In the intricate world of finance, few figures hold as much sway over the average consumer and multinational corporation alike as the prime rate. Often referenced in financial news segments and whispered in boardrooms, this seemingly abstract number is, in reality, a powerful determinant of borrowing costs, investment opportunities, and the overall health of the economy. Understanding the prime rate isn’t just for financial professionals; it’s a critical component of informed personal finance, shrewd business strategy, and effective wealth management.

At its core, the prime rate represents the interest rate that commercial banks charge their most creditworthy corporate customers. It’s not a rate set by a single entity that you can simply look up and apply universally. Instead, it acts as a benchmark, a foundational lending rate from which other variable interest rates across the economy are often derived. When you hear about changes in the prime rate, it’s a signal that the cost of borrowing money is likely to shift, impacting everything from your credit card APR to the interest on your small business loan. Today, more than ever, with economic indicators constantly in flux, knowing what the prime rate is and understanding its implications is paramount to making sound financial decisions. This article will demystify the prime rate, explore how it’s determined, illuminate its far-reaching effects, and guide you on how to track this vital economic benchmark.

Understanding the Prime Rate: The Foundation of Lending

To truly grasp the significance of “what is the prime rate for today,” one must first understand its fundamental definition and the mechanisms that bring it into existence. It is not an arbitrary number but a carefully calculated benchmark rooted in the broader monetary policy of a nation.

Defining the Prime Rate: More Than Just a Number

The prime rate is defined by most U.S. banks as the base rate on corporate loans offered to their best commercial customers. In practical terms, it is the lowest available interest rate that banks offer to borrowers with the strongest credit profiles. While individual consumers rarely qualify for the prime rate directly, it serves as a critical reference point for a vast array of consumer and business loan products. For instance, the interest rate on a variable-rate credit card might be advertised as “prime + 5%,” meaning your actual rate is the current prime rate plus an additional five percentage points. Similarly, many home equity lines of credit (HELOCs) and certain small business loans are structured to float a certain percentage above or below the prime rate.

It’s important to note that while banks define their own prime rates, there’s a strong consensus among major institutions. In the U.S., the prime rate published by The Wall Street Journal is widely accepted as the benchmark, reflecting the prime rate posted by at least 70% of the nation’s 10 largest banks. This consensus ensures uniformity and predictability across the financial sector, even though individual banks retain the theoretical right to set their own.

How the Prime Rate is Determined: The Federal Funds Rate Connection

The primary driver behind the prime rate in the United States is the federal funds rate. This is the target interest rate set by the Federal Open Market Committee (FOMC) of the Federal Reserve. The federal funds rate is the rate at which commercial banks lend their excess reserves to each other overnight. While the Fed doesn’t directly set the prime rate, changes in the federal funds rate almost immediately trigger corresponding changes in the prime rate.

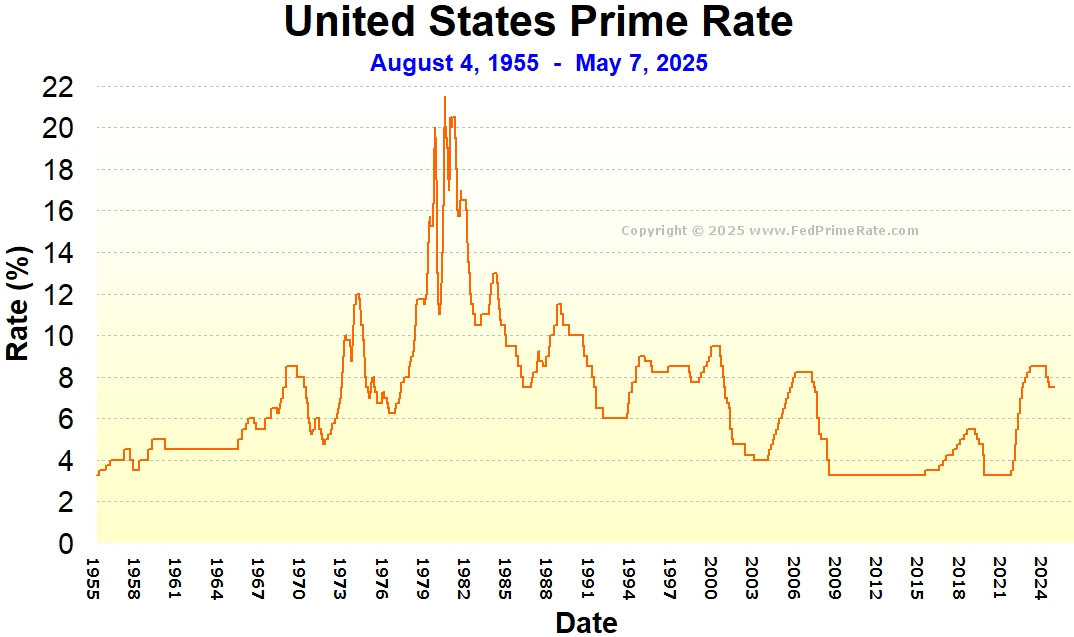

Typically, the prime rate in the U.S. is calculated by adding approximately three percentage points to the upper target limit of the federal funds rate. So, if the Fed sets the federal funds rate target at 2.00% to 2.25%, the prime rate will likely be 5.25% (2.25% + 3%). This stable spread ensures that banks maintain a profitable margin over their cost of borrowing, which is indirectly tied to the federal funds rate. When the Fed raises or lowers the federal funds rate, banks respond by adjusting their prime rate in lockstep, often within hours or days of the Fed’s announcement.

The Federal Reserve’s Influence: Monetary Policy and Economic Goals

The Federal Reserve utilizes the federal funds rate as a key tool of its monetary policy to achieve its dual mandate: maximizing employment and maintaining stable prices (i.e., controlling inflation).

- When the economy is overheating and inflation is a concern, the Fed may choose to raise the federal funds rate. This makes it more expensive for banks to borrow from each other, which in turn leads banks to raise their prime rate. Higher borrowing costs for consumers and businesses then tend to slow down economic activity, cooling inflation.

- When the economy is sluggish and unemployment is high, the Fed may lower the federal funds rate. This reduces banks’ borrowing costs, prompting them to lower their prime rate. Cheaper borrowing encourages consumers to spend and businesses to invest, thereby stimulating economic growth.

Understanding this direct link between the Federal Reserve’s actions and the prime rate is crucial for anticipating financial trends and making informed decisions about borrowing and saving.

Why the Prime Rate Matters: Its Pervasive Impact

The prime rate’s influence extends far beyond a select group of creditworthy corporations. Its fluctuations ripple through the entire financial system, affecting individuals, small businesses, and large enterprises in myriad ways. Its pervasive impact underscores why understanding “what is the prime rate for today” is not merely academic but profoundly practical.

Impact on Consumer Loans: Mortgages, Auto Loans, Credit Cards

For the average consumer, the prime rate is most directly felt through its effect on variable-rate loans.

- Credit Cards: Most credit card Annual Percentage Rates (APRs) are tied to the prime rate. If the prime rate goes up, the interest you pay on your credit card debt, especially if you carry a balance, will also increase. This can significantly raise the cost of existing debt.

- Home Equity Lines of Credit (HELOCs): HELOCs are almost universally variable-rate products linked to the prime rate. As the prime rate shifts, so does the interest payment on your outstanding HELOC balance. For homeowners relying on HELOCs for renovations or other expenses, these changes can have a substantial impact on monthly budgets.

- Adjustable-Rate Mortgages (ARMs): While fixed-rate mortgages are immune, adjustable-rate mortgages (ARMs) often reset based on various indices, some of which are indirectly influenced by the prime rate or directly tied to it. When the prime rate rises, the interest rate on an ARM can increase at its reset period, leading to higher monthly mortgage payments.

- Auto Loans and Personal Loans: While many auto loans and personal loans are fixed-rate, the initial rates offered by lenders are heavily influenced by the prevailing prime rate and overall interest rate environment. A rising prime rate generally means higher initial interest rates for new loans.

Impact on Business Lending: Small Business Loans, Lines of Credit

For businesses, particularly small and medium-sized enterprises (SMEs), the prime rate is a critical factor in their operational costs and growth potential.

- Small Business Loans: Many variable-rate small business loans and equipment financing agreements are indexed to the prime rate. An increase in the prime rate can raise the cost of capital for businesses, making it more expensive to expand, purchase inventory, or manage cash flow.

- Lines of Credit: Business lines of credit, which are vital for working capital management, are almost always variable-rate and directly tied to the prime rate. Fluctuations can significantly impact a company’s liquidity and profitability, especially during periods of high interest rates.

- Corporate Borrowing: Even large corporations, while they might secure rates below prime due to their immense creditworthiness, find their cost of borrowing influenced by the broader prime rate environment. It sets the baseline for all lending.

Implications for Savers and Investors: Indirect Effects

While the prime rate directly impacts borrowers, its influence extends to savers and investors, albeit often more indirectly.

- Savings Accounts and CDs: When the prime rate rises, banks generally increase the interest rates they offer on savings accounts, money market accounts, and certificates of deposit (CDs). This is because the higher lending rates allow them to pay more to attract deposits. For savers, a rising prime rate can present opportunities for better returns on their cash.

- Investment Decisions: Changes in the prime rate, driven by the Federal Reserve’s monetary policy, can influence the stock market, bond market, and other investment vehicles. A rising prime rate (and rising interest rates generally) can make bonds more attractive relative to stocks, as their yields increase. It can also put pressure on corporate earnings by increasing borrowing costs, potentially impacting stock valuations. Conversely, a falling prime rate can stimulate economic growth, benefiting equities.

Finding the Current Prime Rate and Staying Informed

Given its wide-ranging impact, knowing “what is the prime rate for today” is a fundamental piece of financial literacy. Fortunately, tracking this benchmark is straightforward once you know where to look.

Where to Locate the Prime Rate: Reputable Sources

The most widely recognized and authoritative source for the U.S. prime rate is The Wall Street Journal. They publish the current prime rate daily, reflecting the rate posted by the majority of the largest U.S. banks. You can typically find this information in their print edition, on their website, or through financial data services.

Other reliable sources include:

- Major Financial News Outlets: Reputable financial news websites (e.g., Bloomberg, Reuters, CNBC) will consistently report on the prime rate and any changes.

- Federal Reserve Publications: While the Fed sets the federal funds rate, not the prime rate directly, their publications and news releases provide context and signals for future rate movements.

- Your Bank’s Website: Many banks will also publish their current prime rate, though it should align closely with the widely reported benchmark.

The Dynamic Nature of the Prime Rate: Why “Today” is Important

The “today” in “what is the prime rate for today” is critical because the prime rate is not static. It is a dynamic figure that can change. While it doesn’t fluctuate daily like stock prices, it can change swiftly following Federal Reserve meetings where the federal funds rate is adjusted. The FOMC meets eight times a year on a scheduled basis, but unscheduled meetings can occur if economic conditions warrant immediate action.

Because many financial products are tied to the prime rate, even small changes can accumulate and have a significant effect on your finances over time. For those with variable-rate debt, checking the prime rate regularly, especially around FOMC meeting dates, is a prudent practice.

Interpreting Prime Rate Changes: What a Rise or Fall Signifies

Understanding the implications of a prime rate change is key to leveraging this knowledge.

- A Rising Prime Rate: This typically signals that the Federal Reserve is attempting to slow down an overheating economy and combat inflation. For borrowers, it means higher interest payments on variable-rate debt and higher initial rates on new loans. For savers, it can mean better returns on deposits. For investors, it can introduce headwinds for equities but opportunities in fixed income.

- A Falling Prime Rate: This usually indicates the Fed is trying to stimulate a sluggish economy and encourage borrowing and spending. For borrowers, it translates to lower interest payments on variable-rate debt and potentially lower initial rates on new loans. For savers, it means lower returns on deposits. For investors, it can be a tailwind for equities but less attractive for fixed income.

By interpreting these changes, individuals and businesses can make more strategic decisions about managing debt, saving money, and making investments.

Navigating Your Finances in a Shifting Prime Rate Environment

The prime rate’s fluidity necessitates a proactive approach to financial management. Understanding its trajectory and potential impact allows individuals and businesses to adapt strategies and optimize their financial outcomes.

Strategies for Borrowers: Refinancing, Locking in Rates

For borrowers, a shifting prime rate environment presents both challenges and opportunities.

- Consider Refinancing: If the prime rate is falling or has recently fallen, it might be an opportune time to refinance variable-rate loans (like HELOCs or ARMs) into fixed-rate alternatives, or simply to a lower variable rate, to reduce monthly payments. Similarly, consolidating high-interest credit card debt into a lower-rate personal loan (if available) can offer significant savings.

- Locking in Rates: When interest rates are low or perceived to be at their trough, securing new fixed-rate loans (e.g., mortgages, auto loans) can provide long-term stability and protection against future prime rate increases. This strategy is particularly valuable if a rising prime rate environment is anticipated.

- Aggressive Debt Repayment: Regardless of the prime rate’s direction, prioritizing the repayment of high-interest, variable-rate debt (like credit cards) is almost always a sound strategy. Reducing your principal balance minimizes the impact of any rate increases.

- Reviewing Loan Terms: Periodically review the terms of your variable-rate loans. Understand how often your rate adjusts, what indices it’s tied to, and any caps or floors that might apply.

Opportunities for Savers: High-Yield Accounts

While borrowers might find a rising prime rate challenging, savers can often benefit.

- Seek High-Yield Savings Accounts and CDs: When the prime rate (and by extension, the federal funds rate) rises, banks become more competitive in attracting deposits. This is a prime time to shop around for high-yield savings accounts, money market accounts, and certificates of deposit (CDs) that offer better returns on your cash.

- Laddering CDs: For those with substantial savings, a CD laddering strategy can be effective. By investing in CDs with staggered maturity dates, you can take advantage of rising rates as older CDs mature and new ones are opened at higher rates.

- Evaluating Bond Investments: A rising prime rate often correlates with higher yields on newly issued bonds, making fixed-income investments more attractive. However, existing bonds might see their market value decrease as new, higher-yielding bonds become available.

The Role of Financial Planning: Proactive Management

Ultimately, the most effective way to navigate a shifting prime rate environment is through thoughtful and proactive financial planning.

- Budgeting and Cash Flow Analysis: Understand how changes in interest payments affect your monthly budget. A clear picture of your cash flow allows you to adjust spending or savings habits as needed.

- Scenario Planning: Consider different interest rate scenarios. What if the prime rate rises by another 1% or 2%? How would that impact your loan payments and overall financial health? This allows for preparation rather than reaction.

- Consult with a Financial Advisor: A qualified financial advisor can provide personalized guidance, helping you understand how prime rate changes specifically affect your financial situation and suggesting tailored strategies for debt management, savings, and investment.

- Stay Informed: Continuously monitoring financial news, Federal Reserve announcements, and the prime rate itself empowers you to make timely and educated decisions.

The prime rate is far more than just a number; it is a barometer of the economic climate and a foundational element that influences nearly every aspect of our financial lives. By staying informed about “what is the prime rate for today” and understanding its intricate relationship with monetary policy and lending, you equip yourself with the knowledge to make strategic financial choices, mitigate risks, and seize opportunities, regardless of the economic winds. In a world where financial conditions are ever-evolving, an informed approach to the prime rate is an invaluable asset.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.