In the world of real estate investment and personal finance, property is often viewed as a stable, appreciating asset. However, the integrity of that asset is constantly under threat from environmental factors that can silently erode its market value. Among the most pervasive and misunderstood threats are mildew and mold. While often used interchangeably in casual conversation, the financial distinction between the two is profound. For a savvy investor, property manager, or homeowner, understanding the difference between mildew and mold is not merely a matter of home maintenance—it is a critical exercise in risk management and capital preservation.

This article explores the financial implications of fungal growth, categorizing these biological entities as liabilities that require specific budgetary strategies for mitigation and remediation.

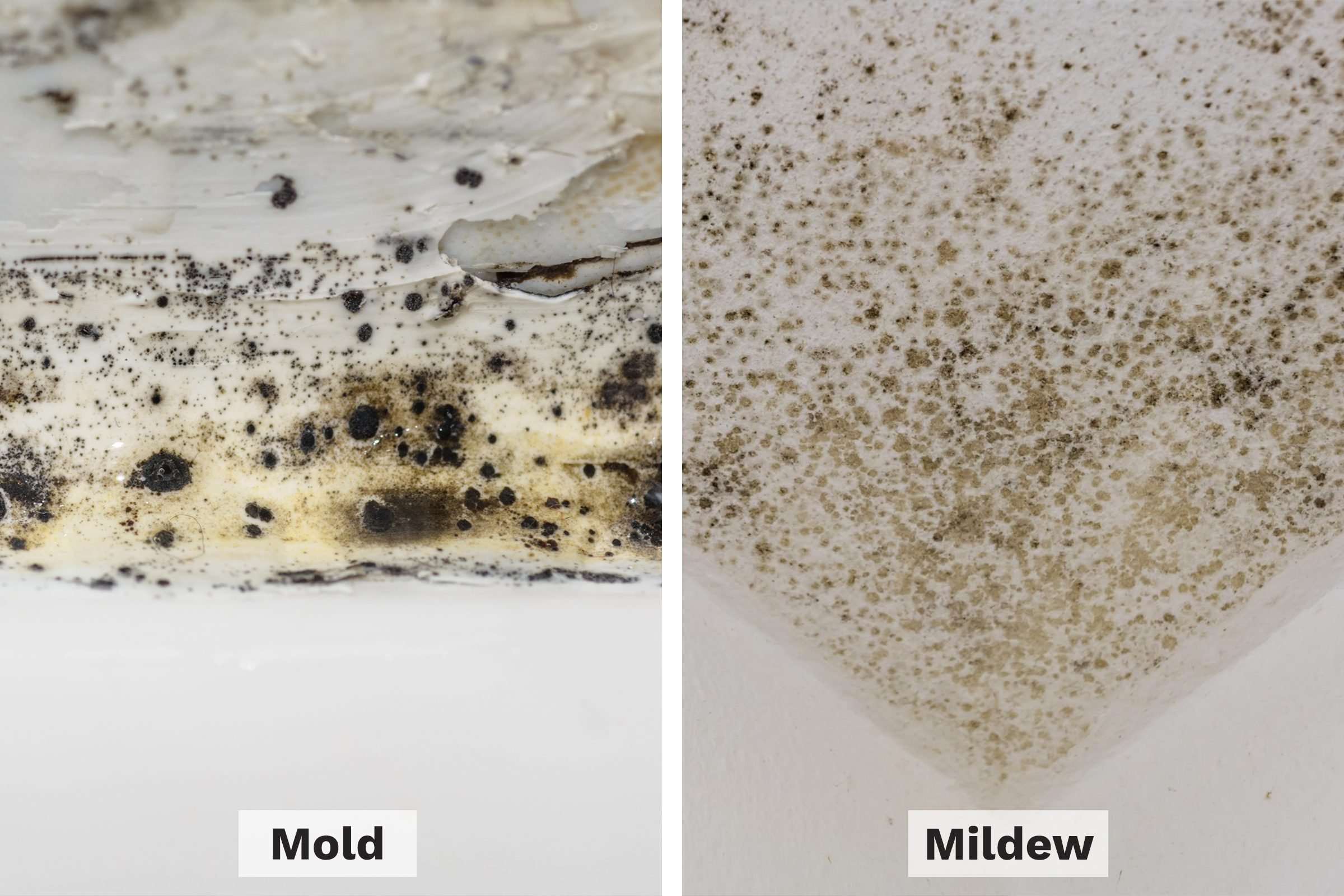

Asset Devaluation: Mildew and Mold as Financial Liabilities

Every property owner must view their building as a living financial statement. When organic growth occurs, it represents a “toxic” entry on the balance sheet. However, the severity of this entry depends entirely on whether the growth is classified as mildew or mold.

Mildew: The Surface-Level Expense

From a financial perspective, mildew is a manageable, low-impact expense. It is a superficial growth that typically appears as a gray or white powdery substance on damp surfaces. In the context of property management, mildew is often categorized under “routine maintenance.”

Because mildew grows on the surface and does not penetrate the substrate of the building material, the cost to address it is minimal. It generally occurs in high-moisture areas like bathrooms or kitchens and can be remediated with over-the-counter chemical solutions and improved ventilation. For a landlord or a house flipper, mildew represents a minor “friction cost”—an annoyance that requires a small allocation of labor and supplies but does not threaten the structural integrity of the asset or its long-term appraisal value.

Mold: The Structural Capital Drain

In contrast, mold is a significant financial liability that can lead to catastrophic capital loss. Unlike mildew, mold is invasive; it penetrates deep into porous materials such as drywall, insulation, and timber. If mildew is a minor market dip, mold is a full-scale systemic collapse.

The financial danger of mold lies in its ability to destroy the structural components of a property. When mold takes hold, it begins to digest the organic material it lives on. This means that “cleaning” is rarely enough; instead, the investor is looking at “reconstruction.” Replacing load-bearing beams, entire sections of drywall, and HVAC systems can cost tens of thousands of dollars. Furthermore, the presence of mold must be disclosed during a sale in many jurisdictions, which can lead to a significant “stigma discount,” reducing the property’s liquidity and final sale price by 10% to 25%.

Risk Mitigation: Identifying Red Flags During the Acquisition Phase

Successful investing is as much about avoiding bad deals as it is about finding good ones. During the due diligence phase of a real estate transaction, distinguishing between mildew and mold is a primary skill for protecting one’s portfolio.

Identifying Red Flags in Commercial Real Estate

In commercial real estate (CRE), the stakes are even higher. A mold infestation in an office building or a multi-family complex can lead to “Sick Building Syndrome,” which creates a massive legal and financial liability for the owner. During the inspection process, investors should look for signs of chronic water intrusion.

While mildew might suggest a simple lack of cleaning by a previous tenant, mold suggests a systemic failure in the building’s envelope or mechanical systems. Investors should analyze the “Financial History of Repairs.” If a property has a history of repeated “minor leaks” that were never professionally dried, the probability of hidden mold—and therefore hidden costs—skyrockets. A professional mold assessment, though an upfront cost of $500 to $1,500, can prevent a $50,000 mistake.

The Hidden Costs of Poor Inspection

Many novice investors attempt to save money by skipping specialized inspections, only to find that they have purchased a “money pit.” The difference between a mildew-affected property and a mold-affected one often lies behind the walls.

If an investor fails to distinguish between the two, they may underestimate the “CapEx” (Capital Expenditure) required to bring the property to market. A surface-level cleaning of mold is a temporary fix that will inevitably lead to the problem returning, often more aggressively. This cycle of “patch-and-repair” is a drain on cash flow. True financial due diligence requires understanding that if you see mold, what you are seeing is likely only 10% of the total financial burden.

ROI and Value Preservation: Remediation Strategies for Profitability

Once an issue has been identified, the investor must decide on a remediation strategy. This decision should be guided by a Cost-Benefit Analysis (CBA) to ensure the highest Return on Investment (ROI) and the preservation of the asset’s equity.

Professional Remediation vs. DIY: A Cost-Benefit Analysis

For mildew, a DIY approach is almost always the more financially sound decision. The materials are inexpensive, and the labor does not require specialized certification. The ROI on a $50 cleaning kit that restores a bathroom’s appearance for a showing is immense.

However, for mold, the DIY route is a “false economy.” Improperly handled mold can release millions of spores into the air, contaminating the entire property and drastically increasing the eventual professional bill. Professional mold remediation companies use “negative air pressure” and HEPA filtration to contain the spread. While the initial bill may be high ($3,000 to $10,000 for a standard residential home), the professional certification of “clearance” is a valuable asset in itself. This document provides a “paper trail” that protects the property’s value during future appraisals and sales.

Enhancing Resale Value through Certified Property Restoration

In the modern real estate market, buyers are increasingly risk-averse regarding environmental health hazards. An investor who can prove they addressed a fungal issue with professional-grade remediation can actually use this as a selling point.

By transforming a liability (mold) into a documented history of structural improvement (certified remediation and moisture control upgrades), the investor protects the property’s valuation. Installing high-efficiency dehumidifiers or upgrading to mold-resistant drywall are examples of “value-add” investments that prevent future depreciation. These upgrades should be viewed as insurance premiums paid upfront to avoid the massive “discounting” that occurs when a buyer’s home inspector finds active mold.

Legal and Insurance Implications: Protecting Your Portfolio

Finally, the difference between mildew and mold extends into the realms of insurance and law. As an investor or business owner, these factors dictate your long-term financial stability and protection against litigation.

Navigating Insurance Policies for Fungal Damage

Most standard property insurance policies have very specific—and often restrictive—language regarding mold. Often, mold damage is only covered if it is the direct result of a “covered peril,” such as a pipe bursting. If mold occurs due to “neglect” or “lack of maintenance” (which is how insurance companies often classify long-term mildew that turns into mold), the claim will likely be denied.

Investors must review their “Fungi, Wet or Dry Rot” endorsements. Understanding the “sub-limits” on these policies is essential. For example, a policy might have a $1,000,000 limit for fire but only a $15,000 limit for mold remediation. Knowing this allows an investor to set aside an appropriate “contingency fund” in their business budget. Mildew rarely triggers insurance claims; mold, however, can exhaust a policy’s limits in a matter of weeks.

Liability and Tenant Relations in Rental Markets

In the rental sector, mold is a leading cause of “constructive eviction” lawsuits. If a landlord fails to distinguish between a tenant’s complaint about “black spots” (which could be mildew) and a serious mold infestation, they risk legal action that can result in the return of all rent paid, plus damages.

Proactive communication and rapid response are the most cost-effective strategies here. A landlord who treats every report of mildew with the seriousness of a mold inspection builds “goodwill capital” and reduces the likelihood of litigation. Financially, it is far cheaper to pay for a $200 inspection and a $100 cleaning than to pay $20,000 in legal fees and lost rent. In the business of property management, the “mildew vs. mold” distinction is a framework for prioritizing maintenance requests to maximize tenant retention and minimize legal exposure.

Conclusion: The Bottom Line on Fungal Financials

In conclusion, while mildew and mold are biologically related, they are worlds apart in the context of finance and investment. Mildew is a maintenance task; mold is a capital crisis.

The successful investor recognizes that mildew is a signal to act before the situation evolves into a mold-driven asset devaluation. By performing rigorous due diligence, choosing the correct remediation path, and understanding the nuances of insurance and liability, property owners can protect their equity from the silent, creeping rot of fungal growth. In the end, the difference between a profitable portfolio and a failing one often comes down to the ability to identify, quantify, and mitigate the hidden costs that grow in the dark.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.