Purchasing a wedding ring is often the first significant capital expenditure a couple makes together. While the emotional weight of the symbol is immeasurable, the financial reality is governed by market trends, commodity pricing, and personal finance strategies. In the landscape of modern personal finance, understanding the “average” cost is less about following a societal rule and more about navigating a complex market to ensure a sound investment that aligns with long-term fiscal health.

The Benchmark: Decoding National Averages and the “Salary Rule”

To understand what a wedding ring costs, one must first distinguish between marketing myths and statistical reality. For decades, the jewelry industry—most notably through De Beers’ mid-20th-century campaigns—suggested that a suitor should spend two to three months’ salary on an engagement ring. From a personal finance perspective, this “rule” is an arbitrary marketing construct designed to maximize consumer spending rather than reflect sound economic planning.

Current Market Statistics: What Couples Are Really Spending

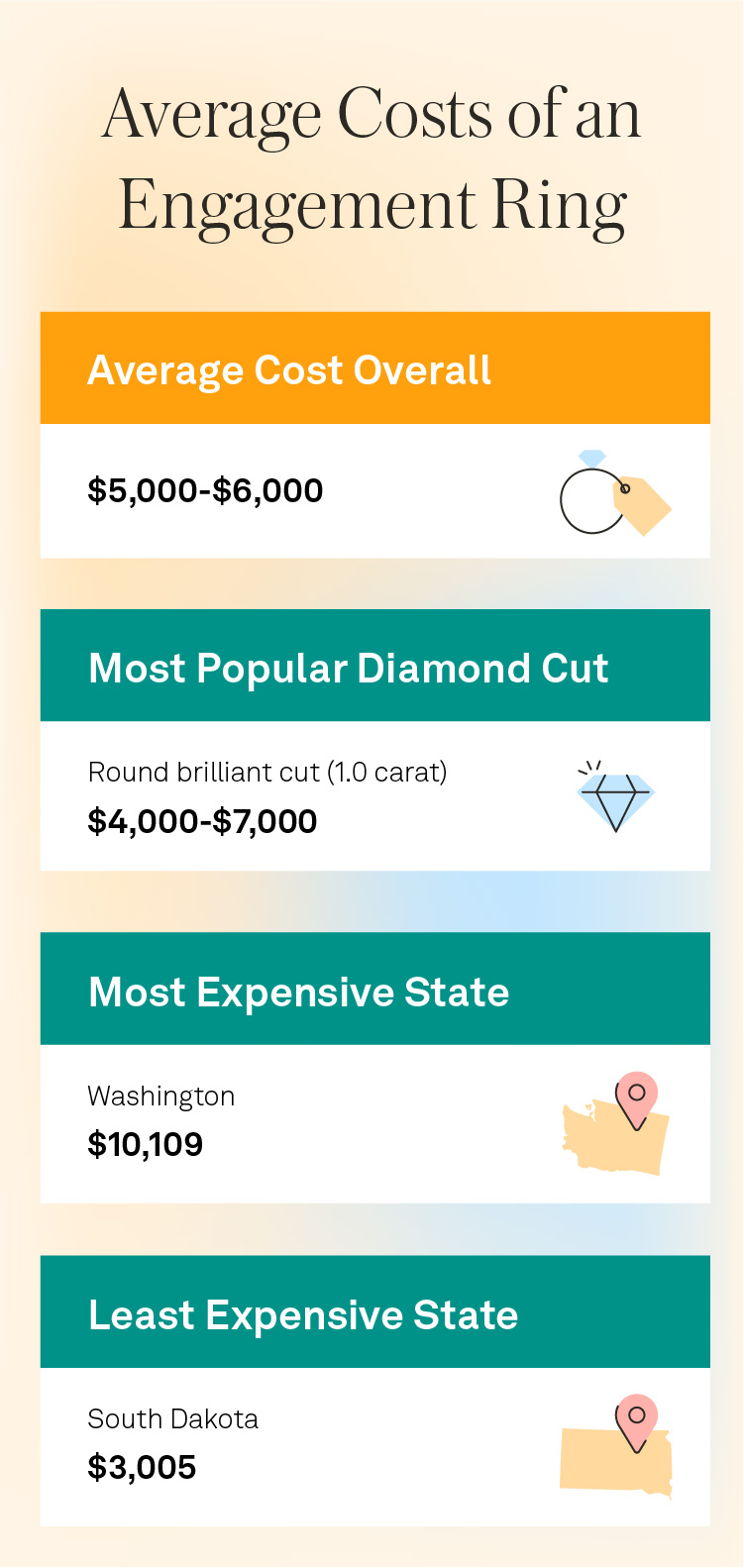

According to recent industry data from 2023 and 2024, the national average for an engagement ring in the United States hovers between $5,500 and $6,500. However, this average is heavily skewed by high-net-worth outliers. The median spend—often a more accurate representation of the typical consumer experience—frequently sits closer to $3,000 to $4,500. Wedding bands, which are purchased closer to the ceremony, typically cost an additional $500 to $1,500 depending on the metal and the presence of stones.

Debunking the Three Months’ Salary Myth

In the context of modern wealth management, the “three months’ salary” rule is increasingly viewed as a financial liability. For an individual earning a median household income, spending 25% of their annual gross pay on a depreciating asset (in liquid terms) can severely hinder other financial milestones, such as a down payment on a home or retirement contributions. Financial advisors today emphasize “affordability based on liquidity” rather than a percentage of gross income.

The Drivers of Cost: Materials, Markets, and Manufacturing

The price of a wedding ring is not a static figure; it is a calculation based on the current market value of precious metals and the scarcity of gemstones. Understanding these drivers allows a buyer to allocate their budget toward the elements that offer the best “value for money.”

The Diamond Premium and the 4Cs

The diamond remains the most significant cost driver in wedding jewelry. The price is determined by the “4Cs”: Cut, Color, Clarity, and Carat weight.

- Cut: This is the most critical factor for brilliance and can account for a 25% difference in price.

- Carat: The price of diamonds increases exponentially, not linearly, with weight. A 1.0-carat diamond will cost significantly more than two 0.5-carat diamonds of equal quality due to the rarity of larger stones.

- Color and Clarity: From a financial optimization standpoint, moving slightly down the scale in color (to G or H) or clarity (to VS1 or VS2) can save thousands of dollars without a visible difference to the naked eye.

Metal Selection: Gold vs. Platinum vs. Alternative Materials

The “housing” of the stone is the second major expense. Platinum is the most expensive due to its density and purity requirements, often costing 30-50% more than 14k gold. Gold prices are subject to global commodity market fluctuations. For those focused on cost-efficiency, 14k gold offers a higher durability-to-price ratio than 18k gold, as it is alloyed with stronger metals and contains less pure gold, which is naturally soft and expensive.

The Hidden Costs: Customization and Labor

Beyond raw materials, the “maker’s mark” adds a premium. Custom-designed rings involve CAD (Computer-Aided Design) fees, 3D printing of wax molds, and specialized labor. While a custom ring offers a unique brand identity for the wearer, it typically carries a 15-25% markup over “off-the-shelf” settings.

Strategic Budgeting: Affording the Ring Without Compromising the Future

A wedding ring should be a symbol of a beginning, not the start of a debt cycle. Managing this purchase requires the same level of due diligence one would apply to an investment portfolio or a vehicle purchase.

Setting a Realistic Spending Limit Based on Net Worth

Instead of following a “salary rule,” buyers should evaluate their “disposable liquidity.” A healthy financial approach involves looking at your current savings, deducting your six-month emergency fund, and seeing what remains. If the desired ring exceeds this amount, the solution is a dedicated sinking fund—saving a specific amount monthly over 12 to 18 months—rather than dipping into long-term investments or retirement accounts.

Financing Options: Interest-Free Periods vs. Personal Loans

Jewelry retailers frequently offer “0% APR” financing for 12 to 24 months. From a cash-flow perspective, this can be an attractive tool, allowing the buyer to keep their cash in a High-Yield Savings Account (HYSA) or invested in the market while paying down the ring. However, this is only a “win” if the buyer has the discipline to pay the balance before the promotional period ends. If a balance remains, interest rates often skyrocket to 25% or higher, retroactively applied to the original balance, turning a smart financial move into a predatory debt trap.

Long-Term Financial Implications: Insurance and Asset Value

Once the ring is purchased, it transitions from a “buy” to an “asset” on the personal balance sheet. However, jewelry is a unique asset class that requires active management to protect its value.

Protecting the Asset: The Necessity of Jewelry Insurance

A wedding ring is a high-concentration risk. Loss, theft, or damage can result in a total loss of the capital invested. Most standard homeowners’ or renters’ insurance policies have a “cap” on jewelry (often $1,000 to $2,500). If the ring exceeds this value, a specialized jewelry rider or a standalone policy is necessary. These policies typically cost 1% to 2% of the ring’s appraised value annually. While it is an ongoing expense, it is a necessary hedge against the loss of a significant financial investment.

Resale Value and the “Investment” Fallacy

It is a common misconception that wedding rings are “investments” that appreciate over time. In reality, the retail markup on jewelry is significant (often 100% or more). If you were to sell a ring back to a jeweler the day after purchase, you would likely receive only the “melt value” of the metal and a fraction of the stone’s retail price. Unless the stone is an exceptionally rare, investment-grade diamond (typically 3+ carats with flawless specifications), a wedding ring should be viewed as a “consumption asset” rather than a financial investment intended for capital gains.

Smart Shopping Strategies for the Modern Consumer

The digital age has disrupted the traditional jewelry markup model, providing consumers with tools to lower the average cost without sacrificing quality.

Lab-Grown Diamonds: A Cost-Efficiency Revolution

Perhaps the greatest shift in the “average cost” of wedding rings in the last decade is the rise of lab-grown diamonds. Chemically, physically, and optically identical to mined diamonds, lab-grown stones currently trade at a 60% to 80% discount compared to their mined counterparts. For a buyer focused on maximizing “visual impact” per dollar spent, lab-grown diamonds represent the most efficient use of capital in the current market.

Timing the Market and Secondary Market Opportunities

The jewelry industry has its own cyclicality. Prices often peak during “engagement season” (November through February). Buying “off-peak” or utilizing reputable secondary market platforms can yield significant savings. Platforms that verify and resell pre-owned luxury rings allow buyers to acquire high-end brands (like Tiffany & Co. or Cartier) at 40-50% off retail prices. From a pure “Money” perspective, the secondary market is the most logical place to find high-intrinsic-value pieces without the “new-car-smell” markup of a retail showroom.

In conclusion, the average cost of a wedding ring is a flexible figure that should be dictated by your personal financial roadmap rather than societal pressure. By understanding the underlying costs of materials, utilizing modern alternatives like lab-grown stones, and protecting the purchase through proper insurance, a couple can ensure that this significant life milestone strengthens their financial foundation rather than weakening it. Professional financial planning suggests that the best ring is not the most expensive one, but the one that is bought with cash, insured properly, and fits comfortably within a broader wealth-building strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.