In the world of personal finance and risk management, the terms we use define the boundaries of our security. One of the most critical, yet frequently misunderstood, terms is “peril.” While in common parlance, peril implies a general sense of danger, its definition within the financial and insurance sectors is far more precise. Understanding what peril is—and, more importantly, how it differs from associated concepts like “hazard”—is the cornerstone of building a robust financial plan.

At its core, a peril is the specific cause of a loss. It is the event that triggers a financial claim or results in the depletion of assets. Whether you are an individual protecting your home, an investor shielding a portfolio, or a business owner safeguarding operations, identifying the perils you face is the first step toward achieving long-term financial stability.

Understanding Peril in the Insurance and Financial Landscape

To manage money effectively, one must look at the world through the lens of potential loss. In insurance contracts, which are essentially financial tools for risk transfer, peril serves as the fundamental trigger for coverage. Without a defined peril, there is no basis for indemnity.

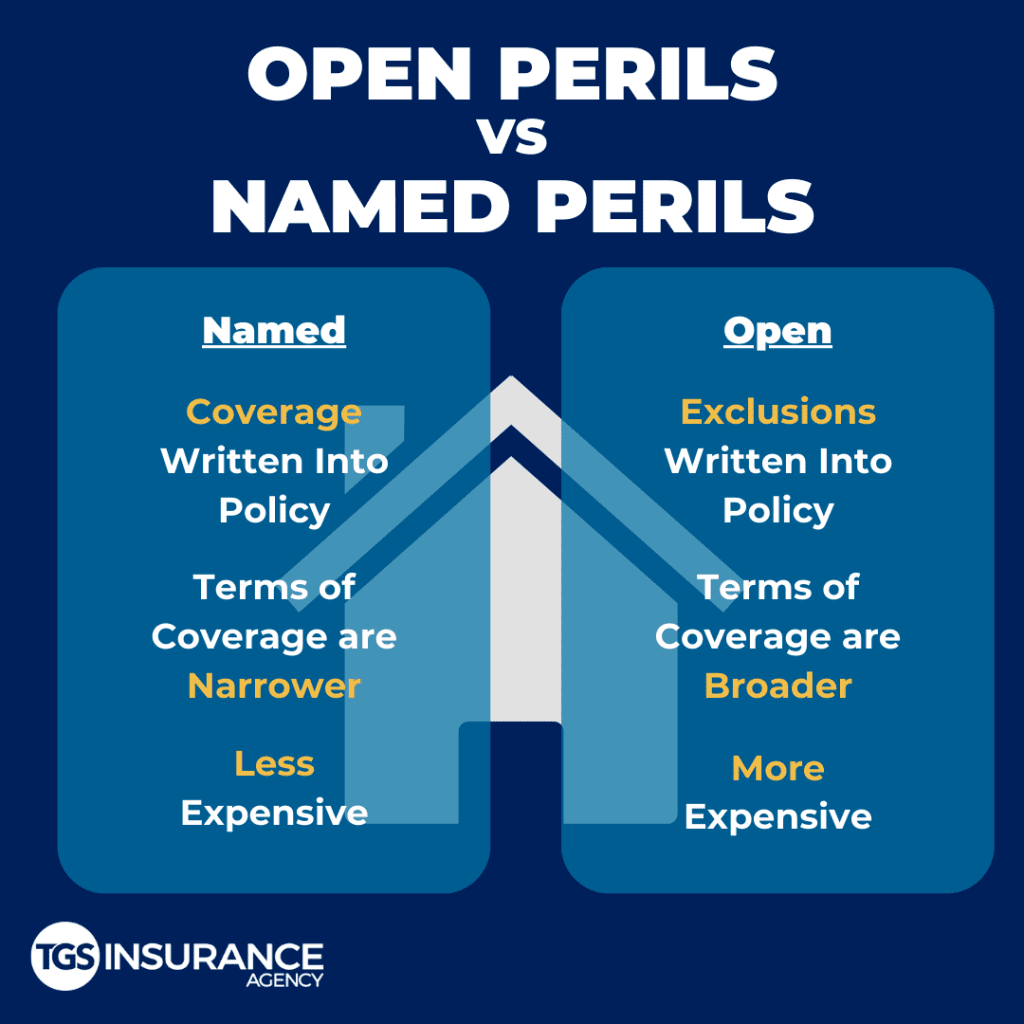

Named Perils vs. Open Perils

When reviewing insurance policies—whether for homeowners, renters, or commercial property—you will encounter two primary structures: “Named Perils” and “Open Perils” (often called All-Risk).

A Named Peril policy provides coverage only for the specific events listed in the contract. Common examples include fire, lightning, windstorm, and theft. If an event occurs that is not explicitly written in the policy, the financial burden remains with the policyholder. This is often a more cost-effective option for those on a tight budget, but it requires a high degree of financial literacy to ensure that the most likely risks are accounted for.

Conversely, an Open Peril policy covers all causes of loss unless they are specifically excluded. Exclusions typically include high-magnitude events like earthquakes, floods, or acts of war, which often require specialized riders. From a financial planning perspective, Open Peril policies offer a higher degree of certainty, protecting your net worth against the “unknown unknowns.”

Peril vs. Hazard: The Financial Distinction

A common mistake in financial management is conflating peril with hazard. A peril is the actual event that causes the loss (e.g., a fire). A hazard is a condition that increases the probability or severity of that loss.

For instance, if you own a warehouse, a “fire” is the peril. “Storing oily rags near a furnace” is the hazard. Understanding this distinction is vital for risk mitigation. While you cannot always control when a peril occurs, you can often manage the hazards that lead to them, thereby lowering your insurance premiums and protecting your capital.

Categorizing the Perils That Threaten Personal Wealth

Financial perils are not limited to physical property damage. To build a comprehensive financial fortress, one must categorize perils based on how they impact different pillars of wealth: assets, liability, and earning capacity.

Natural and Human-Induced Perils

Natural perils are often referred to as “Acts of God” in legal and financial circles. These include hurricanes, tornadoes, earthquakes, and lightning. While these are statistically infrequent for many, their financial impact is often catastrophic, capable of wiping out decades of savings in a single afternoon.

Human-induced perils, on the other hand, involve the actions (or inactions) of people. These include theft, vandalism, arson, and civil unrest. In the modern financial era, this category has expanded to include digital theft and fraudulent transfers, which can be just as devastating to a personal balance sheet as a physical fire.

Liability Perils: The Hidden Threat to Net Worth

Perhaps the most dangerous peril to a high-net-worth individual or a growing business is the liability peril. This refers to the risk of being held legally responsible for injury to others or damage to their property.

Unlike a physical peril, where the loss is capped at the value of the asset (e.g., if your $500,000 house burns down, you lose $500,000), a liability peril has an almost unlimited ceiling. A single lawsuit resulting from an auto accident or an injury on your property can result in a judgment that exceeds your current assets, leading to the garnishment of future wages and the liquidation of investments. Managing this peril requires not just standard insurance, but often an “Umbrella Policy” to provide an extra layer of financial defense.

Economic and Market Perils

In the context of investing, peril takes on a different form. Here, we deal with market perils such as sudden currency devaluation, hyperinflation, or a “black swan” event that causes a market crash. These perils do not destroy physical property, but they destroy the purchasing power of your money. Diversification and asset allocation are the primary tools used to hedge against these economic perils.

Strategic Risk Assessment: Identifying and Mitigating Peril

Knowing what peril is only matters if you have a strategy to address it. Financial professionals use a process called “Risk Assessment” to determine which perils require insurance, which require lifestyle changes, and which can be self-insured.

The Frequency-Severity Matrix

A standard tool in financial risk management is the Frequency-Severity Matrix. This helps individuals and businesses decide how to allocate their financial resources:

- Low Frequency / High Severity: These are perils like a house fire or a major disability. They rarely happen, but when they do, they are financially ruinous. Strategy: Transfer the risk (Insurance).

- High Frequency / Low Severity: These are small, recurring costs, like a cracked phone screen or minor car dings. Strategy: Retain the risk (Self-insurance/Emergency Fund).

- Low Frequency / Low Severity: Events that rarely happen and cost very little. Strategy: Ignore/Accept the risk.

- High Frequency / High Severity: These are activities that are almost guaranteed to result in massive loss. Strategy: Avoid the activity altogether.

Building a Financial Buffer

The most effective way to manage the financial impact of any peril is the maintenance of liquidity. An emergency fund is essentially a “self-funded insurance policy” against minor perils. By having 3–6 months of expenses in a high-yield savings account, you ensure that a minor peril (like a car repair) doesn’t force you to take on high-interest debt, which is a secondary financial peril in itself.

The Role of Peril in Business Finance and Continuity

For entrepreneurs and business owners, the concept of peril extends into the realm of operational viability. A business must account for perils that could halt production or destroy its reputation.

Business Interruption and Contingent Perils

If a fire (a peril) destroys a factory, the immediate loss is the building and equipment. However, the more significant financial peril is “Business Interruption.” This is the loss of income that occurs while the business is unable to operate.

Furthermore, businesses must consider “Contingent Business Interruption.” This occurs when a peril strikes a key supplier or a major customer, causing a ripple effect that impacts your own revenue. In a globalized economy, a peril occurring halfway across the world can have immediate financial consequences for a local business.

Professional Indemnity and Errors & Omissions

For those in service industries—consultants, accountants, and lawyers—the primary peril is a professional mistake. “Errors and Omissions” (E&O) insurance protects against the peril of professional negligence. In the world of business finance, protecting your intellectual and professional standing is just as important as protecting physical assets. Without coverage for these perils, one’s entire professional career can be derailed by a single oversight.

Peril and the Future: Adapting to New Financial Threats

As the global financial landscape evolves, the nature of peril is shifting. The digital age has introduced perils that were unimaginable thirty years ago.

Cyber Perils and Digital Asset Security

Cybercrime is now one of the leading perils facing both individuals and corporations. The theft of identity, the hacking of brokerage accounts, and the deployment of ransomware are digital perils with very real financial consequences. Financial planning in the 21st century must include “cyber hygiene” and potentially cyber insurance to mitigate the risk of digital asset seizure.

Climate Risk and Changing Actuarial Realities

Climate change is currently redefining how insurance companies view natural perils. Areas once considered “low risk” for flooding or wildfire are being reclassified. For the individual, this means that a peril that was once ignored must now be accounted for in the household budget, often in the form of rising insurance premiums or the necessity of expensive home retrofitting. Staying ahead of these shifts is essential for maintaining the value of real estate investments.

Conclusion: Mastering Peril for Financial Peace of Mind

Understanding “what is peril” is not merely an academic exercise in insurance terminology; it is a vital component of financial literacy. By identifying the specific causes of potential loss, categorizing them based on their impact, and implementing strategic defenses, you move from a position of vulnerability to one of empowerment.

The goal of financial planning is not to eliminate peril—that is impossible in an unpredictable world. Instead, the goal is to ensure that when a peril does manifest, it is a manageable event rather than a financial catastrophe. Whether through robust insurance coverage, strategic diversification, or the diligent maintenance of an emergency fund, mastering the concept of peril allows you to navigate the complexities of the financial world with confidence and resilience. Protect your assets, safeguard your income, and always be prepared for the unexpected; that is the essence of true financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.