The phrase “cost of living” is a ubiquitous term in economic discussions and personal financial planning, yet its full implications are often overlooked. At its core, the cost of living represents the amount of money needed to cover basic expenses such as housing, food, transportation, healthcare, and taxes in a certain place and time. It is a critical metric for understanding economic well-being, informing personal financial decisions, and even guiding policy-making. For individuals, understanding the cost of living is the first step towards achieving financial stability, making informed career choices, and planning for major life events like relocation or retirement. For businesses, it influences decisions on employee compensation and expansion. This comprehensive guide will dissect the cost of living, exploring its components, the factors that influence it, methods for measurement, and strategies for managing it effectively.

Understanding the Fundamentals of Cost of Living

To truly grasp the significance of the cost of living, one must first define its boundaries and identify its constituent elements. It’s more than just the price tag on goods; it’s a holistic view of the financial demands placed upon an individual or household in a specific geographical context.

Defining the Cost of Living

The cost of living can be formally defined as the expense of maintaining a certain standard of living. It encompasses the aggregate cost of essential goods and services required for everyday life. This standard is not universally fixed; it varies based on individual expectations, societal norms, and the economic development of a region. For example, what is considered a “basic” necessity in a highly developed nation might be a luxury in a developing one. The concept is intrinsically linked to purchasing power – how much goods and services a unit of currency can buy. When the cost of living increases without a corresponding rise in income, purchasing power diminishes, leading to a decline in the standard of living. This often necessitates adjustments in spending habits or an increased reliance on credit, impacting long-term financial health. Economists and policymakers frequently use the cost of living as an indicator of inflation, economic health, and the overall affordability of a region.

Key Components of the Cost of Living Index

While the specific items can vary, most cost of living calculations and indices focus on several core categories that represent the bulk of household expenditures. Understanding these components helps individuals pinpoint where their money is going and where potential savings might lie.

- Housing: This is typically the largest single component of the cost of living. It includes rent or mortgage payments, property taxes, homeowner’s insurance, and utilities (electricity, gas, water, internet). Housing costs can vary dramatically not just between cities but even within different neighborhoods of the same city, heavily influencing the overall affordability of an area.

- Food: Encompassing groceries purchased for home cooking and meals eaten out, food expenses are a fundamental necessity. Prices can fluctuate based on local agricultural conditions, supply chains, and consumer demand. Dietary preferences and lifestyle choices (e.g., frequent dining out vs. cooking at home) also significantly impact this category.

- Transportation: This includes costs associated with commuting and personal travel, such as public transport fares, fuel, car maintenance, insurance, and vehicle payments. Proximity to work, the availability of public transit, and car ownership rates play a crucial role in determining these expenses.

- Healthcare: Medical expenses can be unpredictable and substantial. This category covers health insurance premiums, deductibles, co-pays, prescription medications, and other medical services. The structure of a country’s healthcare system (e.g., universal vs. private insurance) profoundly impacts these costs.

- Education: For many, this includes tuition fees, school supplies, textbooks, and related expenses for children or adult education. The cost of education, particularly higher education, can be a significant long-term financial burden and a major consideration in family budgeting.

- Personal Care and Recreation: This broad category covers a range of discretionary and semi-discretionary spending, including clothing, toiletries, entertainment (movies, concerts, hobbies), gym memberships, and vacations. While some might consider these non-essentials, a certain level of personal care and leisure contributes to overall well-being and is often included in standard living calculations.

- Taxes: Income taxes, sales taxes, and other local levies directly reduce disposable income and are therefore a critical, albeit often overlooked, part of the true cost of living.

Factors Influencing Cost of Living

The cost of living is not static; it’s a dynamic figure shaped by a confluence of geographical, economic, and individual factors. Awareness of these influences empowers individuals to make more strategic financial decisions.

Geographical Variations: Location, Location, Location

Perhaps the most significant determinant of the cost of living is geographical location. Major metropolitan areas, particularly global economic hubs, almost invariably have a higher cost of living compared to rural areas or smaller towns. This disparity is primarily driven by:

- Demand for Resources: High population density in cities increases demand for housing, leading to higher rents and property values. Similarly, demand for goods and services drives up prices due to limited supply or increased operational costs for businesses.

- Economic Opportunity: Cities often concentrate high-paying jobs, which, while beneficial for income, can also contribute to higher prices as more people can afford to pay more. This creates a supply-demand imbalance across various sectors.

- Infrastructure and Services: Regions with robust infrastructure, high-quality public services (like schools and transit), and cultural amenities often command higher living costs. The cost of providing these services is often passed on to residents through higher taxes or direct user fees.

- Local Policies and Regulations: Zoning laws, building codes, and taxation policies enacted by local governments can significantly impact housing supply and overall business costs, which are then reflected in consumer prices.

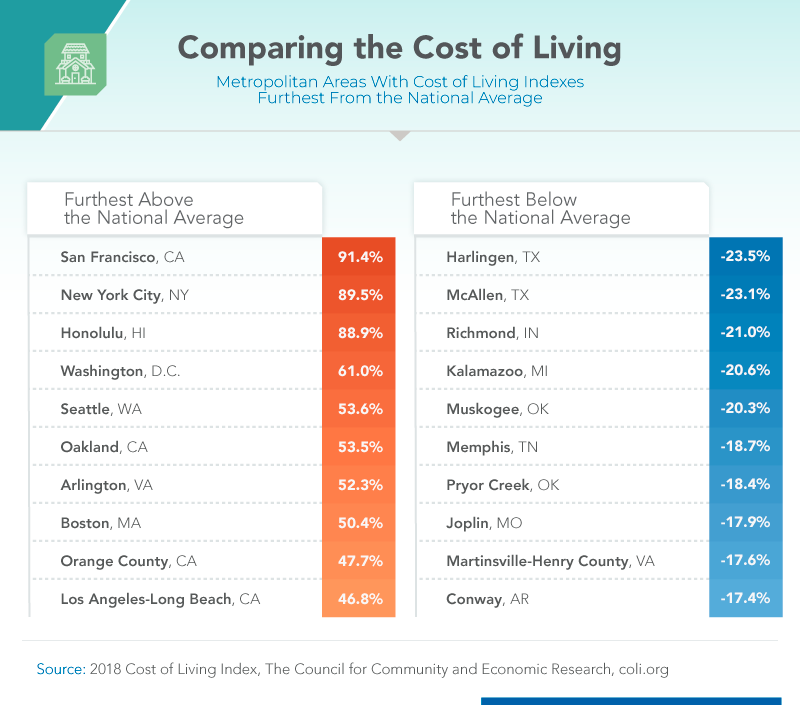

A move from San Francisco to a smaller city in the Midwest, for instance, would likely result in a dramatic decrease in housing expenses, even if salaries also adjust. Understanding these geographical nuances is paramount for anyone considering relocation for work or lifestyle changes.

Economic Indicators: Inflation and Market Dynamics

Beyond location, broader economic forces exert considerable influence on the cost of living. These macroeconomic factors can impact everyone, regardless of where they live.

- Inflation: This is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. Persistent inflation means that the same amount of money buys less over time, directly increasing the cost of living for everyone. Central banks monitor inflation closely and adjust monetary policy (like interest rates) to try and keep it stable.

- Supply and Demand: Fundamental economic principles dictate that when demand for a good or service exceeds its supply, prices tend to rise. Conversely, an oversupply can drive prices down. Disruptions in global supply chains, natural disasters affecting production, or sudden shifts in consumer preferences can all impact the cost of essential goods.

- Interest Rates: Changes in interest rates by central banks affect borrowing costs for mortgages, car loans, and credit cards. Higher interest rates make borrowing more expensive, increasing the cost of debt service for individuals and potentially slowing down economic activity.

- Wages and Income Growth: While not a direct component of the cost of living, wage growth plays a crucial role in its affordability. If wages do not keep pace with inflation and rising costs, the actual standard of living for workers can decline, even if nominal incomes increase.

- Government Policies: Fiscal policies (taxation, government spending) and regulatory policies (environmental standards, labor laws) can directly or indirectly impact prices and the cost of doing business, which are then passed on to consumers.

Lifestyle Choices: The Personal Variable

While external factors significantly shape the baseline cost of living, individual lifestyle choices introduce a highly personal variable. Two individuals living in the same city with identical incomes can experience vastly different costs of living based on their spending habits.

- Housing Choices: Opting for a larger home, a premium neighborhood, or a newly built property will inherently incur higher costs than choosing a smaller, older, or less centrally located residence.

- Consumption Patterns: A preference for organic, gourmet food items versus budget-friendly staples, frequent dining out versus home-cooked meals, or brand-name goods versus generic alternatives significantly impacts food and personal care budgets.

- Transportation Habits: Relying on private vehicles for every trip, especially gas-guzzling models, will be more expensive than utilizing public transport, cycling, or walking. The frequency and distance of travel also play a role.

- Leisure and Entertainment: Engaging in expensive hobbies, frequent international travel, or attending high-cost entertainment events adds considerably to discretionary spending, which some might consider part of their “standard of living.”

- Financial Discipline: Prudent budgeting, saving, and avoiding high-interest debt can lower the effective cost of living by reducing interest payments and facilitating smarter purchasing decisions. Conversely, reliance on credit and impulse buying can artificially inflate one’s personal cost of living.

These personal choices highlight that while a general cost of living exists for an area, an individual’s actual financial burden is often a reflection of their chosen lifestyle.

Measuring and Comparing the Cost of Living

To make informed decisions, individuals and organizations rely on various tools and methodologies to measure and compare the cost of living across different regions. These tools provide valuable benchmarks for financial planning, relocation, and salary negotiations.

Cost of Living Indices: Tools for Comparison

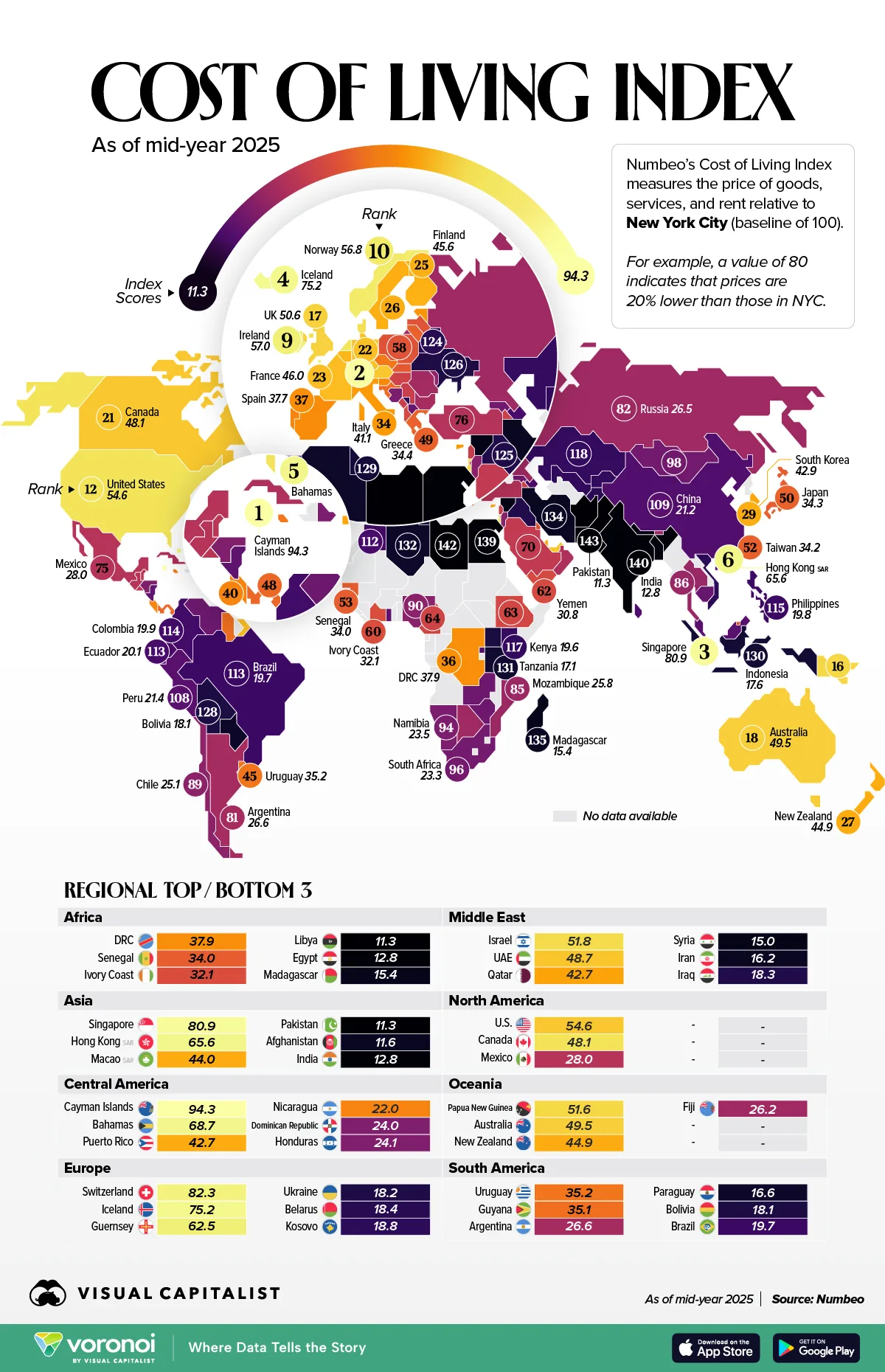

The most common method for measuring and comparing the cost of living is through Cost of Living Indices (COLI). These indices typically compare the price of a standardized basket of goods and services in different locations relative to a base city (often New York City, or an average of national cities, set to 100).

- Consumer Price Index (CPI): While not a direct COLI, the CPI, published by government agencies (like the Bureau of Labor Statistics in the U.S.), measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. It is the most widely used measure of inflation and provides a general sense of how the cost of living is changing nationally or regionally over time.

- City-to-City Indices: Several private organizations (e.g., Numbeo, Mercer, Economist Intelligence Unit) publish detailed city-to-city cost of living indices. These indices typically break down costs by category (housing, groceries, utilities, transportation) and allow users to compare hundreds of cities worldwide. They are particularly useful for multinational corporations relocating employees or individuals planning an international move.

- Poverty Lines and Living Wage Calculators: These tools focus on determining the minimum income required to afford basic necessities in a particular area, often considering local housing, food, and childcare costs. They are crucial for social policy and understanding economic hardship.

These indices, while valuable, should be interpreted with caution. They are averages and may not perfectly reflect an individual’s specific spending patterns or desired standard of living. However, they provide excellent starting points for research and comparison.

Real-World Applications: Relocation and Financial Planning

Understanding and utilizing cost of living data has practical implications across various aspects of financial decision-making:

- Relocation Decisions: For individuals considering moving for a job or lifestyle change, comparing the cost of living between their current location and a prospective one is essential. A higher salary in a new city might be offset by significantly higher housing or childcare costs, resulting in a lower actual standard of living. COLI tools help assess the real purchasing power of a new salary offer.

- Salary Negotiations: Both employees and employers use cost of living data. Employees can leverage this information to argue for higher compensation when moving to a more expensive area. Employers use it to set competitive salary ranges that attract talent while remaining financially viable.

- Retirement Planning: Retirees often seek areas with a lower cost of living to make their savings and fixed income stretch further. Analyzing COLI for potential retirement destinations is a critical step in ensuring financial security during non-working years.

- Budgeting and Expense Management: By understanding the typical cost of various expenses in their area, individuals can set realistic budgets, identify areas where they might be overspending compared to averages, and find opportunities to save.

- Investment Decisions: For investors, understanding regional economic health, influenced by the cost of living and wage growth, can inform decisions related to real estate, local businesses, and regional market trends.

Strategies for Managing Your Cost of Living

Armed with an understanding of what the cost of living entails and the factors that influence it, individuals can proactively implement strategies to manage and even reduce their personal financial burden. Effective management is about balancing income with expenses to achieve financial well-being.

Budgeting and Financial Planning

The cornerstone of managing the cost of living is a robust budget. A budget is a detailed plan for how you will spend and save your money, based on your income and expenses.

- Track Your Spending: Before you can budget effectively, you need to know where your money is going. Use budgeting apps, spreadsheets, or even pen and paper to meticulously record all income and expenses for at least a month.

- Categorize Expenses: Group your spending into categories like housing, food, transportation, debt payments, and discretionary spending. This allows you to visualize your financial outflows and identify patterns.

- Distinguish Needs vs. Wants: Clearly separate essential expenditures (needs) from non-essential ones (wants). This distinction is vital for making cuts when necessary.

- Set Realistic Goals: Based on your tracking and categorization, allocate specific amounts to each category. The “50/30/20 rule” (50% for needs, 30% for wants, 20% for savings/debt repayment) is a popular guideline, but it can be adjusted to fit individual circumstances.

- Regular Review and Adjustment: A budget is not a static document. Life changes, and so should your budget. Review it regularly (monthly or quarterly) and make adjustments as needed to ensure it remains relevant and effective.

Effective budgeting transforms an abstract cost of living into concrete, manageable figures, empowering individuals to take control of their finances rather than being controlled by them.

Smart Spending and Saving Habits

Beyond simply budgeting, adopting smarter spending and saving habits can significantly reduce the actual money required to maintain your desired lifestyle.

- Housing Optimization: Can you downsize? Find a roommate? Negotiate your rent? Refinance your mortgage? Even small adjustments to your largest expense can yield substantial savings. Consider areas slightly outside city centers for potentially lower housing costs.

- Grocery Bill Reduction: Plan meals, create shopping lists, buy in bulk when practical, utilize coupons, and avoid impulse purchases. Cooking at home is almost always cheaper than dining out. Explore farmers’ markets for fresh, often more affordable produce.

- Transportation Alternatives: If feasible, consider public transportation, carpooling, cycling, or walking to work. If you own a car, regular maintenance can prevent costly repairs, and shopping around for better insurance rates can save money.

- Energy Efficiency: Reducing utility bills through energy-efficient appliances, smart thermostats, proper insulation, and mindful usage (turning off lights, unplugging electronics) can lead to notable savings over time.

- Debt Management: High-interest debt (credit cards, personal loans) can significantly inflate your cost of living through interest payments. Prioritize paying down these debts, perhaps using strategies like the debt snowball or avalanche method.

- Value-Based Shopping: For non-essential items, practice mindful consumption. Research purchases, compare prices, wait for sales, and consider second-hand options. Differentiating between “value” and “cheap” is key; sometimes a higher upfront cost for durability saves money in the long run.

- Automate Savings: Set up automatic transfers from your checking account to your savings account each payday. This “pay yourself first” strategy ensures that saving becomes a consistent habit rather than an afterthought.

These habits, collectively, create a more resilient financial profile, allowing individuals to navigate economic fluctuations with greater ease.

Income Generation and Optimization

While managing expenses is crucial, increasing income is another powerful lever for making the cost of living more manageable.

- Career Advancement: Invest in skills and education that can lead to promotions, raises, or higher-paying job opportunities. Continuous learning and professional development are vital in a dynamic job market.

- Side Hustles: Explore opportunities to earn extra income outside your primary job. This could include freelancing, consulting, driving for ride-sharing services, delivering food, or selling handmade goods. A side hustle can provide supplementary income to cover discretionary expenses or accelerate savings goals.

- Passive Income Streams: Investigate options for generating passive income, such as dividend stocks, rental properties, or royalties. While these often require an initial investment of time or capital, they can provide recurring income with minimal ongoing effort.

- Negotiate Salaries: Don’t shy away from negotiating your salary when starting a new job or during annual reviews. Research industry standards and your market value to ensure you are being compensated fairly, especially if you live in a high-cost area.

- Leverage Financial Tools: Utilize tools that help you optimize your income, such as tax planning software to maximize deductions or investment platforms to grow your wealth over time.

A multi-faceted approach, combining astute expense management with strategic income generation, provides the most robust defense against the rising cost of living.

The Broader Implications of Cost of Living

The concept of the cost of living extends far beyond individual budgets, touching upon the health of personal finances, societal well-being, and broader economic stability. Its implications resonate through every layer of the economy.

Impact on Personal Financial Health

For individuals and families, the cost of living is a direct determinant of financial stress, savings potential, and overall economic security.

- Financial Stress and Mental Well-being: A high or rapidly increasing cost of living, especially when not matched by income growth, can lead to significant financial stress. This stress can manifest in anxiety, sleep disturbances, and strained relationships, impacting overall mental and physical health.

- Savings and Investment Capacity: When a large portion of income is consumed by basic necessities, the ability to save for emergencies, retirement, or long-term goals (like a home or education) is severely curtailed. This limits wealth accumulation and future financial security.

- Debt Accumulation: To bridge the gap between insufficient income and a high cost of living, many individuals resort to borrowing, leading to increased debt. This debt, particularly high-interest consumer debt, traps individuals in a cycle of payments, further exacerbating their financial challenges.

- Delayed Life Milestones: High costs can force individuals to delay major life milestones such as marriage, starting a family, purchasing a home, or retiring. This impacts personal aspirations and can have broader demographic consequences.

- Disparity and Inequality: The cost of living often affects low-income households disproportionately, as a larger percentage of their income goes towards necessities. This exacerbates income inequality and creates significant barriers to social mobility.

Societal and Economic Ramifications

On a macro level, the cost of living influences migration patterns, economic competitiveness, and social cohesion.

- Migration and Talent Drain: High costs of living in certain areas can drive residents, especially young professionals and families, to seek more affordable regions. While this can redistribute population, it can also lead to talent drain in economically vital cities if companies cannot offer salaries commensurate with the local cost of living.

- Economic Competitiveness: For businesses, a high cost of living (which often correlates with higher labor costs) can impact their competitiveness. They may choose to relocate or avoid establishing operations in expensive areas, affecting local job markets and economic growth.

- Public Policy and Social Programs: Governments constantly grapple with the cost of living when designing social welfare programs, minimum wage policies, housing subsidies, and affordable healthcare initiatives. The goal is often to ensure that a basic standard of living is accessible to all citizens.

- Inflationary Pressures and Economic Stability: Sustained and widespread increases in the cost of living due to inflation can destabilize an economy, erode consumer confidence, and lead to demands for higher wages, potentially creating a wage-price spiral.

- Quality of Life and Social Cohesion: When basic needs become unaffordable for a significant portion of the population, it can lead to social unrest, increased crime rates, and a breakdown in community well-being. Ensuring an affordable cost of living contributes to a higher quality of life for all citizens and fosters greater social cohesion.

In conclusion, “what is the cost of living” is far more than a simple economic query; it is a fundamental question about financial viability, personal happiness, and societal health. Understanding its intricate dynamics, from geographical variations to personal choices, and proactively employing strategies for management and optimization, is essential for navigating the complexities of modern economic life. By demystifying this crucial concept, individuals and policymakers alike can work towards creating a future where maintaining a dignified standard of living is an achievable goal for everyone.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.