The S&P 500 index stands as a cornerstone of modern investing, representing 500 of the largest publicly traded companies in the United States. For many, it’s synonymous with “the market” and often serves as a benchmark for portfolio performance. The question of “how much to invest in the S&P 500” is a fundamental one for both novice and seasoned investors, yet it lacks a universal answer. Instead, the optimal allocation is deeply personal, rooted in an individual’s financial situation, goals, risk tolerance, and investment horizon. This article will dissect the layers of this critical decision, providing a comprehensive framework to help you determine your ideal investment strategy for the S&P 500.

Understanding the S&P 500 as an Investment Vehicle

Before deciding on an investment amount, it’s crucial to grasp what the S&P 500 truly represents and why it has become such a popular choice for wealth building.

What is the S&P 500?

The S&P 500 is a market-capitalization-weighted index of 500 of the largest U.S. publicly traded companies selected by Standard & Poor’s based on criteria like market size, liquidity, and sector representation. It’s a broad measure of U.S. stock market performance, encompassing diverse sectors from technology and finance to healthcare and consumer goods. When you invest in an S&P 500 fund, you’re not buying 500 individual stocks; rather, you’re buying a share of a fund that holds all these stocks in proportion to the index, giving you immediate diversification across a significant portion of the U.S. economy.

Why Invest in the S&P 500?

The appeal of the S&P 500 is multifaceted. Historically, it has delivered robust long-term returns, averaging around 10-12% annually before inflation over several decades. This track record of growth makes it an attractive option for compounding wealth. Furthermore, investing in the S&P 500 offers inherent diversification. Instead of betting on a single company, you’re spreading your investment across 500 giants, significantly reducing company-specific risk. Should one company falter, its impact on your overall portfolio is mitigated by the performance of the other 499. It also offers simplicity and low cost, as index funds and ETFs tracking the S&P 500 typically have very low expense ratios compared to actively managed funds.

Common Ways to Invest

Accessing the S&P 500 is straightforward. The most common methods include:

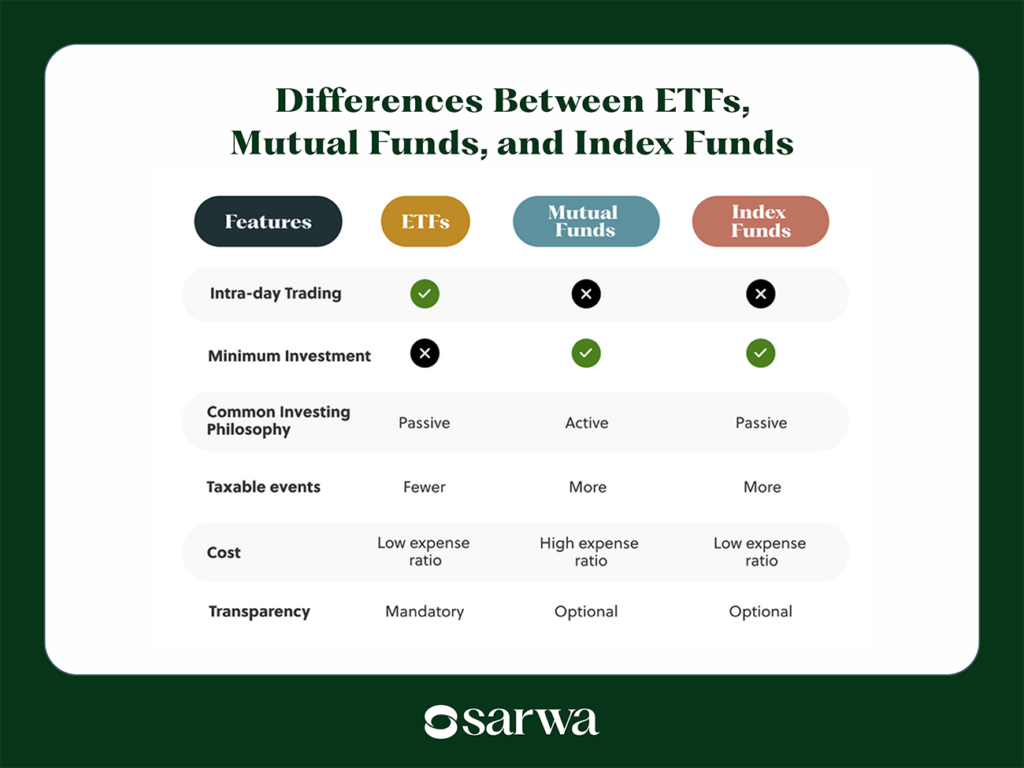

- Exchange-Traded Funds (ETFs): These are baskets of securities that trade like individual stocks on an exchange. Popular S&P 500 ETFs include SPY, IVV, and VOO, known for their low fees and high liquidity.

- Index Mutual Funds: Similar to ETFs, these funds track the S&P 500 but are typically bought and sold through a fund company directly, often at the end-of-day net asset value. Vanguard 500 Index Fund (VFIAX) is a well-known example.

- Robo-advisors: These automated investment platforms often incorporate S&P 500 tracking funds into their diversified portfolios, especially for investors seeking a hands-off approach.

Assessing Your Personal Financial Landscape

Before allocating funds to the S&P 500, a critical self-assessment of your personal financial situation is imperative. This foundational work ensures your investment strategy is built on solid ground.

Establishing an Emergency Fund

The absolute first step before any significant investment is to build a robust emergency fund. This liquid cash reserve, typically 3 to 6 months’ worth of essential living expenses, is crucial for covering unexpected costs like job loss, medical emergencies, or home repairs without having to sell investments prematurely at an inopportune time. Investing without an emergency fund can expose you to unnecessary risk, forcing you to liquidate assets when the market is down.

Eliminating High-Interest Debt

High-interest debt, such as credit card balances or certain personal loans, acts as a significant drag on your financial progress. The interest rates on such debts often far exceed the average returns of the S&P 500. Therefore, prioritizing the repayment of these debts is often a more financially sound decision than investing. Think of paying down a 20% interest credit card as an immediate, guaranteed 20% return on your money – a return you’d be hard-pressed to consistently achieve in the stock market.

Defining Your Financial Goals

Your investment goals dictate your strategy. Are you saving for retirement 30 years from now, a down payment on a house in five years, or a child’s education in ten?

- Long-Term Goals (10+ years): The S&P 500, with its historical growth and ability to recover from market downturns over time, is an excellent vehicle for long-term objectives like retirement.

- Mid-Term Goals (5-10 years): While still potentially suitable, the shorter horizon means you might want a more diversified portfolio with a slightly lower stock allocation to mitigate market volatility closer to your goal date.

- Short-Term Goals (under 5 years): For these, the S&P 500 is generally too risky. Cash or high-yield savings accounts are more appropriate, as a sudden market downturn could jeopardize your ability to meet your goal.

Understanding Your Risk Tolerance

Risk tolerance is your psychological comfort level with investment volatility. Do market dips make you panic and want to sell, or do you view them as buying opportunities?

- Aggressive Investors: Those comfortable with significant fluctuations and potential short-term losses for the prospect of higher long-term gains might have a higher S&P 500 allocation.

- Moderate Investors: Seek a balance between growth and stability, often blending S&P 500 exposure with other asset classes like bonds.

- Conservative Investors: Prioritize capital preservation and are averse to volatility. They might have a minimal S&P 500 allocation, favoring more stable assets.

Your risk tolerance should align with your investment horizon. A young investor with decades until retirement can afford to be more aggressive, while someone nearing retirement might opt for a more conservative approach.

Crafting Your S&P 500 Allocation Strategy

Once your financial foundation is solid, the next step is to determine the appropriate percentage of your investment portfolio to dedicate to the S&P 500. This is where personalized strategies come into play.

The “Core-Satellite” Approach

Many financial advisors advocate for a “core-satellite” strategy. In this model, the S&P 500 (or a broader U.S. total market index fund) forms the “core” of your portfolio – the largest and most stable portion. This core provides consistent, diversified exposure to the U.S. economy. The “satellites” are smaller allocations to other asset classes or niche investments, such as international stocks, emerging markets, small-cap stocks, real estate, or bonds. These satellites aim to enhance returns or provide additional diversification, but the S&P 500 remains the stable foundation. For many, the S&P 500 could represent anywhere from 40% to 80% of their equity allocation, depending on other holdings.

Age-Based Allocation Rules

Several rules of thumb offer a starting point for equity allocation, often adjusting based on age:

- Rule of 110/120 Minus Age: A common guideline suggests that you subtract your age from 110 or 120 to determine the percentage of your portfolio that should be in stocks (including S&P 500). For example, a 30-year-old might have 80-90% in stocks, while a 60-year-old might have 50-60%. The remainder would be in bonds or other less volatile assets.

- 60/40 Portfolio: A classic strategy, especially for moderate investors, is to allocate 60% to stocks (with a significant portion in the S&P 500) and 40% to bonds. This offers a balance of growth and stability.

These rules are merely starting points; individual circumstances (like a secure pension or significant inheritance) might warrant deviations.

The Dollar-Cost Averaging Advantage

Regardless of the percentage you decide, how you invest can be as important as how much. Dollar-cost averaging (DCA) is a powerful strategy, especially for long-term investors. Instead of investing a large lump sum all at once, DCA involves investing a fixed amount of money at regular intervals (e.g., $200 every month). This strategy mitigates the risk of market timing. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more. Over time, this averages out your purchase price and can lead to better returns than trying to predict market tops and bottoms.

Considering Other Investments

While the S&P 500 is excellent, it shouldn’t necessarily be your only investment. A truly diversified portfolio typically includes:

- International Stocks: To gain exposure to global growth and reduce reliance on a single economy.

- Bonds: Provide stability, income, and a hedge against stock market volatility, especially as you approach retirement.

- Real Estate: Either directly or through Real Estate Investment Trusts (REITs), can offer diversification and income.

- Small-Cap and Mid-Cap Stocks: These smaller companies can offer higher growth potential, though with increased volatility.

The amount you allocate to the S&P 500 will depend on how much space you leave for these other asset classes to build a truly robust and diversified portfolio.

Practical Steps and Ongoing Management

Once you’ve decided on your strategy, putting it into action and maintaining it over time are crucial for success.

Choosing the Right Investment Account

The type of account you use can significantly impact your returns due to tax implications:

- Tax-Advantaged Accounts (IRA, 401k, 403b, Roth IRA): These offer tax benefits (tax-deductible contributions, tax-deferred growth, or tax-free withdrawals in retirement) and are often the best place to invest for long-term goals like retirement.

- Taxable Brokerage Accounts: For investments beyond retirement limits or for shorter-term goals, a standard brokerage account is suitable, though subject to capital gains and dividend taxes.

Selecting Your S&P 500 Fund

Focus on low-cost S&P 500 index ETFs or mutual funds. Look for funds with:

- Low Expense Ratios: This is the annual fee you pay, expressed as a percentage of your investment. Even a small difference (e.g., 0.03% vs. 0.50%) can amount to tens of thousands of dollars over decades.

- High Liquidity (for ETFs): Ensures you can easily buy and sell shares.

- Good Tracking Error: The fund should closely replicate the performance of the S&P 500 index.

Automating Your Investments

Consistency is the secret sauce of successful long-term investing. Set up automatic transfers from your bank account to your investment account on a regular schedule (e.g., bi-weekly or monthly). This ensures you stick to your dollar-cost averaging strategy, removes emotion from the investment process, and builds wealth systematically.

Regular Portfolio Review and Rebalancing

Your ideal allocation isn’t static. Over time, market movements will cause your portfolio’s percentages to drift. A growth spurt in the S&P 500 might mean your stock allocation becomes higher than intended.

- Review: Annually, or when significant life changes occur, review your portfolio to ensure it still aligns with your goals and risk tolerance.

- Rebalance: If your S&P 500 allocation has grown significantly above your target, you might sell some shares to bring it back in line and reallocate to underperforming assets (e.g., bonds). Conversely, if it has shrunk, you might buy more. This disciplined approach helps maintain your desired risk profile and can even force you to “buy low and sell high” by trimming winning assets and adding to lagging ones.

Common Pitfalls and Key Considerations

While the S&P 500 offers a compelling investment opportunity, awareness of potential pitfalls and additional considerations is vital.

Avoiding Emotional Investing

The stock market is cyclical, experiencing both booms and busts. Emotional responses to market fluctuations – panicking during downturns and selling, or getting overly confident during bull markets and taking excessive risks – are detrimental to long-term returns. The S&P 500, when viewed through a long-term lens, has consistently trended upwards. Patience and discipline are paramount. Stick to your predetermined plan, especially during turbulent times.

The Impact of Fees and Taxes

Even seemingly small fees can compound into significant amounts over decades, eroding your returns. Always opt for low-cost index funds or ETFs. Similarly, understanding the tax implications of your investment account and withdrawals is crucial. Capital gains taxes (short-term vs. long-term) and dividend taxes can impact your net returns. Utilizing tax-advantaged accounts whenever possible can significantly enhance your after-tax wealth accumulation.

The Importance of Diversification Beyond the S&P 500

While the S&P 500 itself offers excellent diversification across 500 U.S. companies, it does not provide exposure to international markets or other asset classes like bonds, real estate, or commodities. A fully diversified portfolio typically includes:

- International Equities: To capture growth opportunities outside the U.S. and provide a hedge against potential U.S. economic downturns.

- Fixed Income (Bonds): To reduce overall portfolio volatility, generate income, and potentially preserve capital during equity market corrections.

- Alternative Investments: For some investors, a small allocation to alternatives like real estate or commodities can further enhance diversification.

The S&P 500 should be considered a powerful component of a broader, well-thought-out investment strategy, not the entirety of it for most investors.

In conclusion, there’s no single magic number for “how much to invest in the S&P 500.” The answer is deeply personal, flowing from a comprehensive assessment of your individual financial circumstances, goals, time horizon, and risk tolerance. For many, the S&P 500 will form the substantial core of their equity investments, providing diversified exposure to the robust U.S. economy. By establishing a solid financial foundation, setting clear goals, adopting a disciplined, long-term approach with dollar-cost averaging, and regularly reviewing your portfolio, you can effectively leverage the power of the S&P 500 to build significant wealth over time. Remember, the journey of investing is a marathon, not a sprint, and consistency is your most valuable asset.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.