Embarking on the journey of homeownership is often one of the most significant financial decisions an individual or family will make. Amidst the excitement of house hunting and imagining life in a new space, prospective homeowners are quickly confronted with a lexicon of financial terms: interest rates, closing costs, escrow, and perhaps most critically, the Annual Percentage Rate (APR). While the interest rate often takes center stage in initial discussions, understanding the APR is paramount to grasping the true cost of your mortgage over its lifetime. It’s the metric designed to provide a comprehensive, apples-to-apples comparison of loan offers, transcending the seemingly straightforward interest rate to reveal the broader financial implications of borrowing.

This guide will demystify the APR, breaking down its components, explaining its significance, and equipping you with the knowledge to make informed decisions when securing your mortgage. We’ll explore why APR is more than just a number, how it impacts your long-term financial health, and strategies to secure the most favorable terms for your home loan.

Understanding the Fundamentals: APR vs. Interest Rate

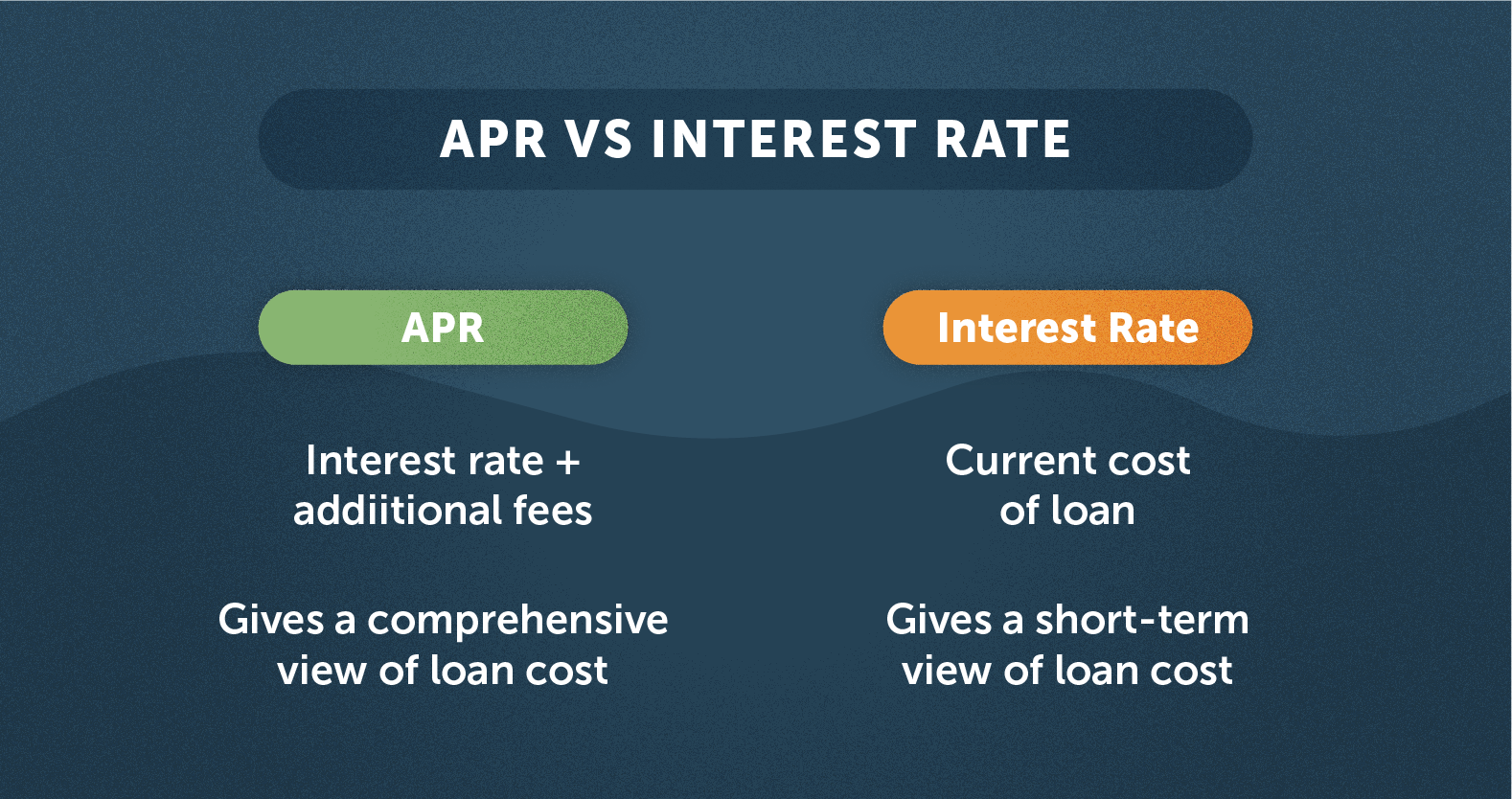

To truly appreciate the APR, it’s essential to first differentiate it from the more commonly discussed interest rate. While often used interchangeably in casual conversation, these two figures represent distinct aspects of your loan’s cost. Grasping this distinction is the cornerstone of intelligent mortgage shopping.

The Stated Interest Rate: Your Principal’s Cost

The interest rate is arguably the most recognized number associated with a loan. In simple terms, it’s the percentage charged by the lender for borrowing the principal amount – the actual money you receive to purchase your home. This rate directly determines your monthly mortgage payment, calculating the cost of using the borrowed funds. If you borrow $300,000 at a 4% interest rate, that 4% is applied to the remaining principal balance each month to calculate a portion of your payment. It’s the engine driving the amortization schedule, dictating how much of each payment goes towards interest versus principal over the loan’s term.

Lenders often quote this rate prominently because it directly influences the affordability of your monthly payments. A lower interest rate typically translates to lower monthly payments, making a loan more accessible in the short term. However, focusing solely on this figure can be misleading, as it doesn’t account for all the costs associated with obtaining the mortgage. It’s merely one piece of a larger financial puzzle, albeit a very significant one. For most homeowners, understanding their interest rate is crucial for budgeting purposes, but for true cost comparison, another metric comes into play.

Beyond the Interest: What APR Truly Represents

This is where the Annual Percentage Rate (APR) steps in to provide a more holistic view of the loan’s cost. Unlike the simple interest rate, the APR encompasses not only the interest charged on the principal but also most of the other fees and charges involved in originating the loan, expressed as a single, annualized percentage. Think of the APR as the “true” or “effective” cost of borrowing. It includes fees such as loan origination fees, discount points, mortgage broker fees, and certain closing costs. By bundling these charges into a single percentage, the APR aims to give consumers a standardized metric for comparing different loan offers.

The purpose of the APR is to standardize loan disclosures, ensuring transparency and enabling consumers to compare apples to apples when evaluating different lenders. Without the APR, a lender could offer a very low interest rate but hide substantial fees, making their loan appear cheaper than it actually is. The APR essentially projects these upfront costs over the life of the loan, adding them to the interest rate to give you a more comprehensive picture. It’s the percentage you’d effectively be paying if all those additional costs were spread out and included in your interest payment from day one. Therefore, while the interest rate dictates your monthly payment, the APR provides the best estimate of the total cost of the loan over its entire term.

Deconstructing the Annual Percentage Rate (APR)

To effectively use the APR as a comparison tool, it’s crucial to understand what goes into its calculation. It’s not just a random number; it’s a carefully calculated figure mandated by consumer protection laws, designed to present a more complete financial picture of your mortgage.

Key Components that Factor into APR

The calculation of APR considers a range of costs beyond the nominal interest rate. These are typically one-time fees paid at closing or during the loan’s origination process, which, when amortized over the loan term, contribute to a higher effective rate. Key components include:

- Loan Origination Fees: These are charges from the lender for processing and underwriting your loan. They cover administrative costs, paperwork, and the lender’s profit for initiating the loan. Often expressed as a percentage of the loan amount (e.g., 1% of the loan), these fees can significantly impact the APR.

- Discount Points (or Mortgage Points): These are optional fees paid upfront to the lender in exchange for a lower interest rate. One “point” typically equals 1% of the loan amount. While paying points reduces the interest rate, the cost of these points is factored into the APR, reflecting that initial outlay.

- Mortgage Broker Fees: If you use a mortgage broker, they charge a fee for their services, which can also be included in the APR calculation.

- Underwriting Fees: A specific charge for the lender’s service in evaluating the risk of lending to you.

- Processing Fees: Fees related to the administrative tasks involved in handling your loan application.

It’s important to note that not all closing costs are included in the APR calculation. For instance, third-party fees such as appraisal fees, title insurance, attorney fees, recording fees, and property taxes are typically excluded from the APR, although they are part of your overall closing costs. The distinction lies in whether the fee is charged directly by the lender or a third-party service provider. This selectivity is why, even with the APR, a careful review of the Loan Estimate is always recommended.

The Significance of Loan Fees and Discount Points

Loan fees, particularly origination fees and discount points, play a pivotal role in shaping your APR. A loan with a seemingly low interest rate might come with hefty upfront fees, which will inevitably push its APR higher than another loan with a slightly higher interest rate but minimal fees. For example, Lender A might offer a 4.0% interest rate with 2 points, while Lender B offers a 4.25% interest rate with no points. While Lender A’s interest rate is lower, the cost of the two points must be factored into the APR, potentially making Lender B’s offer, despite its higher interest rate, have a lower overall APR.

The decision to pay discount points is often a strategic one, aimed at reducing the monthly payment over the long term. However, the calculation of the APR helps borrowers understand the trade-off. It allows you to see the effective cost of “buying down” your interest rate. If you plan to live in the home for a significant period, paying points might be beneficial, but the APR will reflect that initial investment as part of the total cost of borrowing. Conversely, if you anticipate refinancing or selling within a few years, paying points might not be financially advantageous, and the APR will clearly illustrate the higher true cost given the shorter term over which those points are amortized.

Mortgage Insurance and Other Related Costs

For many homeowners, especially those making a down payment of less than 20%, mortgage insurance is a mandatory component of their loan. This can come in various forms, such as Private Mortgage Insurance (PMI) for conventional loans or Mortgage Insurance Premiums (MIP) for FHA loans. The costs associated with mortgage insurance, whether upfront premiums or ongoing monthly charges, are generally included in the APR calculation if they are a condition of obtaining the loan from that specific lender. This inclusion further elevates the APR, providing a more accurate reflection of the total borrowing cost for those who require it.

Other related costs, such as prepaid interest (interest that accrues from the closing date to the first payment due date), can also factor into the APR. The overarching principle is that if a fee is required by the lender as a condition of extending the credit, it’s typically included in the APR. This comprehensive approach ensures that borrowers are not surprised by hidden costs and can genuinely compare the expense of one mortgage product against another. Understanding these included costs empowers you to question line items on your Loan Estimate and engage in more informed negotiations with lenders.

Why APR is Your Most Powerful Comparison Tool

The primary purpose of the APR is not just to confuse you with another acronym, but to serve as a vital consumer protection mechanism. It transforms complex loan offers into a digestible, standardized figure, making it the single most effective tool for comparing different mortgage options.

Evaluating the True Cost of Borrowing

Without the APR, comparing mortgage offers would be akin to comparing apples and oranges. Lenders could entice borrowers with low advertised interest rates while embedding significant fees into the loan, making the true cost opaque. The APR cuts through this complexity by standardizing how these fees are disclosed. When you look at two different Loan Estimates, you might see one with a slightly lower interest rate but a higher APR, and another with a slightly higher interest rate but a lower APR. This immediately tells you that the loan with the higher APR, despite its appealing interest rate, has more upfront or embedded costs that will ultimately make it more expensive over the life of the loan.

The APR essentially annualizes all the included costs, presenting them as a single percentage that reflects the true annual cost of credit. This allows you to evaluate which loan will cost you less in total over the long run, rather than just focusing on the monthly payment which is primarily driven by the interest rate. For major financial commitments like a mortgage, understanding the true cost upfront can save tens of thousands of dollars over 15 or 30 years. It’s a powerful metric that shifts the focus from superficial rates to the comprehensive financial outlay.

Navigating Different Lender Offers

Imagine you’re comparing three loan offers:

- Offer A: 4.0% interest rate, 2 points, $1,500 origination fee. APR: 4.25%

- Offer B: 4.15% interest rate, 1 point, $800 origination fee. APR: 4.20%

- Offer C: 4.3% interest rate, 0 points, $500 origination fee. APR: 4.35%

Without the APR, you might instinctively lean towards Offer A due to its lowest interest rate. However, by looking at the APR, you immediately see that Offer B, despite a slightly higher interest rate, has the lowest overall cost when all fees are factored in. This simple example illustrates the power of the APR in helping you navigate the competitive landscape of mortgage lending. It provides an objective basis for comparison, preventing you from being swayed purely by an attractive interest rate that might be offset by exorbitant fees.

Savvy borrowers use the APR as their primary metric for initial comparison, drilling down into the details of the Loan Estimate once they’ve narrowed down their options based on APR. It streamlines the decision-making process, ensuring that the total cost of borrowing is always considered alongside the monthly payment.

Regulatory Protection: The Truth in Lending Act (TILA)

The concept of the APR as a standardized disclosure mechanism is rooted in the Truth in Lending Act (TILA), a federal law enacted to protect consumers in credit transactions. TILA mandates that lenders provide clear and consistent disclosures about the terms and costs of credit, with the APR being a central component of these disclosures. The goal is to ensure that consumers have accurate and comprehensible information to make informed decisions.

Specifically, TILA requires lenders to disclose the APR, the finance charge (the total dollar amount of all charges, including interest and other fees), and the payment schedule. This regulatory framework ensures that the APR is calculated uniformly across all lenders, making it a reliable benchmark for comparison. Without TILA and the mandatory disclosure of APR, consumers would be at a significant disadvantage, struggling to decipher the true cost of loans and falling prey to potentially misleading advertising. Thus, the APR is not just a useful tool; it’s a legally mandated safeguard designed to foster transparency and fairness in the lending market.

Factors Influencing Your Mortgage APR

While the APR provides a standardized way to compare loans, its specific value for your mortgage is influenced by a multitude of factors. These elements dictate the risk a lender perceives in extending credit to you and the prevailing economic conditions, all of which coalesce into your final APR.

Your Creditworthiness: A Major Determinant

One of the most significant factors influencing the APR you’re offered is your creditworthiness. Lenders assess your financial reliability primarily through your credit score and credit history. A higher credit score (e.g., FICO score typically above 740) indicates a lower risk of default, making you a more attractive borrower. In turn, lenders are willing to offer lower interest rates and, consequently, a lower APR to these prime borrowers. Conversely, individuals with lower credit scores are perceived as higher risk, leading lenders to charge higher interest rates and potentially higher fees, which translate to a higher APR.

Beyond the score itself, your credit history, including payment consistency, debt-to-income ratio, and the duration of your credit history, all play a role. A history of timely payments, a manageable debt load, and a long-established credit profile signal financial responsibility, contributing to a more favorable APR. Conversely, late payments, defaults, or high revolving debt can negatively impact your APR, highlighting the importance of managing your credit proactively before applying for a mortgage.

Loan Type and Term: Fixed vs. Adjustable, 15 vs. 30 Year

The characteristics of the mortgage product itself significantly influence the APR.

- Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs): Fixed-rate mortgages offer a constant interest rate and payment over the life of the loan. Their APR will reflect this stability. ARMs, on the other hand, start with an initial fixed interest rate for a period (e.g., 5, 7, or 10 years) before adjusting periodically based on an index. The APR for an ARM is calculated based on an index and margin, projecting the average annual cost over the loan’s life, assuming certain rate movements. Due to the inherent uncertainty of future rate adjustments, ARMs often have a lower initial interest rate but their APR can be more complex to compare, reflecting potential future increases.

- Loan Term (15-year vs. 30-year): Shorter loan terms, such as a 15-year mortgage, typically come with lower interest rates and often lower APRs compared to 30-year mortgages. This is because the lender is exposed to risk for a shorter period. While the monthly payments on a 15-year loan will be significantly higher, the total interest paid over the life of the loan is substantially less, and this efficiency is reflected in a lower APR. Longer terms, while offering lower monthly payments, accumulate more interest over time, leading to a higher overall APR.

Market Conditions and Economic Indicators

The broader economic environment plays a crucial role in determining prevailing mortgage rates and, by extension, APRs. Factors such as the Federal Reserve’s monetary policy, inflation rates, bond market performance (particularly the yield on U.S. Treasury bonds), and overall economic growth can cause mortgage rates to fluctuate daily. When the economy is strong and inflation is a concern, interest rates tend to rise. Conversely, during periods of economic uncertainty or recession, rates may fall as investors seek safe havens. Lenders price their mortgages based on these market conditions, which means the APRs offered at any given time are a reflection of the current economic climate. Borrowers often monitor these trends to apply for a mortgage when rates are most favorable, as even a quarter-point difference in APR can result in thousands of dollars in savings over the loan term.

Lender-Specific Policies and Profit Margins

While broad market conditions set the baseline, individual lenders also have their own policies, pricing strategies, and profit margin objectives that influence the APR they offer. Some lenders might specialize in certain loan types or borrower profiles, allowing them to offer more competitive rates or lower fees in those niches. Others might have higher overhead costs or different risk assessments, leading to slightly higher APRs. The competitive nature of the mortgage market often means lenders adjust their rates and fees to attract borrowers, but their internal business models dictate the floor and ceiling for their offerings. This variation underscores the importance of comparison shopping, as different lenders will truly offer different APRs for the same borrower and loan type, even on the same day.

Strategies for Securing a Favorable Mortgage APR

Given the long-term financial implications of your mortgage APR, actively pursuing the most favorable rate is a critical step in the homeownership process. While market conditions are beyond your control, several proactive strategies can significantly improve your chances of securing a lower APR.

Bolstering Your Financial Profile

Before you even begin seriously looking for a mortgage, take steps to strengthen your financial standing. This will make you a more attractive borrower and qualify you for better terms.

- Improve Your Credit Score: This is perhaps the most impactful step. Pay all your bills on time, reduce your credit card balances to lower your credit utilization, avoid opening new credit accounts right before applying for a mortgage, and dispute any errors on your credit report. A higher credit score directly translates to lower perceived risk for lenders, which often leads to lower interest rates and fees, thus reducing your APR. Aim for a score of 740 or higher, if possible.

- Reduce Your Debt-to-Income (DTI) Ratio: Your DTI is a key metric lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates you have more disposable income to cover mortgage payments. Work on paying down existing debts, particularly high-interest consumer debt, to improve this ratio. Lenders typically prefer a DTI of 36% or less, though some programs allow up to 43% or even higher.

- Increase Your Down Payment: A larger down payment reduces the loan amount, which in turn reduces the lender’s risk. This often results in a lower interest rate and can help you avoid private mortgage insurance (PMI), which typically gets factored into the APR. Even a slightly larger down payment can have a disproportionate positive impact on your APR.

- Build Cash Reserves: Lenders look favorably upon borrowers with emergency savings. Having a healthy reserve fund demonstrates financial stability and your ability to weather unexpected expenses without defaulting on your mortgage.

The Power of Comparison Shopping

This cannot be stressed enough: do not settle for the first loan offer you receive. The mortgage market is highly competitive, and rates and fees can vary significantly between lenders for the same borrower on the same day.

- Shop Multiple Lenders: Contact at least 3-5 different lenders – including banks, credit unions, and mortgage brokers. Each lender has different pricing models, loan products, and fee structures. By getting multiple Loan Estimates, you can directly compare APRs, interest rates, and all associated costs.

- Get Pre-Approved: Getting pre-approved by multiple lenders can give you concrete loan offers and APRs to compare without impacting your credit score significantly. Most credit scoring models allow for a shopping period (typically 14-45 days) where multiple inquiries for the same type of loan are counted as a single inquiry, minimizing the impact on your credit.

- Compare Loan Estimates Carefully: The Loan Estimate form, standardized by the Consumer Financial Protection Bureau (CFPB), is your best friend here. Pay close attention to Box A (Origination Charges) for fees included in the APR, and then directly compare the APR listed on each document. Remember that not all fees are included in the APR, so also review other closing costs to understand the full financial picture.

Negotiating Fees and Understanding Trade-offs

Once you have multiple offers, you might be in a position to negotiate, especially if you have a strong financial profile.

- Negotiate Loan Origination Fees: Some lenders may be willing to reduce or waive certain fees, particularly if they know you have a better offer from a competitor.

- Consider “No-Closing-Cost” Loans: Some lenders offer “no-closing-cost” mortgages, where they cover your closing costs in exchange for a slightly higher interest rate. While this means less money out of pocket upfront, it will typically result in a higher APR over the life of the loan. Evaluate if this trade-off is worthwhile for your specific financial situation.

- Weigh Discount Points: Decide if paying discount points to reduce your interest rate is a sound strategy for you. While it lowers your interest rate, it increases your upfront costs, which are factored into the APR. Calculate the “break-even point” – how long it will take for the interest savings to offset the cost of the points. If you plan to stay in the home longer than the break-even point, paying points might be advantageous. If not, a loan with fewer points (and a slightly higher interest rate) might result in a lower APR over your anticipated loan term.

By proactively managing your financial health and diligently comparing loan offers, you can significantly influence the APR you secure, potentially saving you a substantial amount of money over the life of your mortgage. Understanding “what is the APR on a mortgage” is not just academic; it’s a fundamental step towards intelligent and cost-effective homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.