In the modern economic landscape, the automobile remains one of the most significant financial commitments for the average household. Second only to housing, transportation costs—specifically car payments—have seen a meteoric rise over the last few years. What used to be a predictable monthly expense has transformed into a complex financial hurdle, influenced by global supply chains, fluctuating interest rates, and a shifting consumer preference toward larger, tech-heavy vehicles. Understanding the average car payment is no longer just about knowing a single number; it is about understanding the broader financial ecosystem that dictates how we spend, save, and invest for the future.

The State of the Market: Breaking Down Current Average Car Payments

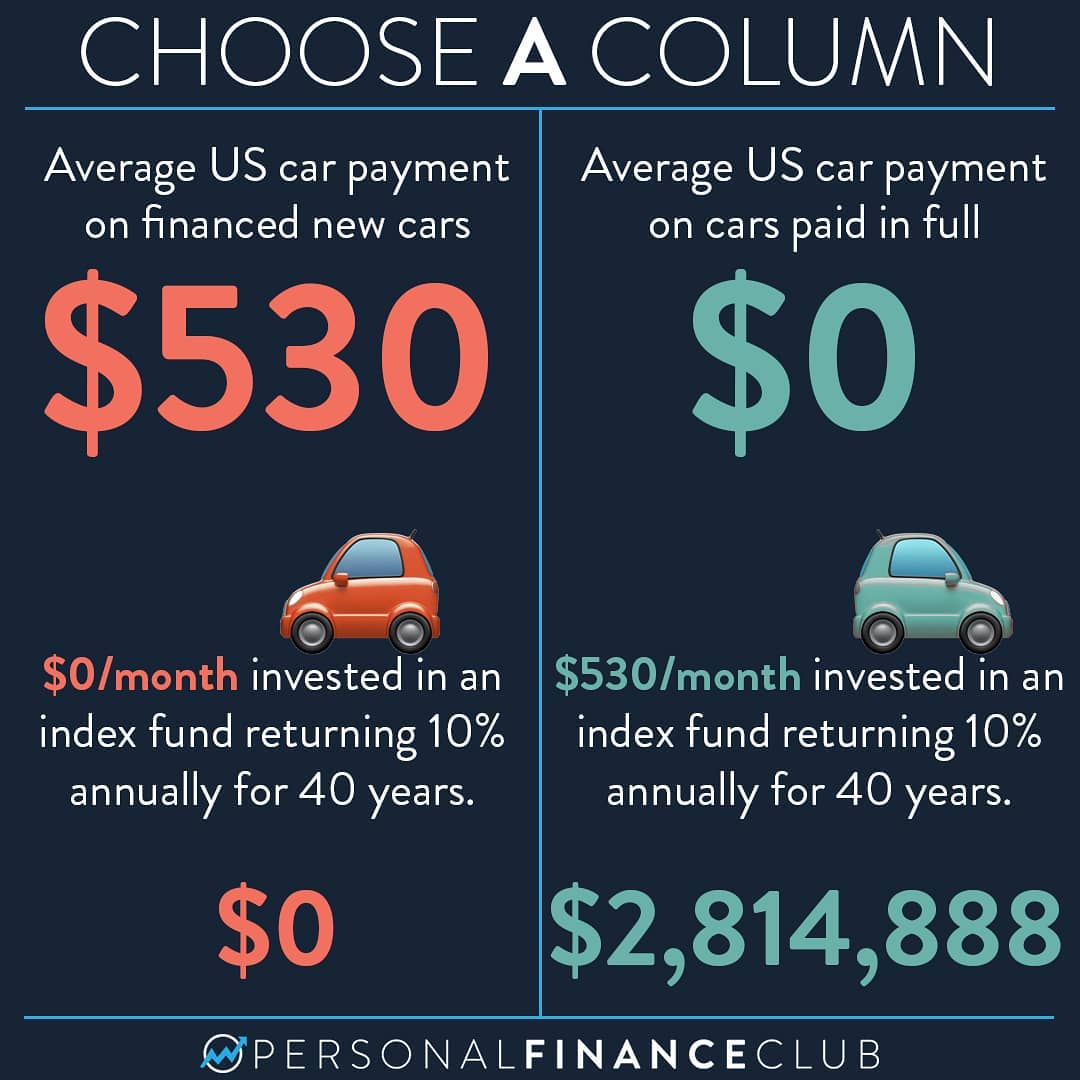

To understand where we are, we must look at the data provided by credit bureaus and financial analysts. As of late 2023 and moving into 2024, the average monthly payment for a new vehicle has hovered around the $730 mark. For used vehicles, which were once the “budget-friendly” alternative, the average has climbed to approximately $530. These figures represent record highs and signal a paradigm shift in how Americans approach vehicle ownership.

New vs. Used: The Widening Gap

Historically, the gap between new and used car payments was significant enough to steer budget-conscious consumers toward the pre-owned market. However, the used car market saw unprecedented inflation during the early 2020s. While prices have begun to stabilize, the “average” used car payment is now higher than the average “new” car payment was just a decade ago. This convergence means that consumers are often forced to choose between a high payment for a reliable new car with a warranty or a still-high payment for a used car with potential maintenance risks.

Lease vs. Loan: Comparing Monthly Outlays

Leasing has traditionally offered a lower monthly payment because the consumer is essentially paying for the vehicle’s depreciation rather than its total value. However, even lease payments have seen a sharp increase, now averaging over $600 per month. From a wealth-building perspective, leasing remains a contentious topic. While it lowers the monthly cash outflow compared to a high-interest loan on a new purchase, it prevents the consumer from building equity in an asset, often resulting in a perpetual cycle of payments.

Why Car Payments Are Soaring: The Macro and Micro Factors

The surge in average car payments is not the result of a single factor but rather a “perfect storm” of economic pressures. To manage personal finances effectively, one must look beneath the sticker price to see the levers that are actually driving these monthly costs higher.

The Impact of Record-High Interest Rates

Perhaps the most significant driver of increased payments in the current market is the Federal Reserve’s stance on interest rates. When the base interest rate rises, auto lenders follow suit. For a consumer with a “prime” credit score, interest rates might sit between 5% and 7%. However, for those in the “subprime” category, rates can soar above 15% or even 20%. On a $40,000 loan, the difference between a 3% and a 10% interest rate can add over $100 a month to the payment and thousands of dollars to the total cost of the loan.

Escalating Vehicle Prices and Inventory Constraints

The average transaction price for a new vehicle has surpassed $48,000. This is driven by two factors: the increased cost of manufacturing (due to raw materials and labor) and a consumer shift away from compact sedans toward SUVs and trucks. Manufacturers have leaned into this trend, prioritizing the production of high-margin luxury trims over base models. Consequently, the “entry-level” vehicle is becoming a rarity, forcing the average payment upward simply because the floor of the market has risen.

The Lengthening of Loan Terms

To keep monthly payments “affordable” in the face of rising prices, many consumers are opting for longer loan terms. It is now common to see 72-month (six-year) or even 84-month (seven-year) auto loans. While this reduces the immediate monthly burden, it is a dangerous financial trap. Longer terms result in paying more total interest and increase the likelihood of becoming “upside down” on the loan—where the vehicle’s value is less than the remaining balance.

The Financial Impact: How Your Car Payment Affects Your Long-Term Wealth

In the world of personal finance, your car payment is often referred to as an “opportunity cost.” Every dollar sent to a depreciating asset is a dollar that cannot be used to purchase an appreciating asset, such as stocks, real estate, or a retirement fund.

Opportunity Cost and the 20/4/10 Rule

Financial experts often recommend the “20/4/10” rule to maintain financial health: put 20% down, finance for no more than 4 years, and ensure total transportation costs (payment, insurance, fuel) do not exceed 10% of your gross monthly income. When the average car payment hits $730, an individual would need a gross monthly income of $7,300—or nearly $88,000 a year—just to afford the car payment comfortably under this rule.

The real danger lies in the lost compound interest. If a 25-year-old invested that $730 monthly payment into a low-cost index fund averaging an 8% annual return instead of paying off a car, they would have over $2.5 million by age 65. This perspective highlights why the “average” car payment is often the biggest obstacle to becoming a millionaire for the middle class.

Credit Score Dynamics: How Your History Dictates Your Monthly Bill

Your credit score is the single most powerful tool for lowering a car payment. A buyer with a 750+ credit score might pay $600 a month for the exact same vehicle that costs a buyer with a 550 score $850 a month. In the “Money” niche, the car payment is a reflection of financial hygiene. Maintaining a strong credit profile allows for lower interest rates, which directly reduces the monthly payment without requiring a cheaper vehicle.

Strategies to Optimize Your Transportation Budget

If you find yourself burdened by a payment that is higher than the national average, or if you are looking to enter the market, there are several strategic moves to protect your net worth.

Refinancing and Negotiation Tactics

For those currently locked into a high-interest loan, refinancing is a powerful tool—especially if your credit score has improved since the initial purchase. Moving from a 12% rate to a 6% rate can save hundreds of dollars a month. Additionally, when shopping, consumers should negotiate based on the out-the-door price rather than the monthly payment. Dealerships often use “payment-based selling” to hide the true cost of the car, extending the loan term to make an expensive car look affordable on a monthly basis.

Prioritizing Total Cost of Ownership (TCO)

The average car payment is only one part of the equation. A savvy investor looks at the Total Cost of Ownership (TCO). A vehicle with a $500 payment might actually be more expensive than one with a $600 payment if the former has higher insurance premiums, poor fuel economy, and a history of expensive repairs. Tools like the Edmunds TCO calculator allow consumers to project these costs over five years, ensuring that the “average” payment doesn’t turn into an above-average financial drain.

The Power of the Down Payment

In an era of high interest rates, the down payment is your best defense. By putting more money down upfront, you reduce the principal balance of the loan, which in turn reduces the amount of interest accrued over time. This also provides an immediate equity cushion, protecting you from the “gap” if the vehicle is totaled or needs to be sold quickly.

Conclusion

The average car payment of today—exceeding $700 for new vehicles—is a reflection of a complex and often predatory lending environment. While a vehicle is a necessity for most, it does not have to be a financial anchor. By understanding the mechanics of interest rates, loan terms, and opportunity costs, consumers can make informed decisions that prioritize their long-term wealth over short-term status. Whether it is through aggressive saving for a down payment, improving a credit score, or simply opting for a reliable used vehicle, the goal should always be to keep the car payment as a small, manageable fraction of one’s broader financial picture. In the end, the most expensive car is the one that prevents you from reaching your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.