Navigating the complexities of Social Security can be daunting, especially when considering the optimal time to begin receiving benefits. For many, turning 62 marks the earliest opportunity to claim Social Security, often coinciding with a desire for early retirement or a need for financial support. Understanding the average benefit at this age is crucial for effective retirement planning, yet it’s equally important to grasp the numerous factors that influence this figure and how individual circumstances can lead to significant variations.

Understanding Early Retirement and Social Security

The decision to claim Social Security benefits at age 62 is a pivotal financial choice with long-term implications. While it offers immediate income, it also permanently reduces the monthly benefit amount compared to waiting until one’s Full Retirement Age (FRA) or even later.

The Choice to Claim at 62

Age 62 is the earliest point at which most individuals can begin receiving Social Security retirement benefits. This option appeals to various individuals, including those facing job loss, health issues, or simply a strong desire to retire sooner. For some, it’s a bridge to other retirement income sources, while for others, it represents a necessary supplement to cover living expenses. The allure of immediate income can be compelling, yet it comes with a trade-off that demands careful consideration.

Full Retirement Age (FRA) Explained

Full Retirement Age (FRA), also known as “normal retirement age,” is the age at which an individual is entitled to receive 100% of their primary Social Security benefit. This age is determined by the year of your birth. For those born between 1943 and 1954, FRA is 66. For those born in 1960 or later, FRA is 67. For birth years in between, FRA gradually increases by a few months each year. Claiming benefits before your FRA results in a permanent reduction in your monthly payment, while waiting after your FRA (up to age 70) results in increased delayed retirement credits.

The Impact of Early Claiming on Benefits

Choosing to claim Social Security at age 62 leads to a permanent reduction in your monthly benefit amount. This reduction is calculated based on how many months early you claim before your FRA. For example, if your FRA is 67, claiming at 62 means you are claiming 60 months early. The reduction is roughly 5/9 of 1% for each of the first 36 months and 5/12 of 1% for each additional month. In practical terms, claiming at 62 with an FRA of 67 results in a benefit reduction of approximately 30% compared to what you would receive at your FRA. This substantial reduction can have a significant impact on your overall retirement income, making a thorough analysis of its long-term financial implications absolutely essential.

Decoding the Average: Factors Influencing Your Check

While there’s an “average” benefit check at age 62, this figure is a composite influenced by several critical factors. Your individual Social Security benefit is highly personalized, reflecting your unique work history and earnings record.

Lifetime Earnings and Your AIME

The foundation of your Social Security benefit is your lifetime earnings. The Social Security Administration (SSA) calculates your Average Indexed Monthly Earnings (AIME) by taking your 35 highest-earning years, indexing them to account for changes in the average wage level over time, and then averaging them. If you have fewer than 35 years of earnings, zero-earning years will be factored into the average, which can significantly lower your AIME and, consequently, your benefit amount. Consistency in employment and higher earnings throughout your career contribute to a more robust AIME.

The Primary Insurance Amount (PIA) Calculation

Your Primary Insurance Amount (PIA) is the monthly benefit you would receive if you started claiming at your Full Retirement Age. The SSA applies a progressive formula to your AIME using “bend points.” This formula ensures that lower-income workers receive a higher percentage of their average indexed earnings back in benefits compared to higher-income workers. Once your PIA is determined, the early claiming reduction (or delayed retirement credit) is applied to arrive at your actual monthly benefit.

Cost-of-Living Adjustments (COLAs)

Social Security benefits are subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help benefits keep pace with inflation and maintain beneficiaries’ purchasing power. COLAs are typically announced in October and take effect in January of the following year. While COLAs help preserve the value of your benefits over time, they are applied to your reduced benefit if you claim early, meaning the percentage increase is applied to a smaller base amount.

Taxation of Social Security Benefits

It’s important to remember that Social Security benefits may be subject to federal income tax, depending on your combined income. Your “combined income” is your adjusted gross income (AGI) plus non-taxable interest plus one-half of your Social Security benefits. If your combined income exceeds certain thresholds, up to 50% or even 85% of your Social Security benefits could be taxable. This is a critical consideration for financial planning, as it can reduce the net amount you receive from your check. State taxation of benefits also varies, with many states not taxing Social Security, but some do.

What the Numbers Show: Average Benefits at 62

While the exact average fluctuates, general figures provide a useful benchmark. However, it’s crucial to look beyond the headline number to understand its context.

Current Averages for Early Claimers

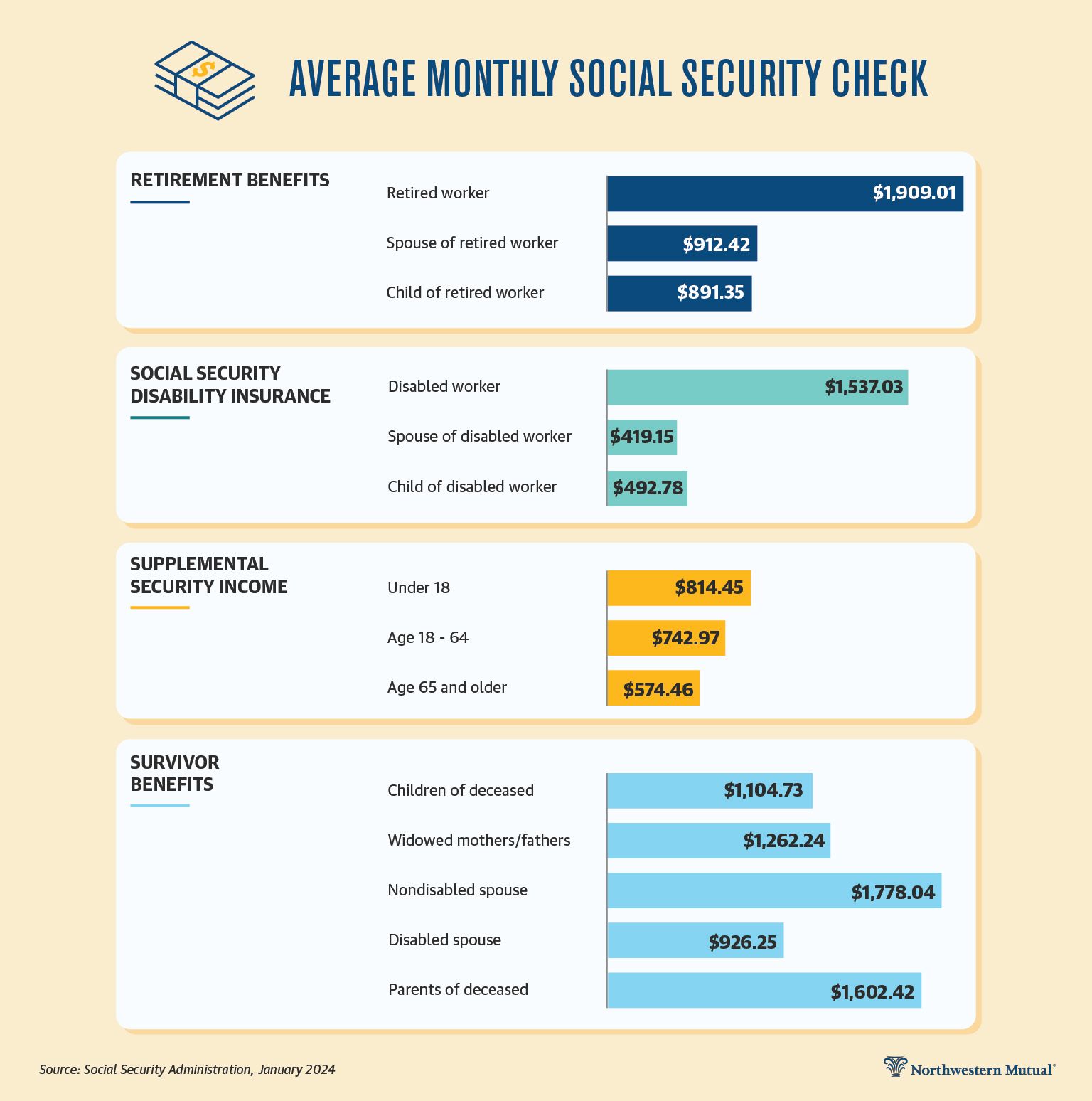

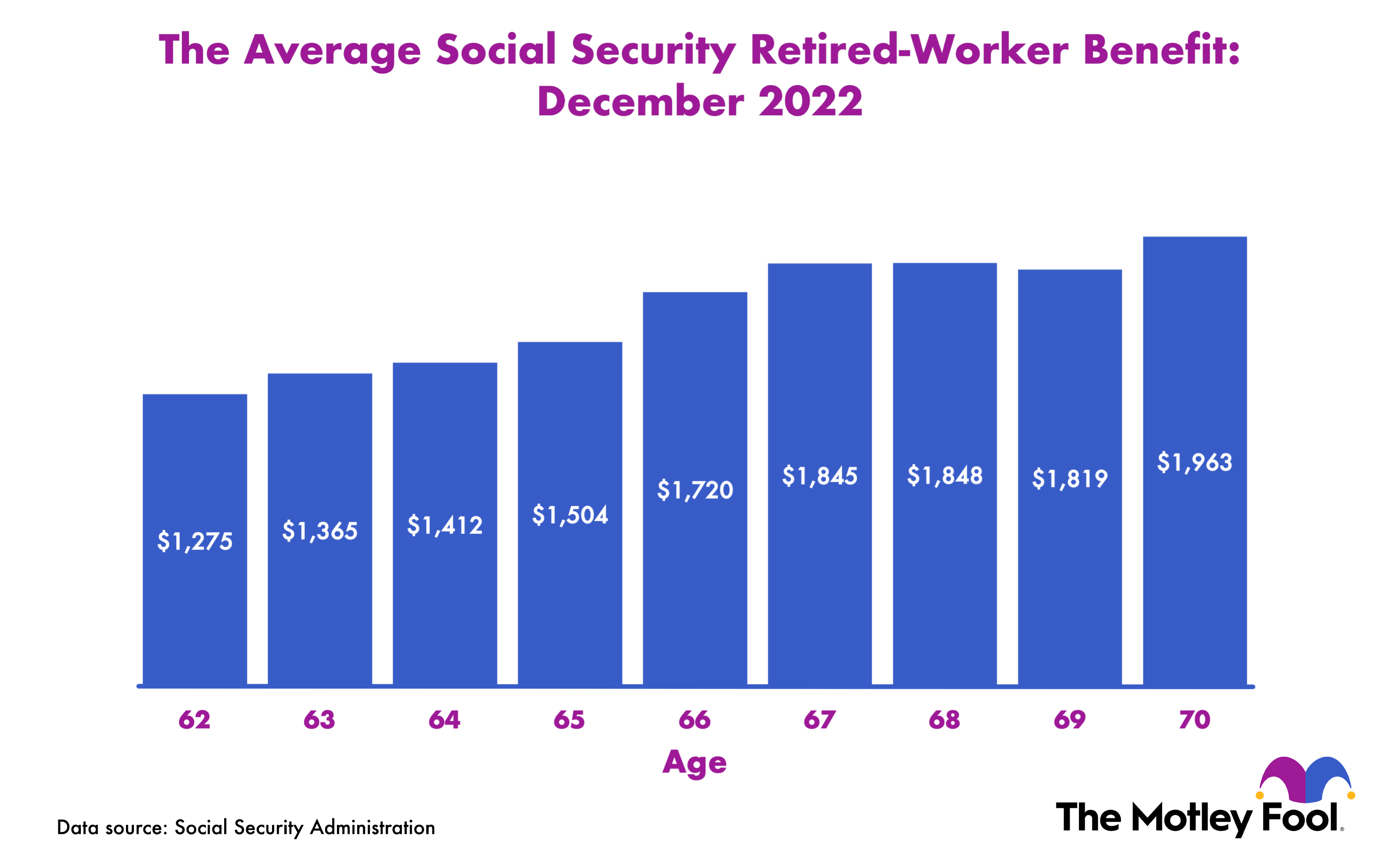

Based on recent data from the Social Security Administration (SSA), the average monthly Social Security benefit for all retired workers is typically around $1,907 as of early 2024. However, the average for those who claim benefits at the earliest possible age, 62, is notably lower. This is due to the permanent reduction applied for early claiming. While exact real-time figures vary and are subject to change, retirees claiming at 62 typically receive a benefit that is roughly 25-30% less than the overall average for all retired workers, assuming their earnings records are similar. This could place the average monthly benefit for a 62-year-old in the range of $1,300 to $1,400, though individual experiences will differ based on their specific earnings history and PIA. It’s a significant reduction compared to what one would receive at FRA.

How Averages Compare to Full Retirement Age Benefits

The contrast between claiming at 62 and waiting until your Full Retirement Age (FRA) is stark. If an individual’s PIA (their benefit at FRA) was, for example, $2,000 per month, claiming at age 62 with an FRA of 67 would reduce that benefit to approximately $1,400 (a 30% reduction). Waiting until FRA would allow them to receive the full $2,000. This $600 difference per month accumulates significantly over a lifetime, emphasizing the financial incentive to defer claiming if feasible.

Gender and Socioeconomic Disparities

It’s also important to acknowledge that averages can mask significant disparities. Women, on average, tend to receive lower Social Security benefits than men. This is often attributed to factors such as lower lifetime earnings, career breaks for childcare or elder care, and working in jobs with lower pay. Similarly, socioeconomic status plays a role, with individuals from lower-income backgrounds often having lower lifetime earnings, which translates into lower Social Security benefits regardless of when they claim. These disparities highlight the importance of personalized financial planning and the potential need for supplemental income sources.

Strategic Considerations for Claiming at 62

Deciding when to claim Social Security is a highly personal financial strategy that should align with your broader retirement plan. Claiming at 62 is not inherently good or bad; it depends entirely on your individual circumstances.

Financial Need vs. Maximizing Lifetime Benefits

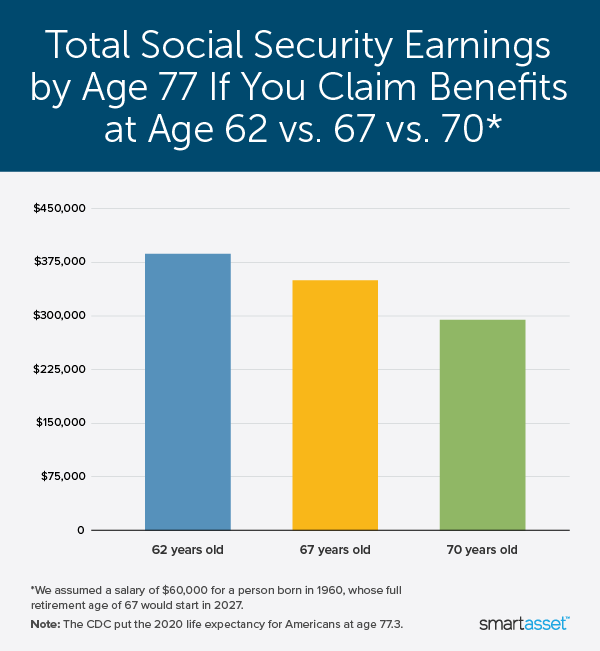

The primary conflict in the claiming decision often lies between immediate financial need and the goal of maximizing total lifetime benefits. If you genuinely need the income at 62 to cover essential living expenses, or if you face health challenges that suggest a shorter life expectancy, claiming early might be the most practical and beneficial choice. However, if you have other sources of income, robust savings, or a family history of longevity, delaying benefits to receive a higher monthly payment for a longer period could result in a greater cumulative payout over your lifetime. A careful assessment of your personal financial runway and health outlook is paramount.

Spousal and Survivor Benefits

Social Security offers spousal and survivor benefits that can significantly influence claiming strategies. A spouse may be eligible to receive up to 50% of the higher-earning spouse’s PIA, while a surviving spouse may receive up to 100% of the deceased spouse’s benefit. The timing of claiming can impact these auxiliary benefits. For instance, if you claim early, it might reduce the amount your spouse could receive as a spousal benefit later. If you are the higher earner, delaying your claim could provide a larger survivor benefit for your spouse should you pass away first. Understanding these interconnected benefits is crucial for couples planning their retirement income.

Working While Receiving Benefits (Earnings Test)

If you claim Social Security benefits before your Full Retirement Age (FRA) and continue to work, your benefits may be reduced if your earnings exceed certain limits. This is known as the Social Security earnings test. For example, in 2024, if you are under FRA for the entire year, the SSA deducts $1 from your benefits for every $2 you earn above an annual limit (e.g., $22,320 in 2024). In the year you reach FRA, a higher limit applies, and the deduction is $1 for every $3 earned above that limit (e.g., $59,520 in 2024) until the month you reach FRA. Once you reach FRA, the earnings test no longer applies, and you can earn any amount without your benefits being reduced. This rule is a critical factor for those considering working part-time in early retirement.

Beyond Social Security: Supplementing Your Income

Regardless of when you claim Social Security, it’s often intended to be a foundational layer of retirement income, not the sole source. Personal savings, 401(k)s, IRAs, pensions, and other investments are vital for a comfortable retirement. For those claiming at 62, given the reduced benefit, supplementing this income becomes even more critical. This could involve drawing down savings, working part-time, or generating income from investments. A holistic financial plan that integrates Social Security with all other income sources is essential for long-term financial security.

Tools and Resources for Financial Planning

Making an informed decision about Social Security requires reliable information and, often, professional guidance.

Social Security Administration (SSA) Online Tools

The Social Security Administration provides a wealth of resources, including online calculators and personalized statements. Creating an account on my Social Security allows you to view your earnings history, get estimates of your future benefits at different claiming ages, and review your Social Security statement. These tools are invaluable for understanding your potential benefits and modeling various claiming scenarios.

Consulting a Financial Advisor

A qualified financial advisor specializing in retirement planning can provide personalized guidance. They can help you analyze your specific financial situation, project your future needs, and determine the optimal Social Security claiming strategy that integrates with your overall retirement portfolio, tax planning, and estate goals. Their expertise can be particularly beneficial for navigating complex situations, such as spousal benefits or the earnings test.

Retirement Planning Software

Various retirement planning software and online calculators are available that allow you to input your financial data, model different income streams, and visualize the impact of claiming Social Security at different ages. These tools can help you understand the long-term implications of your choices and make more confident decisions about your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.