For millions of Americans nearing or in retirement, Medicare represents a cornerstone of healthcare security. This federal health insurance program provides critical coverage for medical services, hospital stays, and prescription drugs. However, a common misconception is that Medicare enrollment and costs are uniform for everyone. The reality is more nuanced, particularly when it comes to income. While there isn’t a strict “income limit” to qualify for Medicare Part A (hospital insurance) if you’ve paid Medicare taxes through employment, your income does play a significant role in determining how much you pay for other parts of Medicare, particularly Part B (medical insurance) and Part D (prescription drug coverage).

Understanding these income-related adjustments is crucial for effective financial planning in retirement. Failing to account for these potential surcharges can lead to unexpected and substantial increases in your monthly healthcare premiums, impacting your overall budget and financial well-being. This article will demystify the income thresholds that affect Medicare costs, known as the Income-Related Monthly Adjustment Amount (IRMAA), and provide actionable insights into navigating this complex but vital aspect of your financial future.

Understanding Medicare: A Brief Overview

Before diving into the intricacies of income limits, it’s essential to have a foundational understanding of Medicare itself. Established in 1965, Medicare serves primarily individuals aged 65 or older, and younger people with certain disabilities or End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS). It’s not a single program but rather a system of different parts, each covering specific types of services.

The Pillars of Medicare: Parts A, B, C, and D

- Medicare Part A (Hospital Insurance): This covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. Most people don’t pay a monthly premium for Part A if they or their spouse paid Medicare taxes for a sufficient number of years (typically 10 years or 40 quarters) through employment.

- Medicare Part B (Medical Insurance): This covers certain doctors’ services, outpatient care, medical supplies, and preventive services. Unlike Part A, Part B almost always has a monthly premium, and this is where income first becomes a significant factor.

- Medicare Part C (Medicare Advantage): These are private insurance plans approved by Medicare that provide all your Part A and Part B benefits. Many Part C plans also include Part D coverage and may offer additional benefits like vision, dental, and hearing. While you still pay your Part B premium, the Part C plan itself may have a separate premium. IRMAA does not directly affect the Part C premium but still applies to the underlying Part B premium.

- Medicare Part D (Prescription Drug Coverage): This helps cover the cost of prescription drugs. It’s offered through private companies approved by Medicare. Like Part B, Part D plans have monthly premiums, and these premiums can also be subject to income-related adjustments.

Who is Eligible for Medicare? (Beyond Income)

While income is a factor in costs, it generally isn’t a barrier to eligibility for the core Medicare program. The primary eligibility criteria include:

- Age: U.S. citizens or legal residents (living in the U.S. for at least five years) who are 65 or older.

- Disability: People under 65 who have received Social Security Disability Insurance (SSDI) benefits for 24 months.

- Specific Medical Conditions: Individuals with End-Stage Renal Disease (ESRD) requiring dialysis or a kidney transplant, or those with Amyotrophic Lateral Sclerosis (ALS), qualify regardless of age.

For most individuals, eligibility for premium-free Part A is tied to their work history and Medicare tax contributions, not their current income. However, for Parts B and D, higher incomes trigger additional premium costs.

Income-Related Monthly Adjustment Amount (IRMAA): The Core of Medicare Income Limits

The concept of an “income limit” for Medicare largely revolves around the Income-Related Monthly Adjustment Amount, or IRMAA. IRMAA is an extra amount you have to pay for your Medicare Part B and Part D premiums if your modified adjusted gross income (MAGI) is above certain thresholds. It’s essentially a surcharge on your standard premiums.

How IRMAA Works: Tiers and Surcharges

IRMAA is structured in tiers, meaning there are different income brackets, and each bracket has a corresponding additional amount added to your standard Part B and Part D premiums. As your income increases and crosses these thresholds, your IRMAA surcharge rises, leading to higher overall monthly payments.

The Social Security Administration (SSA) determines who pays IRMAA and how much. They typically use your tax return information from two years prior to make this determination. For example, the IRMAA for 2024 is generally based on your MAGI from your 2022 tax return. This “look-back period” is important to remember when planning your finances.

Which Parts of Medicare Are Affected by IRMAA?

IRMAA primarily impacts:

- Medicare Part B Premiums: All beneficiaries pay a standard Part B premium, but those above the IRMAA thresholds pay an additional amount on top of this.

- Medicare Part D Premiums: While you pay a premium to your chosen private Part D plan, if your income exceeds the IRMAA thresholds, you will also pay an additional Part D IRMAA directly to Medicare. This is separate from your plan’s premium.

It’s crucial to understand that IRMAA is an addition to your standard premiums, not a replacement. You will still pay the base Part B premium and your chosen Part D plan premium, plus any applicable IRMAA amounts.

The Look-Back Period: When Does Social Security Check Your Income?

As mentioned, the SSA generally uses your tax return from two years prior to determine your IRMAA. So, for Medicare premiums in 2024, the SSA looks at your 2022 tax return. For 2025, they’ll look at your 2023 tax return, and so on.

This two-year look-back period can sometimes create challenges. For instance, if you had a high-income year (e.g., from selling an asset, a large bonus, or a one-time retirement payout) two years ago, but your current income is significantly lower, you might still be subject to IRMAA based on that past income. This is why financial planning, especially as you approach Medicare eligibility, is paramount.

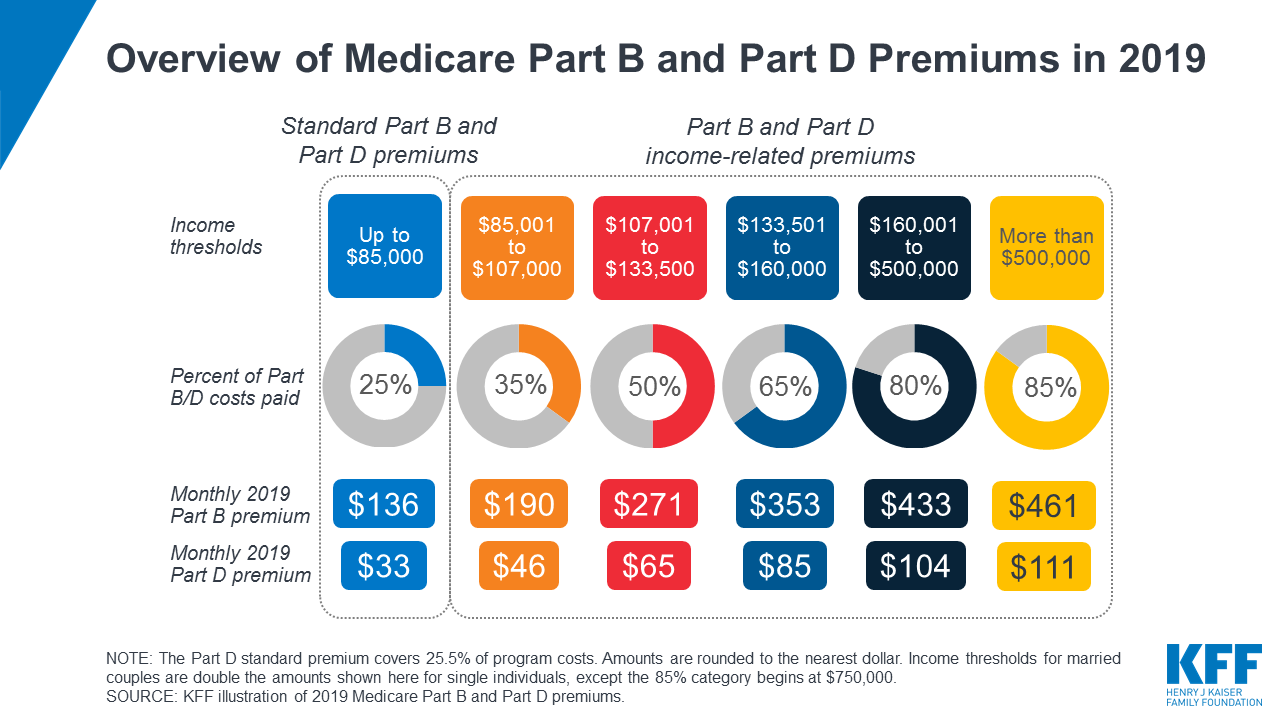

Navigating IRMAA: Income Thresholds and Surcharges for 2024

The specific income thresholds and corresponding IRMAA surcharges are adjusted annually. It’s vital to refer to the most current figures from the Social Security Administration or Medicare.gov. Here’s an illustrative breakdown of the IRMAA tiers for 2024, keeping in mind that these figures are subject to change in future years.

Specific Income Brackets and Corresponding IRMAA Additions (2024 Example)

For 2024, the standard Medicare Part B premium is $174.70. The IRMAA thresholds are based on your Modified Adjusted Gross Income (MAGI) from your 2022 tax return. MAGI for IRMAA purposes is generally your Adjusted Gross Income (AGI) plus tax-exempt interest income.

Here are the estimated IRMAA tiers for 2024:

| Tax Filing Status | Annual Income (MAGI) | Part B Monthly Premium (includes IRMAA) | Part D Monthly Surcharge (in addition to plan premium) |

|---|---|---|---|

| Individual | Up to $103,000 | $174.70 | $0.00 |

| $103,001 – $129,000 | $244.60 | $12.90 | |

| $129,001 – $161,000 | $349.40 | $33.30 | |

| $161,001 – $193,000 | $454.20 | $53.80 | |

| $193,001 – $500,000 | $559.00 | $74.20 | |

| Above $500,000 | $594.00 | $81.00 | |

| Married Filing Jointly | Up to $206,000 | $174.70 | $0.00 |

| $206,001 – $258,000 | $244.60 | $12.90 | |

| $258,001 – $322,000 | $349.40 | $33.30 | |

| $322,001 – $386,000 | $454.20 | $53.80 | |

| $386,001 – $750,000 | $559.00 | $74.20 | |

| Above $750,000 | $594.00 | $81.00 |

Note: These figures are examples based on 2024 data and are subject to change annually. Always verify the latest information from official Medicare sources.

The Impact on Your Premiums: A Financial Snapshot

As you can see, the difference between paying the standard premium and being in the highest IRMAA bracket can be substantial. For an individual, the Part B premium can more than triple, from $174.70 to $594.00 per month. This doesn’t even include the Part D surcharge. Over a year, this can amount to thousands of dollars in additional healthcare expenses, directly impacting your retirement budget. For couples, the financial impact can be even greater.

What Counts as Income for IRMAA? (MAGI Explained)

When determining IRMAA, the SSA uses your Modified Adjusted Gross Income (MAGI). For Medicare purposes, MAGI is generally defined as your Adjusted Gross Income (AGI) as reported on your federal income tax return, plus several other items that are typically excluded from AGI. These generally include:

- Tax-exempt interest (e.g., from municipal bonds)

- Foreign earned income exclusion

- Foreign housing exclusion or deduction

- Interest from U.S. savings bonds used for higher education

- Amounts received from adoption benefits

- Employer-provided adoption assistance

It’s crucial to understand what goes into your MAGI, as seemingly “tax-free” income streams like municipal bond interest can still push you into a higher IRMAA bracket.

Strategies to Mitigate IRMAA and Manage Medicare Costs

Understanding IRMAA is the first step; the next is to strategize how to manage or potentially mitigate its impact on your Medicare premiums. Proactive planning can make a significant difference.

Proactive Financial Planning and Tax Strategies

- Retirement Account Withdrawals: Be mindful of how and when you take withdrawals from retirement accounts, especially Traditional IRAs and 401(k)s. These withdrawals count as taxable income and thus contribute to your MAGI. Converting funds from a Traditional IRA to a Roth IRA, while taxable in the year of conversion, can be a strategy to reduce future MAGI by creating a source of tax-free income in retirement. This needs to be planned carefully, possibly years before Medicare enrollment.

- Tax-Efficient Investing: Consider the tax implications of your investment portfolio. Growth in Roth IRAs and Roth 401(k)s, and distributions from these accounts, are generally tax-free in retirement and do not count towards MAGI for IRMAA purposes.

- Capital Gains Harvesting: Be strategic about selling appreciated assets. Spreading out capital gains over several years or offsetting them with capital losses can help manage your MAGI.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older and have a Traditional IRA, you can make a QCD directly from your IRA to a qualified charity. These distributions count towards your Required Minimum Distributions (RMDs) but are not included in your AGI, thus potentially lowering your MAGI for IRMAA calculations.

- Income Deferral: If you have control over when you receive certain income (e.g., bonuses, severance pay), consider deferring it to years before or after you are subject to IRMAA, if possible.

Appealing an IRMAA Decision: Life-Changing Events

The SSA uses a two-year look-back period for IRMAA, which can sometimes be unfair if your income significantly decreases due to a “life-changing event.” In such cases, you can appeal the IRMAA decision. Life-changing events that may warrant an appeal include:

- Marriage, divorce, or annulment

- Death of your spouse

- Work stoppage or reduction (e.g., retirement)

- Loss of income-producing property

- Loss of pension income

- Employer settlement payment (e.g., a severance package)

If you experience one of these events and your income substantially drops, you can contact the SSA and request a “Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event” form (SSA-44). You’ll need to provide evidence of the event and your current lower income.

Exploring Medicare Advantage (Part C) and Medigap Options

While IRMAA primarily affects Part B and Part D, your choice of supplemental coverage can also impact your overall costs.

- Medicare Advantage (Part C): These plans are offered by private companies and cover all Part A and Part B services, often with additional benefits. While you still pay your Part B premium (and any applicable IRMAA), the Part C plan itself might have a lower or even zero premium, potentially saving you money compared to Original Medicare plus a separate Part D plan and Medigap.

- Medigap (Medicare Supplement Insurance): These plans help cover out-of-pocket costs in Original Medicare, such as deductibles, copayments, and coinsurance. Medigap policies do not include prescription drug coverage (you need a separate Part D plan), and they are not affected by IRMAA. However, their premiums can be substantial, so comparing total costs with a Medicare Advantage plan is wise.

The Broader Context: Low-Income Assistance Programs

While IRMAA focuses on higher incomes, it’s equally important to acknowledge that Medicare offers robust assistance programs for individuals with low incomes and limited resources. These programs can significantly reduce or even eliminate out-of-pocket Medicare costs.

Medicare Savings Programs (MSPs): Help with Premiums and Deductibles

Medicare Savings Programs are state-run programs that help individuals with limited income and resources pay for some or all of their Medicare premiums, deductibles, coinsurance, and copayments. There are several types of MSPs, each with different income and asset limits:

- Qualified Medicare Beneficiary (QMB) Program: Pays for Part A and Part B premiums, deductibles, coinsurance, and copayments.

- Specified Low-Income Medicare Beneficiary (SLMB) Program: Pays for Part B premiums only.

- Qualified Individual (QI) Program: Pays for Part B premiums only.

- Qualified Disabled and Working Individuals (QDWI) Program: Pays for Part A premiums for certain disabled beneficiaries who lost premium-free Part A due to returning to work.

If you qualify for an MSP, it can provide immense financial relief, making Medicare much more affordable.

Extra Help (Low-Income Subsidy) for Prescription Drug Costs

Extra Help, also known as the Low-Income Subsidy (LIS), is a federal program that helps people with limited income and resources pay for their Medicare Part D prescription drug costs. This includes help with monthly premiums, annual deductibles, and prescription copayments. Eligibility for Extra Help is separate from MSPs but often overlaps. If you qualify for Extra Help, your Part D drug costs will be significantly reduced, protecting you from high out-of-pocket expenses for medications.

State-Specific Assistance and Resources

Beyond federal programs, many states offer additional assistance programs for healthcare costs or help navigating Medicare. It’s always a good idea to contact your State Health Insurance Assistance Program (SHIP) or your state’s Medicaid office for information on local resources and counseling services. These programs can provide personalized guidance tailored to your specific situation.

Conclusion

The question “what is the income limit for Medicare?” doesn’t have a simple yes or no answer for eligibility, but it profoundly impacts the financial burden of the program. While there’s no income ceiling to enroll in Medicare, high earners will face increased premiums for Part B and Part D through the Income-Related Monthly Adjustment Amount (IRMAA). Understanding IRMAA, its look-back period, and the income thresholds is critical for proactive financial planning in retirement.

By strategically managing income, considering tax-efficient retirement withdrawals, and being aware of appeal options for life-changing events, individuals can better control their Medicare costs. Conversely, for those with lower incomes, a range of robust federal and state assistance programs exists to ensure access to affordable healthcare. Medicare is a complex but essential system; by equipping yourself with knowledge about its financial intricacies, you can navigate your healthcare journey with greater confidence and stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.