The Earned Income Tax Credit (EITC) stands as one of the largest and most impactful federal tax credits designed to benefit low-to-moderate income working individuals and families. Its primary purpose is to supplement wages, encourage employment, and provide a financial boost, often lifting families out of poverty. Understanding the “cap” for the EITC involves recognizing its maximum potential credit amount, the income thresholds at which it phases out completely, and other limiting factors that determine eligibility. This comprehensive guide will dissect these critical aspects, offering clarity on how this vital credit is calculated and applied.

Understanding the Earned Income Tax Credit (EITC)

The EITC is a refundable tax credit, meaning that eligible individuals and families can receive money back even if they do not owe any taxes. This distinguishes it from non-refundable credits, which can only reduce a tax liability to zero. Administered by the Internal Revenue Service (IRS), the EITC aims to offset the burden of Social Security taxes and provide an incentive for individuals to work. Its design incorporates various factors, including a taxpayer’s earned income, adjusted gross income (AGI), filing status, and the number of qualifying children.

The credit is particularly significant because it supports a diverse group of workers, from young adults without children to single parents and married couples raising multiple children. It is a cornerstone of financial assistance for many households across the United States, providing critical funds for housing, food, education, and other essential needs. Crucially, the maximum credit amounts and the income caps for eligibility are adjusted annually for inflation, reflecting changing economic conditions.

EITC Eligibility Requirements

To qualify for the EITC, taxpayers must meet a strict set of criteria established by the IRS. Failing to meet even one of these requirements can result in the disallowance of the credit. These requirements encompass income thresholds, earned income types, and personal circumstances.

Income and Earned Income Limits

The EITC is specifically designed for working individuals, meaning applicants must have “earned income.” This includes wages, salaries, tips, and net earnings from self-employment. Unemployment benefits, child support, and pensions generally do not count as earned income for EITC purposes. The amount of earned income, along with your Adjusted Gross Income (AGI), dictates both eligibility and the potential credit amount. The IRS sets specific AGI and earned income limits that vary based on your filing status and the number of qualifying children. If your income exceeds these thresholds, you will not be eligible for the EITC.

Valid Social Security Number (SSN)

All individuals listed on the tax return—the taxpayer, spouse, and any qualifying children—must have a valid Social Security Number issued by the Social Security Administration before the due date of the tax return (including extensions). An Individual Taxpayer Identification Number (ITIN) does not qualify an individual for the EITC.

Citizenship or Residency Status

You must be a U.S. citizen or a resident alien for the entire tax year. Those who claim the foreign earned income exclusion are generally not eligible for the EITC.

Investment Income Cap

Beyond the earned income and AGI limits, there’s a separate cap on investment income. For a recent tax year, such as 2023, if your investment income (e.g., from interest, dividends, capital gains) exceeds a certain amount (e.g., $11,000 for 2023), you become ineligible for the EITC, regardless of your earned income. This cap ensures the credit remains targeted at individuals primarily relying on their earned wages.

Age and Dependent Status (for those without children)

If you do not have a qualifying child, you must meet additional age criteria. For example, for the 2023 tax year, you must generally be at least 25 but under 65 years old at the end of the tax year. You cannot be claimed as a dependent on someone else’s tax return, and you cannot be a qualifying child of another person.

Qualifying Child Rules

For those claiming the EITC with one or more children, the child must meet specific criteria:

- Relationship Test: The child must be your son, daughter, stepchild, foster child, brother, sister, half-brother, half-sister, stepbrother, stepsister, or a descendant of any of them.

- Age Test: The child must be under age 19 at the end of the tax year, or under age 24 if a full-time student. There is no age limit for a child who is permanently and totally disabled.

- Residency Test: The child must have lived with you in the United States for more than half of the tax year.

- Joint Return Test: The child cannot file a joint tax return for the year, unless it’s solely to claim a refund of withheld income tax or estimated tax paid.

How the EITC Amount is Calculated

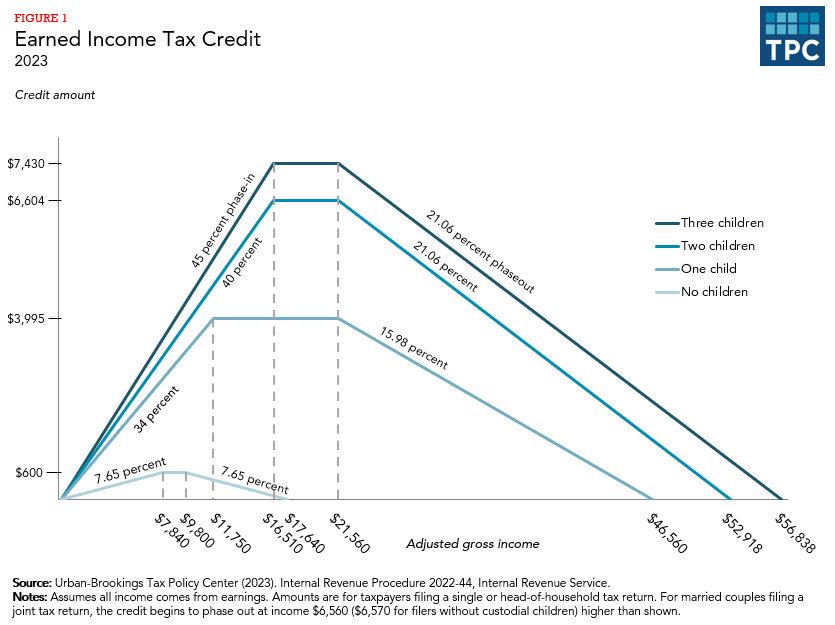

The calculation of the EITC is not a straightforward percentage of income. It involves a progressive formula that considers your income level, filing status, and the number of qualifying children. The credit undergoes distinct phases: a “phase-in,” where the credit amount increases with earned income; a “plateau,” where it reaches its maximum; and a “phase-out,” where it gradually decreases as income continues to rise.

Phase-in and Maximum Credit

As your earned income increases from zero, the EITC also increases proportionally. This “phase-in” period continues until your income reaches a specific threshold, at which point the credit hits its maximum amount. The maximum credit is often the “cap” most taxpayers inquire about. This maximum figure varies significantly based on the number of qualifying children you claim. The more children you have, the higher the potential maximum credit.

The Plateau

Once your earned income reaches the level for the maximum credit, the credit remains at this peak amount for a certain income range. This “plateau” period provides the full benefit of the credit to taxpayers whose incomes fall within this range, before the phase-out begins.

Phase-out

Beyond the plateau, as your earned income and AGI continue to increase, the EITC begins to “phase out.” This means the credit amount gradually decreases until it reaches zero. The rate at which the credit phases out is also determined by your filing status and the number of qualifying children. The income level at which the credit completely disappears represents the ultimate income “cap” for EITC eligibility.

The IRS publishes detailed tables and worksheets, typically found in Publication 596, “Earned Income Credit (EIC),” to help taxpayers calculate their precise credit. Tax software and professional tax preparers utilize these guidelines to accurately determine the EITC amount.

The Maximum EITC Amounts and Phase-Out Thresholds

Understanding the “cap” for Earned Income Credit primarily involves looking at the maximum credit available and the income levels at which the credit is fully phased out. It is crucial to remember that these figures are updated annually by the IRS to account for inflation. The figures provided here are illustrative, based on a recent tax year (e.g., 2023 tax year for returns filed in 2024), and should always be verified with the most current IRS publications or a tax professional for the relevant tax year.

Maximum Credit Amounts (Illustrative for 2023 Tax Year)

- No Qualifying Children: The maximum EITC for taxpayers with no qualifying children was approximately $600.

- One Qualifying Child: For those with one qualifying child, the maximum credit was around $3,995.

- Two Qualifying Children: Taxpayers with two qualifying children could receive a maximum credit of about $6,604.

- Three or More Qualifying Children: The highest credit amount, for taxpayers with three or more qualifying children, was roughly $7,430.

These maximum amounts represent the peak of the credit before the phase-out process begins.

Income Caps and Phase-Out Thresholds (Illustrative for 2023 Tax Year)

The income caps for eligibility depend significantly on both your filing status (Single, Head of Household, or Widowed vs. Married Filing Jointly) and the number of qualifying children. The credit will be completely phased out when your earned income or AGI exceeds these limits.

For Single, Head of Household, or Widowed Filers:

- No Qualifying Children: The EITC begins to phase out at a certain income level (e.g., around $9,000) and is fully phased out when earned income or AGI reaches approximately $17,640.

- One Qualifying Child: The EITC phases out completely when earned income or AGI reaches approximately $46,560.

- Two Qualifying Children: The EITC phases out completely when earned income or AGI reaches approximately $52,930.

- Three or More Qualifying Children: The EITC phases out completely when earned income or AGI reaches approximately $56,838.

For Married Filing Jointly Filers:

- No Qualifying Children: The EITC phases out completely when earned income or AGI reaches approximately $24,210.

- One Qualifying Child: The EITC phases out completely when earned income or AGI reaches approximately $53,120.

- Two Qualifying Children: The EITC phases out completely when earned income or AGI reaches approximately $59,470.

- Three or More Qualifying Children: The EITC phases out completely when earned income or AGI reaches approximately $63,698.

Important Note on Investment Income:

As mentioned, there’s a separate cap for investment income. For the 2023 tax year, if your investment income was more than $11,000, you could not claim the EITC, regardless of your earned income or filing status. This cap serves as another crucial limiting factor for eligibility.

These figures illustrate the various caps associated with the EITC, emphasizing that the “cap” isn’t a single, universal number but rather a dynamic set of limits based on individual circumstances.

Claiming the EITC and Common Pitfalls

Claiming the EITC accurately is crucial to ensure you receive the benefit you are entitled to and avoid potential issues with the IRS. While the credit can be substantial, its complexity often leads to errors.

How to Claim the EITC

To claim the Earned Income Tax Credit, you must file a federal income tax return, even if your income is below the filing threshold and you are not otherwise required to file. You must explicitly request the EITC on your tax form (Form 1040 or 1040-SR). If you have qualifying children, you must also complete and attach Schedule EIC, “Earned Income Credit,” to your return. This schedule provides detailed information about your qualifying children, allowing the IRS to verify their eligibility.

Taxpayers have several options for filing:

- Tax Software: Most reputable tax software programs will guide you through the EITC eligibility questions and calculate the credit automatically.

- IRS Free File: If your income is below a certain threshold (adjusted annually), you can use IRS Free File software through IRS.gov to prepare and file your federal taxes for free.

- Volunteer Income Tax Assistance (VITA) or Tax Counseling for the Elderly (TCE): These programs offer free tax help to qualified individuals, including EITC guidance, from IRS-certified volunteers.

- Professional Tax Preparer: A qualified tax professional can help ensure accuracy, especially for complex situations.

Common Mistakes and Pitfalls

The EITC is one of the most frequently misclaimed credits, often due to misunderstandings of the eligibility rules. Common errors include:

- Incorrectly Claiming a Child: This is the most common error. A child might not meet the age, residency, or relationship tests, or they might be claimed by more than one person (e.g., in divorced or separated families). Strict “tie-breaker rules” exist to determine which parent can claim the child for EITC purposes if both could potentially do so.

- Misreporting Income: Understating or overstating earned income or AGI can lead to incorrect credit amounts or ineligibility.

- Incorrect Filing Status: Using the wrong filing status (e.g., claiming Head of Household when you don’t qualify) can affect EITC eligibility and amount.

- No Valid SSN: As mentioned, everyone listed for the EITC must have a valid SSN by the due date of the return.

- Investment Income Exceeding the Cap: Failing to track and report investment income that pushes you over the annual limit can lead to disallowance.

Consequences of Errors

If the IRS determines you erroneously claimed the EITC, you may be required to repay the credit, along with interest and penalties. Furthermore, if the error was due to reckless or intentional disregard of the rules, you could be barred from claiming the EITC for two years. If fraud is involved, the ban can extend to 10 years. The IRS exercises due diligence requirements for tax preparers to help minimize these errors.

To avoid these pitfalls, always consult the most current IRS Publication 596, “Earned Income Credit (EIC),” or seek assistance from a qualified tax professional or a free tax preparation service like VITA or TCE. Accurate reporting and careful review of eligibility criteria are paramount to successfully claiming this valuable credit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.