The prime rate is often referred to as the heartbeat of the consumer lending market. While it may seem like a dry economic statistic discussed only on financial news networks, it is, in fact, one of the most influential numbers in your daily financial life. Whether you are carrying a balance on a credit card, looking to tap into your home’s equity, or managing a small business loan, the current prime rate dictates exactly how much your debt will cost you.

In the current economic climate, characterized by the Federal Reserve’s aggressive stance against inflation and subsequent shifts toward stabilization, understanding the prime rate is more than just academic—it is a vital component of strategic financial planning.

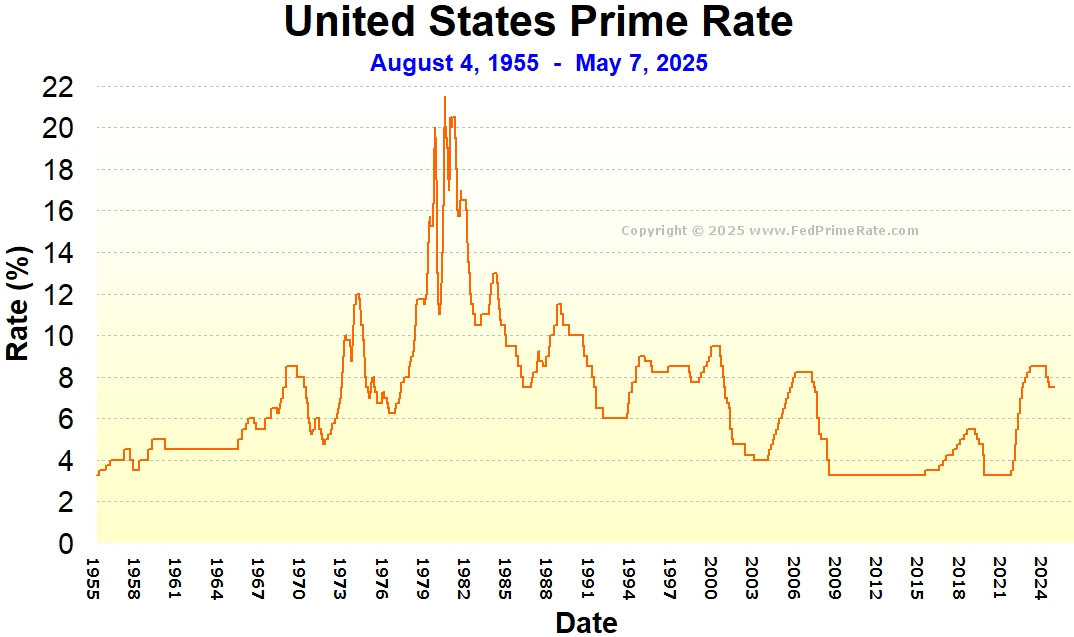

The Mechanics of the Prime Rate: How the Number is Determined

To understand what the prime rate is today, one must first understand where it comes from. The prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. While each bank technically sets its own prime rate, the industry follows a standardized benchmark—most notably the “Wall Street Journal Prime Rate,” which is derived by polling the 30 largest banks in the United States.

The Inextricable Link to the Federal Funds Rate

The prime rate does not move in a vacuum. It is directly tied to the Federal Funds Rate, which is the interest rate banks charge each other for overnight loans to maintain their reserve requirements. As a rule of thumb, the prime rate is almost always set at 3% above the federal funds target range.

When the Federal Open Market Committee (FOMC) decides to raise or lower interest rates to control inflation or stimulate growth, the prime rate moves in lockstep. For example, if the Fed raises the target range by 25 basis points (0.25%), the prime rate will typically increase by the same amount within 24 to 48 hours.

Why Banks Use a “Prime” Benchmark

Banks use the prime rate as a base for various types of lending because it reflects the cost of doing business in the current liquidity environment. By starting with the prime rate and adding a “margin” based on an individual borrower’s risk profile (e.g., Prime + 2%), lenders ensure they maintain a profit margin regardless of how the Federal Reserve fluctuates. For the consumer, this means that even if your credit score remains perfect, your interest rate can rise simply because the macroeconomic environment has shifted.

Why the Prime Rate Matters for Your Personal Finances

The most immediate impact of a change in the prime rate is felt in variable-interest debt. Unlike a fixed-rate mortgage, where your payment remains the same for 30 years, many consumer products are “floating,” meaning they adjust automatically when the benchmark changes.

The Impact on Variable-Rate Credit Cards

Most credit cards today carry a variable Annual Percentage Rate (APR). If you look at your credit card agreement, you will likely see that your interest rate is defined as “The Prime Rate + [X]%.” When the prime rate stays high, the cost of carrying a balance becomes significantly more expensive. For instance, a move from a 4% prime rate to an 8% prime rate can add hundreds of dollars in annual interest charges to a modest balance, making it much harder for households to pay down principal debt.

Home Equity Lines of Credit (HELOCs)

For homeowners, the prime rate is the primary driver of HELOC costs. Unlike traditional home equity loans which are often fixed, HELOCs are almost universally tied to the prime rate. In a rising rate environment, homeowners who tapped into their equity for renovations or debt consolidation may find their monthly interest-only payments doubling or tripling. This makes monitoring the “current prime rate today” essential for anyone utilizing their home’s value as a liquid resource.

Personal Loans and Private Student Debt

While federal student loans have rates set by Congress, many private student loans and unsecured personal loans are tied to the prime rate or LIBOR (now transitioning to SOFR). Borrowers in these categories must remain vigilant; a high prime rate environment suggests that refinancing variable-rate debt into a fixed-rate product should be a top financial priority to protect against further volatility.

The Broader Economic Implications for Business and Investment

The prime rate does not just affect the individual consumer; it serves as a throttle for the entire economy. It influences how businesses expand, how stocks are valued, and how much liquidity is circulating in the market.

Borrowing Costs for Small and Medium Enterprises (SMEs)

Small businesses are the backbone of the economy, and they are also the most sensitive to prime rate fluctuations. Most small business loans, including many SBA (Small Business Administration) loans, are pegged to the prime rate. When the rate is high, the cost of capital increases. This often leads to a slowdown in hiring, a reduction in capital expenditures (like buying new equipment), and a general tightening of business operations. For a business owner, a 1% increase in the prime rate could be the difference between a profitable year and a break-even year.

The Ripple Effect on the Stock and Real Estate Markets

Investors watch the prime rate closely because it represents the “opportunity cost” of capital. When the prime rate is high, “safe” investments like high-yield savings accounts or CDs become more attractive compared to the risky stock market. Furthermore, as borrowing costs rise for corporations (linked to the prime rate and corporate bond yields), their earnings often take a hit due to higher interest expenses. This can lead to downward pressure on stock valuations, particularly in growth sectors like technology that rely on heavy borrowing to fuel expansion.

Inflation Control and Consumer Spending

The primary reason the prime rate remains high in certain cycles is to combat inflation. By making it more expensive to borrow money, the Federal Reserve—via the prime rate—effectively reduces the amount of “cheap money” in the system. This cools demand for goods and services, which eventually brings prices down. For the savvy investor, understanding this cycle is key to timing entries into the market or shifting assets into inflation-protected securities.

Navigating the Current Rate Environment: Strategic Financial Moves

When the prime rate is elevated or volatile, “business as usual” is not an effective financial strategy. You must take proactive steps to insulate your net worth from the eroding effects of high interest rates.

Prioritizing Debt Liquidation

In a high prime rate environment, the “return on investment” for paying off debt is often higher than the expected return from the stock market. If your credit card is charging you 22% (Prime + 14%), paying off that balance is the equivalent of a guaranteed 22% return on your money. Financial advisors often recommend the “avalanche method” during these times—focusing all extra cash flow on the highest-interest variable debt first.

Re-evaluating Cash Reserves

On the flip side, a high prime rate usually coincides with higher yields on cash. If the prime rate is high, banks are forced to compete for your deposits to fund their lending. This is the ideal time to move dormant cash from a traditional checking account (yielding 0.01%) into a High-Yield Savings Account (HYSA) or a Certificate of Deposit (CD). In many cases, you can now find safe, liquid accounts yielding 4% to 5%, providing a silver lining to an otherwise expensive borrowing landscape.

Fixed-Rate Conversions and Refinancing

If you are currently holding a variable-rate loan and the outlook for the prime rate remains high or uncertain, it may be worth investigating a “fixed-rate conversion.” Many lenders allow you to lock in a portion of your HELOC balance at a fixed rate for a fee. While the fixed rate might be slightly higher than the current variable rate, it provides “certainty insurance” against future hikes.

Future Projections: When Will the Prime Rate Move?

Predicting the future of the prime rate requires keeping a close eye on the Federal Reserve’s “Dot Plot” and inflation data (CPI and PCE). Most economists agree that the era of “near-zero” interest rates is behind us for the foreseeable future. However, as inflation nears the Fed’s 2% target, the market begins to price in “rate cuts.”

When the Federal Reserve eventually pivots and begins to lower the federal funds rate, the prime rate will drop immediately. For consumers, this will offer a window of opportunity to refinance high-interest debt or take out new loans for major purchases like homes or vehicles. Until then, the mantra for personal finance remains: Minimize variable debt and maximize the yield on your cash.

In conclusion, the current prime rate is more than just a headline; it is a fundamental tool used to balance the global economy. By understanding how it is calculated, which of your financial products it affects, and how to pivot your strategy in response to its movement, you can maintain financial stability regardless of which way the economic winds blow. Monitoring the prime rate today is the first step toward a more disciplined and profitable financial tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.