In the intricate landscape of urban housing, the concept of rent stabilization stands as a critical mechanism designed to balance housing affordability with property ownership. For millions of tenants, it offers a bulwark against unchecked rent hikes, providing a degree of financial predictability and stability in an often volatile real estate market. For landlords and investors, however, it represents a complex set of regulations that profoundly impact revenue streams, property valuation, and investment strategies. Understanding rent stabilization, therefore, is not merely a legal exercise but a deep dive into its multifaceted financial implications for all stakeholders involved.

At its core, rent stabilization is a form of rent control, typically implemented in cities experiencing housing shortages and rapidly escalating rents. Its primary goal is to ensure that a significant portion of the housing stock remains affordable, particularly for middle- and lower-income residents, preventing displacement and fostering community stability. Unlike strict rent control, which might cap rents at historical levels and allow minimal increases, rent stabilization permits landlords to raise rents annually by a certain percentage, often determined by a municipal housing board or tied to economic indicators like the Consumer Price Index. This nuanced approach attempts to protect tenants from predatory pricing while still allowing landlords some flexibility to cover increasing operating costs. This article will explore the financial mechanics, eligibility, economic implications, and strategic financial planning within a rent-stabilized environment, exclusively through the lens of personal and business finance.

The Financial Mechanics of Rent Stabilization

The financial impact of rent stabilization is profound, directly influencing the income and expenses of both tenants and property owners. It introduces a structured framework for rent adjustments, moving away from the purely market-driven pricing seen in unregulated properties.

Understanding Rent Ceilings and Annual Increases

The most defining feature of rent stabilization is the imposition of rent ceilings and prescribed annual increases. In jurisdictions with rent stabilization laws, a Rent Guidelines Board (RGB) or similar body typically convenes annually to determine the permissible percentage increase for lease renewals. These increases are often differentiated based on lease term (e.g., a higher percentage for a two-year lease renewal versus a one-year renewal). The factors considered by these boards can include the Consumer Price Index (CPI), operating and maintenance costs for property owners, vacancy rates, and the overall economic health of the region.

For tenants, this mechanism translates into significant financial predictability. Knowing that their rent will only increase by a regulated percentage each year allows for more accurate long-term budgeting and financial planning. It shields them from the abrupt, substantial rent increases that can occur in a fully deregulated market, which often force residents to relocate due to unaffordability. This stability can represent substantial savings over several years, allowing tenants to allocate more of their income towards other financial goals, such as saving for a down payment, retirement, or educational expenses, instead of having a disproportionate amount absorbed by housing costs.

Conversely, for landlords, these rent ceilings impose a clear constraint on potential income growth. While they can implement annual increases, these are often below the prevailing market rate, especially in popular or rapidly appreciating areas. This limitation can compress profit margins, particularly if operating expenses—such as property taxes, insurance, utilities, and maintenance costs—rise at a faster rate than the permissible rent increases. It forces landlords to operate with greater financial discipline and seek efficiencies to maintain profitability.

Impact on Tenant Finances: Affordability and Budgeting

For tenants, rent stabilization is a powerful tool for enhancing personal financial health. The primary benefit is sustained affordability. In cities where median rents can consume a significant portion of household income, stabilized units provide a crucial financial anchor. This stability allows individuals and families to maintain a consistent housing expense, which is the largest single expenditure for most households.

This predictable expense facilitates effective budgeting and financial planning. Tenants can confidently project their housing costs for the next year or two, making it easier to save, invest, or pay down debt. Without the constant threat of a massive rent hike, tenants experience reduced financial stress and greater housing security. This security can indirectly foster economic growth within households, as disposable income is less volatile and more available for consumption or wealth building. Moreover, it protects against the severe financial disruption and potential homelessness that can arise from sudden, unaffordable rent increases, acting as a crucial social safety net.

Impact on Landlord Finances: Revenue and Property Valuation

From a landlord’s perspective, rent stabilization presents a unique set of financial challenges and opportunities. The most immediate impact is on revenue generation. Capped rent increases mean that the income from rent-stabilized units will likely grow more slowly than market-rate units, especially in appreciating markets. This can lead to lower cash flow and potentially a reduced return on investment (ROI) compared to unregulated properties.

This revenue constraint necessitates a more strategic approach to property management and financial oversight. Landlords must meticulously manage expenses, seek out cost-effective maintenance solutions, and look for opportunities to increase value through permissible avenues. For instance, in some jurisdictions, landlords can apply for rent increases above the annual guidelines for major capital improvements (MCIs) that benefit all tenants (e.g., new roof, boiler system) or individual apartment improvements (IAIs) when an apartment becomes vacant and is substantially renovated. However, the process for approving these increases is often bureaucratic and capped, limiting their overall financial impact.

Furthermore, rent stabilization can affect property valuation. Properties with a significant number of rent-stabilized units may trade at lower capitalization rates (cap rates) than comparable market-rate properties, reflecting the limitations on future income growth. This can impact a landlord’s ability to secure financing or refinance loans, as lenders may view these properties as carrying higher risk due to restricted income potential. Investors in rent-stabilized properties often focus on long-term appreciation of the underlying real estate rather than aggressive short-term cash flow generation, making it a distinct investment niche requiring specialized financial due diligence.

Eligibility and Navigating the System

Understanding which properties and tenants are covered by rent stabilization laws is crucial for both parties, as it dictates financial rights and responsibilities. The specifics vary significantly by jurisdiction, but general principles apply.

Criteria for Rent-Stabilized Units

The eligibility for rent stabilization is typically tied to the age and size of the building, and its location. For example, in New York City, buildings constructed before a certain date (e.g., January 1, 1974) with six or more units are often subject to rent stabilization. Newer buildings or smaller buildings might be exempt. Some localities also have specific geographic zones where stabilization applies.

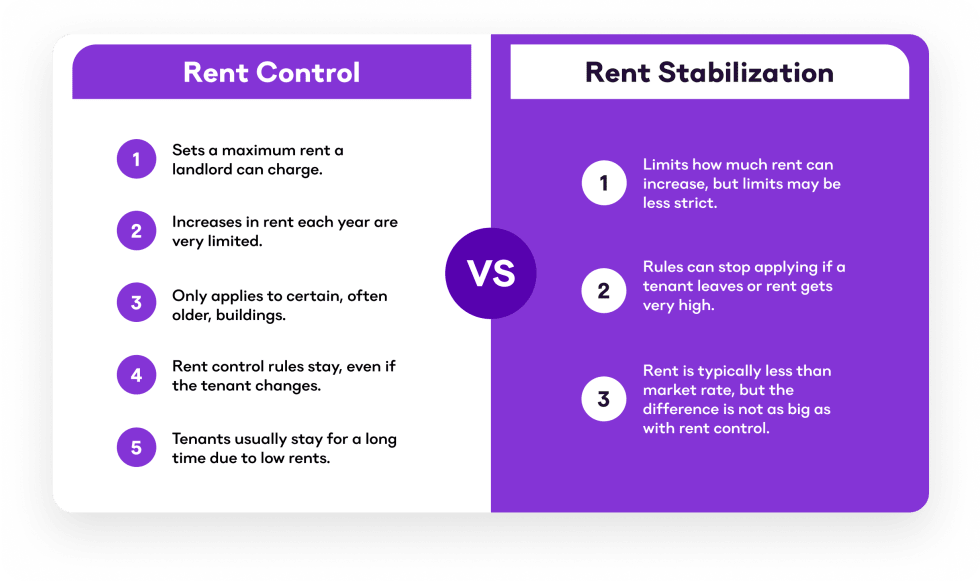

It’s vital to differentiate between “rent control” and “rent stabilization.” Rent control, the older and stricter form, usually applies to buildings constructed much earlier and allows for very minimal rent increases. Many rent-controlled units have transitioned to rent stabilization over time. Rent stabilization is more widespread and often seen as a more flexible regulatory framework. Tenant income limits are generally not a direct criterion for rent stabilization itself, meaning tenants of any income level can reside in a stabilized unit if they meet other tenancy requirements. The focus is on the unit and the building, rather than the individual tenant’s financial status.

Rights and Responsibilities for Tenants

For tenants, living in a rent-stabilized unit confers substantial financial and legal protections. The most significant right is the right to a lease renewal, meaning landlords cannot refuse to renew a lease without specific, legally sanctioned “good cause” (e.g., non-payment of rent, nuisance, owner occupancy). This protection provides immense housing security and prevents arbitrary evictions aimed at raising rents.

Tenants also have the right to specific services and maintenance, and landlords are obligated to maintain the premises in a habitable condition. If services are reduced or conditions deteriorate, tenants may have legal and financial recourse, potentially including rent reductions through administrative channels. Furthermore, tenants have the right to challenge rent overcharges, where a landlord charges more than the legally permissible rent. Financial tools and resources are often available through local housing authorities or tenant advocacy groups to help tenants understand their rights and pursue remedies, which can result in significant financial recovery for past overpayments.

Obligations and Challenges for Landlords

Landlords of rent-stabilized properties face a stringent set of obligations. Their primary duty is to adhere strictly to the rent increase limits set by the governing body. Failing to do so can result in severe penalties, including fines and orders to refund overcharged rent. They must also maintain essential services and property conditions, as failure can lead to rent reductions or legal action.

One of the significant challenges for landlords is navigating the legal frameworks for requesting rent adjustments for capital improvements. The process for Major Capital Improvements (MCIs) or Individual Apartment Improvements (IAIs) is often complex, requiring extensive documentation, approvals from housing agencies, and strict adherence to cost recovery schedules. This adds an administrative burden and can delay the financial returns on property investments. Landlords must also manage a higher level of financial transparency, as they are often required to disclose rent histories and abide by specific leasing and record-keeping requirements.

Economic Implications and Market Dynamics

The presence of rent stabilization laws fundamentally alters the economic dynamics of local housing markets, creating a tension between affordability goals and market efficiency.

The Affordability vs. Supply Debate

Rent stabilization is championed as a vital tool for promoting housing affordability, preventing displacement, and preserving economic diversity in urban centers. By capping rent increases, it helps low- and middle-income residents remain in their communities, contributing to local economies and preventing the socio-economic homogenization of neighborhoods.

However, critics argue that rent stabilization can have unintended negative consequences on housing supply and quality. From an economic perspective, by limiting the potential for profit, rent stabilization can deter new construction of rental units, exacerbating housing shortages in the long run. Developers may choose to build in unregulated areas or pursue other types of real estate development, such as condominiums. Furthermore, some economists argue that restricted rental income can disincentivize landlords from investing adequately in maintenance and upgrades for existing stabilized units, leading to a deterioration of the housing stock over time. This creates a complex financial trade-off: immediate affordability for current tenants versus potential long-term impacts on housing availability and quality.

Investment Considerations in Stabilized Markets

For real estate investors, rent-stabilized markets present a distinct investment profile. The financial characteristics of these properties — lower but predictable cash flow, potential for slower rent growth, and extensive regulatory oversight — lead to different valuation metrics and investment strategies. Investors typically seek properties with strong underlying asset value (e.g., prime location, potential for future redevelopment under different zoning) and understand that their returns will be more modest and long-term oriented compared to market-rate properties.

Due diligence in these markets is paramount. Prospective buyers must meticulously examine rent rolls, understanding the proportion of stabilized units, the legal registered rents, and the potential for legal increases through IAIs or MCIs. They must also factor in higher compliance costs and potential legal expenses associated with navigating the regulatory environment. Investment in stabilized properties often suits institutional investors or experienced landlords who have a deep understanding of local housing laws and a long-term capital appreciation strategy, rather than those seeking rapid cash flow or quick flips.

Regional Variations and Future Trends

The application and impact of rent stabilization vary widely across different cities and states. Jurisdictions like New York City, San Francisco, and Los Angeles have some of the most comprehensive and long-standing rent stabilization laws, each with its unique nuances and historical context. Other cities or states have recently adopted or expanded rent control/stabilization measures (e.g., Oregon, California), often in response to escalating housing crises.

The future of rent stabilization is subject to ongoing political and social pressures. Advocates continue to push for stronger tenant protections and expansion of stabilization, viewing it as essential for social equity and economic justice. Opponents argue for deregulation, citing concerns about market distortions and impacts on property values and new construction. These debates often revolve around the financial implications for various segments of the population and the broader economy, indicating that financial advisors, property managers, and real estate professionals must stay abreast of evolving legislation and its potential financial ramifications.

Financial Planning Strategies in a Stabilized Environment

Successfully navigating a rent-stabilized environment requires specific financial planning strategies for both tenants and landlords.

For Tenants: Maximizing Your Financial Advantage

Rent stabilization offers a unique opportunity for tenants to optimize their personal finances. The stability of housing costs can free up significant portions of income for savings and investments. Tenants should leverage this predictability to build emergency funds, contribute consistently to retirement accounts (e.g., 401k, IRA), or save for major life goals like education or homeownership (in a different market, perhaps). The difference between a stabilized rent and a market-rate rent can be viewed as “found money” that, if strategically invested, can substantially accelerate wealth accumulation.

Furthermore, tenants should be proactive in understanding their rights. This includes knowing the legal registered rent for their unit, understanding the permissible annual increases, and being aware of their rights regarding maintenance and services. Ignorance can be costly, as tenants might unknowingly pay overcharges or accept substandard living conditions. Utilizing free or low-cost resources from tenant advocacy groups or city housing agencies can help tenants protect their financial interests and ensure they are not being exploited.

For Landlords: Adapting Business Models

For landlords, adapting to a rent-stabilized environment means adopting a more disciplined and long-term-oriented business model. Financial planning should focus on maximizing efficiency, controlling operational costs, and strategically investing in the property. This includes:

- Efficient Property Management: Streamlining maintenance, utility consumption, and administrative tasks to minimize expenses.

- Strategic Capital Improvements: Identifying and executing major capital improvements that qualify for rent increases and genuinely enhance property value and tenant experience. This requires careful financial modeling to ensure a positive ROI.

- Long-Term Portfolio Management: Diversifying investments across various property types and markets, understanding that rent-stabilized properties may serve a specific role within a broader portfolio (e.g., stable, albeit lower, cash flow).

- Navigating Vacancy: If permitted by law, maximizing legal rent increases upon vacancy (vacancy decontrol or vacancy bonuses) while ensuring compliance with all regulations.

Financial forecasting for rent-stabilized properties must be conservative, factoring in potential slow rent growth and rising expenses. Landlords might also explore tax incentives or subsidies available for properties that provide affordable housing.

The Role of Financial Professionals

Given the complexities, both tenants and landlords can benefit significantly from consulting financial professionals. Real estate lawyers specializing in rent stabilization are invaluable for understanding legal rights and obligations, challenging overcharges, or navigating the MCI/IAI approval process. Financial advisors can help tenants integrate their stable housing costs into a comprehensive financial plan, advising on investment strategies and wealth building. For landlords, property managers with expertise in rent-stabilized properties can handle day-to-day operations and compliance, while real estate consultants can provide insights into market valuation and investment strategies specific to regulated assets. These experts can help stakeholders optimize their financial outcomes and mitigate risks within the framework of rent stabilization.

Conclusion

Rent stabilization is a multifaceted policy that profoundly impacts the financial lives of millions of urban residents and property owners. From the tenant’s perspective, it is a crucial financial safeguard, providing housing security, predictable expenses, and the ability to better plan for their financial future. It directly contributes to personal financial stability, allowing for greater savings and reduced economic stress. For landlords, it presents a distinct business challenge, imposing limitations on income growth and necessitating a more disciplined, long-term financial strategy focused on efficiency, strategic improvements, and rigorous compliance.

The ongoing debate surrounding rent stabilization highlights its complex economic implications, pitting the goal of affordability against concerns about housing supply and property investment incentives. As cities continue to grapple with housing crises, the role of rent stabilization, and its evolving financial ramifications, will remain a central topic. Ultimately, understanding “what is rent stabilized” transcends a simple definition; it requires a comprehensive appreciation of its intricate financial mechanics, its impact on budgeting and investment decisions, and the strategic planning necessary for both tenants and landlords to thrive within this unique housing environment. Informed financial decision-making, supported by expert guidance, is key to navigating its complexities successfully.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.