In the modern financial landscape, few symbols command as much attention as “NVDA.” For the seasoned investor and the casual observer alike, the question of what Nvidia’s stock price is represents more than a simple numerical inquiry; it is a pulse check on the global shift toward artificial intelligence and the future of high-performance computing. To understand Nvidia’s price is to understand the complex interplay of supply chain dominance, massive capital expenditures by big tech, and the psychological cycles of the equity markets.

Nvidia has transitioned from a niche provider of graphics processing units (GPUs) for gamers to a foundational pillar of the global economy. As its market capitalization has soared into the trillions, its stock price has become a bellwether for the broader technology sector and the S&P 500 index. However, evaluating this price requires a deep dive into financial metrics, valuation models, and the macroeconomic environment that dictates whether a price is “expensive” or a “value play.”

The Mechanics of Nvidia’s Current Market Valuation

When an investor asks about a stock price, they are looking at a snapshot in time—a reflection of the last trade made on an exchange. For Nvidia, this price is the result of millions of data points being synthesized by algorithmic traders and human investors. However, the price per share is only part of the story; it must be viewed through the lens of market capitalization and share structure.

Real-Time Pricing vs. Intrinsic Value

The market price of Nvidia is a “voting machine” in the short term, reflecting sentiment, news cycles, and quarterly earnings beats. However, the intrinsic value—what the company is actually worth based on its future cash flows—is what long-term investors focus on. In recent years, Nvidia’s price has seen extreme volatility, driven by “beat and raise” earnings reports where the company consistently exceeds analyst expectations. This creates a scenario where the stock price can move double digits in a single trading session, reflecting the market’s attempt to price in growth that is happening faster than traditional models can predict.

The Impact of Stock Splits on Price Perception

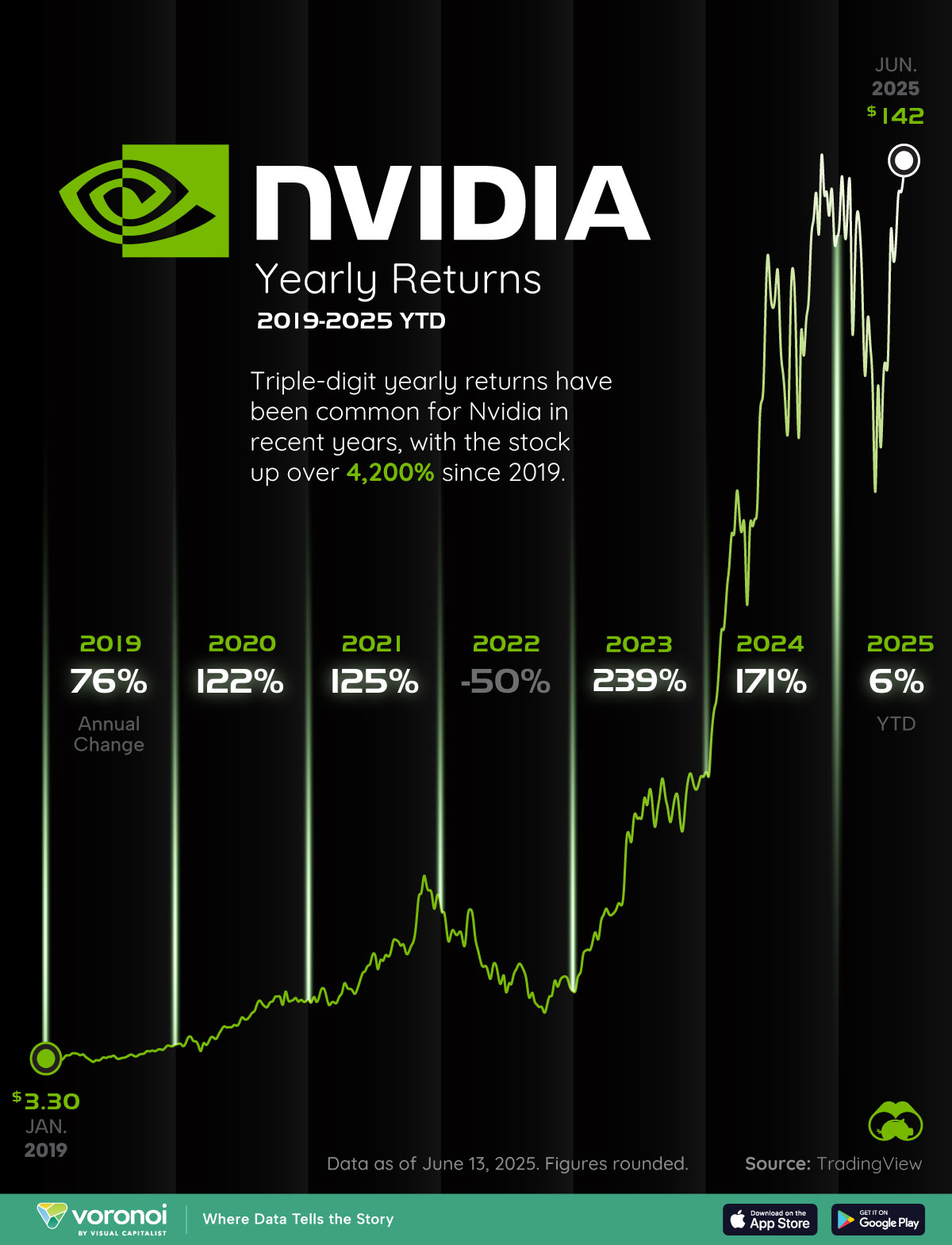

One cannot discuss Nvidia’s price without acknowledging its history of stock splits, most notably the 10-for-1 split in mid-2024. While a split does not change the fundamental value of the company (it is akin to cutting a pizza into more slices), it drastically lowers the nominal price per share. This psychological “lowering” of the price increases liquidity and makes the stock more accessible to retail investors who might be deterred by a four-digit share price. Understanding this helps investors realize that a “lower” price post-split does not mean the company is cheaper; it simply means the entry point is more flexible.

Key Financial Drivers Influencing the Stock Price

To understand why Nvidia’s stock price sits where it does today, one must look at the engine room of the company: its financial statements. The price is a reflection of the company’s ability to generate cash, and in Nvidia’s case, that cash generation has become legendary in the annals of corporate finance.

Revenue Growth in the Data Center Segment

The primary catalyst for Nvidia’s price appreciation has been the explosive growth of its Data Center division. This segment, which houses the H100 and Blackwell chips, has moved from a secondary revenue stream to the company’s primary source of income. When Nvidia reports a 200% or 300% year-over-year increase in data center revenue, the stock price reacts because it proves that the “AI gold rush” is translating into hard currency. Investors monitor these quarterly figures to justify the stock’s premium, looking for signs of sustained demand from cloud service providers like Microsoft, Amazon, and Google.

Gross Margins and Profitability Ratios

Unlike many high-growth tech companies that sacrifice profits for scale, Nvidia has maintained exceptionally high gross margins—often exceeding 70%. This level of profitability is rare for a hardware company and suggests a powerful “moat” or competitive advantage. The stock price reflects this efficiency; investors are willing to pay a higher multiple for Nvidia because a large portion of every dollar earned drops straight to the bottom line. If margins were to compress due to competition or rising manufacturing costs, the stock price would likely face downward pressure, regardless of total revenue.

Analyzing Valuation Metrics: Is the Price Justified?

A common debate in the financial community is whether Nvidia’s stock price is a “bubble” or a fair reflection of its dominance. To answer this, analysts move beyond the price-over-time chart and look at specific valuation ratios.

Understanding the Forward P/E Ratio

The Price-to-Earnings (P/E) ratio is the standard yardstick for valuation. However, for a company growing as fast as Nvidia, the trailing P/E (based on past earnings) is often misleading. Instead, the market looks at the Forward P/E, which uses estimated earnings for the next twelve months. Interestingly, even as Nvidia’s stock price has hit record highs, its forward P/E has occasionally decreased because its earnings are growing even faster than its share price. This phenomenon suggests that the stock, while high in nominal price, may actually be “cheaper” on an earnings-adjusted basis than it was in previous years.

The PEG Ratio: Growth at a Reasonable Price

Another critical metric is the Price/Earnings-to-Growth (PEG) ratio. This factors in the company’s expected growth rate alongside its P/E ratio. A PEG ratio of 1.0 is generally considered fair value. For much of its recent run, Nvidia’s PEG ratio has remained surprisingly competitive compared to other “Magnificent Seven” stocks. By looking at the PEG ratio, an investor can determine if the current stock price is factoring in too much optimism or if there is still room for the price to catch up to the projected growth of the AI industry.

External Economic Factors and Market Sentiment

No stock exists in a vacuum. Nvidia’s price is heavily influenced by the broader macroeconomic environment, which can either act as a tailwind or a headwind for high-valuation growth stocks.

Interest Rates and Tech Equity Sensitivity

As a growth stock, Nvidia is sensitive to the Federal Reserve’s interest rate policy. High interest rates increase the “discount rate” applied to future cash flows, which can lower the present value of the stock. Conversely, a pivot toward lower interest rates generally boosts tech stocks. Investors watching Nvidia’s price must keep a close eye on inflation data and central bank commentary, as these factors often dictate the “risk-on” or “risk-off” sentiment of the market, regardless of Nvidia’s individual performance.

Institutional Ownership and the “Index Effect”

Nvidia is a staple in almost every major mutual fund and ETF, including the S&P 500 and the Nasdaq-100. This high level of institutional ownership creates a compounding effect on the stock price. As more money flows into passive index funds, those funds must buy shares of Nvidia in proportion to its market weight. This creates a consistent floor of buying pressure. However, it also means that if there is a general market sell-off, Nvidia’s price can be dragged down by institutional rebalancing, even if the company’s fundamentals remain flawless.

Strategic Outlook: Predicting the Trajectory of NVDA

Investing is a forward-looking endeavor. To gauge where Nvidia’s stock price might go, one must analyze the roadmap of the company and the potential obstacles in its path.

The Impact of Product Cycles: From Hopper to Blackwell

The release of new architecture is the single most important event for Nvidia’s stock price. The transition from the Hopper architecture (H100) to the Blackwell platform represents a significant leap in computing power and energy efficiency. The market price often “front-runs” these releases, pricing in the expected sales before the chips even hit the shelves. If the rollout of a new product line faces delays or technical glitches, the stock price usually sees a sharp correction as analysts downwardly revise their revenue targets.

Potential Risks: Geopolitics and Competition

Finally, every investor must weigh the risks that could decouple Nvidia’s price from its growth trajectory. Geopolitical tensions, particularly concerning semiconductor manufacturing in Taiwan, represent a systemic risk to Nvidia’s supply chain. Furthermore, while Nvidia currently holds a dominant market share, the rise of custom AI silicon from big tech companies (in-house chips by Apple, Amazon, or Meta) and competition from rivals like AMD could eventually lead to price wars. Monitoring these competitive threats is essential for anyone trying to determine if Nvidia’s stock price can maintain its premium valuation in the long run.

In conclusion, Nvidia’s stock price is a complex barometer of the digital age. It is fueled by unprecedented earnings growth and high-profit margins, yet it remains tethered to the realities of interest rates, valuation metrics, and geopolitical stability. For the modern investor, the price is not just a number on a screen; it is a narrative of technological disruption and the immense financial stakes of the AI revolution. Whether the price continues its ascent or enters a period of consolidation, its movement will remain the most watched signal in the global financial markets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.