In an era defined by fluctuating inflation rates, a volatile housing market, and the rising cost of essential goods, the question of where one lives has become a pivotal financial decision. For many, “home” is no longer just a place of residence; it is a strategic asset in a broader personal finance portfolio. Choosing a state with a low cost of living is one of the most effective ways to accelerate wealth building, increase discretionary income, and achieve financial independence.

However, identifying the “most affordable” state is not as simple as looking at the lowest price tag on a three-bedroom house. To a savvy investor or a budget-conscious professional, affordability is a multifaceted equation involving tax structures, utility costs, healthcare expenses, and the local labor market. This guide analyzes the top contenders for the most affordable state to live in through the lens of personal finance and strategic wealth management.

The Financial Metrics of Affordability

To determine which state truly offers the best value, we must look beyond surface-level statistics. In the world of personal finance, affordability is measured by how much of your gross income remains after “nondiscretionary” expenses—the costs you cannot avoid.

The Impact of Housing and Real Estate Markets

Housing is consistently the largest line item in any household budget, often consuming 25% to 35% of an individual’s take-home pay. When evaluating the affordability of a state, the Median Home Price and Median Monthly Rent are the primary metrics. In states like Mississippi or Kansas, the barrier to entry for property ownership is significantly lower than the national average. From an investment perspective, lower housing costs mean smaller mortgages, lower interest payments over the life of the loan, and a faster path to 100% equity. For those looking to maximize their “Money” strategy, low-cost housing allows for the redirection of capital into high-yield investment vehicles like index funds or retirement accounts.

Navigating State Tax Environments

A state’s affordability is heavily influenced by its fiscal policy. There are three main tax categories that affect your bottom line: income tax, property tax, and sales tax. While some states, like Tennessee or Florida, boast no state income tax, they often compensate for this loss of revenue through higher sales or property taxes. Conversely, some states with low property taxes may have a progressive income tax system that eats into the earnings of high-performers. A truly affordable state maintains a balance that allows residents to retain a higher percentage of their gross earnings.

The Cost of Living Index (COLI)

The Cost of Living Index is a theoretical price level that allows for a direct comparison of expenses between different geographic areas. A score of 100 represents the national average. States that fall significantly below this mark—often in the 80s or low 90s—offer a “geographic arbitrage” opportunity. This index factors in groceries, utilities, transportation, and healthcare. For a professional working remotely, moving from a state with a COLI of 120 to one with a COLI of 85 is equivalent to receiving a massive, tax-free raise.

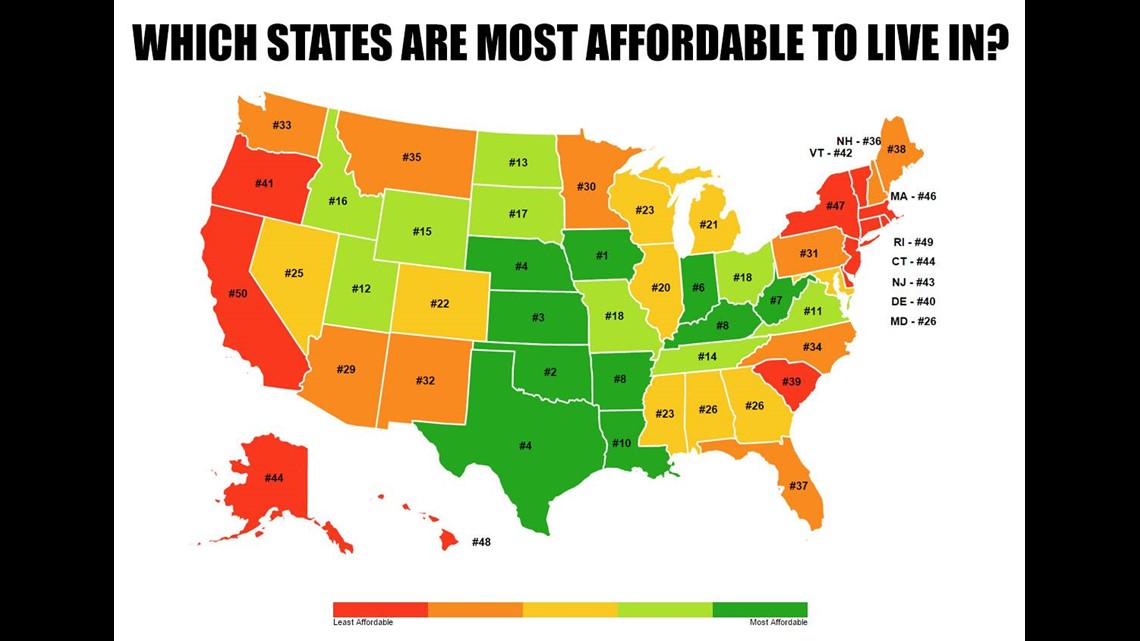

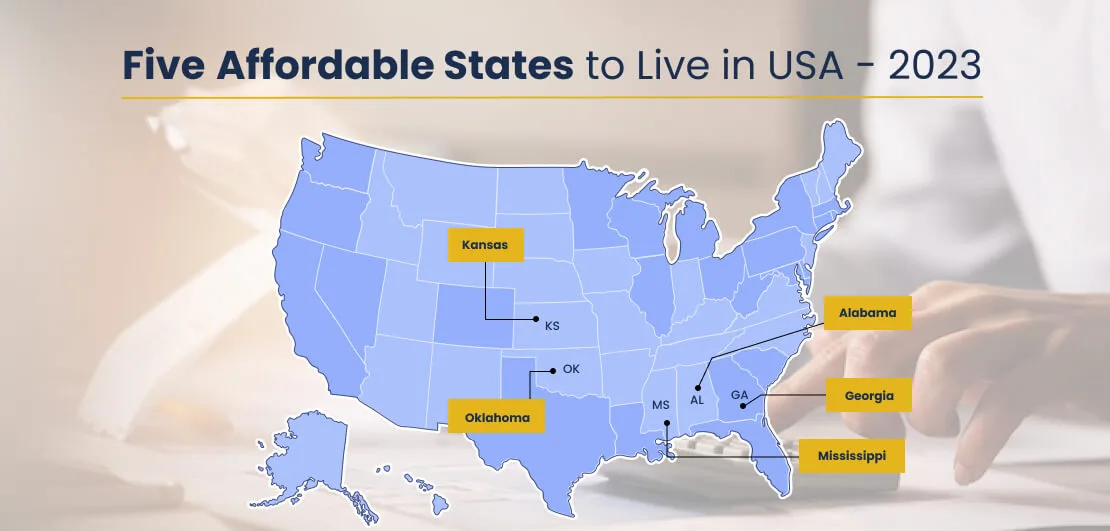

Leading Candidates for the Most Affordable State

Based on recent economic data and financial reporting, several states consistently vie for the top spot. While the rankings may shift slightly year-to-year based on local economic shifts, the following states represent the gold standard for low-cost living.

Mississippi: The Benchmark for Low Costs

Mississippi frequently ranks as the most affordable state in the U.S., primarily driven by its exceptionally low housing costs. The state’s Cost of Living Index is often nearly 15% lower than the national average. For a personal finance enthusiast, Mississippi represents the lowest “burn rate” possible. Not only is real estate inexpensive, but the costs of essential services—from childcare to automotive repair—are significantly lower than in coastal hubs. However, one must balance these savings against the state’s median income levels to ensure that the “affordability” doesn’t come at the cost of earning potential.

Oklahoma: Energy and Housing Balance

Oklahoma is a powerhouse in the affordability category, particularly regarding energy costs and housing. Because of its robust energy sector, utility bills in Oklahoma are among the lowest in the nation. This is a critical factor for families and small business owners who want to keep overhead low. Furthermore, cities like Oklahoma City and Tulsa offer a rare combination: a low cost of living paired with a diversifying economy that supports remote workers and tech professionals. From a wealth-building perspective, the ability to buy a high-quality home for a fraction of the national median allows for aggressive debt repayment and investment.

Kansas and West Virginia: Mid-Continent Value

Kansas and West Virginia are perennial favorites for those prioritizing financial stability. Kansas offers a remarkably stable housing market and low food costs, thanks to its agricultural prominence. West Virginia, on the other hand, offers some of the lowest property taxes in the country. For retirees or those living on a fixed investment income, West Virginia’s low tax burden on real estate can save thousands of dollars annually, preserving the longevity of a retirement nest egg.

The Strategy of Geo-Arbitrage and Wealth Accumulation

Identifying the most affordable state is only the first step. The real financial “win” comes from how you leverage that affordability to change your financial trajectory. This is where the concept of geo-arbitrage becomes essential.

Earning High While Spending Low

Geo-arbitrage is the practice of earning a salary based on a high-cost labor market (like San Francisco, New York, or a global digital firm) while physically residing in a low-cost area (like Arkansas or Nebraska). In the “Money” niche, this is considered one of the fastest ways to reach “FIRE” (Financial Independence, Retire Early). If your income is $150,000 but your cost of living is calibrated to a state where the median home price is $200,000, your savings rate can easily exceed 50%. This surplus capital can then be deployed into the stock market, doubling or tripling your net worth in a decade.

Long-term Wealth vs. Short-term Savings

While moving to an affordable state provides immediate relief to a monthly budget, the long-term financial implications are even more profound. Lower cost of living leads to lower insurance premiums, lower property taxes, and lower lifestyle inflation. Over 30 years, the difference between living in a high-cost state versus an affordable one can result in a multi-million dollar difference in total net worth due to the power of compound interest on the money saved.

Evaluating the Trade-offs: Is Cheap Always Better?

In personal finance, there is no such thing as a free lunch. A lower cost of living often comes with trade-offs that can impact your long-term financial health if not properly managed.

Opportunity Cost and Salary Compression

One of the primary risks of moving to the “most affordable” state is the potential for salary compression. Local employers in low-cost states often pay less because the cost of labor is lower. If you do not have a remote job or a portable business, your “affordability” might be offset by a smaller paycheck. Before relocating, it is vital to calculate your “real” income—the amount you have left after all expenses. A $100,000 salary in an expensive state might actually provide more discretionary income than a $50,000 salary in a cheap state.

Infrastructure and Property Appreciation

Another factor to consider is the appreciation of assets. Real estate in high-cost, high-demand coastal states typically appreciates at a faster rate than in rural or low-cost states. While you save money on your monthly mortgage in an affordable state, you may not see the same level of capital gains when it comes time to sell the property. For a pure investor, this means your home becomes less of a growth asset and more of a “utility” that keeps your expenses low so you can invest elsewhere.

Final Verdict: Choosing Your Financial Future

Ultimately, the “most affordable” state is a title currently held by Mississippi, closely followed by Oklahoma and Kansas. However, the best state for your money depends on your specific financial goals.

If your goal is to minimize taxes, a state with no income tax might be your priority. If your goal is to own a large piece of property for a small amount of capital, the Midwest and Deep South offer the best ROI. If you are a remote worker looking to maximize the gap between earnings and expenses, geo-arbitrage in any of the top ten most affordable states will serve as a powerful catalyst for wealth creation.

In the world of finance, location is more than a point on a map—it is a strategic decision that dictates your ability to save, invest, and eventually achieve financial freedom. By choosing a state that aligns with your financial objectives and minimizes your largest expenses, you are not just finding a cheaper place to live; you are architecting a more prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.