Understanding your monthly income is not just a rudimentary accounting exercise; it is the bedrock of sound financial health. For many, it seems like a straightforward figure – the amount that lands in your bank account on payday. However, a truly insightful look at “what is my monthly income” involves far more than a single number. It encompasses identifying all sources, distinguishing between gross and net, understanding its stability, and ultimately, leveraging this critical information to budget effectively, save strategically, invest wisely, and plan for a secure future. Without a clear and accurate grasp of your income, financial planning becomes a shot in the dark, leading to potential instability and missed opportunities. This comprehensive guide will dissect the concept of monthly income, offering practical steps to calculate it, strategies to optimize it, and insights into its profound impact on your overall financial well-being.

Understanding the Nuances of “Monthly Income”

Before you can effectively manage your money, you must first precisely define what “monthly income” truly means for you. It’s a term often used loosely, but its implications are vast.

Gross vs. Net Income: The Critical Distinction

Perhaps the most fundamental aspect of understanding your income is differentiating between gross and net.

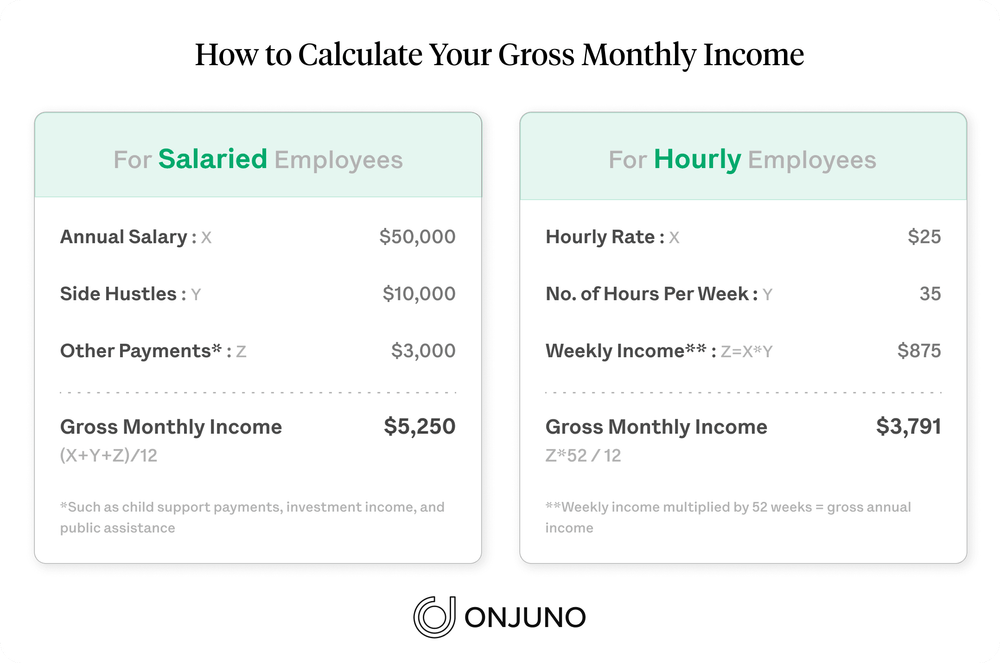

- Gross Income is the total amount of money you earn before any deductions are taken out. For salaried employees, this is your annual salary divided by twelve. For freelancers, it’s the sum of all invoices before expenses and self-employment taxes. For business owners, it’s total revenue before operating costs. While an impressive figure on paper, gross income is rarely the amount you have available to spend.

- Net Income, conversely, is the amount of money you actually receive after all mandatory deductions have been made. For employees, this includes federal, state, and local taxes, Social Security, Medicare, health insurance premiums, retirement contributions (401k, 403b), and any other pre-tax deductions like commuter benefits. For self-employed individuals, net income is what remains after business expenses and estimated taxes are set aside. It is your net income – often referred to as your “take-home pay” – that dictates your true purchasing power and forms the basis for all personal budgeting and financial planning. Focusing solely on gross income without accounting for these deductions is a common pitfall that can lead to overspending and financial stress.

Sources of Income: Uncovering Every Stream

Most people have at least one primary source of income, typically a salary or wages from employment. However, a holistic view requires identifying all streams, big or small.

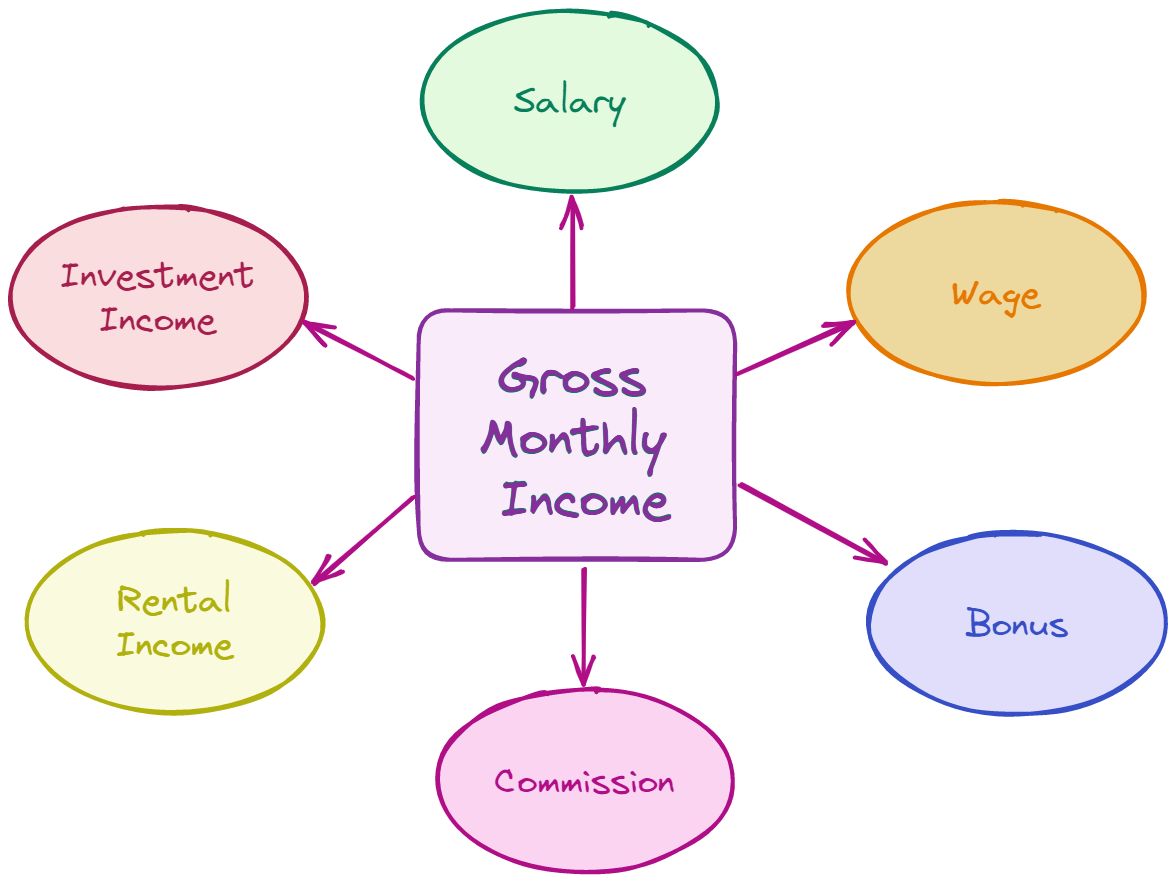

- Primary Employment: Your main job, whether salaried, hourly, or commission-based.

- Side Hustles & Freelance Work: Income from gig economy platforms, consulting, creative projects, or part-time jobs.

- Investment Income: Dividends from stocks, interest from savings accounts or bonds, rental income from properties, or distributions from mutual funds.

- Benefits & Allowances: Social Security benefits, disability payments, alimony, child support, or unemployment benefits.

- Other Income: Royalties, inheritances, gifts, or even regular refunds/rebates.

Identifying and tallying all these sources provides a more comprehensive picture of your financial inflow. Missing even small, irregular income streams can skew your perception of available funds.

Variable vs. Fixed Income: Stability and Predictability

The nature of your income — whether it’s fixed or variable — profoundly impacts your budgeting approach and financial stability.

- Fixed Income is predictable and consistent. This typically applies to salaried employees who receive the same amount of net pay each month. It allows for straightforward budgeting and easier long-term financial planning.

- Variable Income fluctuates from month to month. This is common for freelancers, commission-based sales professionals, small business owners, or those with significant overtime hours. While potentially offering higher earning potential, variable income requires a more conservative budgeting strategy, often involving averaging income over several months or planning based on your lowest expected monthly earnings. Understanding this distinction is crucial for setting realistic financial goals and avoiding budget shortfalls during leaner months.

The Imperative of Calculating Your True Monthly Income

Accurately calculating your true monthly income is not just an administrative task; it is the foundational step for every other aspect of your financial life. Without this precise figure, you are essentially flying blind, making decisions based on assumptions rather than concrete data.

Why Accuracy Matters: Beyond the Bank Statement

The number that appears on your bank statement each month may seem like your income, but it often isn’t the whole story. An accurate calculation provides clarity and prevents crucial missteps.

- Effective Budgeting: Knowing your precise net income is the first step in creating a realistic budget that aligns with your actual spending capacity. It allows you to allocate funds effectively to needs, wants, and savings, preventing overspending or under-saving.

- Debt Management: Understanding how much disposable income you have available after essentials is critical for formulating a coherent debt repayment strategy. You can determine how much extra you can put towards high-interest debts, accelerating your path to financial freedom.

- Saving and Investing Goals: Whether you’re building an emergency fund, saving for a down payment, or planning for retirement, your consistent monthly income dictates how much you can contribute towards these goals. Accurate figures ensure your savings targets are achievable and your investment strategy is sustainable.

- Financial Planning and Growth: For long-term financial planning, such as purchasing a home, planning for children’s education, or retirement, your income is the central variable. It informs what you can afford, how quickly you can achieve milestones, and what your long-term wealth potential looks like.

Step-by-Step Calculation Guide: A Practical Approach

Let’s break down how to get to that crucial net monthly income figure.

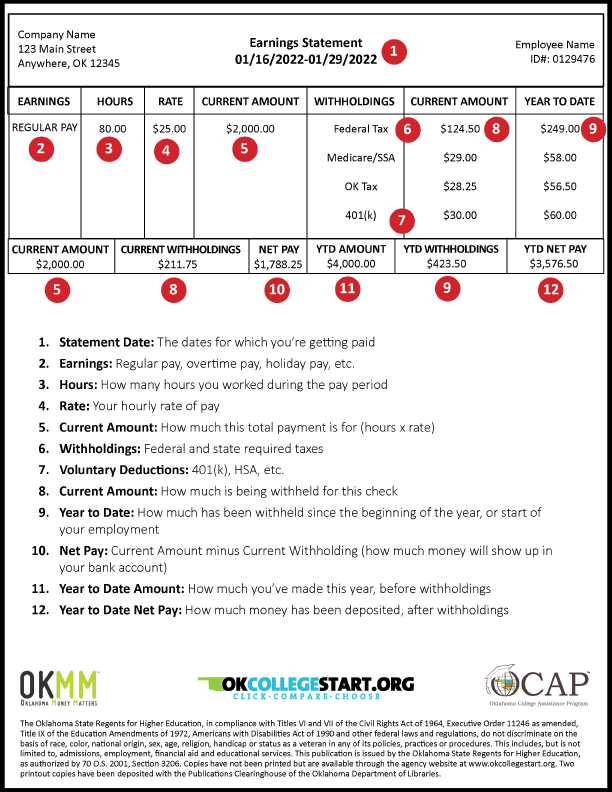

- Gather All Income Statements: Collect recent pay stubs (for employees), bank statements showing direct deposits, invoices paid (for freelancers), and any records of investment distributions or other regular income. Aim for at least three to six months of data, especially if your income varies.

- Identify and Sum All Gross Income: For each source, list the total amount earned before any deductions. If you are salaried, this is usually straightforward. For variable income, this means the full amount of payments received.

- Account for All Deductions (Employees): From your gross income, subtract all deductions itemized on your pay stub:

- Federal, state, and local taxes

- Social Security and Medicare (FICA)

- Health, dental, and vision insurance premiums

- Retirement contributions (401k, 403b, etc.)

- Any other pre-tax deductions (e.g., FSA, commuter benefits)

- Account for Expenses and Estimated Taxes (Self-Employed/Freelancers): From your gross freelance or business income, subtract legitimate business expenses. Crucially, also set aside a significant portion (often 25-35% or more, depending on your income level and state) for estimated quarterly taxes. Do not count this money as spendable income.

- Sum All Net Income Sources: Once you have calculated the net income from each source, add them all together. If your income is variable, calculate an average over the three to six months you analyzed. Consider planning your budget around your lowest typical month to ensure you always have enough.

- Include Other Regular Inflows: Don’t forget any other consistent money coming in, like child support, alimony, or regular investment dividends.

Tools and Resources: Simplifying the Process

You don’t have to do this with just a pen and paper. Leverage available tools:

- Spreadsheets: Google Sheets or Microsoft Excel offer customizable templates to track income and expenses.

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), Personal Capital, or Simplifi can link to your bank accounts and automatically categorize income and transactions, providing real-time insights.

- Online Calculators: Many financial websites offer net pay calculators that can help employees estimate their take-home pay based on gross salary and deductions.

Leveraging Your Monthly Income for Financial Health

Once you have a clear understanding of your true monthly income, the real work begins: using that knowledge to build a robust financial foundation and achieve your monetary goals. Your income is not just for spending; it’s a powerful tool for wealth creation and security.

Budgeting and Expense Tracking: Your Financial Roadmap

A budget is not about restriction; it’s about intentional spending and saving. Your net monthly income is the budget’s cornerstone.

- The 50/30/20 Rule: A popular guideline where 50% of your net income goes to Needs (housing, utilities, groceries, transportation), 30% to Wants (dining out, entertainment, hobbies), and 20% to Savings & Debt Repayment (emergency fund, retirement, extra debt payments). This provides a flexible framework.

- Zero-Based Budgeting: Every dollar of your net income is assigned a “job” (spending, saving, debt repayment) until your income minus your expenses equals zero. This ensures you’re intentional with every penny.

- Creating a Realistic Spending Plan: Track your expenses for a month or two to understand where your money actually goes. Compare this to your income and adjust your spending categories to align with your financial priorities. Be honest with yourself about your habits.

Debt Management Strategies: Accelerating Freedom

Your monthly income dictates your capacity to tackle debt strategically.

- Debt Snowball: Prioritize paying off the smallest debt first, regardless of interest rate. Once that’s paid, roll its payment into the next smallest debt. The psychological wins keep you motivated.

- Debt Avalanche: Focus on paying off debts with the highest interest rates first. This saves you the most money in the long run.

- Allocating Extra Funds: Once you know your disposable income, you can consciously allocate a portion of it to accelerate debt repayment, freeing up cash flow for other goals sooner.

Building an Emergency Fund: Your Financial Safety Net

An emergency fund is paramount. It’s a cushion of readily accessible cash to cover unexpected expenses (job loss, medical emergency, car repair) without going into debt.

- How Much to Save: Aim for 3-6 months’ worth of essential living expenses (rent/mortgage, utilities, food, transportation, insurance).

- How Income Dictates Pace: Your monthly net income directly determines how quickly you can build this fund. Dedicate a consistent portion of your income each month until your target is met. Automating these transfers can be highly effective.

Saving for Future Goals: Bringing Dreams to Life

Beyond immediate needs and debt, your monthly income fuels your aspirations.

- Retirement: Contribute regularly to retirement accounts (401k, IRA). Many employers offer a match – take advantage of this free money.

- Down Payment: Saving for a house, car, or other significant purchase requires consistent contributions from your income.

- Education: Whether for yourself or your children, allocate funds to educational savings accounts.

- Vacations: Budgeting for leisure from your monthly income makes these experiences guilt-free.

Strategic Investing: Making Your Money Work for You

Once your emergency fund is robust and high-interest debts are under control, a portion of your monthly income should be directed towards investments to grow your wealth over time.

- Diversification: Spread investments across different asset classes (stocks, bonds, real estate) to mitigate risk.

- Automated Investments: Set up automatic transfers from your checking account to your investment accounts. Even small, consistent contributions can compound significantly over the years.

- Professional Advice: Consider consulting a financial advisor to help tailor an investment strategy that aligns with your income, risk tolerance, and long-term goals.

Strategies to Boost and Optimize Your Monthly Income

While managing your current income is vital, actively seeking ways to increase and optimize it can significantly accelerate your financial journey. Your income isn’t necessarily a fixed ceiling; it can be a dynamic figure that grows with strategic effort.

Professional Development: Investing in Yourself

One of the most direct paths to increasing your monthly income is by enhancing your value in the job market.

- Skills Acquisition: Learn new skills relevant to your industry or a high-demand field. Online courses, workshops, and certifications can make you more competitive.

- Advanced Education: A degree or specialized certification can open doors to higher-paying positions.

- Negotiation for Raises: Regularly research industry salary benchmarks. When performance reviews come around, be prepared to articulate your accomplishments and value to the company, then confidently negotiate for a higher salary.

- Job Hopping: Sometimes, the quickest way to a significant pay raise is to switch companies. Use your enhanced skills and experience to secure a better offer elsewhere.

Exploring Side Hustles: Diversifying Income Streams

In today’s economy, relying on a single income source can be risky. Side hustles offer a fantastic way to supplement your primary income and even discover new passions.

- Gig Economy: Platforms like Uber, Lyft, DoorDash, or Instacart offer flexible ways to earn extra cash.

- Freelancing: Leverage your professional skills (writing, graphic design, web development, consulting) on platforms like Upwork, Fiverr, or LinkedIn.

- Selling Products/Services: Start an e-commerce store, create handmade goods, offer tutoring, pet-sitting, or house-sitting services.

- Monetizing Hobbies: Turn a passion into profit – photography, baking, crafting, or teaching music lessons.

Passive Income Opportunities: Earning While You Sleep

The ultimate goal for many is to generate income that doesn’t require active, ongoing work.

- Investments: Dividend stocks, interest-bearing savings accounts, bonds, or real estate investment trusts (REITs) can provide regular income.

- Rental Property: Owning rental properties can generate consistent monthly income, though it requires initial capital and management.

- Intellectual Property: Royalties from books, music, patents, or online courses can provide recurring income streams.

- Affiliate Marketing/Blogging: Creating content and earning commissions from promoting products or services.

Reviewing and Adjusting: The Ongoing Process

Your monthly income and financial situation are not static. It’s crucial to regularly review and adjust your strategy.

- Annual Financial Check-up: At least once a year, revisit your income sources, expenses, and financial goals.

- Adapt to Life Changes: Major life events (marriage, children, new job, home purchase) necessitate a re-evaluation of your income and budget.

- Monitor Performance: Keep an eye on your investments and side hustles to ensure they are performing as expected and adjust strategies as needed.

Conclusion

The question “what is my monthly income?” transcends a simple numerical answer. It is a gateway to financial empowerment, requiring an in-depth understanding of every dollar earned, its source, its stability, and its true spending power. By diligently calculating your net income, differentiating between various streams, and acknowledging its variable nature, you lay a concrete foundation for informed financial decisions.

Leveraging this knowledge allows you to construct robust budgets, tackle debt strategically, build vital emergency funds, and save for future aspirations with precision. Furthermore, by proactively exploring avenues for professional growth, side hustles, and passive income, you can transform your income from a static figure into a dynamic engine for wealth accumulation.

In essence, mastering your monthly income is not just about knowing a number; it’s about gaining control, fostering discipline, and charting a clear course towards lasting financial health and security. It’s an ongoing journey, but one that begins with a clear, honest assessment of what truly flows into your financial life each month. Take the time to understand your income, and you unlock the potential to reshape your entire financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.