For many homeowners, the journey of mortgage repayment feels like a rigid, unchangeable contract. You sign the papers, agree to an interest rate, and follow an amortization schedule that stretches across 15 or 30 years. However, life rarely follows a linear path. Perhaps you have come into a sudden windfall, such as an inheritance, a substantial work bonus, or the proceeds from the sale of another asset. When you find yourself with a large lump sum of cash, the traditional instinct is to pay down your mortgage principal. But while paying down the principal is a wise financial move, it often leaves you with the same monthly payment—just a shorter timeline to completion. This is where mortgage recasting becomes a powerful, yet often overlooked, financial tool.

Understanding the Mechanics of Mortgage Recasting

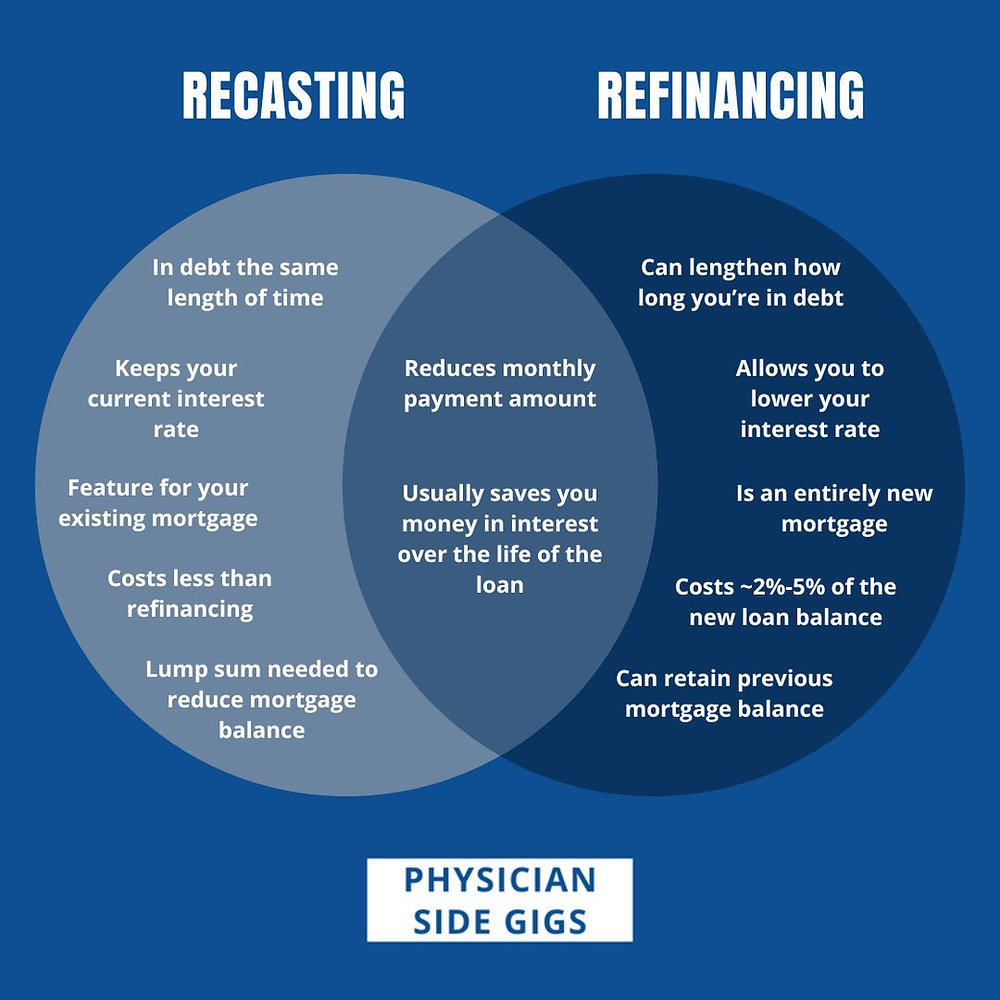

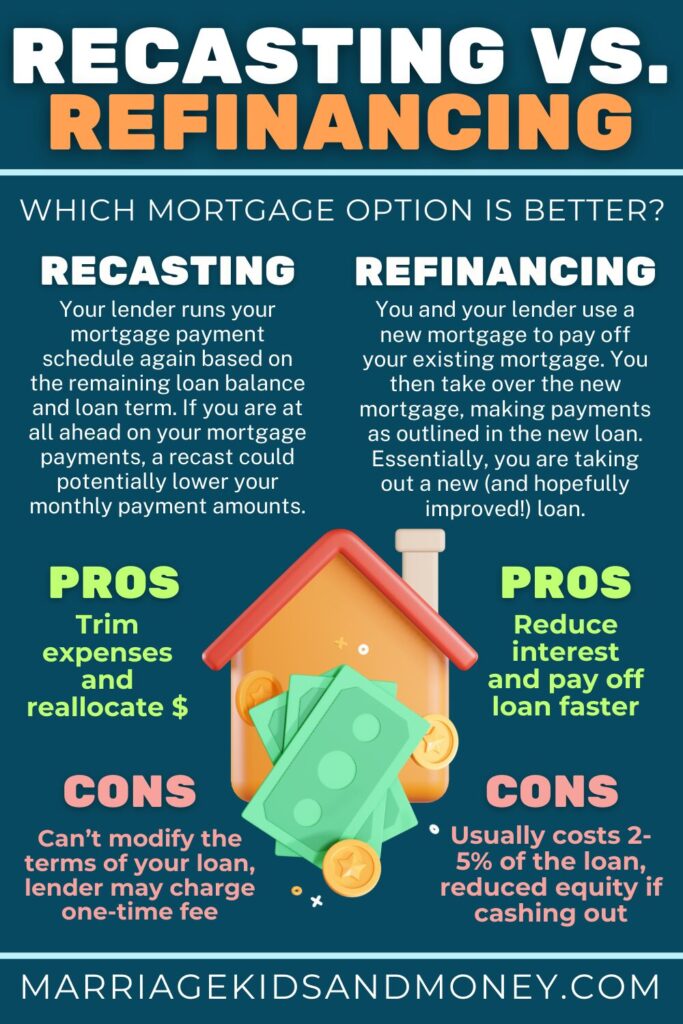

At its core, mortgage recasting—also known as a re-amortization—is a process where a lender recalculates your monthly principal and interest payments based on your new, lower principal balance. It is important to distinguish this from refinancing. When you refinance, you are taking out an entirely new loan, which involves new closing costs, a new interest rate, and an entirely new credit underwriting process. Recasting, conversely, keeps your original loan terms—including your interest rate and the remaining time on your loan—intact.

How the Process Works

When you make a significant lump-sum payment toward your mortgage principal, your total debt decreases. However, without a formal recast, your monthly payment amount remains exactly the same as it was before the payment; you are simply paying off the loan faster because a larger portion of your regular monthly payment is now directed toward the principal rather than interest.

When you request a recast, you are asking the lender to take that new, smaller principal balance and spread it out over the remaining months of your original loan term. Because the balance is lower, the bank recalculates the math. The result is a significantly lower monthly mortgage payment. It is a mathematical adjustment that offers immediate relief to your monthly cash flow without requiring you to go through the arduous and expensive process of qualifying for a new loan.

Eligibility and Lender Requirements

Not every mortgage is eligible for recasting. Most conventional loans, particularly those sold to Fannie Mae or Freddie Mac, generally allow for recasting, but the decision ultimately rests with your loan servicer. Government-backed loans, such as FHA, VA, and USDA loans, typically do not allow for recasting.

Furthermore, lenders usually require a minimum lump-sum payment to initiate the process, often ranging from $5,000 to $20,000, depending on the institution. You must also have a strong payment history; if you are currently delinquent or have a history of missed payments, the bank is unlikely to grant a request for re-amortization. Always start by calling your loan servicer and asking if they offer “re-amortization” or “recasting” services, and be prepared to pay a modest administrative fee, which typically ranges from $150 to $500.

The Strategic Advantages of Recasting

Why would you want to lower your monthly payment if you already have the capital to pay down your debt? The answer lies in flexibility and the optimization of your broader financial portfolio.

Enhancing Monthly Cash Flow

For many households, the biggest monthly burden is the mortgage payment. By recasting your loan, you effectively “buy” more monthly freedom. The reduced monthly obligation can be redirected toward other financial goals. For example, if your mortgage payment drops by $400 or $500 a month after a recast, that capital can be diverted into high-yield savings accounts, retirement funds like an IRA or 401(k), or even used to pay down higher-interest consumer debt like credit cards or personal loans.

Maintaining Your Interest Rate

One of the most compelling reasons to choose recasting over refinancing is the protection of your current interest rate. If you locked in a low mortgage rate several years ago—perhaps 3% or 4%—refinancing in a higher-rate environment would be a catastrophic financial move. You would effectively be trading a cheap, long-term debt for a much more expensive one just to access your equity or lower your payment. Recasting allows you to keep your advantageous interest rate while still benefiting from a lower monthly payment, making it the superior choice in a rising interest rate environment.

Avoiding Closing Costs

Refinancing is expensive. Between appraisal fees, title insurance, loan origination fees, and various administrative costs, refinancing can easily cost several thousand dollars. These costs are often folded into the loan, meaning you pay interest on your closing costs for the next 30 years. Recasting, by comparison, involves a negligible administrative fee. Because it does not involve a new loan, there are no appraisals, no credit pulls, and no title insurance requirements. It is an efficient, cost-effective adjustment to your existing financial commitment.

When Recasting Makes Financial Sense

Recasting is not a universal solution for every homeowner, but it shines in specific financial scenarios. Understanding the “when” is just as important as understanding the “how.”

Planning for Retirement

As homeowners approach retirement, the focus often shifts from wealth accumulation to cash flow management. Carrying a large mortgage payment on a fixed retirement income can be stressful. If you have a lump sum of cash available—perhaps from a severance package, a matured investment, or the sale of a vacation home—recasting allows you to lower your fixed costs permanently. This creates a more sustainable budget for your golden years without forcing you to sell your home or move to a less expensive property.

Managing Life Transitions

Significant life events often necessitate a shift in financial strategy. A divorce, a career change, or the decision for one spouse to stay home with children can all lead to a tighter monthly budget. If you find yourself in a position where your income has changed but your assets remain, recasting serves as a tool to adjust your primary housing expense to match your new reality, providing a buffer that could prevent the need to downsize prematurely.

Comparing Alternatives: The Opportunity Cost

Before committing to a mortgage recast, it is essential to consider the opportunity cost. Every dollar you put toward your mortgage is a dollar that cannot be invested elsewhere.

Investing vs. Paying Down Debt

If you have a mortgage at 3.5% interest, you must weigh the benefit of “earning” that 3.5% return (by avoiding interest payments) against the potential return of the stock market or other investments. Historically, a diversified equity portfolio may yield returns significantly higher than your mortgage interest rate over the long term. If you have a high risk tolerance and a long time horizon, investing your lump sum might lead to greater net worth growth than the interest savings realized through recasting.

Liquidity Considerations

Once you pay that lump sum into your mortgage principal, that money is effectively “trapped” in your home’s equity. Unless you take out a Home Equity Line of Credit (HELOC) or a cash-out refinance later—which involves interest and potential fees—you cannot easily access that cash for an emergency. Recasting reduces your monthly payment, which improves your monthly liquidity, but it does not provide you with a safety net of cash. Ensure you have an adequate emergency fund (three to six months of expenses) before you commit your surplus capital to a mortgage principal reduction.

In conclusion, recasting is a sophisticated tool for homeowners who possess surplus capital and wish to optimize their cash flow without disturbing their original, favorable loan terms. It is the surgical alternative to the “sledgehammer” approach of refinancing. By understanding your lender’s requirements, calculating the impact on your monthly budget, and carefully weighing the opportunity costs of your capital, you can utilize mortgage recasting to create a more resilient and manageable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.