Keynesian theory, named after British economist John Maynard Keynes, represents a fundamental shift in economic thought, particularly concerning the role of government in managing economic stability. Developed in response to the devastating Great Depression of the 1930s, it challenged the prevailing classical economic belief that free markets would naturally self-correct from recessions and achieve full employment. Instead, Keynesian economics posits that aggregate demand—the total spending in an economy—is the primary driver of economic activity, and that insufficient demand can lead to prolonged periods of high unemployment and underutilized productive capacity. For individuals, businesses, and investors, understanding Keynesian principles offers critical insights into governmental financial policy, market trends, and the underlying forces shaping economic cycles.

The Roots of a Revolution: Understanding the Great Depression’s Impact

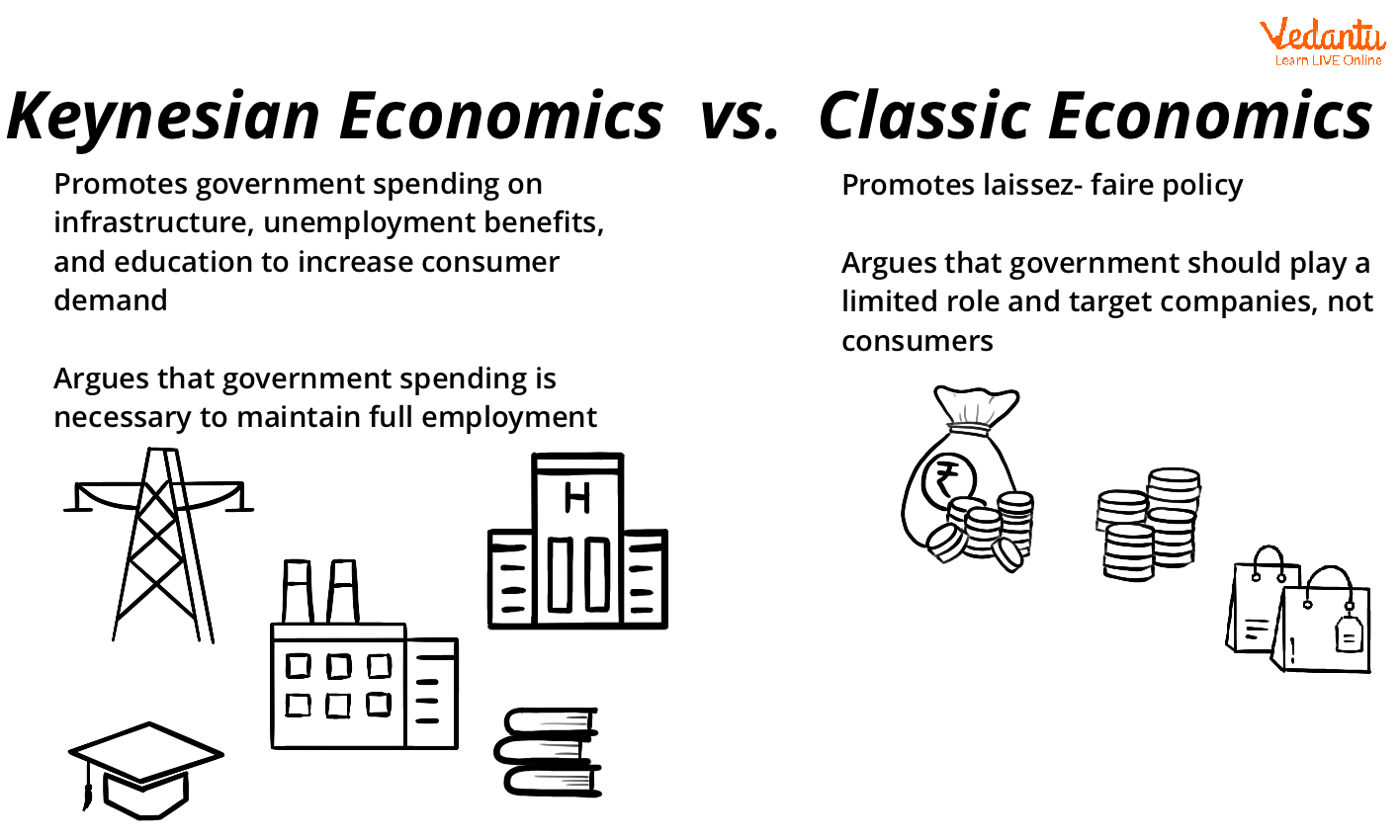

Before Keynes, classical economics held sway, advocating for minimal government intervention. This school of thought, rooted in Adam Smith’s “invisible hand,” believed that market forces, including flexible wages and prices, would automatically adjust to ensure full employment and efficient resource allocation. Recessions were seen as temporary aberrations that the market would naturally correct given enough time. However, the Great Depression, with its unprecedented levels of unemployment, business failures, and prolonged economic stagnation, severely tested and ultimately discredited these classical assumptions. Factories stood idle, not because workers were unavailable or capital lacking, but because there was insufficient demand for their products. Millions were jobless, not due to an unwillingness to work, but because businesses had no incentive to hire them in the face of dwindling sales.

John Maynard Keynes, in his seminal 1936 work, The General Theory of Employment, Interest and Money, offered a radical alternative explanation. He argued that economies could get stuck in equilibrium below full employment, a state where market forces alone were insufficient to restore prosperity. He observed that during severe downturns, a vicious cycle could emerge: falling incomes lead to reduced spending, which further dampens production, leading to more job losses and even lower incomes. This created a powerful theoretical framework for understanding why the Great Depression persisted and, crucially, what could be done to counteract it. For any business operating in a volatile economy, or an investor seeking to navigate market downturns, Keynes’s insights into the potential for persistent disequilibrium remain highly relevant, framing the potential for governmental response to financial crises.

Core Tenets of Keynesian Economics

Keynesian theory introduced several groundbreaking concepts that continue to inform macroeconomic policy and influence financial markets today. These principles explain how economic downturns occur and provide a framework for governmental action.

Aggregate Demand as the Primary Driver

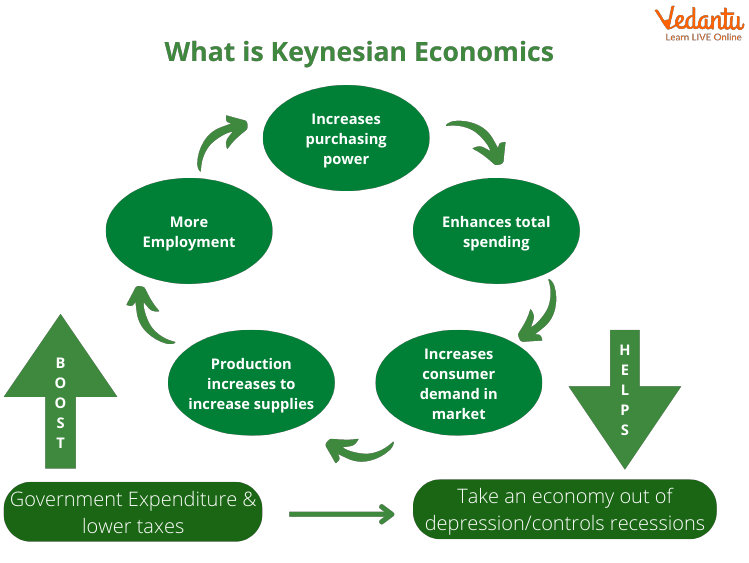

At the heart of Keynesian economics is the concept of aggregate demand (AD), defined as the total demand for all goods and services produced in an economy. It comprises consumption (C), investment (I), government spending (G), and net exports (NX). Keynes argued that it is insufficient aggregate demand, not a lack of supply or structural issues, that causes unemployment and recessions. If consumers are hesitant to spend, businesses are reluctant to invest, and exports fall, the overall demand for goods and services declines. This leads firms to reduce production, lay off workers, and postpone investments, even if their productive capacity remains intact. For businesses, this means that understanding the factors influencing aggregate demand—consumer confidence, interest rates, government fiscal policy, and global trade dynamics—is paramount to strategic planning and financial forecasting. Investors, too, must track these indicators as they signal potential shifts in corporate earnings and overall market performance.

The Role of Government Intervention

Unlike classical economists, Keynes advocated for active government intervention to stabilize the economy. He argued that when private sector demand (consumption and investment) falls, the government must step in to fill the gap.

Fiscal Policy

This involves the government directly influencing aggregate demand through its spending and taxation policies. During a recession, Keynesians advocate for expansionary fiscal policy:

- Increased Government Spending: Investing in infrastructure projects, social programs, or direct aid can create jobs, boost incomes, and stimulate demand. For construction firms, material suppliers, and service providers, government contracts become a vital revenue stream during economic slumps.

- Tax Cuts: Reducing taxes leaves more disposable income in the hands of consumers and businesses, encouraging spending and investment. This can provide a critical liquidity injection for small businesses and incentivize larger corporations to expand.

Conversely, during periods of rapid growth and potential inflation, Keynesians recommend contractionary fiscal policy:

- Reduced Government Spending: To cool down an overheating economy and prevent excessive price increases.

- Tax Increases: To reduce disposable income and curb demand.

Monetary Policy

While Keynes’s primary focus was on fiscal policy, his work also laid the groundwork for modern central banking’s role in managing the money supply and interest rates. Central banks can lower interest rates to make borrowing cheaper, encouraging investment and consumption, or raise them to slow down an economy. For businesses, understanding these policy shifts is crucial for managing debt, planning capital expenditures, and assessing the cost of financing. Investors closely monitor interest rate announcements, as they directly impact bond yields, stock valuations, and currency exchange rates.

The Paradox of Thrift

A counterintuitive but central Keynesian concept is the “paradox of thrift.” During an economic downturn, individuals and businesses may rationally choose to save more and spend less, driven by uncertainty about the future. While saving is generally considered a virtue, if everyone collectively increases their saving and reduces spending, aggregate demand plummets further. This collective action, intended to improve individual financial security, can deepen and prolong a recession, leading to lower overall income and employment, making everyone worse off. For financial planners, this highlights the societal consequences of individual financial decisions when aggregated, underscoring the need for a macroeconomic perspective.

The Multiplier Effect

Keynes introduced the concept of the “multiplier effect,” which suggests that an initial injection of spending into the economy can lead to a much larger overall increase in national income. For example, if the government spends $100 million on a new road project, that money becomes income for construction workers and suppliers. These recipients, in turn, spend a portion of their new income, which becomes income for others, and so on. The impact ripples through the economy, with each round of spending generating additional demand. The size of the multiplier depends on the marginal propensity to consume (MPC)—the fraction of new income that people spend rather than save. Understanding the multiplier effect is crucial for businesses evaluating the potential impact of government stimulus packages and for investors anticipating the ripple effects of major public works projects or tax rebates across various sectors.

Sticky Wages and Prices

Keynes observed that wages and prices do not adjust instantly downward during a recession, a phenomenon known as “sticky wages” and “sticky prices.” Due to labor contracts, minimum wage laws, union power, and psychological resistance to wage cuts, workers’ pay often remains rigid even when unemployment is high. Similarly, businesses may be reluctant to cut prices due to production costs, fear of price wars, or the perception of quality reduction. This stickiness prevents markets from rapidly clearing, meaning that unemployment can persist for extended periods, as firms cannot easily lower labor costs or prices to stimulate demand. This insight helps explain why a recession can be prolonged, making financial planning more challenging for individuals and requiring businesses to adjust to slower demand rather than simply cutting prices.

Keynesianism in Practice: Policy Applications and Impact on Business Finance

Keynesian principles have profoundly influenced economic policy worldwide, particularly in managing business cycles and responding to financial crises. Its practical application directly affects the financial landscape for businesses and investors.

Counter-Cyclical Policies

The most visible application of Keynesian theory is the use of counter-cyclical policies. During recessions, governments employ expansionary measures like increased spending or tax cuts to stimulate demand. Examples include the New Deal programs in the US during the Great Depression, the global stimulus packages following the 2008 financial crisis, and the vast government spending and unemployment benefits during the COVID-19 pandemic. These policies aim to cushion the economic blow, prevent widespread business failures, and expedite recovery. For businesses, these interventions can mean the difference between survival and bankruptcy, with direct benefits from government contracts, increased consumer spending, or access to subsidized credit. Investors track these policies closely, as they can indicate which sectors might receive a boost (e.g., infrastructure, healthcare, technology during remote work mandates) and can influence the overall trajectory of equity and bond markets.

Conversely, during periods of economic overheating and inflationary pressure, Keynesian theory suggests governments should implement contractionary policies—reducing spending or raising taxes—to cool down demand. While often politically challenging, the theoretical aim is to prevent asset bubbles and unsustainable price increases, which can ultimately damage long-term financial stability.

Implications for Investors and Businesses

Understanding Keynesian policies is critical for strategic financial decisions:

- Market Dynamics: Government spending and taxation directly influence aggregate demand, which in turn drives corporate revenues and profitability. Businesses need to anticipate these shifts to adjust production, inventory, and staffing levels.

- Sector-Specific Impacts: Fiscal policy is rarely uniform. Infrastructure spending benefits construction, materials, and engineering firms. Healthcare reforms impact pharmaceutical companies and service providers. Defense spending bolsters aerospace and security industries. Investors can identify potential growth areas or vulnerabilities based on the government’s budgetary priorities.

- Inflation and Interest Rates: Expansionary fiscal policies, especially when coupled with accommodative monetary policy, can lead to inflation. Businesses must manage rising input costs and adjust pricing strategies. Investors must consider the erosion of purchasing power and seek investments that offer inflation protection. Monetary policy, guided by central banks, directly influences borrowing costs for businesses and the returns on fixed-income investments.

- Predicting Economic Cycles: By observing government rhetoric and policy actions (e.g., discussions about stimulus vs. austerity), businesses and investors can gain insights into the likely direction of the economy and anticipate subsequent market reactions.

Debt and Deficits

A key debate around Keynesian policy revolves around government debt. Keynes argued that during a severe downturn, accumulating national debt through deficit spending is not only permissible but necessary to avoid a deeper crisis. The long-term economic damage of a prolonged recession, he contended, would far outweigh the costs of increased public debt. The goal is to return the economy to full employment, at which point tax revenues would naturally increase, and deficits could be reduced. However, critics often raise concerns about the sustainability of public debt, its potential to “crowd out” private investment, and the burden on future generations. For business finance, significant national debt can influence interest rates, bond markets, and the perceived stability of a nation’s economy, affecting foreign investment and currency values.

Criticisms and Evolution of Keynesian Thought

While immensely influential, Keynesian theory has faced substantial criticism and has evolved significantly over time.

The Challenge of Implementation

One practical critique is the difficulty of implementing Keynesian policies effectively and precisely.

- Political Feasibility: Cutting spending or raising taxes during boom times to prevent inflation is often politically unpopular. Conversely, distributing stimulus effectively and without corruption during a recession can be challenging.

- Time Lags: There are often significant time lags between recognizing an economic problem, formulating a policy response, enacting it, and seeing its effects. By the time a fiscal stimulus kicks in, the economy might already be recovering on its own, potentially leading to overheating or misallocation of resources.

- Measurement Challenges: Accurately gauging the size of the output gap (the difference between potential and actual output) or the precise value of the multiplier effect is difficult, making it hard to calibrate policy interventions correctly. For financial analysts, these implementation hurdles mean that policy outcomes are rarely as clean as theoretical models suggest, adding complexity to market predictions.

“Crowding Out” Effect

A significant criticism, particularly from classical and monetarist economists, is the “crowding out” effect. This theory suggests that extensive government borrowing to finance deficit spending can increase demand for credit, driving up interest rates. Higher interest rates then make it more expensive for private businesses to borrow and invest, thereby “crowding out” private sector investment and potentially negating some of the positive effects of government stimulus. For companies considering capital expenditures, higher interest rates directly impact the profitability of their projects, making careful financial planning and cost-of-capital analysis even more critical.

Stagflation and the Rise of New Schools

The 1970s presented a major challenge to traditional Keynesianism with the phenomenon of “stagflation”—simultaneous high inflation and high unemployment. Keynesian theory struggled to explain this, as it typically linked high unemployment to low demand and thus low inflation. This era gave rise to alternative economic schools of thought, such as monetarism (led by Milton Friedman), which emphasized the role of the money supply in controlling inflation, and supply-side economics, which focused on policies to boost production and reduce regulatory burdens. The inability of pure demand-side management to address stagflation forced an evolution in macroeconomic thinking.

Neoclassical Synthesis and New Keynesianism

Despite these criticisms, Keynesian ideas did not disappear but rather evolved. The “neoclassical synthesis” integrated Keynesian insights on market failures and government intervention with classical microeconomic foundations. More recently, “New Keynesian economics” has sought to provide microeconomic explanations for sticky wages and prices, rationalizing why markets do not always clear efficiently. These modern iterations retain the core belief that market imperfections can lead to suboptimal outcomes and that active government policy has a crucial role in stabilizing the economy. For modern businesses and investors, this means that while market forces are powerful, governmental and central bank actions remain a central variable in the financial equation, influencing everything from interest rates and inflation to industry-specific growth prospects. Understanding the theoretical underpinnings of these actions provides a vital framework for navigating complex financial landscapes.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.