The year 2025 is on the horizon, and for those diligently planning their personal finances, understanding the maximum Health Savings Account (HSA) contribution limits is a crucial piece of the puzzle. HSAs have emerged as powerful tools, blending the benefits of a tax-advantaged savings vehicle with the flexibility to manage healthcare expenses. As technology rapidly evolves, so too do financial planning strategies, and keeping abreast of these changes, particularly concerning HSAs, can significantly impact your long-term financial well-being. This article will delve into the anticipated maximum HSA contribution for 2025, explore the underlying factors influencing these limits, and provide actionable insights on how to maximize your HSA for both immediate health needs and future financial security, all within the context of today’s dynamic tech and brand-conscious world.

Understanding the HSA Advantage in a Digital Age

Before diving into the specifics of 2025 contribution limits, it’s essential to reiterate the fundamental advantages of an HSA. An HSA is a tax-advantaged savings account that allows individuals with high-deductible health plans (HDHPs) to set aside money for qualified medical expenses. The “triple tax advantage” is its most compelling feature:

- Tax-Deductible Contributions: Contributions made to an HSA are typically tax-deductible, lowering your taxable income for the year.

- Tax-Free Growth: Any earnings within the HSA grow tax-free.

- Tax-Free Withdrawals: When funds are withdrawn for qualified medical expenses, they are not taxed.

In an era where digital tools are integral to managing every facet of our lives, from personal finance apps to AI-driven productivity enhancers, HSAs are no exception. Many employers and financial institutions now offer sophisticated online portals and mobile applications that make tracking contributions, managing investments within the HSA, and submitting claims incredibly straightforward. This digital integration not only simplifies the process but also empowers individuals to make more informed decisions about their healthcare spending and long-term savings strategy. Furthermore, the concept of personal branding extends to our financial management; presenting a well-organized and strategically utilized HSA can be seen as a testament to diligent personal financial planning.

The rise of FinTech has revolutionized how we approach money management. Online income platforms, budgeting apps, and investment tools have made financial literacy more accessible than ever. Within this landscape, the HSA stands out as a particularly robust tool for proactive financial planning, especially when combined with a strategic approach to investing its accumulated funds. The ability to invest HSA funds, much like a 401(k) or IRA, opens up significant opportunities for wealth accumulation, making the maximum contribution limits a topic of considerable interest.

Factors Influencing 2025 HSA Contribution Limits: The Inflation Connection

The Internal Revenue Service (IRS) is responsible for setting the annual HSA contribution limits. These limits are not arbitrary; they are directly tied to inflation adjustments. The Consumer Price Index (CPI) is a primary driver, and as the cost of goods and services rises, so too do the HSA contribution caps. This mechanism ensures that the purchasing power of the HSA remains relatively consistent over time, allowing individuals to save meaningfully for healthcare costs that are also subject to inflationary pressures.

The Role of Inflation and the CPI

The Consumer Price Index (CPI) measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The IRS uses specific CPI data, often from the preceding fiscal year, to calculate the adjustments for HSA limits. A higher inflation rate generally leads to higher contribution limits, while periods of low inflation may result in smaller adjustments or no change at all.

HDHP Minimum Deductible and Out-of-Pocket Maximums

Beyond inflation, HSA contribution limits are intrinsically linked to the definitions of High-Deductible Health Plans (HDHPs). The IRS sets minimum deductible requirements and maximum out-of-pocket expense limits for plans to be considered qualified HDHPs eligible for HSA contributions. These parameters also undergo annual adjustments, influenced by inflation, and directly impact the framework within which HSA contributions are permissible.

For instance, if the IRS adjusts the minimum deductible for an HDHP upwards, it often correlates with an increase in the allowable HSA contribution. This creates a symbiotic relationship: the IRS ensures that HSAs are paired with plans that necessitate a certain level of self-funding for healthcare, thereby incentivizing savings, while also adjusting the savings limits to reflect the changing cost landscape.

Anticipating the 2025 Maximum HSA Contribution: Projections and Considerations

While official IRS figures for 2025 HSA contribution limits won’t be released until later in the year, we can make informed projections based on historical trends and current economic indicators. Understanding these potential increases can help individuals adjust their financial strategies and maximize their savings.

Projected Contribution Limits for 2025

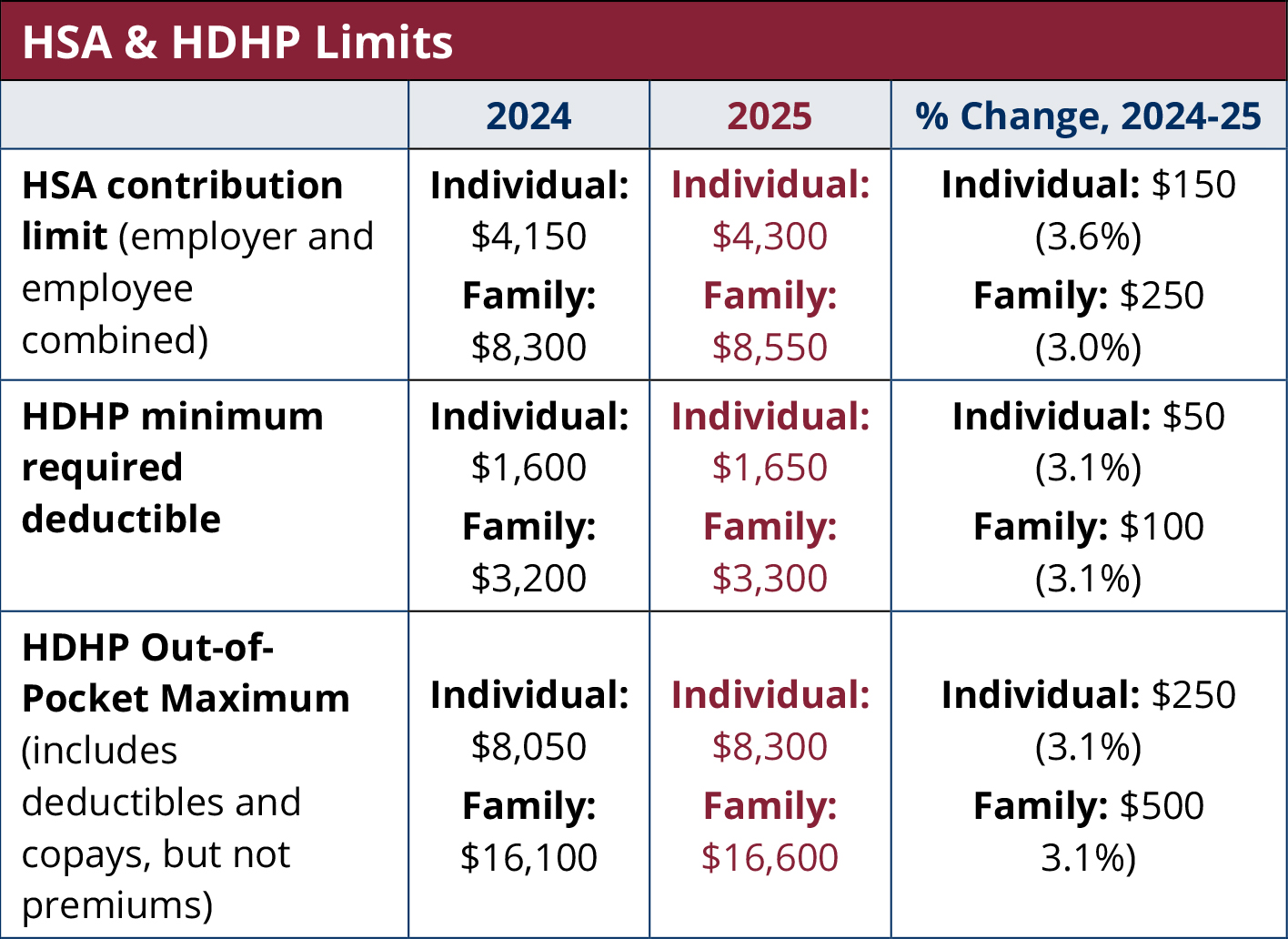

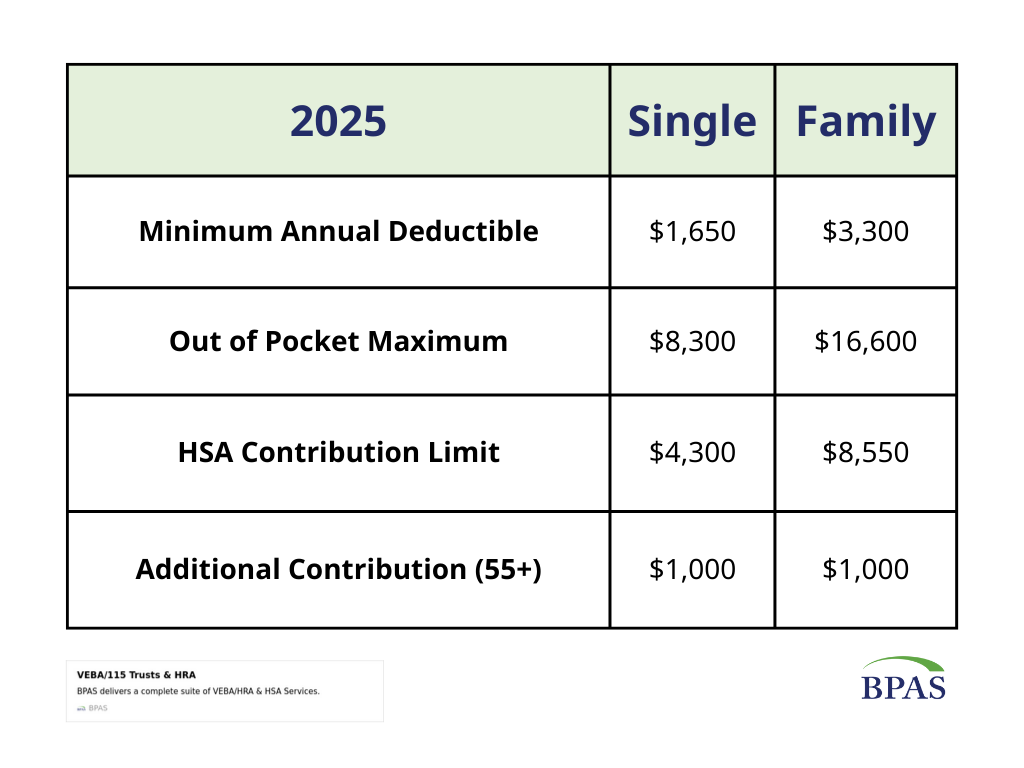

Based on recent inflation data and historical patterns, it is highly probable that the maximum HSA contribution limits for 2025 will see an increase. For 2024, the limits were set at $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up contribution allowed for individuals aged 55 and older.

Considering the inflation observed in the CPI over the past year, we can anticipate a modest, yet significant, rise in these figures for 2025. For example, if inflation continues at a similar pace, the individual limit could potentially rise to around $4,250-$4,350, and the family limit could approach $8,500-$8,700. The catch-up contribution for those 55 and older is generally fixed, but it’s always wise to confirm this specific detail once the IRS releases its official guidance.

It is crucial to remember that these are projections. The final numbers will be released by the IRS, typically in May or June of the preceding year. Staying informed through reputable financial news outlets and official IRS publications is paramount.

The Importance of Staying Informed and Planning Ahead

The power of an HSA lies not just in its tax advantages but in its potential for long-term growth through investment. Many individuals utilize their HSA as a supplemental retirement savings vehicle, investing the funds in a diversified portfolio of stocks, bonds, and mutual funds. This strategy, coupled with consistent contributions up to the maximum limit, can lead to substantial wealth accumulation over decades.

For those who are self-employed or whose employers do not offer HSAs, the process of opening and managing one still falls under the purview of these IRS limits. This provides a valuable opportunity for independent wealth building, especially for entrepreneurs and freelancers who might be navigating the complexities of business finance and personal income streams. The ability to earmark funds for healthcare while simultaneously growing them for future needs offers unparalleled financial flexibility.

Furthermore, in the rapidly evolving landscape of personal branding, demonstrating sound financial management is a key component of a well-curated personal identity. A robust HSA, strategically managed and utilized, can be a silent yet powerful indicator of foresight and fiscal responsibility. It reflects a proactive approach to life’s uncertainties, a trait highly valued in both personal and professional spheres.

Maximizing Your HSA for Long-Term Financial Health and Well-being

Understanding the maximum contribution limits is only the first step. Truly leveraging an HSA involves strategic planning and consistent action. Here’s how you can maximize its benefits for both immediate health needs and long-term financial security, especially with the support of modern tech tools.

Automating Contributions and Investing Wisely

The simplest way to ensure you meet the maximum contribution limit is to automate your savings. Most employers allow you to set a percentage or a fixed amount to be deducted from your paycheck each pay period directly into your HSA. For those who are self-employed or not offered an employer-sponsored HSA, setting up automatic transfers from your checking account to your HSA provider is equally effective.

Once your HSA reaches a sufficient balance, consider investing the funds. Look for HSA providers that offer a range of investment options, similar to a 401(k) plan. Diversify your portfolio based on your risk tolerance and time horizon. For younger individuals, a more aggressive investment strategy might be suitable, while those closer to retirement may opt for more conservative investments. Many FinTech apps now offer integrated HSA investment management tools, providing insights and rebalancing capabilities at your fingertips.

Leveraging Technology for Smart Healthcare Spending

The integration of technology into healthcare management can further enhance the value of your HSA. Many health insurance providers and HSA administrators offer online portals or apps where you can:

- Track Expenses: Easily log and categorize medical expenses, ensuring you have accurate records for tax purposes.

- Submit Claims: Streamline the reimbursement process for qualified medical expenses.

- Research Providers and Treatments: Use online resources to compare costs for procedures and medications, helping you make more cost-effective decisions. This is where the intersection of tech and money becomes particularly potent. By researching the best prices for necessary medical care, you directly reduce your out-of-pocket expenses, leaving more funds in your HSA to grow.

- Access Educational Content: Many platforms provide articles, webinars, and tools to help you understand your health plan benefits and HSA utilization better.

By actively engaging with these digital tools, you can make more informed healthcare choices, reduce unnecessary spending, and ultimately preserve and grow your HSA balance. This proactive approach to health and wealth management aligns perfectly with the principles of smart personal branding – demonstrating competence, foresight, and a strategic approach to life’s challenges.

Understanding the Long-Term Benefits: Beyond Healthcare

It’s crucial to remember that HSAs are designed for long-term savings. While immediate healthcare needs are the primary purpose, the funds can be used for any qualified medical expense throughout your lifetime, and even passed on to beneficiaries tax-free. This makes the HSA an incredibly versatile financial tool.

As you approach retirement, if you haven’t utilized all your HSA funds for medical expenses, you can withdraw the money without penalty after age 65. At that point, the withdrawals are taxed as ordinary income, similar to withdrawals from a traditional IRA or 401(k). However, you still retain the benefit of tax-free growth accumulated over the years. This makes the HSA a powerful supplement to traditional retirement savings, especially for those who have managed to consistently contribute the maximum allowed amount.

In conclusion, staying informed about the maximum HSA contribution for 2025 is more than just a financial exercise; it’s a strategic move towards securing your future. By understanding the factors influencing these limits, utilizing modern technology to manage your finances and healthcare, and planning for long-term growth, you can transform your HSA into a cornerstone of your financial resilience. As the world continues to embrace digital solutions for every aspect of life, the smart management of your HSA stands as a testament to your proactive approach to building a secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.