Understanding the Annual Percentage Rate (APR) is fundamental for anyone navigating the complex world of personal finance, whether you’re borrowing money for a home, a car, or simply using a credit card. It’s more than just a number; it’s a critical indicator of the true cost of borrowing, encompassing not only the interest rate but also most associated fees and charges. In a dynamic economic environment, the “current APR” is not a static figure but a moving target, influenced by a myriad of factors from central bank policies to individual creditworthiness. Grasping these nuances is essential for making informed financial decisions, optimizing your borrowing costs, and effectively managing your debt. This article delves into what APR truly represents, how it’s calculated, the factors that dictate its current levels across various financial products, and strategies to secure the most favorable rates.

Decoding APR: Beyond Just a Number

The Annual Percentage Rate (APR) is a cornerstone concept in finance, yet its full implications are often misunderstood. While many consumers focus solely on the interest rate, the APR provides a more comprehensive and accurate picture of the total cost of borrowing over a year. This distinction is crucial for comparing different loan products and understanding your financial commitments.

The Fundamental Definition of APR

At its core, the APR represents the annual rate charged for borrowing or earned through an investment. For borrowers, it’s the cost of credit expressed as a yearly percentage. What sets APR apart from a simple interest rate is its inclusiveness. It takes into account not only the nominal interest rate but also various fees associated with the loan, such as origination fees, closing costs, discount points, and sometimes even mortgage insurance premiums (though rules vary by loan type). By consolidating these costs into a single percentage, the APR provides a standardized metric that allows consumers to make apples-to-apples comparisons between different loan offers. This transparency is vital, as a loan with a seemingly lower interest rate might end up being more expensive overall due to higher hidden fees, which the APR would reveal. For instance, a loan with a 5% interest rate but significant upfront fees might have an APR of 5.5% or higher, making it less attractive than a loan with a 5.2% interest rate but no additional charges.

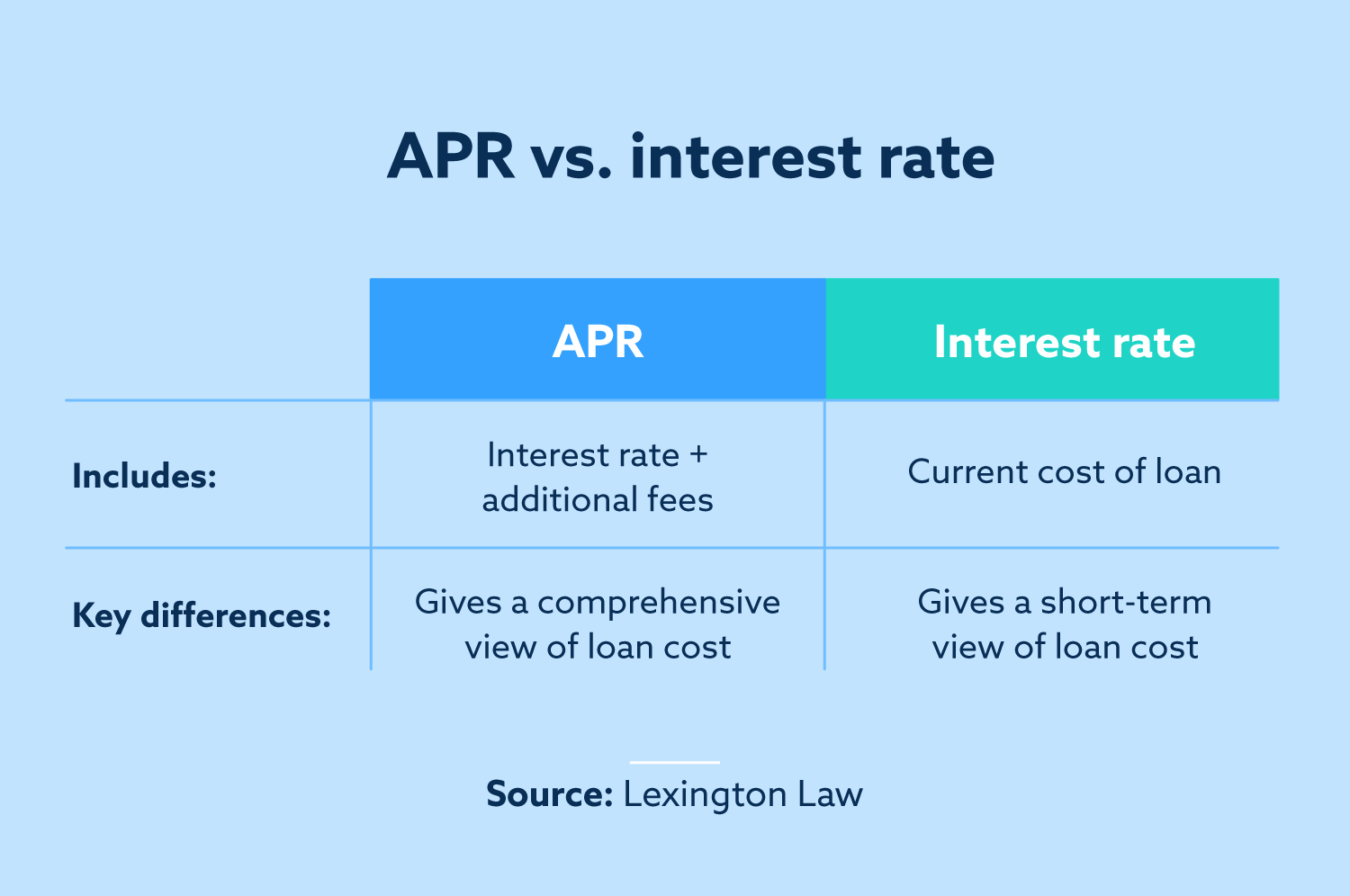

APR vs. Interest Rate: A Crucial Distinction

While often used interchangeably in casual conversation, the interest rate and APR are distinct financial terms with different implications. The interest rate is simply the percentage charged by a lender for the use of borrowed money, usually expressed on an annual basis. It’s the primary component of your borrowing cost but doesn’t tell the whole story. The APR, conversely, offers a broader view. It includes the interest rate, but then adds most other charges and fees that the borrower must pay to get the loan. For example, on a mortgage, the interest rate dictates your monthly payment amount for the principal and interest portion. However, the APR will factor in closing costs like appraisal fees, loan processing fees, and points paid to reduce the interest rate. Therefore, the APR will almost always be higher than the stated interest rate, making it a more accurate representation of the total cost of credit over the life of the loan. Understanding this difference is paramount: when comparing loan offers, always prioritize the APR as the most comprehensive metric for cost evaluation.

Why APR Varies: Factors Influencing the Rate

The “current APR” for any given financial product is not a single, universal number. Instead, it fluctuates significantly based on a multitude of factors, broadly categorized into macroeconomic conditions and individual borrower characteristics. At the macroeconomic level, the most influential factor is the federal funds rate, set by a country’s central bank (e.g., the Federal Reserve in the U.S.). This benchmark rate impacts interest rates across the entire economy. When the central bank raises rates to combat inflation, borrowing costs generally increase, leading to higher APRs. Conversely, rate cuts typically result in lower APRs. Inflation expectations, the overall economic outlook, and the bond market also play significant roles. For individual borrowers, creditworthiness is paramount. Lenders assess risk based on your credit score, credit history, debt-to-income ratio, and income stability. Borrowers with excellent credit scores (e.g., 760+) are perceived as lower risk and therefore qualify for the most competitive, lower APRs. Those with lower scores or a checkered credit history will face higher APRs as compensation for the increased risk to the lender. Additionally, the type of loan, the loan term (e.g., 15-year vs. 30-year mortgage), the loan amount, the presence of collateral, and even the lender’s own profit margins and competitive landscape all contribute to the final APR offered.

Current APR Landscape Across Key Financial Products

The “current APR” is a dynamic figure that varies wildly depending on the specific financial product. What’s considered a good APR for a credit card would be exorbitant for a mortgage, and vice versa. Each product category operates under different risk profiles, market conditions, and regulatory frameworks, leading to distinct APR ranges.

Credit Cards: Understanding Purchase, Balance Transfer, and Cash Advance APRs

Credit cards typically feature some of the highest APRs among consumer lending products, reflecting their unsecured nature and the convenience they offer. A single credit card can have multiple APRs:

- Purchase APR: This is the rate applied to new purchases if you don’t pay your balance in full by the due date. Current purchase APRs can range from the low double digits (e.g., 15-18%) for those with excellent credit and promotional offers, to well over 25-30% for standard cards or those for individuals with less-than-perfect credit. The current economic climate, particularly inflation and central bank rate hikes, has generally pushed these rates higher.

- Balance Transfer APR: Many cards offer promotional 0% APR periods for balance transfers, typically lasting 6-21 months, often with a balance transfer fee (e.g., 3-5% of the transferred amount). After the promotional period, the rate reverts to a standard purchase APR, which can be high.

- Cash Advance APR: This is usually the highest APR on a credit card, often starting immediately with no grace period, and can exceed 30%. Cash advances also typically incur a separate transaction fee.

Factors influencing credit card APRs include your credit score, the card issuer’s risk assessment, the type of card (e.g., rewards card, secured card), and prevailing market interest rates.

Personal Loans: Fixed vs. Variable Rates and Eligibility Factors

Personal loans offer a lump sum of money that is repaid in fixed monthly installments over a set period, typically 1 to 7 years. APRs for personal loans are generally lower than credit card APRs but higher than secured loans like mortgages.

- Fixed-Rate Personal Loans: The APR remains constant throughout the loan term, providing predictable monthly payments. Current fixed APRs can range from as low as 6-8% for borrowers with excellent credit and strong income, up to 30-36% for those with lower credit scores.

- Variable-Rate Personal Loans: The APR can fluctuate based on a benchmark index (e.g., the prime rate), meaning your monthly payments could change. While they may start lower than fixed rates, they carry the risk of increasing over time. Variable rates are less common for traditional personal loans but do exist.

Key eligibility factors driving personal loan APRs include your credit score (the higher, the better), debt-to-income ratio, income stability, and the loan term. Shorter loan terms often come with slightly lower APRs as they represent less risk to the lender.

Mortgages: The Impact of Credit Score, Loan Term, and Market Conditions

Mortgage APRs are typically among the lowest borrowing rates due to the secured nature of the loan (the property serves as collateral). However, they are highly sensitive to market conditions and individual borrower profiles.

- Fixed-Rate Mortgages (e.g., 30-year, 15-year): These are the most common, offering a consistent interest rate and payment for the life of the loan. Current APRs for 30-year fixed mortgages can fluctuate significantly based on economic indicators like inflation, the federal funds rate, and bond yields. A period of high inflation or aggressive central bank tightening can push these rates up, sometimes into the 6-8% range, while periods of economic stability or easing monetary policy can bring them down to 3-5% or even lower. 15-year fixed mortgages typically have slightly lower APRs than 30-year ones, but higher monthly payments.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an initial fixed-rate period (e.g., 3, 5, 7, or 10 years) followed by an adjustable rate that changes periodically based on a benchmark index. Initial APRs for ARMs are often lower than fixed-rate mortgages, making them attractive for borrowers planning to sell or refinance before the adjustment period. However, they carry the risk of significantly higher payments in the future.

Your credit score (generally 740+ for the best rates), loan-to-value (LTV) ratio (influenced by down payment size), debt-to-income ratio, and current market conditions are critical in determining your mortgage APR.

Auto Loans: New vs. Used Cars and Lender Competition

Auto loan APRs generally fall between personal loan and mortgage rates. They are secured by the vehicle itself, reducing lender risk compared to unsecured personal loans.

- New Car Loans: Dealers often offer promotional APRs as low as 0-3% for highly qualified buyers on specific models, often subsidized by manufacturers. Otherwise, standard new car APRs can range from 4-8% for excellent credit.

- Used Car Loans: Used car loans typically carry higher APRs than new car loans, reflecting the increased depreciation risk and potential for mechanical issues with older vehicles. Current APRs can range from 6-12% for good credit, escalating significantly for lower credit scores.

Factors influencing auto loan APRs include your credit score, the car’s age and mileage (for used cars), the loan term, the down payment amount, and the competitive landscape among lenders (banks, credit unions, dealership financing). Credit unions often offer highly competitive auto loan rates.

How Current APRs Impact Your Financial Decisions

The APR is not merely a technical detail; it is a fundamental determinant of your financial health and capacity. Its current levels directly influence the cost of credit, the feasibility of major purchases, and the effectiveness of debt management strategies.

The Cost of Borrowing: Calculating Total Repayment

The most direct impact of current APRs is on the total cost of borrowing. A higher APR translates to a larger portion of your monthly payment going towards interest, rather than principal. Over the lifespan of a loan, even a seemingly small difference in APR can result in thousands, or even tens of thousands, of dollars in additional costs. For example, on a $300,000 30-year mortgage:

- At a 6.0% APR, the total interest paid would be approximately $347,515.

- At a 7.0% APR, the total interest paid would jump to approximately $419,000.

This $71,485 difference in interest cost for just a one percentage point rise in APR vividly illustrates how crucial securing a lower rate is. Similarly, on a $10,000 personal loan over 5 years: - At 10% APR, total interest is about $2,748.

- At 15% APR, total interest rises to about $4,275.

These calculations underscore that current APRs dictate not just your monthly outlay but your overall financial commitment and the efficiency with which you can allocate your resources.

Comparing Offers: The Importance of a Low APR

In a competitive lending market, you will likely receive multiple offers for the same type of loan. Focusing on the APR is the most effective way to compare these offers accurately. As established, the APR includes most fees beyond the nominal interest rate, providing a standardized basis for comparison. A lender might entice you with a slightly lower interest rate, but if their associated fees (like origination fees or discount points) are substantially higher, their overall APR could be less favorable than a competitor’s. Always request and scrutinize the APR when evaluating loan proposals. This disciplined approach ensures you are considering the true, all-inclusive cost of borrowing, preventing you from falling prey to offers that look good on the surface but are expensive in the long run. Savvy borrowers understand that a fraction of a percentage point in APR can translate into significant savings over the loan’s term.

Strategizing Debt Management with Current Rates

Current APRs play a pivotal role in debt management strategies. High-APR debts, like many credit card balances or older personal loans, erode your financial progress rapidly due to accruing interest. When APRs are high across the board, consumers carrying revolving debt face an uphill battle. Strategies like the “debt snowball” or “debt avalanche” methods become even more critical, prioritizing the elimination of high-interest debt first. Furthermore, understanding current APR trends is essential for refinancing decisions. If prevailing market APRs for mortgages, auto loans, or personal loans have dropped significantly since you took out your original loan, refinancing could potentially save you a substantial amount of money by securing a lower rate. Conversely, if current APRs are rising, it might be a good time to consolidate variable-rate debts into a fixed-rate loan to lock in a predictable payment before rates climb further. Monitoring and understanding the current APR environment empowers you to make timely decisions that can significantly reduce your financial burden and accelerate your path to debt freedom.

Navigating the Market: Strategies for Securing Favorable APRs

Given the profound impact of APRs on your financial life, proactively seeking the best possible rates is a crucial financial skill. While market conditions are beyond individual control, several strategies can significantly improve your chances of securing a favorable APR, leading to substantial savings over the life of your loans.

Building and Maintaining a Strong Credit Score

Your credit score is arguably the most influential factor in determining the APRs you’re offered. Lenders use it as a primary indicator of your creditworthiness and the likelihood of you repaying your debts. A higher credit score (typically FICO scores above 740-760) signals lower risk to lenders, enabling you to qualify for the most competitive, lowest APRs. To build and maintain a strong credit score:

- Pay bills on time, every time: Payment history is the most important factor in your credit score.

- Keep credit utilization low: Aim to use no more than 30% (ideally less than 10%) of your available credit on revolving accounts.

- Maintain a long credit history: The longer your credit accounts have been open and in good standing, the better.

- Diversify your credit mix: A healthy mix of credit (e.g., credit cards, installment loans) shows responsible management.

- Avoid unnecessary new credit applications: Each hard inquiry can temporarily ding your score.

By diligently managing your credit, you position yourself to access better rates across all lending products.

Shopping Around and Negotiating with Lenders

Never accept the first loan offer you receive. The lending market is highly competitive, and different institutions—banks, credit unions, online lenders, and even peer-to-peer platforms—have varying risk appetites, overheads, and target customer segments. This means their APRs for the exact same borrower profile can differ significantly.

- Get multiple quotes: Apply to several lenders for the same type of loan within a short window (typically 14-45 days for most credit models, as multiple inquiries for the same type of loan are often treated as a single inquiry).

- Compare APRs, not just interest rates: As discussed, APR provides the true cost.

- Leverage offers: Use a better offer from one lender to negotiate a lower APR with another, particularly if you have a preferred banking relationship.

- Consider credit unions: Credit unions are member-owned and often offer lower rates and more flexible terms than traditional banks.

This proactive approach can save you a significant amount over the life of a loan.

Understanding Loan Terms and Hidden Fees

While APR is a comprehensive metric, it’s still vital to read the fine print of any loan agreement.

- Grace periods: For credit cards, understand if there’s a grace period before interest accrues on new purchases.

- Prepayment penalties: Ensure there are no penalties for paying off your loan early, which could negate some of the benefits of securing a low APR.

- Variable rate caps: For ARMs or variable personal loans, understand the maximum rate your APR can reach.

- Late payment fees: Be aware of charges for missed payments, which can add substantially to your borrowing cost.

A thorough understanding of all terms and conditions ensures you’re not caught off guard by unexpected costs that could effectively raise your overall borrowing expense, even with a seemingly low APR.

The Role of Economic Indicators and Central Bank Policies

Staying informed about broader economic trends can also help you time your borrowing decisions. Central banks’ decisions on benchmark interest rates (like the federal funds rate) directly influence the cost of borrowing for financial institutions, which in turn affects consumer APRs.

- Rising rates: If the central bank signals future rate hikes, it might be prudent to lock in a fixed-rate loan sooner rather than later to avoid higher APRs.

- Falling rates: If rates are expected to drop, waiting a few months to apply for a loan or considering a variable-rate product might be beneficial, especially for a large loan like a mortgage where a small rate difference translates to significant savings.

- Inflation: High inflation often leads to higher interest rates and consequently higher APRs, as lenders seek to maintain the real value of their returns.

While you can’t control these macro factors, awareness empowers you to make more strategic borrowing choices.

The Future of APRs: What to Expect

The financial landscape is ever-evolving, and APRs are no exception. Predicting future movements with absolute certainty is impossible, but by understanding key economic drivers and technological shifts, consumers can better anticipate trends and prepare their financial strategies accordingly. The direction of APRs will largely be shaped by global economic conditions, the ongoing battle against inflation, and the continued innovation in the financial technology sector.

Inflation and Interest Rate Trends

The most significant factor influencing future APRs will undoubtedly be the trajectory of inflation and the corresponding responses from central banks worldwide. In periods of high inflation, central banks typically raise their benchmark interest rates to cool down the economy and stabilize prices. This, in turn, cascades through the financial system, leading to higher APRs across nearly all lending products, from mortgages and auto loans to credit cards and personal loans.

Conversely, if inflation moderates and central banks feel confident that price stability is being restored, they may begin to lower interest rates, resulting in a general decrease in APRs. The “current APR” is, therefore, a snapshot in an ongoing economic cycle. Consumers should closely monitor inflation reports, central bank policy statements, and economists’ forecasts to gauge the likely direction of rates. Persistent inflation could mean higher APRs for the foreseeable future, while a return to lower, stable inflation could herald a period of more affordable borrowing.

Technological Advancements in Lending

Technology is rapidly transforming the lending industry, with significant implications for how APRs are determined and offered.

- AI and Machine Learning: Lenders are increasingly using artificial intelligence and machine learning algorithms to assess creditworthiness more accurately and efficiently. These advanced analytics can process vast amounts of data beyond traditional credit scores, potentially offering more personalized APRs based on a holistic view of a borrower’s financial behavior. This could lead to more tailored rates for individuals who might be overlooked by traditional models but are genuinely creditworthy.

- Blockchain and Decentralized Finance (DeFi): While still nascent for mainstream lending, blockchain technology and DeFi platforms could revolutionize lending by reducing intermediaries and operational costs. If adopted widely, this could theoretically lead to lower APRs for borrowers by cutting down on institutional overhead.

- Fintech Innovation: The rise of fintech companies continues to introduce new lending models and competition. These agile players often leverage technology to streamline the application process, offer faster approvals, and sometimes provide more competitive APRs to specific market segments. This increased competition generally benefits consumers by pushing traditional lenders to innovate and offer better rates.

Consumer Empowerment and Financial Literacy

The future will also see a greater emphasis on consumer empowerment and financial literacy as tools for navigating APRs. With an abundance of online comparison tools, educational resources, and transparent lending platforms, consumers are increasingly equipped to understand, compare, and negotiate for better rates.

- Personalized Financial Management Tools: Apps and platforms that track spending, monitor credit scores, and recommend optimal debt strategies will become even more sophisticated, helping individuals manage their finances to qualify for lower APRs.

- Greater Transparency: Regulatory bodies and consumer advocates will continue to push for greater transparency in lending, ensuring that all fees are clearly communicated and APRs accurately reflect the total cost of borrowing.

- Focus on Financial Wellness: As more employers and financial institutions prioritize financial wellness programs, a more financially literate population will be better positioned to understand the impact of APRs and make smarter borrowing decisions, thereby demanding more competitive rates from the market.

In conclusion, the “current APR” is a reflection of a complex interplay of global economics, individual financial health, and technological innovation. While rates will always fluctuate, a proactive approach centered on understanding these dynamics and employing smart financial strategies will be key to securing the most favorable APRs in the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.