For many veterans transitioning from military service to civilian life, the path is often complicated by physical and mental health challenges sustained during their time in uniform. While the Department of Veterans Affairs (VA) provides a sliding scale of disability ratings, these ratings do not always reflect the true economic impact of a disability on a veteran’s ability to earn a living. This is where Total Disability based on Individual Unemployability (TDIU) becomes a critical financial tool.

TDIU is a specific disability benefit that allows the VA to pay veterans at the 100% disability rate, even if their service-connected disabilities do not mathematically add up to a 100% rating. From a financial perspective, TDIU is an income replacement program designed to bridge the gap between a veteran’s actual rating and their total loss of earning capacity. Understanding the nuances of TDIU is essential for any veteran looking to secure their financial future while navigating the constraints of service-connected limitations.

Understanding the Economic Impact of TDIU

The VA’s disability compensation system is fundamentally an economic program. It is designed to compensate veterans for the “average loss of earning capacity” resulting from their service-connected conditions. However, the standard “schedular” rating system—which uses a complex formula to combine multiple disabilities—often falls short for veterans whose specific conditions make working impossible, despite having a combined rating of 60% or 70%.

The Financial Difference Between Schedular Ratings and TDIU

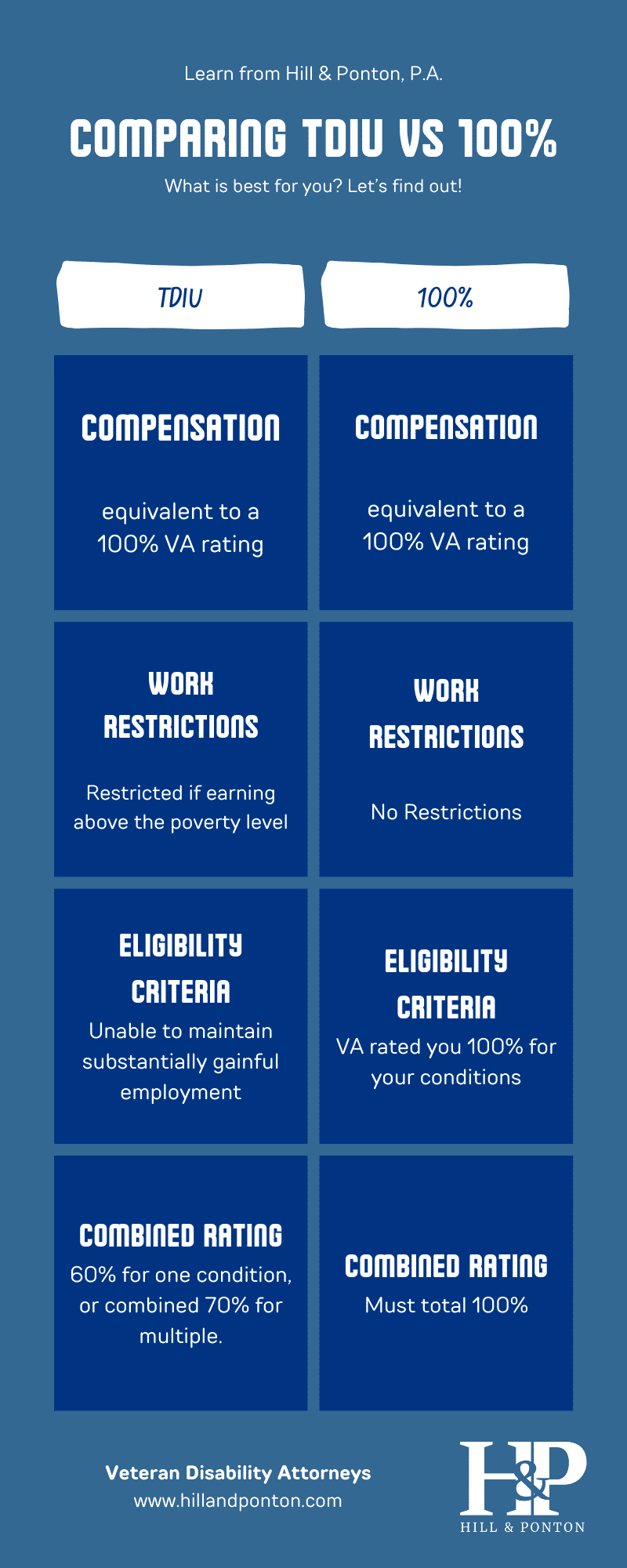

The primary appeal of TDIU is the significant increase in monthly tax-free compensation. For example, the difference between a 70% disability rating and a 100% rating (the TDIU rate) can be over $1,500 per month, depending on the veteran’s dependency status. Over a decade, this translates to more than $180,000 in additional tax-free income.

For a veteran who is unable to maintain a job, this increase is not just a “bonus”; it is the difference between financial instability and a middle-class standard of living. Because VA compensation is adjusted annually for inflation through Cost-of-Living Adjustments (COLA), TDIU acts as a stable, inflation-protected pension that provides a foundation for long-term financial planning.

How TDIU Bridges the Income Gap

In the traditional labor market, a veteran with a 70% rating for Post-Traumatic Stress Disorder (PTSD) or severe back pain might find it impossible to maintain a 40-hour work week. However, under the strict schedular math, they are only compensated for 70% of their “lost” capacity. TDIU acknowledges the economic reality that in the eyes of an employer, a person who cannot work consistently is 100% “economically disabled,” regardless of whether their medical charts say 70% or 100%. By paying at the 100% rate, the VA compensates the veteran for their total inability to compete in the workforce.

Eligibility and the Concept of “Substantially Gainful Employment”

To qualify for TDIU from a financial standpoint, the veteran must prove that their service-connected disabilities prevent them from securing or following “substantially gainful employment.” This term is the cornerstone of the TDIU claim and is defined primarily by economic thresholds.

The 60/40 and 70/40 Rules

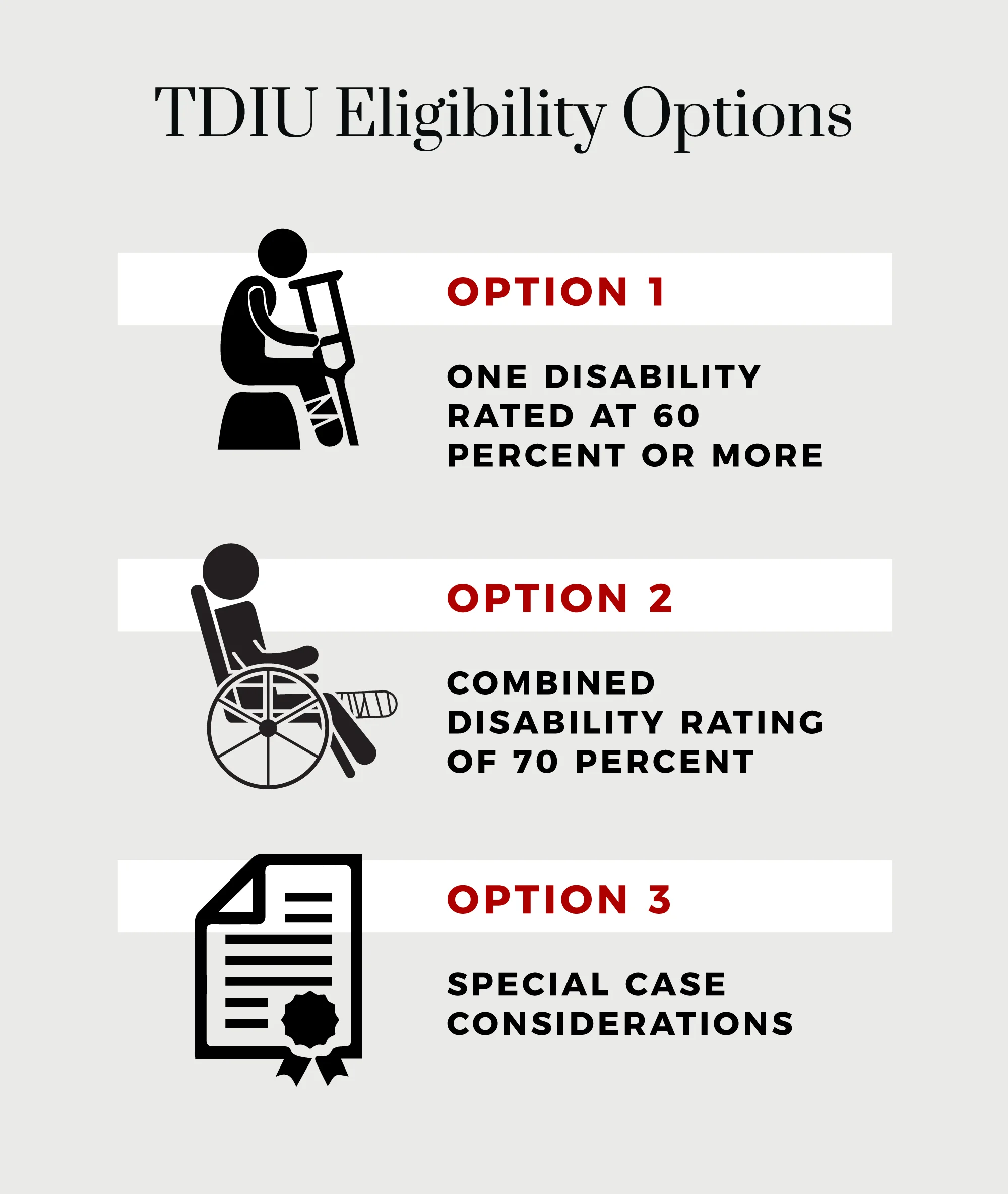

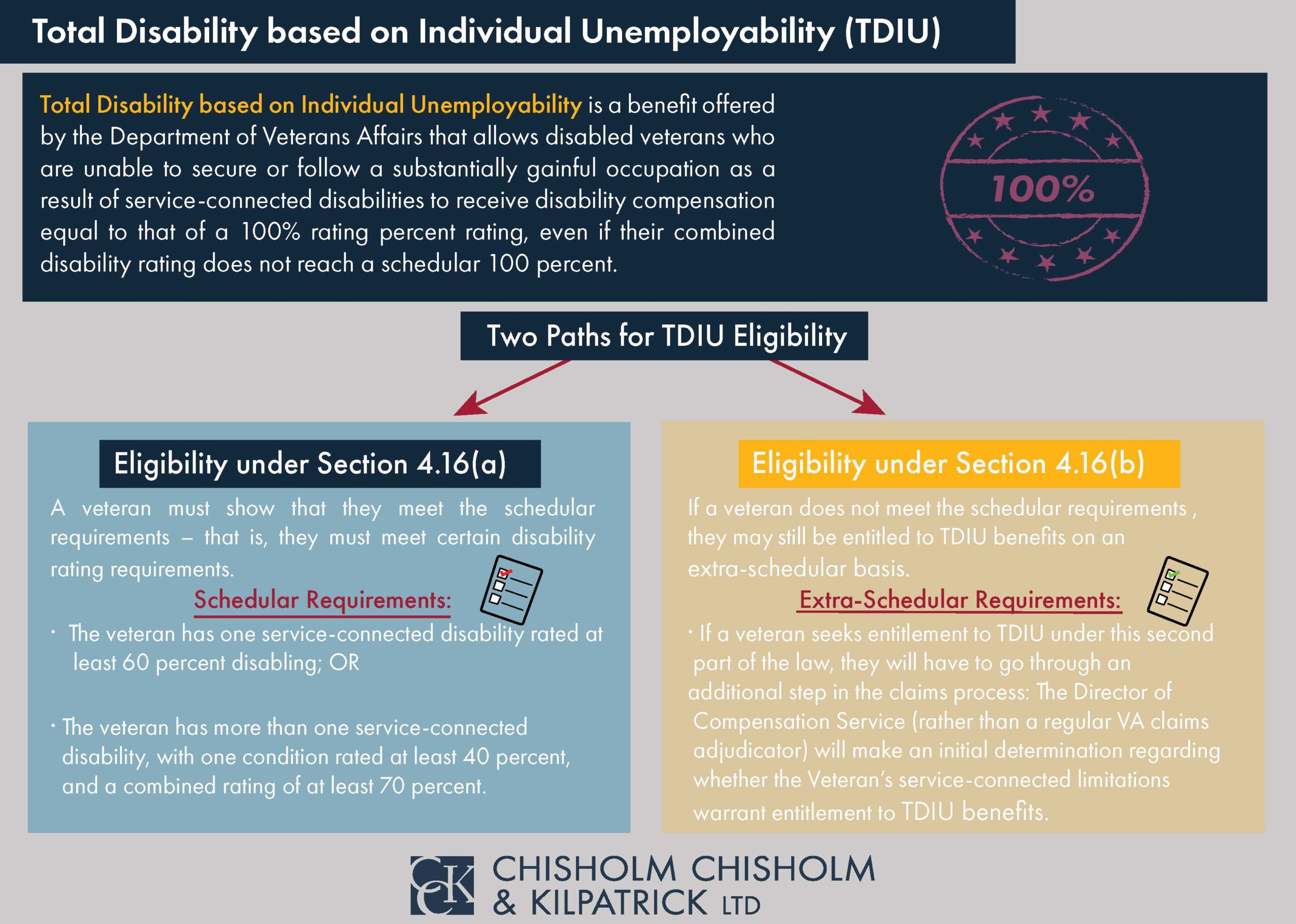

Before the VA evaluates a veteran’s ability to work, they generally look for specific percentage thresholds. To be eligible for “schedular” TDIU:

- The veteran must have one service-connected disability rated at least 60%; OR

- If the veteran has two or more disabilities, at least one must be rated at 40%, with a combined rating of 70% or more.

While “extra-schedular” TDIU exists for those who don’t meet these percentages, the majority of successful financial claims fall under these benchmarks. These thresholds serve as a gateway, ensuring that the veteran’s service-connected conditions are severe enough to plausibly interfere with their financial independence.

Marginal Employment vs. Protected Workshops

A common misconception is that a veteran cannot earn any money while receiving TDIU. This is not strictly true. The VA distinguishes between “substantially gainful employment” and “marginal employment.”

Marginal employment exists if a veteran’s annual earned income does not exceed the federal poverty threshold for a single person. As of 2024, if a veteran earns less than approximately $15,000 a year, the VA generally considers this marginal, and it does not disqualify them from TDIU. Furthermore, employment in a “protected environment” (such as a family business or a sheltered workshop where special accommodations are made that would not be available in the competitive market) may also be overlooked, even if the income exceeds the poverty line. From a business finance perspective, this allows veterans to engage in limited therapeutic work or side hustles without jeopardizing their primary source of income.

The Financial Application Process and Documentation

Securing TDIU is akin to applying for a high-stakes insurance settlement. It requires meticulous documentation of both medical history and vocational limitations. Because the benefit involves a substantial lifelong financial commitment from the government, the VA scrutinizes these applications heavily.

VA Form 21-8940: The Gateway to Increased Compensation

The formal application for TDIU is VA Form 21-8940, Veteran’s Application for Increased Compensation Based on Unemployability. This document is essentially a financial and vocational history report. It requires the veteran to list their employment history for the five years prior to their last day of work, as well as any disability-related reasons for leaving those positions.

For veterans, treating this form as a professional business disclosure is vital. Providing clear data on lost wages, frequent medical leaves, and failed attempts at vocational rehabilitation helps build the economic case that the veteran is no longer a viable candidate for the competitive labor market.

Vocational Expert Testimony and Financial Evidence

In many contested TDIU cases, the difference between approval and denial lies in the use of a Vocational Expert (VE). Just as a financial auditor reviews a company’s books, a VE reviews a veteran’s medical records and employment history to determine if there are any jobs in the national economy they can perform.

A vocational report translates medical symptoms into economic limitations. For instance, a doctor might note “chronic back pain,” but a VE will translate that into “inability to sit for more than 20 minutes, necessitating frequent unscheduled breaks that would lead to termination in 95% of available sedentary roles.” This type of evidence is powerful because it addresses the financial core of the TDIU claim: the loss of earning capacity.

Long-Term Wealth Management and Ancillary Benefits

Winning a TDIU claim is a transformative financial event. It moves a veteran into the highest tier of VA benefits, which brings a suite of secondary financial advantages that extend beyond the monthly check.

Tax-Free Status and Its Role in Retirement Planning

One of the most significant financial aspects of TDIU—and all VA disability compensation—is that it is 100% free from federal and state income taxes. When comparing a TDIU payment to a civilian salary, one must calculate the “grossed-up” value. A $3,700 monthly tax-free payment is equivalent to a taxable salary of roughly $55,000 to $65,000 per year, depending on the state of residence.

For long-term financial planning, this tax-free income provides a unique advantage. Since it is not earned income (W-2 wages), it cannot be used to contribute to a traditional or Roth IRA. However, it provides a guaranteed “floor” of liquidity that allows a veteran to manage other investments more aggressively or ensure that their mortgage and essential expenses are covered regardless of market volatility.

Additional Benefits: Health Care, Education, and State Tax Exemptions

TDIU status often unlocks “P&T” (Permanent and Total) status, which triggers a cascade of additional financial benefits:

- CHAMPVA: High-quality health insurance for the veteran’s spouse and children, significantly reducing household insurance premiums.

- Chapter 35 DEA: Education assistance for dependents, providing monthly stipends for college or vocational training, which can save a family tens of thousands of dollars in tuition costs.

- Property Tax Exemptions: Many states offer partial or total property tax exemptions for veterans rated at 100% or receiving TDIU. In high-tax states, this can save a veteran $5,000 to $10,000 annually.

- Commissary and Exchange Access: Unlimited access to tax-free shopping on military installations.

Conclusion: Securing the Financial Future

TDIU is more than just a medical rating; it is a vital economic safety net. It recognizes that for some veterans, the true cost of their service is the total loss of their ability to compete in the workforce. By understanding the eligibility requirements, the definition of gainful employment, and the strategic importance of vocational evidence, veterans can successfully navigate the VA system to secure a 100% compensation rate.

In the broader context of personal finance, TDIU provides the stability necessary for a veteran to live with dignity despite their disabilities. It offers a tax-advantaged, inflation-protected stream of income that supports not only the veteran but also their family, ensuring that the sacrifice made during military service does not result in a lifetime of financial hardship. For those who qualify, TDIU is the single most important financial milestone in their post-service life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.