Understanding the average cost of living in America is a foundational step in personal financial planning, budgeting, and making informed life decisions. While a national average provides a useful benchmark, it’s crucial to recognize the immense variation across states, cities, and even neighborhoods. This article delves into the components that constitute the cost of living, examines the geographical disparities, and offers strategies for effectively managing these expenses within the broader economic landscape.

Deconstructing the Average: Key Components of Living Expenses

The “cost of living” encompasses all expenditures required to maintain a certain standard of living. It typically includes housing, transportation, food, healthcare, utilities, and a range of miscellaneous goods and services. Each category contributes significantly to a household’s financial outlay, and their proportional impact can shift based on location and individual circumstances.

Housing: The Dominant Factor

For most American households, housing represents the largest single expense. This includes rent or mortgage payments, property taxes, homeowner’s insurance, and maintenance costs. The median rent for an apartment can fluctuate wildly, from under $1,000 in less populated areas to several thousand dollars in major metropolitan centers like New York City, San Francisco, or Boston. Homeownership, while offering long-term equity building, often comes with substantial upfront costs (down payments, closing costs) and ongoing responsibilities that factor heavily into a monthly budget. A common financial guideline suggests allocating no more than 30% of gross income to housing, though this can be challenging to meet in high-cost areas. The choice between renting and buying, and the type of dwelling, profoundly impacts an individual’s financial flexibility and savings potential.

Transportation Costs

Commuting, errands, and travel all contribute to transportation expenses. This category typically includes vehicle payments, fuel, insurance, maintenance, public transportation fares, and ride-sharing services. For many, car ownership is a necessity, especially in areas with limited public transit. The average American household spends a significant portion of their income on transportation, often second only to housing. Factors like vehicle efficiency, daily commute distance, and reliance on personal vehicles versus public transit directly influence these costs. Living in a walkable city with robust public transport can drastically reduce personal vehicle reliance, freeing up substantial funds that would otherwise be allocated to car-related expenses. Conversely, rural living often necessitates multiple vehicles, increasing this financial burden.

Food and Groceries

Feeding a household is a non-negotiable expense. This category includes groceries purchased for home consumption and meals eaten out at restaurants. The cost of food can vary based on dietary preferences, family size, and whether individuals prioritize cooking at home versus dining out. While grocery prices have seen inflationary pressures nationwide, local availability and the presence of discount retailers can influence weekly spending. Strategic meal planning, buying in bulk when appropriate, and reducing restaurant visits are common strategies to control food budgets. Beyond mere sustenance, food spending also reflects lifestyle choices, from organic preferences to convenience meals, each carrying a different price tag.

Healthcare Expenditures

Healthcare costs are a significant and often unpredictable component of the cost of living. These expenses include health insurance premiums, deductibles, co-pays, prescription medications, and out-of-pocket costs for doctor visits, specialists, and emergencies. Even with employer-sponsored insurance, individuals can face substantial monthly premiums and high deductibles before coverage kicks in. For those without employer benefits, purchasing insurance through the Affordable Care Act (ACA) marketplace or private plans can be a major financial commitment. The rising cost of medical care and pharmaceuticals continues to be a top concern for many American families, impacting financial stability and retirement planning. Proactive health management and understanding insurance plans are crucial for mitigating these costs.

Utilities and Miscellaneous

Beyond the major categories, a host of other expenses contribute to the cost of living. Utilities include electricity, gas, water, internet, and sometimes trash collection. These costs vary based on climate, home size, and usage habits. Miscellaneous expenses cover a broad spectrum: personal care items, clothing, entertainment, education, childcare, pet care, subscriptions, and personal debt payments. While individually smaller, these discretionary and semi-discretionary expenses can accumulate rapidly. Effective budgeting requires allocating funds for these diverse categories and distinguishing between essential needs and wants to maintain financial control.

Geographic Variance: Why Averages Can Be Misleading

The concept of an “average” cost of living across the entire United States can be highly misleading due to staggering regional disparities. Averages obscure the fact that financial realities differ dramatically from one state or city to another.

High-Cost Metropolitan Areas

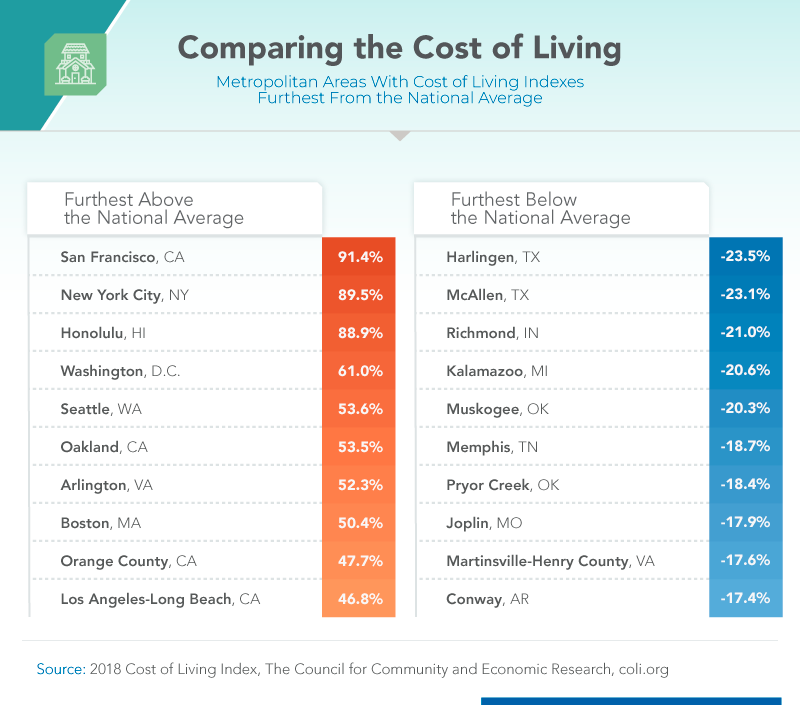

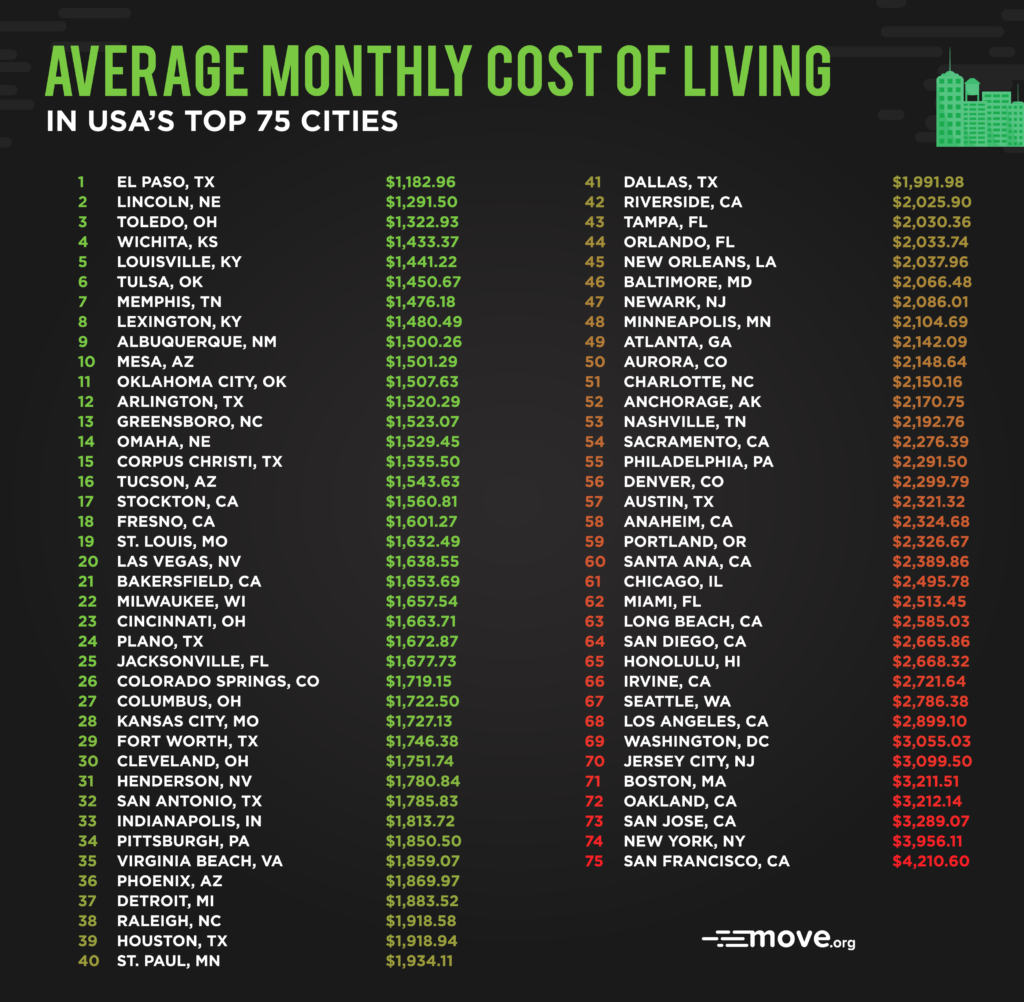

Major metropolitan areas and coastal cities consistently rank among the most expensive places to live. Cities like New York, San Francisco, Los Angeles, Washington D.C., Boston, and Seattle exhibit housing costs that are often two to three times the national average. This inflated housing market subsequently drives up the cost of nearly everything else, from groceries to services, as businesses face higher operational costs. While these areas often offer higher wages and more job opportunities, the elevated cost of living can negate the benefits of a larger paycheck, leading to a phenomenon where even high earners struggle to save or achieve financial milestones like homeownership. The competitive nature of these markets often forces residents into smaller living spaces or longer commutes.

Affordable Regions and States

Conversely, many states in the Midwest, South, and certain parts of the Mountain West offer a significantly lower cost of living. States like Arkansas, Mississippi, Oklahoma, and parts of the Midwest feature more affordable housing, lower property taxes, and generally lower costs for goods and services. While wages might be comparatively lower in these regions, the purchasing power of each dollar stretches further. This allows residents to achieve a higher quality of life, save more, or afford larger homes than their counterparts in high-cost areas. The increasing flexibility of remote work has enabled some individuals to leverage these geographical arbitrage opportunities, earning a high-cost-of-living salary while enjoying a low-cost-of-living lifestyle.

Urban vs. Rural Differences

Beyond state-level comparisons, the distinction between urban, suburban, and rural living is critical. Rural areas typically boast the lowest housing costs and often lower prices for certain goods due to fewer taxes or lower demand. However, rural living can come with its own set of financial challenges, such as higher transportation costs due to longer distances and limited public transit, and potentially higher costs for specialized services or certain utilities. Suburban areas often strike a balance, offering more affordable housing than central cities while maintaining access to amenities and employment opportunities, albeit often at the cost of a longer commute. Understanding these nuances is vital for accurate financial planning based on one’s specific location.

Factors Influencing Your Personal Cost of Living

While national and regional averages provide context, an individual’s personal cost of living is ultimately shaped by their unique choices and circumstances.

Income and Lifestyle Choices

Your income level directly dictates your financial capacity, but lifestyle choices determine how that income is spent. A high income can still result in financial strain if matched by an equally high-spending lifestyle characterized by frequent dining out, luxury purchases, expensive hobbies, and extensive travel. Conversely, a modest income, coupled with frugal habits and mindful spending, can lead to financial stability and even significant savings. Lifestyle choices impact discretionary spending in areas like entertainment, clothing, and vacations, which, while not strictly essential, contribute significantly to overall expenditure. The decision to prioritize savings, debt repayment, or specific experiences profoundly influences one’s effective cost of living.

Family Size and Dependents

The number of individuals in a household dramatically impacts the cost of living. Raising children introduces substantial expenses related to food, clothing, education, healthcare, childcare, and extracurricular activities. The cost of childcare alone can be equivalent to a second mortgage in many parts of the country. Supporting elderly parents or other dependents also adds to the financial burden. Single individuals or couples without dependents generally have lower per-person costs and greater financial flexibility. Family planning, therefore, is not just a personal decision but a significant financial one, requiring careful consideration of present and future expenses.

Debt Obligations

Outstanding debts, particularly high-interest consumer debt like credit card balances or personal loans, can significantly inflate an individual’s effective cost of living. Monthly debt payments divert funds that could otherwise be allocated to savings, investments, or discretionary spending. Student loan debt, car loans, and medical debt also contribute to the overall financial outflow. Managing and strategically reducing debt is a critical component of lowering one’s effective cost of living and improving long-term financial health. The interest accumulated on debts represents money spent that provides no current or future asset, effectively making living more expensive.

Strategies for Managing and Reducing Living Costs

Effectively managing and, where possible, reducing the cost of living is central to achieving financial stability and reaching personal finance goals.

Budgeting and Financial Planning

The cornerstone of managing living costs is a robust budget. A budget provides a clear picture of income versus expenses, identifying where money is going and highlighting areas for potential savings. Tools ranging from simple spreadsheets to sophisticated financial apps can help track spending, categorize expenses, and set limits. Regular review and adjustment of the budget are essential as income or expenses change. Financial planning extends beyond monthly budgeting to include long-term goals like saving for a down payment, retirement, or a child’s education, ensuring that current spending aligns with future aspirations.

Smart Housing Choices

Given that housing is often the largest expense, making smart choices in this category offers the greatest potential for savings. This could involve choosing to live in a slightly less expensive neighborhood, opting for a smaller living space, exploring roommate situations, or carefully weighing the financial implications of renting versus buying. For homeowners, refinancing a mortgage, challenging property tax assessments, or making energy-efficient home improvements can yield long-term savings. Geographic flexibility, if possible through remote work, can allow individuals to move to lower-cost regions without sacrificing income.

Optimizing Transportation

Reducing transportation costs can involve a variety of strategies. If public transport is available, utilizing it can be significantly cheaper than car ownership. Carpooling, cycling, or walking for shorter distances also cut down on fuel and maintenance. For those who own vehicles, choosing fuel-efficient models, regularly maintaining the car to prevent costly repairs, and shopping around for competitive auto insurance rates can make a difference. Reassessing the necessity of a second car for multi-vehicle households can also unlock substantial savings.

Frugal Food Practices

Controlling food costs often comes down to conscious consumption. Meal planning, preparing meals at home, buying groceries in bulk when discounts are available, and minimizing food waste are effective strategies. Shopping at discount supermarkets, utilizing coupons, and focusing on seasonal produce can also reduce grocery bills. Limiting restaurant meals, takeout, and expensive coffee habits can free up a surprising amount of money over time. Learning to cook and exploring affordable recipes can transform this significant expense into an area of considerable savings.

Leveraging Financial Tools and Resources

A variety of financial tools and resources can aid in managing living costs. High-yield savings accounts can maximize returns on emergency funds. Budgeting apps provide insights into spending patterns. Comparison websites help find better deals on insurance, utilities, and internet services. Financial advisors can offer personalized guidance on optimizing budgets, investments, and debt management. Additionally, understanding and utilizing employer benefits, such as health savings accounts (HSAs) or flexible spending accounts (FSAs), can lead to tax advantages and reduced out-of-pocket healthcare costs.

The Broader Economic Context

The average cost of living is not static; it is influenced by larger economic forces that impact individual financial realities.

Inflation and Economic Trends

Inflation, the general increase in prices and fall in the purchasing value of money, directly impacts the cost of living. When inflation rates are high, the same dollar buys less, making everything from groceries to gasoline more expensive. Economic trends such as interest rate changes, supply chain disruptions, and global events can all ripple through the economy, affecting consumer prices and household budgets. Understanding these broader trends is crucial for anticipating changes in personal finance and adjusting spending habits accordingly.

The Impact on Financial Well-being

The rising cost of living has profound implications for the financial well-being of Americans. It can make saving for retirement, a down payment, or a child’s education more challenging. It can contribute to increased household debt and reduce financial flexibility in the face of unexpected expenses. For many, a stagnant wage growth combined with rising costs creates a squeeze on disposable income. Therefore, a comprehensive understanding of the cost of living is not just an academic exercise but a practical necessity for maintaining and improving personal financial health in a dynamic economic environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.