In the dynamic world of personal finance and investment, few concepts hold as much transformative power as compound interest. Often lauded as the “eighth wonder of the world,” compound interest is a fundamental principle that underpins wealth creation, offering a profound mechanism for growing capital over time. Understanding its mechanics, implications, and strategic application is not merely an academic exercise; it is an essential pillar for anyone aspiring to build financial security, save for retirement, or achieve significant investment goals. This article delves into the core of compound interest, demystifying its operations, illustrating its profound impact, and offering actionable insights on how to harness its power for your financial betterment.

Understanding the Fundamentals of Compound Interest

At its heart, compound interest is a concept that builds upon itself, creating an accelerating effect on your money. It’s not just about earning interest on your initial principal; it’s about earning interest on the interest you’ve already accumulated. This subtle yet powerful distinction is what sets it apart and makes it such a potent force in financial planning.

Defining the “Interest on Interest” Concept

Imagine you deposit a sum of money into an account or make an investment. In the first period, you earn interest on your initial deposit, known as the principal. With compound interest, this earned interest is then added back to your principal. In the subsequent period, you not only earn interest on your original principal but also on the interest that accumulated previously. This process repeats, creating a snowball effect where your capital grows at an ever-increasing rate. Each cycle, your base for calculating interest expands, leading to exponential growth rather than linear growth. This continuous re-investment of earnings is the engine behind compounding, allowing your money to work harder and more effectively for you over the long term.

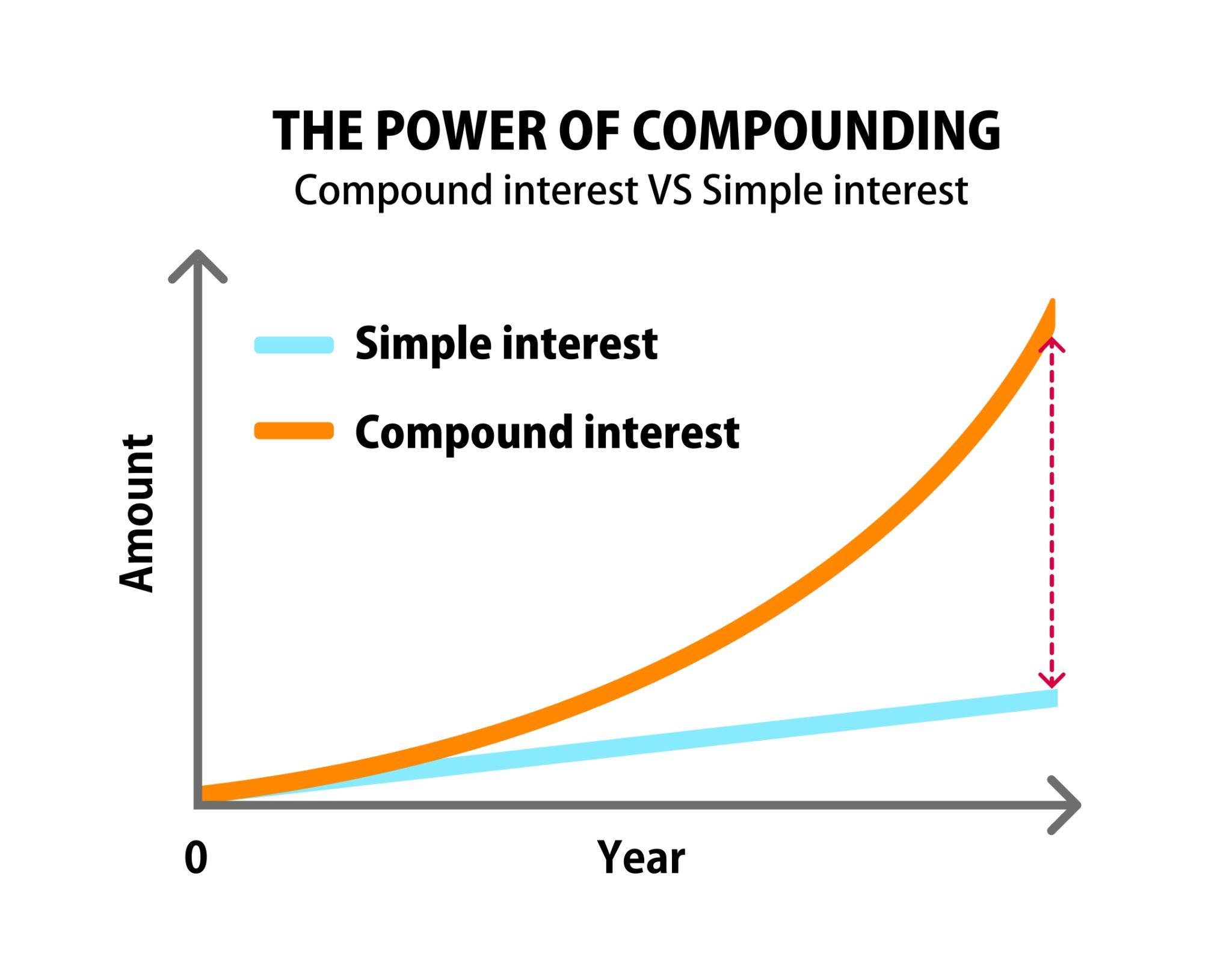

Compound Interest vs. Simple Interest: A Crucial Distinction

To fully appreciate the magic of compound interest, it’s vital to contrast it with its simpler counterpart: simple interest. Simple interest is calculated only on the original principal amount. For example, if you invest $1,000 at a 5% simple interest rate for 10 years, you would earn $50 per year ($1,000 * 0.05 = $50). Over 10 years, your total interest would be $500, and your investment would grow to $1,500. The principal amount remains the same for interest calculations throughout the entire period.

Compound interest, however, tells a different story. Using the same $1,000 at a 5% interest rate, compounded annually:

- Year 1: You earn $50 interest. Your total is now $1,050.

- Year 2: You earn interest on $1,050, which is $52.50. Your total is now $1,102.50.

- Year 3: You earn interest on $1,102.50, which is $55.13. Your total is now $1,157.63.

As you can see, the amount of interest earned each year increases because the base on which it’s calculated grows. Over a decade, the difference between simple and compound interest, while seemingly small initially, becomes significantly larger. Over several decades, the divergence is truly staggering, illustrating why understanding this distinction is foundational for any sound financial strategy.

The Exponential Power of Compounding

The real allure of compound interest lies in its exponential nature. It’s not just about adding a fixed amount each period; it’s about adding a growing amount, leading to rapid acceleration in wealth accumulation.

The Snowball Effect: How Time Magnifies Returns

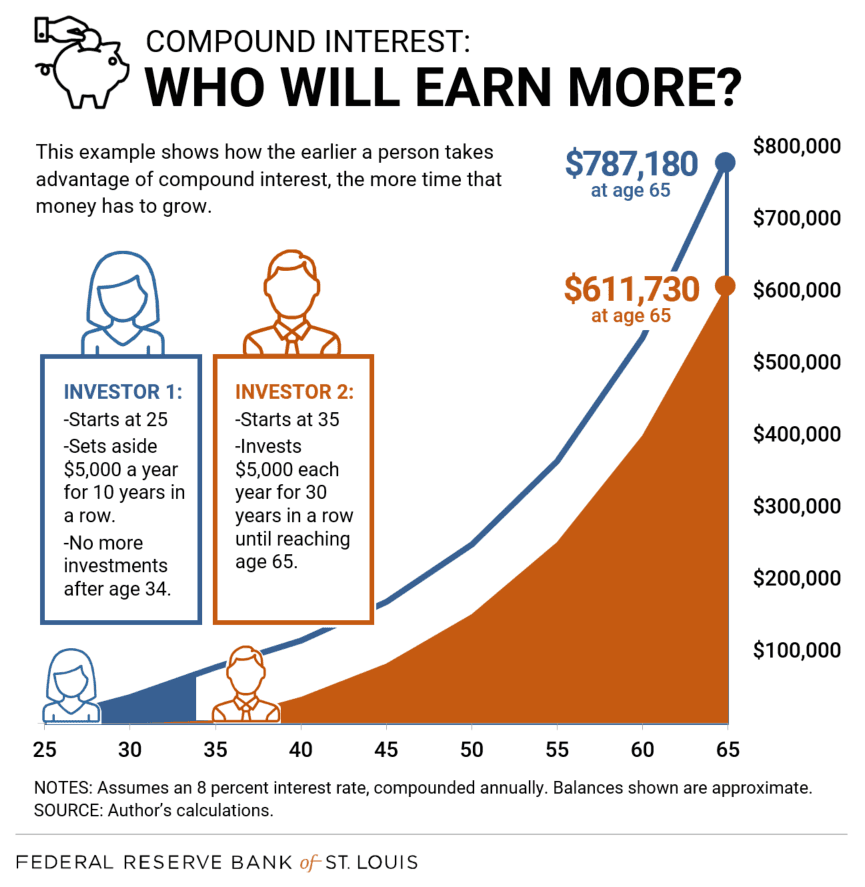

Think of a small snowball rolling down a hill. Initially, it picks up snow slowly, growing modestly. But as it gets larger, it covers more ground, accumulating snow at an increasingly faster rate. This is precisely how compound interest works with your money. The longer your money is invested and allowed to compound, the more significant the impact. Early returns, even if modest, become part of the principal for future calculations, generating even larger returns. This cyclical growth, fueled by time, means that every dollar invested early has far greater earning potential than a dollar invested later. The “snowball” truly begins to pick up momentum and mass over extended periods, turning relatively small initial investments into substantial sums. This effect is why financial advisors consistently emphasize the importance of starting to save and invest as early as possible.

The Rule of 72: A Quick Estimator for Growth

While precise calculations can be complex, the “Rule of 72” offers a remarkably simple and useful mental shortcut to estimate how long it will take for an investment to double at a given annual compound interest rate. The rule states:

Years to Double = 72 / Annual Interest Rate (as a whole number)

For instance, if your investment earns an 8% annual compound interest rate, it will take approximately 9 years (72 / 8 = 9) for your money to double. If you earn 6%, it will take roughly 12 years (72 / 6 = 12). This rule is an excellent tool for quick financial planning and understanding the impact of different interest rates on your money’s growth trajectory. It vividly highlights that even small differences in interest rates can have a substantial impact on the time it takes for your wealth to multiply.

Calculating and Maximizing Your Compound Returns

While the concept is intuitive, understanding the underlying formula and the factors that influence compound growth can empower you to make more informed financial decisions.

The Compound Interest Formula Explained

The standard formula for calculating compound interest is:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

Let’s use an example: If you invest $10,000 at an annual interest rate of 7% compounded quarterly for 10 years:

- P = $10,000

- r = 0.07

- n = 4 (compounded quarterly)

- t = 10

- A = 10,000 (1 + 0.07/4)^(4*10)

- A = 10,000 (1 + 0.0175)^(40)

- A = 10,000 (1.0175)^(40)

- A ≈ 10,000 * 1.9965

- A ≈ $19,965.25

After 10 years, your initial $10,000 would grow to nearly $20,000, almost doubling your money due to the power of compounding.

Key Factors Influencing Compound Growth

Several variables play a critical role in determining the ultimate impact of compound interest:

- Initial Principal (P): The larger your initial investment, the larger the base for compounding, leading to greater absolute returns.

- Interest Rate (r): This is perhaps the most significant factor. Even a seemingly small increase in the annual interest rate can dramatically alter the long-term growth of your investment. A higher rate means faster growth.

- Compounding Frequency (n): The more frequently interest is compounded (e.g., daily vs. annually), the faster your money grows. While the difference might be marginal over a short period, it becomes more noticeable over decades. Daily compounding generally yields slightly more than monthly, which yields more than quarterly, and so on.

- Time (t): As highlighted by the snowball effect, time is arguably the most crucial factor. The longer your money is allowed to compound, the more significant the exponential growth. This factor emphasizes the unparalleled advantage of starting early.

- Additional Contributions: While not explicitly in the formula, regularly adding more money to your principal significantly boosts the compounding process, accelerating your wealth accumulation far beyond what a static initial principal could achieve.

Practical Applications in Personal Finance and Investing

Compound interest is not merely a theoretical concept; it’s a practical tool that impacts various aspects of your financial life, from growing savings to managing debt.

Building Wealth Through Savings and Investments

For savers and investors, compound interest is the engine of long-term wealth creation. It’s the reason retirement accounts like 401(k)s and IRAs, which allow investments to grow tax-deferred or tax-free for decades, are so powerful.

- Retirement Planning: By consistently contributing to retirement accounts and investing in diversified assets (stocks, bonds, mutual funds) that offer reasonable returns, individuals can leverage compound interest to accumulate substantial nest eggs over 30-40 years.

- Long-term Savings Goals: Whether saving for a child’s education, a down payment on a house, or a major life event, allowing your savings to compound in high-yield savings accounts, Certificates of Deposit (CDs), or investment vehicles can significantly reduce the amount of “new money” you need to contribute to reach your goals.

- Dividend Reinvestment: Many stocks and mutual funds pay dividends. By choosing to reinvest these dividends to buy more shares, investors amplify the compounding effect, as future dividends will be paid on an even larger number of shares.

Understanding Compound Interest in Debt Management

While a powerful ally for saving, compound interest can become a formidable foe when applied to debt. Just as it grows your assets, it can rapidly inflate your liabilities, making debt repayment a challenging uphill battle.

- Credit Card Debt: Credit cards are notorious for high interest rates (often 15-25% APR) compounded daily or monthly. If only minimum payments are made, the interest can quickly spiral, leading to a situation where a significant portion of your payment goes towards interest, not the principal. This “debt snowball” works against you, making it difficult to pay off the balance.

- Loans: Personal loans, student loans, and mortgages also involve compound interest. While typically at lower rates than credit cards, the long repayment periods mean that a substantial amount of interest can accrue over the life of the loan. Understanding this allows you to strategize early repayments or extra principal payments to reduce the overall interest paid.

Recognizing how compound interest works on both sides of the balance sheet is crucial for financial health. It underscores the urgency of paying off high-interest debt quickly while simultaneously maximizing the compounding potential of your savings and investments.

Strategic Approaches to Harness Compound Interest

Leveraging compound interest effectively requires discipline, foresight, and a well-thought-out financial strategy. By adopting key habits, you can significantly enhance its positive impact on your financial future.

Starting Early and Staying Consistent

The single most impactful strategy for maximizing compound interest is to start investing as early as possible. The “time” variable in the compound interest formula is truly paramount. Even small, consistent contributions made over several decades will often outperform larger, later contributions due to the extended period available for compounding. An individual who starts investing $200 per month at age 25 will likely have significantly more wealth at retirement than someone who starts investing $400 per month at age 35, assuming similar returns. This highlights the immense cost of procrastination when it comes to financial planning. Consistency in contributions, even modest ones, ensures that the compounding engine is always fueled and running.

Reinvesting Dividends and Interest

Many investments, such as stocks, mutual funds, and even certain savings accounts, generate income in the form of dividends or interest. A powerful strategy to accelerate compounding is to automatically reinvest these earnings back into the investment. Instead of taking the cash, using it to purchase more shares or increase the principal of your savings account means that future dividends or interest will be earned on a larger base. This essentially compounds your earnings, allowing your investment to grow at an even faster rate without requiring additional “new money” from your pocket. Most brokerage accounts and investment platforms offer easy options for dividend reinvestment plans (DRIPs).

The Importance of a High Savings Rate

While starting early and reinvesting are crucial, the ultimate fuel for compounding is the amount of money you are putting into your investments. A higher savings rate means a larger principal amount, which in turn leads to greater absolute interest earnings. Increasing your contributions, even incrementally, can have a surprisingly large effect over time. For example, if you can increase your monthly investment from $300 to $400, that extra $100 compounds over decades, contributing significantly to your total wealth. Achieving a high savings rate often involves disciplined budgeting, identifying areas to reduce expenses, and prioritizing financial goals over immediate gratification. The more you can set aside and allow to grow, the more powerfully compound interest will work in your favor.

In conclusion, compound interest is not a complex financial trick but a fundamental force of nature in finance. By understanding how it works, respecting its power, and implementing strategic habits of early investment, consistent contributions, and diligent reinvestment, anyone can harness this “eighth wonder” to build substantial wealth and achieve their financial aspirations. Its true power lies in patience and time, transforming modest beginnings into significant financial legacies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.