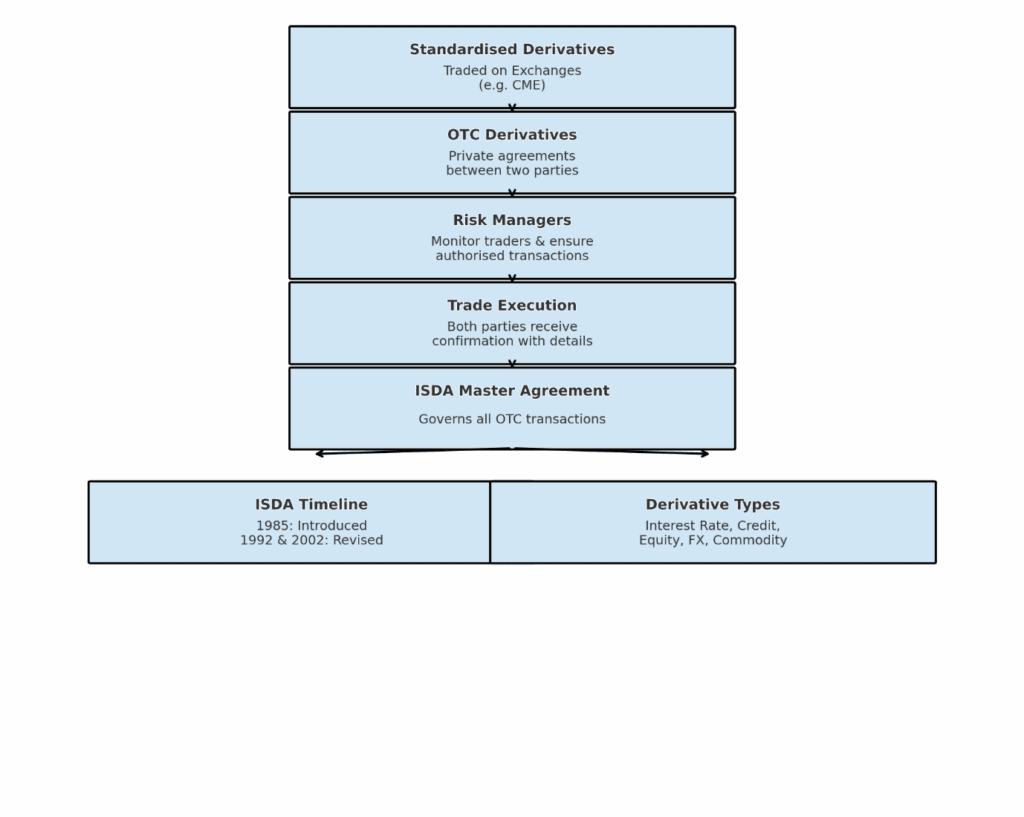

The International Swaps and Derivatives Association (ISDA) Master Agreement is a cornerstone of the global financial markets, providing a standardized framework for over-the-counter (OTC) derivatives transactions. While the term “agreement” might suggest a simple contract, the ISDA Master Agreement is a sophisticated legal document designed to reduce the risks inherent in complex financial instruments. Understanding its structure, purpose, and implications is crucial for anyone involved in the derivatives market, from large financial institutions to sophisticated corporate treasuries.

The Genesis and Purpose of the ISDA Master Agreement

The ISDA Master Agreement emerged from a recognized need for standardization and clarity in the burgeoning OTC derivatives market. Before its widespread adoption, transactions were often governed by bespoke, bilateral agreements, leading to inconsistencies, legal uncertainties, and increased counterparty risk. ISDA, established in 1985, set out to address these challenges by creating a globally accepted template that streamlined negotiations and enhanced market efficiency.

Addressing Counterparty Risk in Derivatives

At its core, the ISDA Master Agreement is a tool to manage counterparty risk, which is the risk that one party to a contract will default on its obligations. In derivatives, where parties exchange future cash flows based on underlying assets, this risk can be substantial. The agreement introduces several mechanisms to mitigate this:

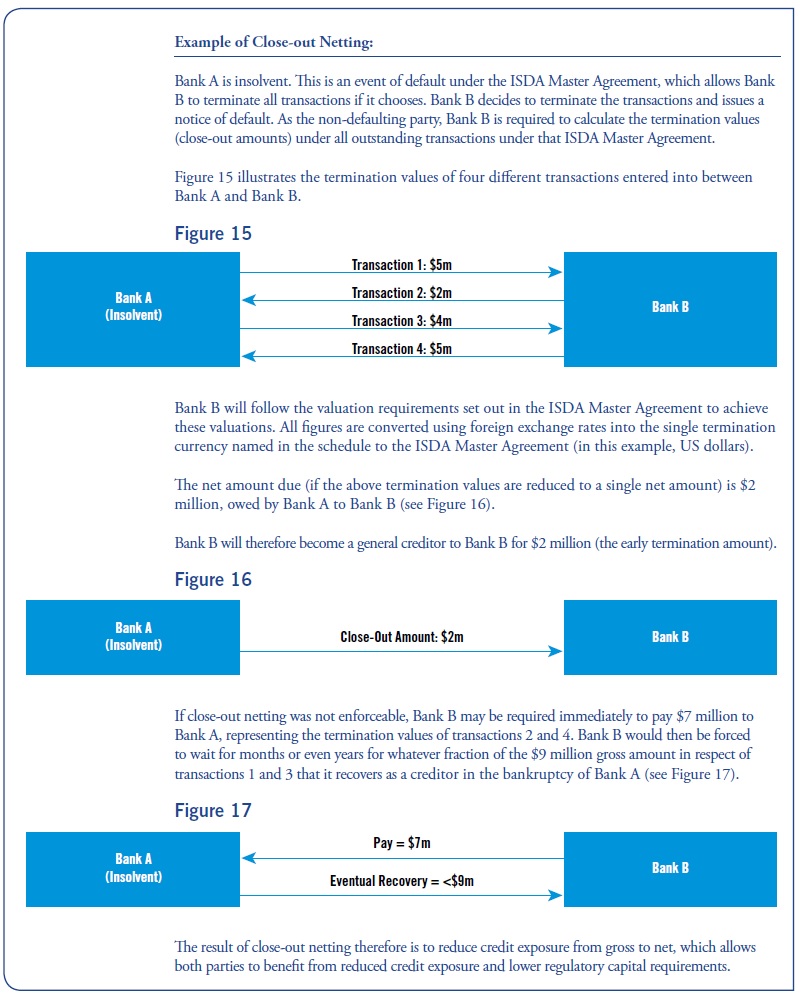

- Netting: Perhaps the most significant feature of the ISDA Master Agreement is its robust netting provisions. In the event of a default by one party, netting allows for the offsetting of all outstanding obligations between the two parties. Instead of demanding full payment for each defaulted transaction, the non-defaulting party calculates a single net amount owed. This dramatically reduces the exposure and the potential for cascading defaults throughout the financial system.

- Collateralization: The agreement facilitates the posting of collateral by parties to secure their obligations. This is often achieved through an accompanying ISDA Credit Support Annex (CSA). The CSA specifies the type and amount of collateral required, how it is valued, and the conditions under which it can be called upon. This acts as a buffer against losses if a counterparty defaults and the market has moved unfavorably.

- Cross-Default Provisions: Many ISDA Master Agreements include cross-default clauses. This means that a default on one financial obligation (not necessarily related to the ISDA agreement itself) can trigger a default under the ISDA agreement, allowing for immediate termination and netting of all covered transactions. This provides a broader protection against a counterparty’s overall financial distress.

Standardization and Efficiency in OTC Markets

The OTC derivatives market is characterized by its flexibility and ability to tailor contracts to specific needs. However, this flexibility can lead to lengthy and costly negotiation processes. The ISDA Master Agreement provides a common foundation, significantly reducing the time and expense involved in documenting new trades.

- Reduced Negotiation Time: By establishing a widely understood and accepted set of terms, parties can focus their negotiations on the specific economic terms of the derivative transaction, rather than on fundamental legal concepts. This allows for faster execution of trades, which is critical in volatile markets.

- Enhanced Liquidity: A standardized framework fosters greater confidence among market participants. This increased confidence contributes to higher liquidity in the OTC derivatives market, making it easier for parties to enter and exit positions.

- Regulatory Compliance: The ISDA Master Agreement is designed to be compatible with various regulatory regimes worldwide. As regulations have evolved, ISDA has continually updated its documentation to ensure continued compliance, providing a reliable legal basis for derivative activities.

Key Components of the ISDA Master Agreement

While the ISDA Master Agreement is a single document, it is typically accompanied by several other schedules and annexes that tailor its application to specific circumstances. Understanding these components is essential for comprehending its full scope.

The Master Agreement Document Itself

The Master Agreement document is the overarching legal framework. It contains the fundamental terms and conditions governing the relationship between the two parties. Key sections typically include:

- Definitions: This section defines crucial terms used throughout the agreement, such as “Affiliate,” “Business Day,” “Confidential Information,” and “Termination Event.” Precise definitions are critical to avoid ambiguity.

- Obligations: This outlines the basic undertaking of each party to enter into transactions.

- Representations: Parties provide assurances about their legal capacity, authorization, and financial standing.

- Agreements: This section covers various covenants, such as the obligation to provide information, the confidentiality of trades, and compliance with laws.

- Events of Default and Termination Events: This is a critical part of the agreement, defining the circumstances under which a party can terminate the agreement and trigger netting. Events of Default are more severe breaches, while Termination Events are broader, often relating to external factors.

- Calculation of Payments and Deliveries: This details how payments and deliveries are to be made, including the methodology for determining amounts in the event of termination.

- Miscellaneous Provisions: This includes standard legal clauses such as governing law, jurisdiction, notices, and entire agreement clauses.

The Schedule: Tailoring the Master Agreement

The Schedule is an integral part of the ISDA Master Agreement, allowing parties to customize certain provisions to their specific needs and regulatory requirements. It is appended to the Master Agreement and forms part of it.

- Elective Provisions: The Schedule allows parties to elect various options and provisions. For example, parties can choose whether to include certain types of collateral or specific termination events.

- Trade Confirmation Incorporation: It clarifies how trade confirmations, which detail the specific terms of each individual derivative transaction, are incorporated into the overall agreement.

- Credit Support Annex Selection: The Schedule is where parties will typically specify whether a Credit Support Annex is in effect and which annex they are using.

- Governing Law and Jurisdiction: While the Master Agreement may have a default, the Schedule can specify the preferred governing law and jurisdiction for dispute resolution, which can be crucial for cross-border transactions.

The Credit Support Annex (CSA): The Collateral Mechanism

The ISDA Credit Support Annex (CSA) is a separate but often inseparable document from the ISDA Master Agreement, particularly for transactions where collateral is required. It provides the detailed framework for how collateral is managed.

- Collateral Amount and Valuation: The CSA specifies how the “Initial Margin” (a fixed amount of collateral posted upfront) and “Variation Margin” (collateral that fluctuates with the mark-to-market value of the trades) are determined. It also details the methodology for valuing the collateral and the underlying transactions.

- Eligible Collateral: The annex lists the types of assets that can be used as collateral (e.g., cash, government bonds).

- Triggering Events for Collateral Call: It outlines the thresholds and conditions that trigger a party’s obligation to post additional collateral.

- Dispute Resolution for Collateral: Provisions are made for resolving disputes regarding collateral calculations or valuation.

- Rehypothecation Rights: The CSA will typically address whether the recipient of collateral has the right to rehypothecate (reuse) that collateral.

ISDA Definitions: The Building Blocks of Derivatives

Beyond the Master Agreement itself, ISDA publishes a comprehensive set of “Definitions” which are fundamental to understanding and documenting specific types of derivatives. These are not part of the Master Agreement but are usually incorporated by reference via trade confirmations or specific elections in the Schedule.

Interest Rate Derivatives Definitions

These definitions provide standardized terms for interest rate swaps, caps, floors, and other related instruments. They cover:

- Interest Rate Matrices: Standardized conventions for calculating interest rates for various currencies and tenors.

- Reset Dates and Payment Dates: Clear definitions for when interest rates are reset and when payments are made.

- Day Count Conventions: Standardized methods for calculating accrued interest over specific periods.

Equity Derivatives Definitions

These definitions are used for derivatives whose underlying asset is an equity security or index. They address:

- Share Adjustments: How corporate actions (e.g., stock splits, dividends) affect the terms of the derivative.

- Cash Settlement vs. Physical Settlement: Provisions for how payoffs are calculated and delivered.

- Index Definitions: Standardized definitions for major equity indices.

Credit Derivatives Definitions

These definitions are used for credit default swaps (CDS) and other credit derivative products. They define:

- Credit Events: What constitutes a default or creditworthiness deterioration that triggers a payout (e.g., bankruptcy, failure to pay).

- Reference Entities and Obligations: Precise identification of the credit the derivative is based upon.

- Settlement Mechanisms: How the payout is calculated and delivered upon the occurrence of a credit event.

Foreign Exchange and Other Derivatives Definitions

ISDA also publishes definitions for currency swaps, commodity derivatives, and other complex financial instruments, ensuring a consistent language across diverse markets.

The Significance and Evolution of the ISDA Agreement

The ISDA Master Agreement has evolved significantly since its inception, adapting to market changes, new product innovations, and evolving regulatory landscapes. Its continued relevance underscores its importance in maintaining stability and facilitating trade in the global financial system.

Adapting to Market Evolution and Innovation

The derivatives market is dynamic, with constant innovation in product design. ISDA has played a crucial role in developing standardized documentation for these new products, ensuring they can be traded efficiently and with appropriate risk management. This includes:

- New Product Addenda: ISDA regularly releases addenda and protocols to the Master Agreement to accommodate new types of derivatives.

- Documentation for Emerging Markets: As derivatives markets grow in developing economies, ISDA documentation has been adapted to suit local legal and market practices.

Responding to Regulatory Changes

The post-financial crisis era has seen a significant increase in derivatives regulation globally. ISDA has been at the forefront of developing documentation that aligns with these new requirements, such as:

- Dodd-Frank Act Compliance: ISDA provided guidance and documentation for compliance with the U.S. Dodd-Frank Wall Street Reform and Consumer Protection Act, particularly regarding central clearing and trade execution.

- European Market Infrastructure Regulation (EMIR): Similarly, ISDA has facilitated compliance with EMIR in Europe.

- Margin Reforms for Uncleared Derivatives: ISDA has been instrumental in developing the framework for posting initial and variation margin for uncleared derivatives, as mandated by global regulators.

The Role of ISDA in Global Financial Stability

By providing a standardized, robust, and continuously updated framework for OTC derivatives, the ISDA Master Agreement contributes significantly to global financial stability. Its emphasis on netting and collateralization directly addresses the systemic risks that can arise from unmanaged counterparty exposures. The widespread adoption of ISDA documentation fosters trust and predictability, enabling the efficient allocation of capital and the effective hedging of risks, which are vital for a healthy global economy.

In conclusion, the ISDA Agreement is far more than a simple contract; it is a sophisticated legal and operational framework that underpins a vast portion of the global financial markets. Its comprehensive nature, focus on risk mitigation, and continuous evolution make it an indispensable tool for any entity engaged in the complex world of derivatives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.