system is paramount. At the heart of these principles lies the Fair Credit Reporting Act (FCRA), a pivotal piece of United States federal legislation enacted in 1970. Its primary purpose is not merely administrative; it is a profound commitment to fairness, accuracy, and privacy in consumer credit reporting, safeguarding the financial reputation and opportunities of every American.

The FCRA serves as the vital regulatory framework that dictates how credit reporting agencies (CRAs) – such as Equifax, Experian, and TransUnion – collect, use, and disseminate consumer financial data. It also outlines the responsibilities of those who furnish this data, like banks and lenders, and those who use it, such as employers and landlords. In an age where digital footprints are increasingly scrutinized, the FCRA’s role in protecting consumer data against inaccuracies and misuse is more critical than ever, forming the bedrock upon which sound personal and business financial decisions are made.

Cornerstone of Consumer Credit Protections

The FCRA was born out of a recognized need to standardize and regulate an industry that, prior to its enactment, operated with little oversight, leaving consumers vulnerable to erroneous information and privacy breaches. Its foundational objective is to ensure that the information compiled about individuals for credit-related decisions is accurate, relevant, and kept confidential, fostering a trustworthy financial environment.

Ensuring Accuracy and Data Integrity

Imagine applying for a mortgage or a car loan, only to be denied due to information on your credit report that is entirely incorrect – a reported late payment you never made, an account that isn’t yours, or a debt that has already been settled. Before the FCRA, such scenarios were far too common, with little recourse for the affected individual. The Act directly addresses this vulnerability by imposing strict obligations on all parties involved in the credit reporting process to ensure accuracy.

Credit reporting agencies are mandated to implement reasonable procedures to ensure the maximum possible accuracy of the information they collect and report. Similarly, information furnishers – financial institutions, creditors, and collection agencies – are held responsible for providing accurate and complete data to the CRAs. When a consumer disputes an item on their report, both the CRA and the furnisher have a legal obligation to investigate the discrepancy promptly and thoroughly. This commitment to data integrity is crucial because credit reports are not just historical records; they are predictive tools that influence future financial opportunities, making accuracy non-negotiable for fair financial assessment.

Safeguarding Consumer Privacy

Beyond accuracy, privacy stands as another pillar of the FCRA. The Act strictly limits who can access a consumer’s credit report and under what circumstances, introducing the concept of “permissible purpose.” This means that an entity cannot simply pull your credit report without a legitimate, legally sanctioned reason.

Permissible purposes typically include applications for credit, insurance, employment, housing, or legitimate business transactions initiated by the consumer. For instance, a bank assessing your loan application has a permissible purpose, as does a landlord considering your rental application. However, a nosy neighbor or a random business conducting market research does not. This provision is vital in preventing unauthorized access to sensitive financial information, protecting individuals from potential fraud, identity theft, and unwarranted scrutiny. The FCRA ensures that your financial narrative, as told through your credit report, remains largely a private matter, accessible only when a genuine and legal need arises.

Empowering Consumers with Fundamental Rights

A critical aspect of the FCRA’s purpose is to level the playing field between powerful financial institutions and individual consumers. It grants consumers an array of fundamental rights designed to provide transparency, recourse, and control over their financial information, ensuring they are not passive subjects in the credit reporting ecosystem.

The Right to Access and Review Your Credit Report

One of the most empowering provisions of the FCRA is the right for consumers to access their own credit reports. Annually, every individual is entitled to a free credit report from each of the three major credit reporting agencies – Equifax, Experian, and TransUnion – via the official website, AnnualCreditReport.com. This right is not merely a formality; it is a crucial tool for financial vigilance.

Regularly reviewing your credit reports allows you to verify the accuracy of the information, identify any unauthorized accounts or inquiries, and detect potential signs of identity theft. It empowers you to understand what lenders and others see when they assess your creditworthiness, giving you the opportunity to proactively manage and improve your financial profile. This access ensures that consumers are informed participants in their own financial journey, rather than being left in the dark about the data that profoundly impacts their lives.

The Right to Dispute Inaccurate Information

Perhaps the most direct form of consumer empowerment under the FCRA is the right to dispute inaccurate or incomplete information on a credit report. If, upon review, you discover errors, the Act outlines a clear, legally mandated process for challenging them. You can initiate a dispute directly with the credit reporting agency, and often with the information furnisher as well.

Once a dispute is filed, the CRA is legally obligated to investigate the disputed item, typically within 30 days. They must contact the information furnisher, who then also has a duty to investigate and report back. If the investigation confirms the information is inaccurate, incomplete, or unverifiable, the item must be corrected or removed from your report. This right ensures that consumers are not stuck with damaging errors and provides a mechanism for correcting their financial records, which can significantly impact their credit scores and financial opportunities.

The Right to Know About Adverse Actions

The FCRA also ensures transparency when an unfavorable decision is made based on information in a credit report. If a lender denies you credit, an insurer denies you coverage, or an employer decides not to hire you – partly or wholly due to information in your credit report – they are legally required to provide you with an “adverse action notice.”

This notice must inform you of the decision, identify the credit reporting agency that provided the report, and explain your right to obtain a free copy of that specific report (within 60 days) and dispute any inaccuracies. This provision is crucial because it ensures consumers are not left guessing why they were denied. It allows them to understand the specific factors influencing the decision and take corrective action if the underlying information is flawed, further reinforcing the FCRA’s commitment to fairness and consumer insight.

Regulating the Credit Information Ecosystem

The FCRA’s effectiveness hinges on its comprehensive regulation of the various entities involved in the credit reporting process. It delineates specific duties and responsibilities for credit reporting agencies, information furnishers, and governmental oversight bodies, creating a system of checks and balances.

Responsibilities of Credit Reporting Agencies (CRAs)

The major credit reporting agencies – Equifax, Experian, and TransUnion – are the central repositories of consumer credit information. The FCRA places significant responsibilities on these CRAs. They must maintain reasonable procedures to assure the maximum possible accuracy of the information they report, ensuring that the data they disseminate is fair and truthful. They are also responsible for reinvestigating disputed information, correcting or deleting inaccuracies promptly, and providing consumers with free copies of their reports annually. Furthermore, CRAs must establish and maintain secure systems to protect sensitive consumer data and limit access to those with a permissible purpose.

Duties of Information Furnishers

Beyond the CRAs, the FCRA also imposes obligations on the “furnishers” of information – the banks, credit card companies, auto lenders, mortgage providers, and collection agencies that report your financial activity. These entities are responsible for reporting accurate and complete information to the CRAs. Crucially, if a consumer disputes an account, the furnisher must conduct a reasonable investigation into the dispute and, if warranted, correct or delete the inaccurate information it has reported. This dual responsibility between CRAs and furnishers creates a more robust system for maintaining data accuracy and resolving consumer complaints.

Enforcement and Oversight

To ensure compliance with its provisions, the FCRA is primarily enforced by federal agencies. The Consumer Financial Protection Bureau (CFPB) holds the primary enforcement authority for most financial institutions, while the Federal Trade Commission (FTC) continues to enforce the Act for other entities. These agencies investigate violations, issue regulations, and can take enforcement actions against companies that fail to comply with the FCRA, including imposing fines and requiring corrective measures. This robust regulatory framework ensures that the FCRA’s protections are not just theoretical but are actively enforced, providing a powerful deterrent against negligence or willful non-compliance.

Broader Financial Implications and Modern Relevance

While primarily focused on credit decisions, the FCRA’s influence extends far beyond mere lending, touching critical aspects of everyday life and serving as a crucial defense in the fight against modern financial crimes.

Beyond Lending: Employment, Housing, and Insurance

The scope of the FCRA’s protection is broad. It acknowledges that credit reports are used for more than just granting loans. Employers often use credit reports (with explicit written consent from the applicant) as part of background checks, particularly for positions involving financial responsibility. Landlords use them to assess potential tenants, and insurance companies may review them when underwriting policies.

In these contexts, the FCRA maintains that the same standards of accuracy, privacy, and consumer rights apply. Employers, landlords, and insurers must have a permissible purpose to access these reports and must provide adverse action notices if the report contributes to a negative decision. This extended reach ensures that the financial data collected under the FCRA does not unfairly hinder opportunities in areas critical to an individual’s livelihood and stability.

A Shield Against Identity Theft and Fraud

In an increasingly digital world, identity theft and financial fraud pose significant threats. The FCRA provides essential tools for consumers to protect themselves and recover from such crimes. Under the Act, consumers have the right to place “fraud alerts” on their credit files, which notify potential creditors to take extra steps to verify identity before extending new credit. For more severe cases, individuals can also place a “security freeze” (or credit freeze) on their reports, which completely restricts access to their credit file, making it much harder for identity thieves to open new accounts in their name.

These provisions are vital safeguards, empowering consumers to proactively protect their financial identities and regain control if their personal information is compromised. By enabling individuals to restrict access to their credit files, the FCRA serves as a powerful deterrent against unauthorized account openings and a critical tool in mitigating the damage caused by identity theft.

Conclusion

The Fair Credit Reporting Act is far more than a technical piece of legislation; it is a foundational pillar of consumer financial protection in the United States. Its purpose is multifaceted: to ensure that the vast amount of personal financial data collected and disseminated is accurate, to safeguard the privacy of that information, and to empower consumers with explicit rights to access, review, and dispute their credit reports. By imposing strict obligations on credit reporting agencies and information furnishers, and by providing robust enforcement mechanisms, the FCRA fosters a credit ecosystem built on fairness and transparency.

In an economy increasingly reliant on credit and in an era marked by digital data flows and the ever-present risk of identity theft, the FCRA’s enduring relevance cannot be overstated. It remains an indispensable tool for maintaining financial stability, protecting individual opportunities, and ensuring that every consumer has a fair chance to build and maintain a healthy financial future. Understanding its purpose and leveraging its protections is a non-negotiable aspect of sound personal finance management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.