The quest to identify “the best IRA” is a common starting point for anyone serious about securing their financial future. However, it’s crucial to understand that the concept of a single “best” Individual Retirement Account (IRA) is a myth. Rather, the optimal IRA for you is the one that aligns most effectively with your unique financial situation, income level, tax bracket, retirement goals, and investment preferences. This article will delve into the various types of IRAs, explore their distinct features, and provide a comprehensive guide to help you determine which IRA truly is “best” for your specific circumstances.

In the complex landscape of personal finance, understanding the nuances of retirement savings vehicles is paramount. IRAs represent a powerful tool in your financial arsenal, offering tax advantages that can significantly accelerate your wealth accumulation over decades. But with options ranging from the traditional and Roth to specialized accounts for the self-employed, making an informed choice is essential. Let’s embark on this journey to demystify IRAs and equip you with the knowledge to make the right decision for your retirement.

Understanding the Core IRA Types

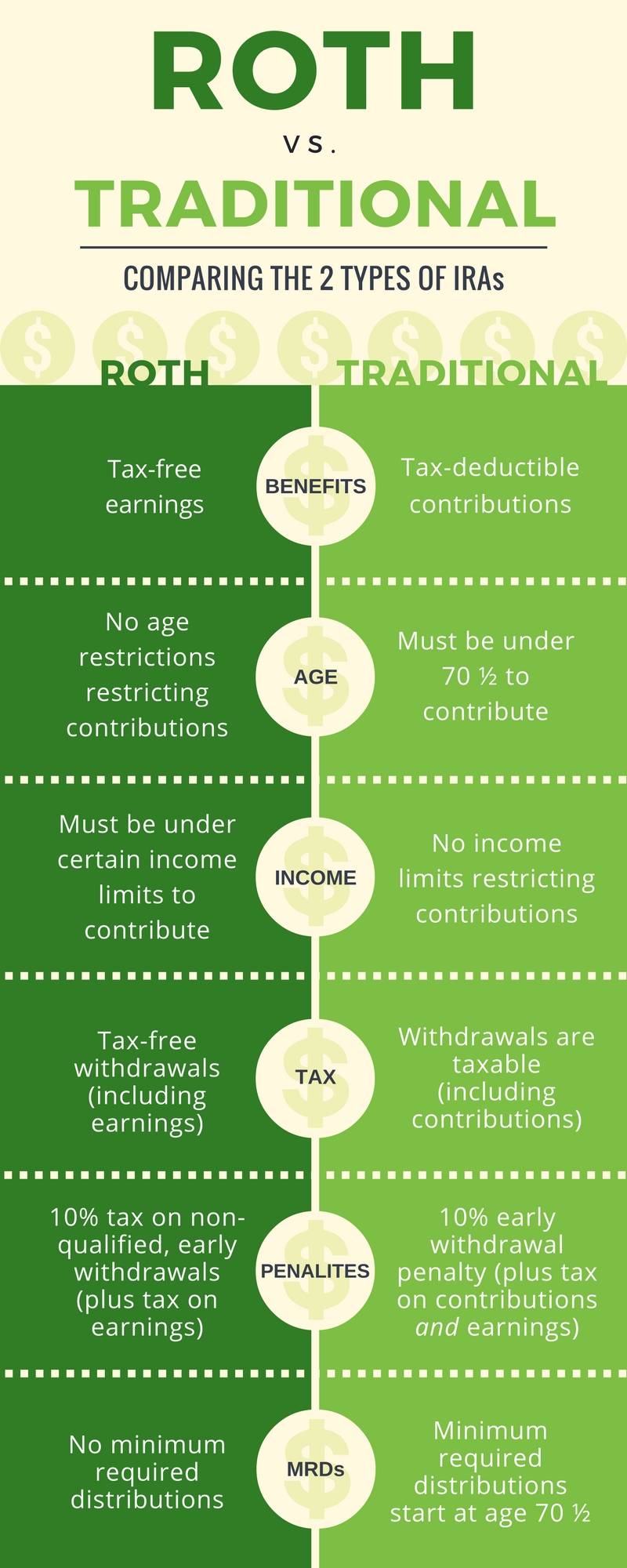

At the heart of the IRA landscape are the two most popular and widely utilized options: the Traditional IRA and the Roth IRA. While both serve the same ultimate goal—to help you save for retirement—they differ fundamentally in their tax treatment, which dictates when you pay taxes on your contributions and earnings.

Traditional IRA

The Traditional IRA is often considered the classic retirement savings vehicle, and it has been a cornerstone of American retirement planning for decades. Its primary appeal lies in its immediate tax benefits for many contributors.

- Tax-Deductible Contributions: For many individuals, contributions to a Traditional IRA are tax-deductible in the year they are made. This means you can reduce your taxable income for the current year, potentially lowering your income tax bill. The ability to deduct contributions is subject to income limitations if you (or your spouse) are also covered by a retirement plan at work (like a 401(k)). If you are not covered by an employer-sponsored plan, your contributions are always deductible, regardless of income.

- Tax-Deferred Growth: Once your money is in a Traditional IRA, it grows tax-deferred. This means you don’t pay taxes on the interest, dividends, or capital gains your investments earn year after year. This allows your money to compound more aggressively, as you’re not losing a portion to taxes annually.

- Taxes Paid Upon Withdrawal in Retirement: The flip side of tax-deferred growth and deductible contributions is that withdrawals in retirement (after age 59½) are generally taxed as ordinary income. The assumption here is that your tax bracket might be lower in retirement than it is during your peak earning years.

- Required Minimum Distributions (RMDs): One important consideration for Traditional IRAs is that you must begin taking Required Minimum Distributions (RMDs) from your account starting at age 73 (as of 2023, per SECURE Act 2.0). These distributions are mandatory and are designed to ensure that the IRS eventually collects taxes on the deferred income.

- Income Limitations for Deductibility: While contributions are broadly tax-deductible, there are income phase-outs that apply if you (or your spouse) also participate in an employer-sponsored retirement plan. If your income exceeds certain thresholds, your deduction may be reduced or eliminated entirely.

Roth IRA

The Roth IRA, introduced in 1997, offers a compelling alternative to the Traditional IRA, primarily appealing to those who anticipate being in a higher tax bracket in retirement or who value tax-free income later in life.

- After-Tax Contributions: The defining characteristic of a Roth IRA is that contributions are made with after-tax dollars. This means you don’t get an upfront tax deduction for your contributions in the year they are made.

- Tax-Free Growth and Qualified Withdrawals: The immense advantage of a Roth IRA is that all qualified withdrawals in retirement are completely tax-free. This includes both your contributions and all the earnings your investments have generated over the years. For withdrawals to be qualified, two conditions must be met: you must be at least 59½ years old, and the Roth IRA must have been open for at least five years (the “five-year rule”).

- Income Limitations for Contributions: Unlike Traditional IRAs, there are specific income limitations that can restrict your ability to contribute directly to a Roth IRA. If your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds, you may not be able to contribute the full amount or any amount at all. However, strategies like the “backdoor Roth” exist for high-income earners to indirectly contribute.

- No RMDs for the Original Owner: A significant advantage for estate planning and flexibility is that the original owner of a Roth IRA is not subject to Required Minimum Distributions (RMDs) during their lifetime. This means your money can continue to grow tax-free indefinitely and be passed on to heirs tax-free (though heirs will have RMDs).

- Flexibility for Early Withdrawals of Contributions: One often-overlooked benefit of a Roth IRA is the ability to withdraw your contributions (not earnings) at any time, for any reason, tax-free and penalty-free. This provides a level of liquidity not found in most other retirement accounts, though it should ideally be avoided to preserve retirement savings.

Beyond Traditional and Roth: Specialized IRAs

While Traditional and Roth IRAs are suitable for most individuals, the IRS also provides specialized IRA options tailored for self-employed individuals and small business owners, offering higher contribution limits and unique benefits.

SEP IRA (Simplified Employee Pension)

A SEP IRA is a retirement plan designed primarily for self-employed individuals and small business owners. It allows employers (including self-employed individuals who are their own employers) to contribute to retirement accounts for themselves and their eligible employees.

- For Self-Employed Individuals and Small Business Owners: This plan is ideal for freelancers, independent contractors, and small businesses with a few employees. It’s relatively simple to set up and administer compared to a 401(k).

- Higher Contribution Limits: One of the most attractive features of a SEP IRA is its significantly higher contribution limits compared to Traditional or Roth IRAs. In 2024, you can contribute up to 25% of your net self-employment earnings (or 25% of an employee’s compensation) up to a maximum of $69,000.

- Employer-Funded: Contributions to a SEP IRA must be made by the employer. For a self-employed individual, this means you contribute as the employer for yourself. Contributions are made to each eligible employee’s SEP IRA account.

- Tax-Deductible Contributions: All contributions made to a SEP IRA are tax-deductible for the business (or the self-employed individual), reducing taxable income. Earnings grow tax-deferred until withdrawal in retirement.

- Flexibility in Contributions: Employers are not required to contribute every year, nor are they required to contribute the same percentage each year. This flexibility can be beneficial for businesses with fluctuating revenues.

SIMPLE IRA (Savings Incentive Match Plan for Employees)

The SIMPLE IRA is another retirement plan option for small businesses, typically those with 100 or fewer employees. It’s designed to be a simpler alternative to a 401(k) plan, requiring both employee contributions and mandatory employer contributions.

- For Small Businesses (100 or Fewer Employees): A SIMPLE IRA is a good fit for very small businesses that want to offer a retirement plan but find 401(k) plans too complex or costly to administer.

- Both Employer and Employee Contributions: Unlike a SEP IRA, employees can contribute to a SIMPLE IRA through payroll deductions. Employers are required to make contributions as well, either a matching contribution (up to 3% of an employee’s pay) or a non-elective contribution (2% of an employee’s pay).

- Lower Contribution Limits than SEP but Higher than Traditional/Roth: Employee contribution limits are higher than for Traditional/Roth IRAs but lower than for SEP IRAs. For 2024, employees can contribute up to $16,000, with an additional catch-up contribution of $3,500 for those aged 50 and over.

- Tax Advantages: Employee contributions are made on a pre-tax basis and grow tax-deferred. Employer contributions are tax-deductible for the business. Withdrawals in retirement are taxed as ordinary income.

- Vesting: Employee contributions are always 100% vested, and employer contributions are immediately 100% vested as well.

Self-Directed IRA

A Self-Directed IRA (SDIRA) isn’t a different type of IRA in terms of tax treatment (it can be a Traditional, Roth, SEP, or SIMPLE IRA). Instead, it’s an IRA held by a custodian that allows for a much broader range of investment options than a typical IRA.

- Allows Investments in Alternative Assets: While most IRAs allow investments in stocks, bonds, mutual funds, and ETFs, an SDIRA allows you to invest in alternative assets such as real estate, private equity, precious metals, limited partnerships, and more.

- Requires a Specialized Custodian: Due to the complexity of holding alternative assets, SDIRAs require specialized custodians who are equipped to handle these unique investments and ensure IRS compliance.

- Higher Complexity and Potential Risks: Investing in alternative assets carries inherently higher risks and requires more due diligence from the investor. It’s crucial to understand the rules regarding “prohibited transactions” to avoid jeopardizing your IRA’s tax-advantaged status. An SDIRA gives you greater control but also greater responsibility.

Key Factors in Choosing Your Best IRA

Determining the “best” IRA for you hinges on a careful evaluation of several personal financial factors. There’s no one-size-fits-all answer, and what works for one person might be suboptimal for another.

Current Income Level and Tax Bracket

Your current income and the corresponding tax bracket are arguably the most significant factors in deciding between a Traditional and a Roth IRA.

- High Current Income, Expect Lower Income in Retirement: If you are currently in a high tax bracket and anticipate being in a lower tax bracket during retirement (e.g., you plan to work less, have fewer income streams, or live on a fixed income), a Traditional IRA might be more advantageous. The tax deduction now saves you money at your higher current rate, and you’ll pay taxes in retirement at a potentially lower rate.

- Lower Current Income, Expect Higher Income in Retirement: Conversely, if you are currently in a lower tax bracket and expect your income, and therefore your tax bracket, to be higher in retirement (e.g., early career professional, significant growth potential), a Roth IRA could be the superior choice. Paying taxes on your contributions now at a lower rate allows for tax-free growth and withdrawals later when you might otherwise be in a higher tax bracket.

- Income Phase-Outs for Roth Contributions and Traditional Deductibility: Be mindful of IRS income limitations. Your ability to contribute directly to a Roth IRA phases out at higher income levels, and your ability to deduct Traditional IRA contributions is limited if you also participate in an employer-sponsored retirement plan and your income exceeds certain thresholds.

Future Tax Expectations

This factor is closely related to your current income and tax bracket but involves an element of prediction regarding the broader tax environment.

- Believe Tax Rates Will Be Higher in Retirement: If you believe that overall income tax rates in the U.S. will be higher in the future (due to government spending, economic factors, etc.), then locking in tax-free withdrawals with a Roth IRA by paying taxes now might be a wise move.

- Believe Tax Rates Will Be Lower in Retirement: If you foresee a future with generally lower tax rates, then deferring taxes with a Traditional IRA could be more beneficial, allowing you to pay taxes on your distributions when rates are lower. This is, of course, speculative, but it’s a valid consideration.

Access to Funds Before Retirement

The liquidity and accessibility of your retirement savings can be a deciding factor, especially if you foresee potential needs for funds before age 59½.

- Roth Contributions Can Be Withdrawn Tax and Penalty-Free: One unique feature of a Roth IRA is that you can withdraw your contributions (the money you put in, not the earnings) at any time, for any reason, completely tax-free and penalty-free. This offers a valuable emergency fund or flexibility, though ideally, retirement savings should remain untouched.

- Traditional Withdrawals Before 59½ Generally Incur Penalties: With a Traditional IRA, withdrawals before age 59½ are typically subject to ordinary income tax and a 10% early withdrawal penalty, with only a few exceptions (e.g., qualified higher education expenses, first-time home purchase up to $10,000, un-reimbursed medical expenses).

Employment Status

Your employment situation heavily influences which types of IRAs are available or most beneficial to you.

- Self-Employed/Small Business Owner: If you are self-employed, a freelancer, or own a small business, a SEP IRA or a SIMPLE IRA (if you have employees) can offer significantly higher contribution limits than a Traditional or Roth IRA. These accounts allow you to save a larger percentage of your income for retirement while enjoying substantial tax deductions.

- Employed with Employer-Sponsored Plan: If you have access to a 401(k), 403(b), or similar plan through your employer, your decision for an IRA might be influenced by whether you’ve maximized your employer plan first, and how your income impacts Traditional IRA deductibility or Roth IRA direct contribution eligibility. Often, it’s beneficial to contribute enough to an employer plan to get the full match, then max out an IRA, and then return to maximizing the employer plan.

Investment Preferences

While an IRA is a container, your choice of container might indirectly affect your investment options, especially for niche strategies.

- Standard Mutual Funds/ETFs/Stocks: For most investors interested in traditional assets like mutual funds, exchange-traded funds (ETFs), stocks, and bonds, any standard Traditional or Roth IRA offered by major brokerages will suffice.

- Alternative Assets (Real Estate, Private Equity): If you’re an experienced investor looking to diversify into non-traditional assets like real estate, private equity, or cryptocurrencies within your retirement account, a Self-Directed IRA will be necessary. This requires a specialized custodian and a deeper understanding of prohibited transactions.

Maximizing Your IRA: Strategies and Best Practices

Choosing the right IRA is only the first step. To truly benefit from this powerful retirement vehicle, you need to employ smart strategies and adhere to best practices for ongoing management.

Start Early and Contribute Consistently

The single most impactful strategy for any retirement account is to start as early as possible and contribute regularly. The magic of compound interest works best over long periods. Even small, consistent contributions made in your 20s can outperform much larger contributions started later in life. Automate your contributions to ensure consistency and eliminate the temptation to skip.

Diversify Your Investments

While the IRA itself is an account, the investments within it are what drive growth. Ensure your portfolio inside your IRA is well-diversified across different asset classes (stocks, bonds, real estate, etc.), industries, and geographies. This helps mitigate risk and enhance returns over the long term. Your asset allocation should align with your risk tolerance and time horizon.

Understand Contribution Limits

The IRS sets annual contribution limits for IRAs. For Traditional and Roth IRAs, the limit is typically the same (e.g., $7,000 in 2024, with an additional $1,000 catch-up contribution for those aged 50 and over). SEP and SIMPLE IRAs have higher limits. Always be aware of these limits and strive to contribute the maximum amount allowable each year, if your finances permit. Over-contributing can lead to penalties.

Consider a “Backdoor Roth” (If Applicable)

For high-income earners whose Modified Adjusted Gross Income (MAGI) exceeds the limits for direct Roth IRA contributions, the “backdoor Roth” strategy can be a legal and effective way to contribute to a Roth IRA. This involves contributing to a non-deductible Traditional IRA and then immediately converting it to a Roth IRA. This strategy requires careful execution, especially if you have existing pre-tax Traditional IRA balances (which can trigger the “pro-rata rule”). Consulting a financial advisor or tax professional is highly recommended for this strategy.

Review and Rebalance Regularly

Your financial situation, goals, and risk tolerance can change over time. It’s crucial to review your IRA and its investments annually. This involves checking if your current IRA type still aligns with your tax situation, if your asset allocation is still appropriate, and if any underperforming investments need adjustment. Rebalancing your portfolio ensures it stays aligned with your target asset allocation.

Common Misconceptions and Important Considerations

As with any financial product, IRAs come with their share of misunderstandings and crucial details that investors often overlook.

IRAs Are Not Investments Themselves

This is a fundamental point often confused. An IRA (Individual Retirement Account) is simply the account or the container that holds your investments. It provides the tax-advantaged status. The actual investments inside the IRA can be stocks, bonds, mutual funds, ETFs, real estate (in an SDIRA), and more. Think of the IRA as a special type of wallet, and your investments as the money or assets within it.

Rollovers from Employer Plans

When you leave a job, you often have the option to roll over your employer-sponsored retirement plan (like a 401(k) or 403(b)) into an IRA. A direct rollover to a Traditional IRA is a common and often advantageous move, preserving the tax-deferred status and potentially offering more investment options and lower fees than your old employer plan. You can also roll over a pre-tax 401(k) to a Roth IRA, but this will trigger a taxable event as the entire converted amount will be treated as ordinary income in the year of conversion.

Spousal IRAs

If you are married and file jointly, and one spouse earns income but the other does not (or earns very little), the working spouse can contribute to an IRA on behalf of the non-working spouse. This is known as a Spousal IRA. It allows a non-earning spouse to save for retirement and take advantage of the same tax benefits as if they had earned income, provided the couple’s combined earned income exceeds the total contributions made to both IRAs.

Prohibited Transactions

With a Self-Directed IRA, especially, it’s vital to understand what constitutes a “prohibited transaction.” The IRS has strict rules to prevent self-dealing or the use of IRA assets for personal benefit outside of the plan’s retirement purpose. Examples include using IRA funds to purchase a personal residence, engaging in certain transactions with “disqualified persons” (like yourself, your spouse, or certain family members), or borrowing money from your IRA. Engaging in prohibited transactions can lead to severe penalties, including the disqualification of your IRA.

Conclusion

The question “What is the best IRA?” has no single answer because “best” is entirely subjective and dependent on individual circumstances. For most people, the choice boils down to a Traditional IRA versus a Roth IRA, dictated primarily by current versus future tax expectations and income levels. Self-employed individuals have the added benefit of considering SEP or SIMPLE IRAs for their higher contribution limits. And for those seeking alternative investments, a Self-Directed IRA opens up a broader universe.

The ultimate goal is to choose an IRA that aligns with your financial strategy, maximize your contributions within that account, diversify your investments wisely, and monitor your progress regularly. Don’t let the array of options paralyze you. The most important step is to start saving and investing for retirement.

When in doubt, or when navigating complex situations like backdoor Roth conversions or Self-Directed IRAs, consulting a qualified financial advisor or tax professional is invaluable. They can provide personalized guidance, ensure you adhere to IRS regulations, and help you craft a retirement savings strategy that is truly “best” for you. Your future self will thank you for making an informed decision today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.