Realtor commission represents the fee paid to real estate agents for their services in facilitating the sale or purchase of a property. Far from being a simple flat fee, this payment is a cornerstone of the real estate industry’s financial model, directly impacting the budgets of both buyers and sellers. Understanding how these commissions are structured, calculated, and ultimately paid is crucial for anyone navigating the complex world of property transactions. It’s a significant financial outlay that funds the expertise, marketing efforts, negotiation skills, and administrative tasks real estate professionals provide to ensure a successful deal.

Decoding Realtor Commission: The Fundamentals

At its core, realtor commission is a percentage of the property’s final sale price. This percentage is not standardized by law but is typically negotiated between the seller and their listing agent at the outset of the listing agreement. Once agreed upon, this total commission is then divided, usually between the seller’s agent (listing agent) and the buyer’s agent (selling agent). This cooperative commission model incentivizes buyer’s agents to show properties listed by other brokers, creating a broad market for sellers.

The Buyer’s Agent vs. Seller’s Agent Split

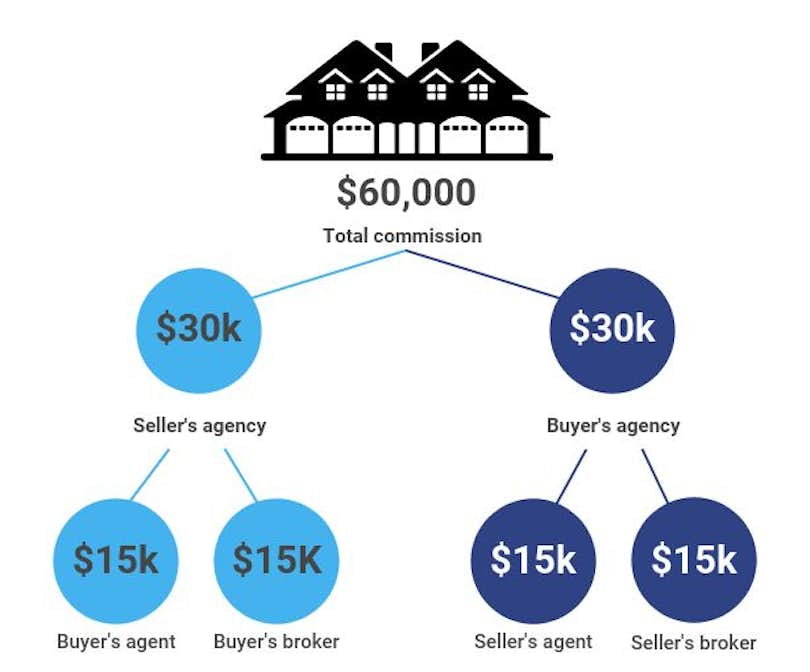

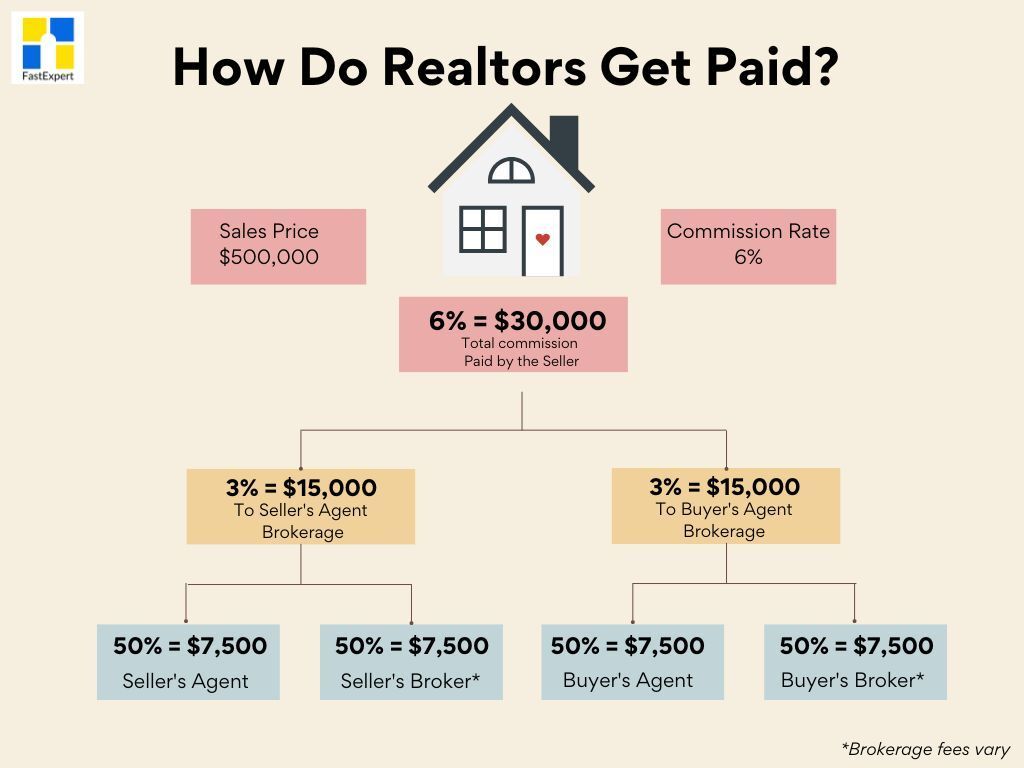

The most common arrangement involves a split of the total commission. For instance, if the agreed-upon commission is 5% or 6% of the sale price, this amount is generally divided equally or near-equally between the brokerage representing the seller and the brokerage representing the buyer. So, a 6% commission might see 3% go to the listing broker and 3% to the buyer’s broker. Each of these brokerages then pays a portion of their share to the individual agent who handled the transaction, based on their individual contract with the brokerage. This split underscores the collaborative financial ecosystem that drives most real estate transactions, ensuring both sides of the deal are professionally represented.

How Commissions are Calculated

The calculation is straightforward: multiply the final sale price by the agreed-upon commission rate. For example, on a $400,000 home with a 6% commission, the total commission would be $24,000. This $24,000 would then be split between the two brokerages involved. It’s vital to remember that this commission is applied to the gross sale price, not after any deductions or concessions. This clear financial mechanism ensures transparency in the primary fee structure, though other closing costs and fees will also apply.

Who Pays and When: Understanding the Financial Flow

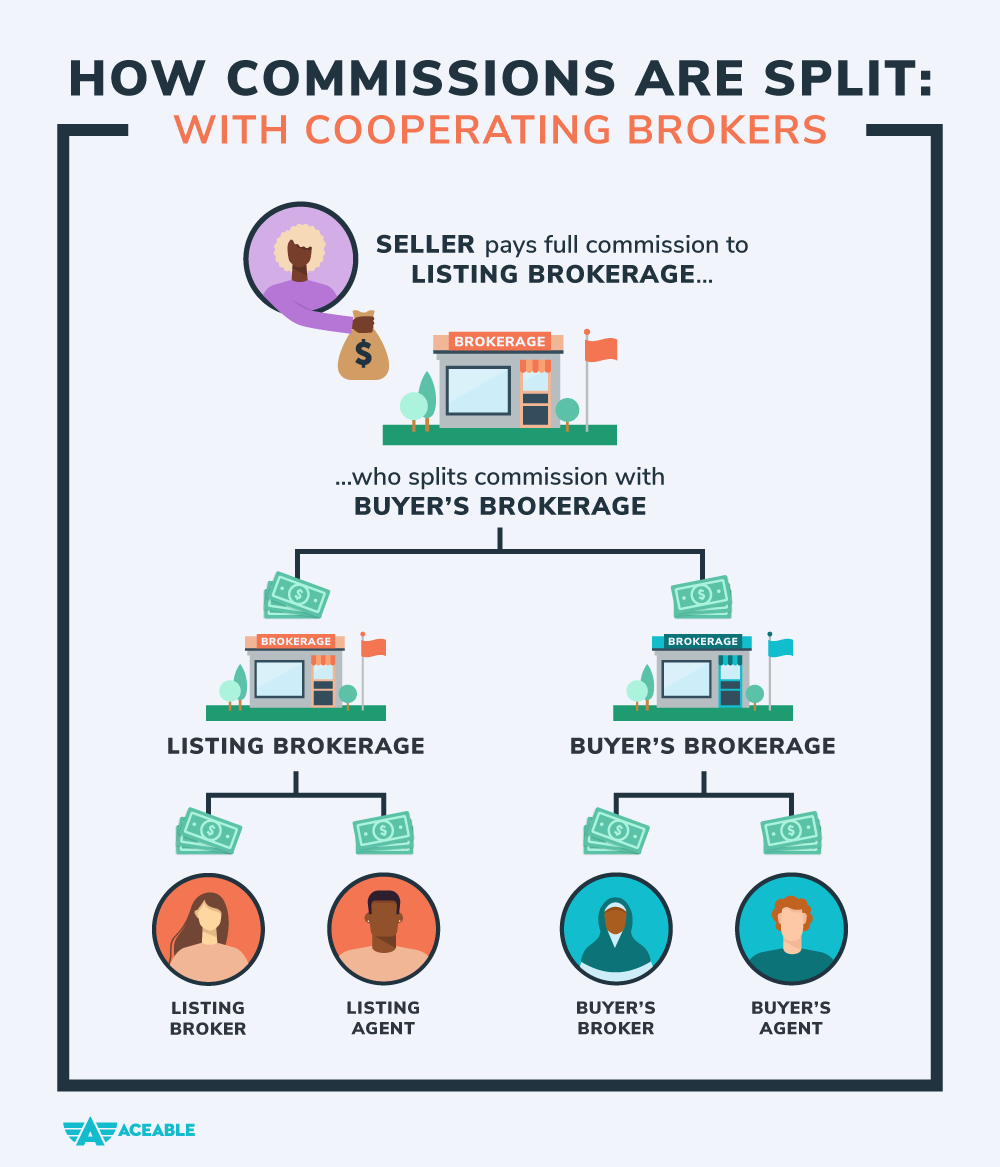

One of the most common misconceptions about realtor commission revolves around who ultimately bears the cost. While the financial impact is felt by both parties, the mechanics of payment are typically directed through the seller.

The Seller’s Financial Responsibility

In almost all residential real estate transactions, the seller is contractually obligated to pay the entire commission for both their agent and the buyer’s agent. This payment is typically stipulated in the listing agreement signed between the seller and their real estate brokerage. The commission is not paid upfront but rather at the closing table, deducted directly from the sale proceeds. This means that the seller’s net proceeds from the sale are reduced by the total commission amount, along with other closing costs such as transfer taxes, legal fees, and title insurance. From a financial planning perspective, sellers must factor this significant expense into their expected net proceeds when pricing their home and forecasting their financial outcome.

Indirect Costs for Buyers

While buyers do not directly write a check for the realtor commission, they indirectly contribute to it. The commission is built into the sale price of the home. When a seller prices their property, they invariably consider the commission they will owe, aiming to set a price that covers their desired net profit after all expenses. Therefore, a higher commission rate effectively means a slightly higher list price, which the buyer ultimately pays. This dynamic highlights the interconnected financial interests in a real estate transaction, where the buyer’s purchase price implicitly incorporates the seller’s cost of sale.

The Closing Statement: Where It All Comes Together

The “Settlement Statement” or “Closing Disclosure” is the definitive financial document that itemizes all costs and credits for both the buyer and the seller. This document transparently lists the total commission paid, detailing how it’s distributed among the various parties. For sellers, it will show a debit for the full commission amount. For buyers, while there won’t be a direct commission debit, the purchase price itself reflects this embedded cost. Reviewing this document carefully is crucial for both parties to understand the exact financial implications of their transaction.

Factors Influencing Commission Rates

While industry averages for realtor commission often hover around 5-6%, these figures are not static or legally mandated. Several factors can influence the commission rate a seller agrees to pay, reflecting market dynamics, property specifics, and the scope of services provided.

Standard Rates vs. Flexibility

The concept of a “standard” commission rate is more of an industry custom than a rule. In competitive markets, agents might be more willing to negotiate their rates to secure a listing. Conversely, in hot seller’s markets, sellers might be less inclined to push for lower rates, understanding that agents are less desperate for listings. The prevailing economic conditions, local housing inventory, and average property values in a specific area all play a role in setting these customary rates and determining their flexibility.

The Role of Service and Value Proposition

A realtor’s commission is not just for opening doors; it compensates for a comprehensive suite of services. These include professional photography, staging advice, extensive marketing (online listings, social media, print ads), hosting open houses, negotiating offers, managing complex paperwork, and guiding clients through the entire closing process. Agents who offer a higher level of service, broader marketing reach, or specialized expertise (e.g., luxury properties, unique historical homes) may command higher commission rates, justifying it with the added value and potentially faster, more lucrative sales they can secure. Sellers must weigh the financial implications of a lower commission against the potential for a less robust marketing effort or less experienced representation, which could ultimately impact the final sale price or transaction smoothness.

Impact of Market Dynamics

Local market conditions significantly influence commission rates. In a strong seller’s market with low inventory and high demand, properties often sell quickly and sometimes above asking price. In such scenarios, some agents might be more open to negotiating a slightly lower commission, as their effort to sell the property might be reduced. Conversely, in a buyer’s market or a slow market, where properties take longer to sell and require more intensive marketing and negotiation, agents may be less willing to discount their rates, as their workload and risk are higher. The financial risk assumed by the agent (investing time and money in marketing without guaranteed payment until closing) is directly tied to market conditions.

Negotiating Commission: Is It Possible?

The short answer is yes, commission rates are often negotiable. However, the decision to negotiate and the extent to which an agent is willing to concede involves a delicate balance of financial considerations, perceived value, and market realities.

Weighing the Pros and Cons of Negotiation

For sellers, negotiating a lower commission directly translates to higher net proceeds from the sale. A 1% reduction in commission on a $500,000 home saves $5,000 – a significant sum. However, sellers must consider the potential downsides. An agent who agrees to a significantly lower commission might be less motivated, or they might reduce the quality or quantity of services they provide, such as professional photography, extensive marketing, or personalized attention. This could potentially lead to a longer time on the market, a lower final sale price, or a more stressful transaction. The financial gain from a lower commission must be weighed against the potential financial losses or inconveniences resulting from reduced service.

Alternative Commission Models

Beyond the traditional percentage-based model, some alternative financial arrangements exist:

- Flat Fee Services: Some brokerages or agents offer a fixed fee for specific services, such as listing the property on the MLS (Multiple Listing Service) but with minimal additional support. This significantly reduces the commission cost but requires the seller to handle much of the marketing, showings, and negotiation themselves, demanding considerable time and expertise.

- Limited Service Brokerages: These models offer a reduced commission in exchange for fewer services. For example, they might handle paperwork but leave open houses and negotiations to the seller. While offering financial savings, this approach shifts more responsibility and potential risk onto the seller.

- Discount Brokers: These firms typically offer lower commission rates, often by operating with a higher volume of transactions, using technology to streamline processes, or by employing agents on a salary rather than pure commission. The financial benefit is clear, but sellers should diligently research the scope of services provided to ensure it meets their needs.

The Value Beyond the Percentage

Ultimately, the decision to negotiate and which commission model to choose should extend beyond the immediate financial savings. A skilled, well-compensated agent often brings invaluable financial benefits through their expertise: accurate pricing to attract optimal offers, robust negotiation skills that can secure a higher sale price, and efficient transaction management that prevents costly delays or legal issues. The incremental cost of a full-service agent’s commission can often be offset, or even surpassed, by their ability to achieve a better sale price, faster closing, or smoother process, translating into a greater net financial gain for the seller in the long run. When evaluating commission, consider not just the cost, but the potential return on investment in professional guidance.

The Financial Value Proposition of a Realtor

Engaging a real estate professional, while incurring a significant commission, offers a substantial financial value proposition for both sellers and buyers. This value extends far beyond mere transaction processing, encompassing strategic advice, market insights, and risk mitigation.

Maximizing Your Return on Investment

For sellers, a competent realtor’s primary financial value lies in their ability to maximize the sale price of a property. This isn’t achieved by chance but through strategic pricing based on deep market analysis, professional staging and photography that enhance perceived value, and extensive marketing efforts that expose the property to the widest possible pool of qualified buyers. A skilled negotiator can also secure a higher sale price and more favorable terms, directly impacting the seller’s net proceeds. Without professional guidance, sellers risk underpricing their home and leaving money on the table or overpricing it, leading to extended market time and eventual price reductions. The commission, in this light, becomes an investment in achieving the best possible financial outcome.

For buyers, a realtor’s financial value is realized through their ability to identify properties that meet financial criteria, negotiate a favorable purchase price, and protect their interests during due diligence. A buyer’s agent can spot overpriced listings, identify potential future costs (e.g., repairs, taxes), and negotiate concessions that save the buyer thousands of dollars. They also help buyers avoid common financial pitfalls, ensuring they don’t overpay or purchase a property with unforeseen liabilities.

Mitigating Financial Risks

Real estate transactions are fraught with potential financial risks. Errors in contracts, overlooked property issues, or missteps in the negotiation process can lead to significant monetary losses or legal complications. Realtors act as a financial safeguard, leveraging their expertise to navigate these complexities. They ensure all legal disclosures are made, contracts are properly executed, and deadlines are met, thereby minimizing the risk of costly disputes or delays. For sellers, this means reducing the chance of post-sale litigation; for buyers, it means ensuring they are not unknowingly inheriting expensive problems. The commission paid is, in part, a premium for this crucial financial risk management and peace of mind.

In essence, realtor commission is the financial engine of the real estate industry, compensating professionals for their specialized knowledge, labor, and risk. Understanding its mechanics, implications, and the value it underpins is fundamental to making informed financial decisions in any property transaction.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.