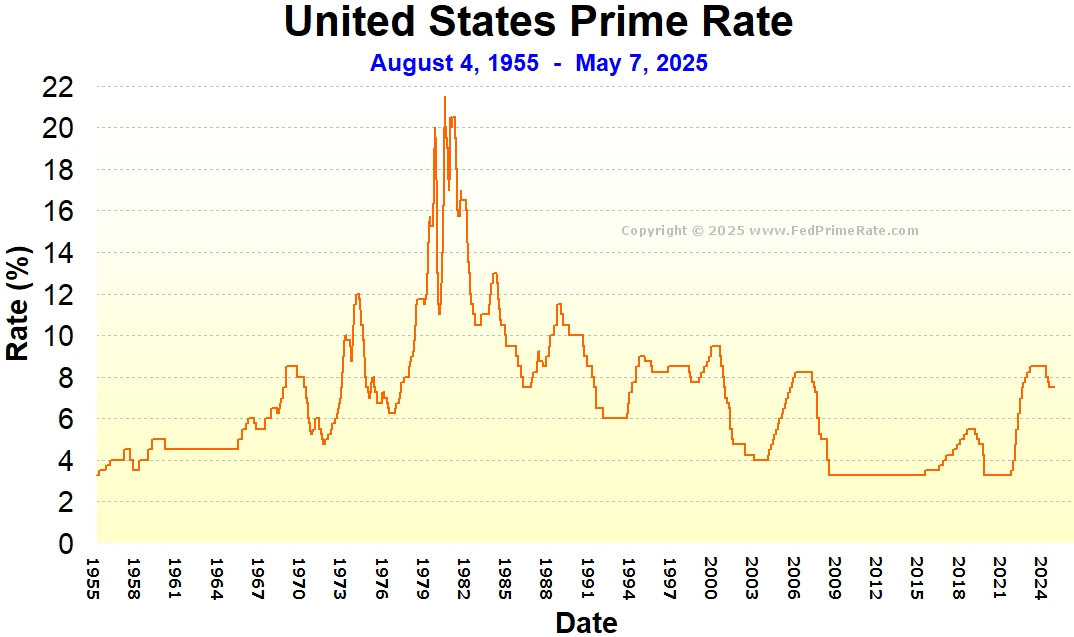

The prime interest rate serves as the foundational heartbeat of the American credit system. Often referred to simply as “the prime rate,” it is the base interest rate that commercial banks charge their most creditworthy corporate customers. While it might seem like a figure reserved for Wall Street boardrooms, its influence trickles down to almost every aspect of personal and business finance, from the interest on your credit card to the cost of a small business loan.

As of the current economic cycle, the prime rate has remained a focal point for investors and consumers alike. Understanding what it is, how it is determined, and why it fluctuates is essential for anyone looking to navigate the complexities of the modern financial landscape.

The Mechanics of the Prime Rate: How It Is Determined

The prime interest rate does not exist in a vacuum. It is inextricably linked to the monetary policy set by the Federal Reserve, the central bank of the United States. To understand the current prime rate, one must first understand the federal funds rate.

The Link to the Federal Reserve and the FOMC

The Federal Open Market Committee (FOMC) meets several times a year to determine the target range for the federal funds rate—the rate at which commercial banks lend to one another overnight. When the Fed decides to raise or lower this target range to combat inflation or stimulate economic growth, the prime rate follows suit almost immediately.

By industry standard, the prime rate is typically set 3 percentage points (300 basis points) above the upper bound of the federal funds target range. For example, if the Federal Reserve sets the federal funds rate at 5.5%, the prime rate will almost universally be adjusted to 8.5%. This spread allows banks to cover administrative costs and maintain a profit margin while providing a benchmark for lending.

The Wall Street Journal Prime Rate

While many banks set their own prime rates, the most widely recognized benchmark is the Wall Street Journal (WSJ) Prime Rate. The WSJ surveys the 30 largest banks in the United States; when at least 23 of them (three-quarters) change their prime rate, the WSJ updates its published figure. This creates a standardized reference point that lenders across the country use to peg their variable-interest financial products.

Why the Prime Rate Fluctuations Matter

The prime rate is a tool for economic equilibrium. During periods of high inflation, the Federal Reserve raises rates to “cool” the economy by making borrowing more expensive. Conversely, during a recession, the Fed lowers rates to encourage borrowing and spending. For the consumer, these fluctuations determine the “price” of money. When the prime rate is high, debt becomes a heavier burden; when it is low, it presents an opportunity for expansion and investment.

Impact on Consumer Credit and Personal Finance

For the average individual, the prime rate is most visible through variable-rate debt. Unlike fixed-rate mortgages or auto loans where the interest remains static, many common financial products are “indexed” to the prime rate.

Variable-Rate Credit Cards

Most credit cards carry a variable Annual Percentage Rate (APR). If you look at the fine print of your credit card agreement, you will likely see a formula such as “Prime Rate + 15.99%.” This means that every time the Federal Reserve moves the needle, your credit card interest rate moves in tandem. In a high-prime-rate environment, carrying a balance becomes significantly more expensive, as the interest charges compound on a higher base rate, making it harder for consumers to pay down principal balances.

Home Equity Lines of Credit (HELOCs)

HELOCs are one of the most prime-sensitive products in the mortgage industry. Unlike a standard 30-year fixed mortgage, a HELOC usually features a floating interest rate tied directly to the prime rate. For homeowners using a HELOC to fund renovations or consolidate debt, a 0.25% increase in the prime rate translates to an immediate increase in their monthly interest-only payments. This makes monitoring the prime rate vital for anyone utilizing their home equity as a revolving source of credit.

Personal Loans and Adjustable-Rate Mortgages (ARMs)

While many personal loans are fixed, some are variable, and nearly all Adjustable-Rate Mortgages (ARMs) use a benchmark that is influenced by the same economic forces that move the prime rate. When the prime rate is on an upward trajectory, borrowers with ARMs may face “payment shock” when their initial fixed-rate period ends and the loan resets to current market levels.

The Influence on Business Operations and Commercial Lending

The prime rate is not just a consumer metric; it is a primary driver of corporate strategy and small business viability. Businesses rely on credit to manage cash flow, purchase inventory, and invest in long-term growth.

Working Capital and Small Business Administration (SBA) Loans

Small businesses are particularly sensitive to the prime rate. Many Small Business Administration (SBA) loans, specifically the popular 7(a) loan program, have maximum interest rates tied to the prime rate. A rising prime rate increases the cost of capital for the local hardware store or the burgeoning tech startup. When the cost of servicing existing debt rises, businesses may have less capital available for hiring new employees or expanding their operations.

Capital Expenditure and Investment Decisions

For larger corporations, the prime rate influences the “hurdle rate”—the minimum rate of return a company expects on a project or investment. When the prime rate is high, the cost of borrowing to build a new factory or develop a new product line increases. Consequently, companies may become more conservative, delaying major capital expenditures until borrowing costs decrease. This slowdown in corporate spending is exactly what the Federal Reserve intends when it raises rates to dampen inflationary pressures.

Inventory Financing and Supply Chain Management

Many industries, such as automotive and retail, rely on “floor plan” financing or lines of credit to maintain inventory. Because these lines of credit are almost always variable and tied to the prime rate, a high-rate environment increases the “carrying cost” of inventory. This often leads to leaner inventory levels and can even result in higher prices for end consumers as businesses pass on their increased financing costs.

Current Market Trends and the Economic Outlook

Navigating the current prime interest rate requires an understanding of the broader economic signals that the Federal Reserve monitors. We are currently in a period of transition where the “easy money” era of near-zero interest rates has been replaced by a “higher-for-longer” philosophy.

Inflationary Pressures and the Fed’s Stance

The primary driver of the current prime rate level is the Consumer Price Index (CPI). The Federal Reserve has a dual mandate: to promote maximum employment and to maintain stable prices (targeting 2% inflation). After the spike in inflation following the global pandemic, the Fed embarked on one of the fastest rate-hiking cycles in history. This pushed the prime rate to levels not seen in over a decade. Currently, the market is closely watching for “disinflationary” trends—evidence that price growth is slowing—which would provide the Fed with the justification to lower the federal funds rate and, by extension, the prime rate.

Predictors for the Coming Years

Economists and market analysts utilize tools like the “Dot Plot”—a chart that summarizes the FOMC’s outlook for interest rates—to predict where the prime rate might go. While predictions are never guaranteed, the current consensus suggests a period of stabilization. If the labor market remains strong and inflation continues to cool, we may see a gradual reduction in the prime rate. However, any resurgence in inflation or geopolitical instability could lead the Fed to keep rates elevated to prevent the economy from overheating.

The Role of the Yield Curve

While the prime rate is a short-term benchmark, it is often viewed in relation to the yield on the 10-year Treasury note. A “normal” yield curve suggests that long-term rates should be higher than short-term rates. However, in recent times, we have seen an “inverted yield curve,” where short-term benchmarks (like those influencing the prime rate) are higher than long-term yields. This is often viewed as a precursor to an economic slowdown, which eventually leads to a lowering of the prime rate to jumpstart the economy.

Strategies to Manage Finances in a High-Interest Environment

When the prime rate is high, the financial playbook must change. Passive management of debt can lead to significant wealth erosion through interest payments.

Refinancing and Debt Consolidation

For those holding variable-rate debt, such as credit card balances or HELOCs, now is the time to explore fixed-rate alternatives. Debt consolidation loans with a fixed interest rate can “lock in” your costs, protecting you from future prime rate hikes. Even if the fixed rate seems high compared to historical norms, the certainty of a fixed payment can provide essential budget stability in a volatile market.

Prioritizing High-Interest Liabilities

In a high-prime-rate environment, the “Avalanche Method” of debt repayment becomes even more effective. This involves directing all discretionary income toward the debt with the highest interest rate (usually credit cards) while making minimum payments on others. Because the interest on these accounts is tied to the prime rate, every dollar of principal paid down saves more money today than it did several years ago.

Optimizing Cash Reserves

On the flip side, a high prime rate is often accompanied by higher yields on savings accounts, Money Market Accounts (MMAs), and Certificates of Deposit (CDs). While the prime rate represents the cost of borrowing, the “yield environment” represents the reward for saving. Savvy investors should ensure their cash reserves are sitting in High-Yield Savings Accounts (HYSA) that reflect the current interest rate environment, rather than traditional checking accounts that offer near-zero interest.

Strategic Business Borrowing

For business owners, timing is everything. If the prime rate is expected to fall in the next 12–18 months, it may be wise to utilize shorter-term financing or variable-rate loans with the intention of refinancing into a fixed-rate product once the Fed begins its easing cycle. Conversely, if you believe rates have not yet peaked, securing a fixed-rate loan now can protect your margins from further erosion.

Summary: Navigating the Ripple Effects

The current prime interest rate is more than just a percentage point; it is a reflection of the national economy’s health and the Federal Reserve’s strategy for the future. For the individual consumer, it dictates the cost of a lifestyle funded by credit. For the entrepreneur, it defines the feasibility of the next big venture.

By staying informed about the movements of the Federal Reserve and the resulting adjustments to the Wall Street Journal Prime Rate, you can make proactive decisions rather than reactive ones. Whether it is consolidating high-interest debt, moving savings to higher-yielding vehicles, or adjusting business expansion plans, understanding the prime rate empowers you to maintain control over your financial destiny in an ever-changing economic world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.