For most individuals, a mortgage is the largest financial commitment they will ever undertake. When shopping for a home loan, the sheer volume of terminology—escrow, amortization, principal, points, and interest—can be overwhelming. Among these terms, the Annual Percentage Rate, or APR, stands as one of the most critical metrics for any borrower to understand. While many homebuyers focus solely on the “sticker price” interest rate, the APR provides a more comprehensive picture of the true cost of borrowing.

In the realm of personal finance, understanding the nuances of APR is not just an academic exercise; it is a vital skill that can save a homeowner tens of thousands of dollars over the life of a loan. This guide delves deep into what the APR represents, how it differs from the base interest rate, and why it is the ultimate tool for comparing mortgage offers.

What is APR and How Does It Differ from Interest Rates?

To understand a mortgage offer, one must first distinguish between the nominal interest rate and the APR. While they are both expressed as percentages, they serve two distinct purposes in your financial planning.

The Definition of APR

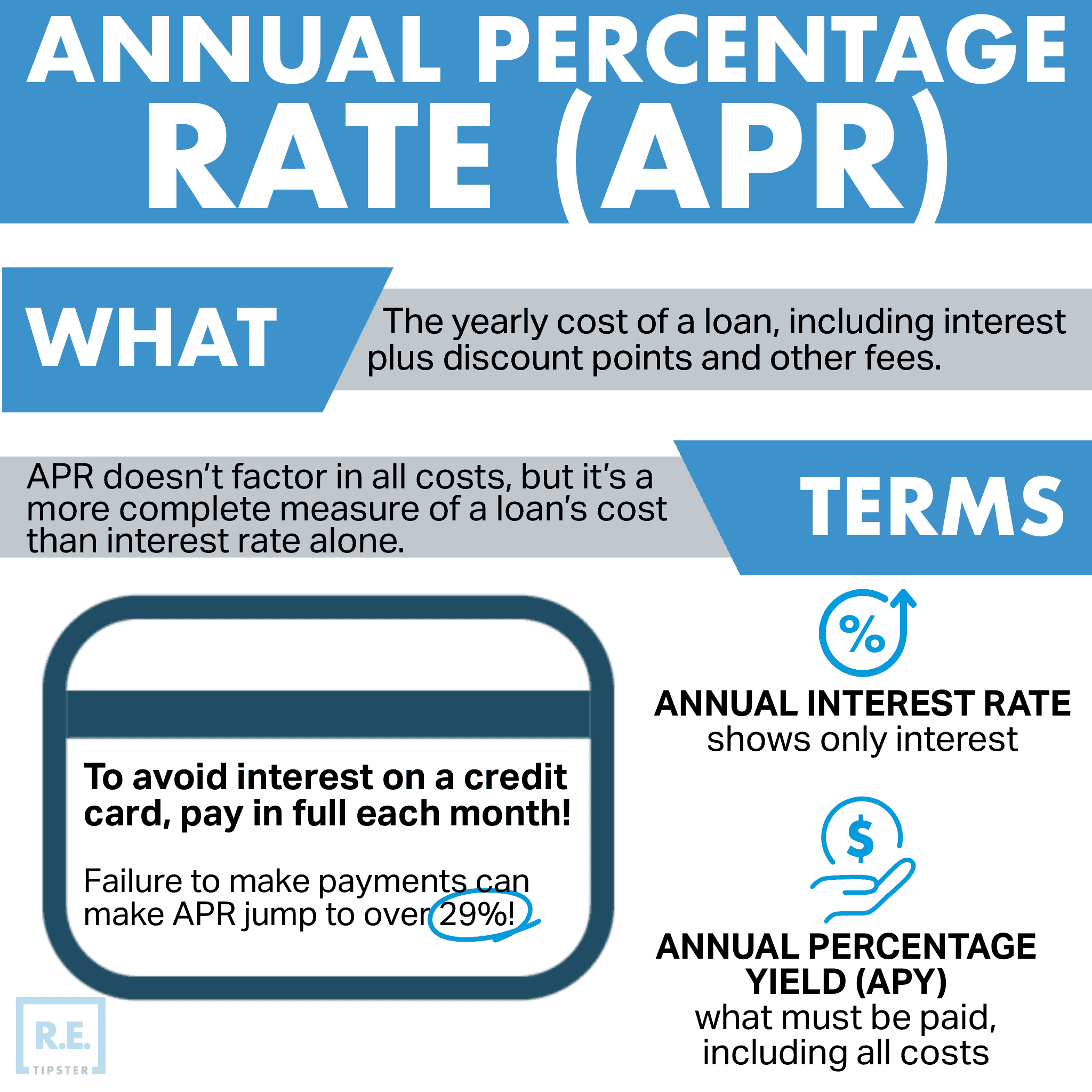

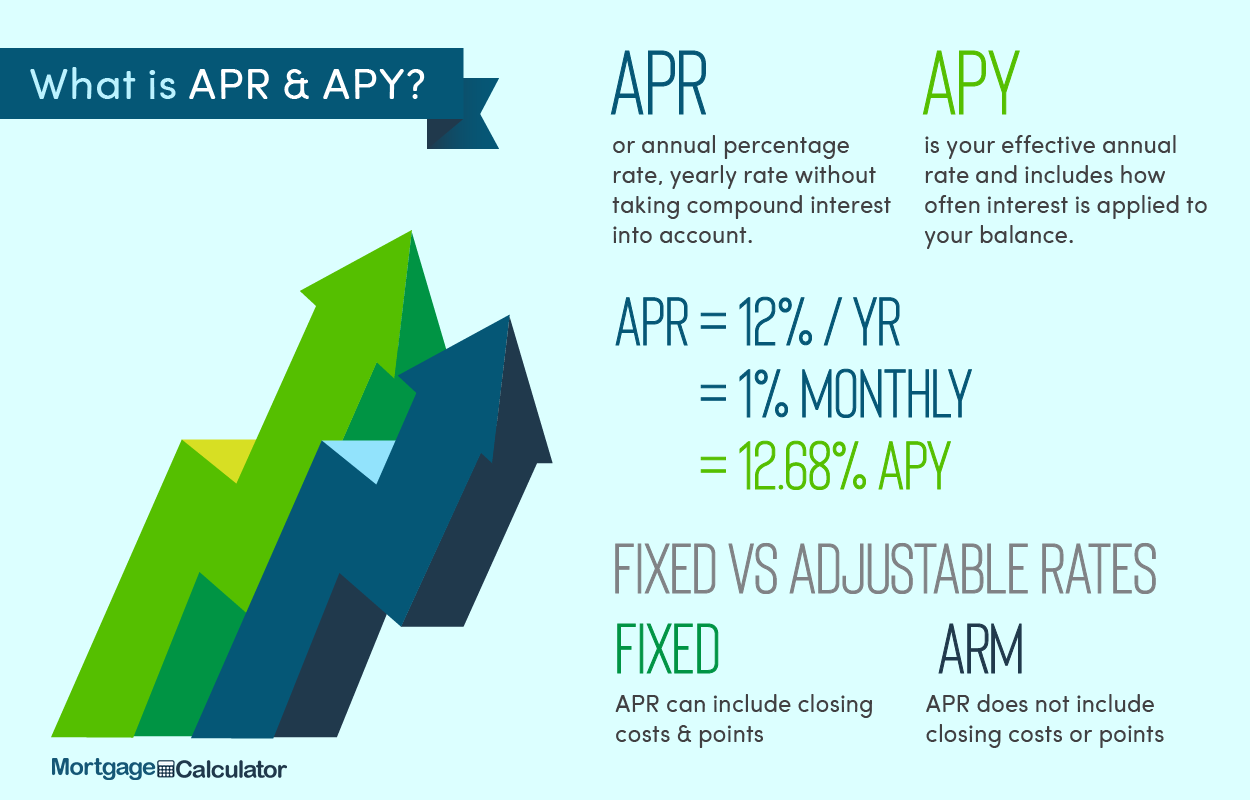

The Annual Percentage Rate (APR) is a broader measure of the cost of borrowing money than the interest rate. It reflects not only the interest rate but also the points, broker fees, and other charges that you pay to get the loan. For this reason, the APR is usually higher than your interest rate. Federal law, specifically the Truth in Lending Act (TILA), requires lenders to disclose the APR so that consumers can compare loans on a level playing field. It essentially “annualizes” the upfront costs of the loan, spreading them out over the full term of the mortgage to show you the effective cost per year.

Nominal Interest Rate vs. APR

The nominal interest rate is the percentage of the principal balance that the lender charges you annually to borrow the money. This rate determines your monthly mortgage payment. However, the interest rate does not account for the administrative costs of setting up the loan.

If you were to look only at the interest rate, you might choose a loan that appears cheaper on the surface but carries heavy upfront fees. The APR closes this gap by factoring in those fees. For example, a 6.5% interest rate loan with $5,000 in fees might have an APR of 6.8%. Another lender might offer a 6.6% interest rate with zero fees, resulting in an APR of 6.6%. In this scenario, despite the higher base interest rate, the second loan is actually the more cost-effective option over the long term.

Components That Make Up Your Mortgage APR

To fully grasp why an APR is calculated the way it is, you must understand the specific financial ingredients that go into the formula. Lenders calculate APR by taking the total interest you will pay over the life of the loan, adding in specific closing costs, and then expressing that total as a yearly rate.

Discount Points and Origination Fees

One of the primary drivers of the difference between an interest rate and an APR is “points.” Mortgage points, also known as discount points, are fees paid directly to the lender at closing in exchange for a reduced interest rate. One point typically costs 1% of the total loan amount. Because points are a cost of obtaining credit, they are included in the APR calculation.

Similarly, origination fees—what the lender charges for processing the loan application, underwriting, and funding—are included. These are essentially the “service fees” for the mortgage, and by including them in the APR, the lender provides transparency regarding the total cost of the transaction.

Mortgage Insurance and Closing Costs

For many borrowers, especially those putting down less than 20%, Private Mortgage Insurance (PMI) is a necessary expense. If the mortgage insurance is a requirement for the loan, the premiums are often factored into the APR. Additionally, other costs such as loan processing fees, document preparation fees, and certain prepaid interest amounts are bundled into the APR calculation.

Costs Not Included in the APR

It is equally important to know what is not included in the APR. Generally, costs that you would incur regardless of the specific lender—such as title insurance, appraisal fees, home inspection fees, and attorney fees—are excluded. These are considered “third-party” costs. Since these costs do not vary based on the lender’s credit terms, they are omitted to keep the APR focused strictly on the cost of the financing itself.

Why APR is the Ultimate Tool for Loan Comparison

The primary reason the APR exists is to protect consumers from “hidden” costs. Without a standardized APR, lenders could advertise incredibly low interest rates while burying exorbitant fees in the fine print of the closing disclosure.

Evaluating Different Loan Offers

When you receive Loan Estimates from multiple banks or mortgage brokers, the APR allows for an “apples-to-apples” comparison. A lender offering a 6.0% rate with $10,000 in closing costs might be a worse deal than a lender offering a 6.25% rate with only $1,000 in costs. By looking at the APR, you can see the cumulative impact of these variables. A lower APR almost always indicates a more cost-effective loan over the full duration of the mortgage.

The Impact of Loan Term on APR

The APR calculation assumes that you will keep the mortgage for its entire term (usually 15 or 30 years). This is a critical distinction for personal finance strategy. Because the upfront fees are spread out over 30 years in the calculation, the APR looks lower for a long-term loan. However, if you plan to sell the home or refinance in five years, the “effective” APR you actually experience will be much higher because those upfront costs weren’t spread out over the full 30 years. When comparing loans, consider how long you intend to stay in the home; if your stay is short-term, a loan with a slightly higher interest rate but much lower upfront fees (and thus a lower APR in the short term) might be preferable.

Factors That Influence Your Specific APR

Not every borrower is offered the same APR. Since the APR is built upon the interest rate and the risk profile of the loan, several personal financial factors come into play.

Credit Score and Debt-to-Income Ratio

Your credit score is perhaps the most significant factor in determining the interest rate a lender offers you. A higher credit score signals to the lender that you are a low-risk borrower, leading to a lower base interest rate and, consequently, a lower APR. Furthermore, your Debt-to-Income (DTI) ratio—the percentage of your monthly gross income that goes toward paying debts—tells the lender if you can afford the monthly payments. A lower DTI can often lead to better terms and lower origination fees.

Down Payment Size and Loan-to-Value Ratio

The amount of equity you have in the home also influences the APR. A larger down payment reduces the Loan-to-Value (LTV) ratio. When the LTV is lower, the lender’s risk is reduced. This can result in the elimination of PMI and a reduction in the interest rate margin the lender charges. In the world of investing and personal finance, a larger down payment is often viewed as a way to “buy down” the long-term cost of debt, which is reflected in a more favorable APR.

Limitations of APR: When It Might Mislead You

While the APR is a powerful tool, it is not a perfect one. There are specific scenarios where relying solely on the APR can lead to a sub-optimal financial decision.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

For a fixed-rate mortgage, the APR is relatively straightforward because the interest rate remains constant. However, for an Adjustable-Rate Mortgage (ARM), the APR is much more complex. The APR on an ARM is calculated based on the initial “teaser” rate and an estimate of how the rate will perform in the future based on current market indices. Because no one can accurately predict where interest rates will be in five or ten years, the APR on an ARM is merely an educated guess. Borrowers should look closely at the “caps” (the maximum the rate can rise) rather than just the APR when considering an ARM.

The Problem with Short-Term Refinancing

As previously mentioned, the APR assumes you will hold the loan for its entire life. If you pay “discount points” to lower your interest rate, your APR will reflect that benefit over 30 years. However, if you refinance the loan two years later, you will have paid those upfront points but will not have stayed in the loan long enough to recoup the costs through the lower monthly payments. In this instance, the APR was a misleading indicator of the loan’s value.

In conclusion, the Annual Percentage Rate is an indispensable metric for anyone navigating the mortgage market. It serves as a beacon of transparency, forcing lenders to reveal the true cost of credit by aggregating interest and fees into a single, digestible percentage. By understanding the components of APR and recognizing its strengths and limitations, you can move forward in your home-buying journey with the confidence of a seasoned financial strategist, ensuring that your mortgage aligns with your long-term wealth-building goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.