Insurance and reinsurance are fundamental pillars of the modern financial system, providing a crucial mechanism for risk management and financial stability. While often discussed together, they represent distinct yet interconnected layers of protection against the uncertainties of life and business. Understanding these concepts is essential for individuals, businesses, and even entire economies to navigate potential financial perils and ensure resilience.

The Core Concept of Insurance: Spreading and Pooling Risk

At its heart, insurance is a contract. An individual or entity (the insured) pays a premium to an insurance company (the insurer) in exchange for financial protection against specific, defined losses. This exchange is built on the principle of pooling risk. A large number of individuals or entities, each facing a similar potential risk (e.g., a car accident, a house fire, a serious illness), contribute relatively small amounts of money (premiums) into a common pool. When a loss occurs for one member of the pool, the accumulated funds from all members are used to compensate that individual.

This pooling mechanism is what makes insurance feasible. Without it, the financial burden of a catastrophic event on a single individual would be insurmountable. Insurance companies, through actuarial science and statistical analysis, calculate the probability of these events occurring and the likely cost of claims. This allows them to set premiums that are sufficient to cover expected losses, administrative expenses, and generate a profit, while remaining affordable for the insured.

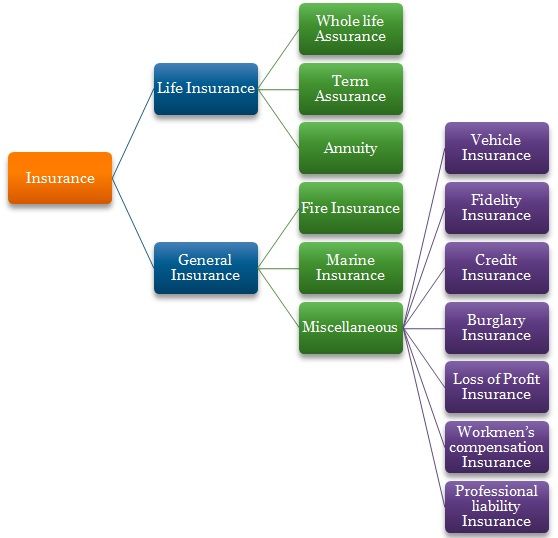

Types of Insurance and Their Applications

The application of insurance is vast, covering nearly every conceivable risk. Broadly, these can be categorized by the type of risk they mitigate:

Property and Casualty Insurance

This category protects against damage to or loss of property, as well as liability for damage or injury caused to others.

- Homeowners Insurance: Covers damage to a dwelling and its contents from perils like fire, theft, and natural disasters. It also provides liability coverage if someone is injured on the property.

- Auto Insurance: Protects against financial loss due to car accidents, theft, or damage to the vehicle. It typically includes liability coverage for damage or injury to others, as well as collision and comprehensive coverage for the insured’s vehicle.

- General Liability Insurance: Essential for businesses, this covers claims of bodily injury or property damage caused by the business’s operations, products, or on its premises.

- Professional Liability Insurance (Errors & Omissions): Protects professionals (doctors, lawyers, consultants) against claims of negligence or inadequate service that result in financial loss for their clients.

Life and Health Insurance

These types of insurance focus on protecting individuals and their dependents from financial consequences related to health and mortality.

- Life Insurance: Provides a death benefit to designated beneficiaries upon the insured’s death. This can help replace lost income, cover funeral expenses, or provide for long-term financial needs of dependents.

- Health Insurance: Covers medical expenses, including doctor visits, hospital stays, prescription drugs, and preventive care. This is crucial for managing the often-significant costs of healthcare.

- Disability Insurance: Provides income replacement if the insured becomes unable to work due to illness or injury.

Specialty Insurance

Beyond these common types, numerous specialty insurance products exist to cover unique or high-risk scenarios.

- Cyber Insurance: Addresses the growing risks associated with data breaches, cyberattacks, and other digital security incidents.

- Event Cancellation Insurance: Protects organizers from financial losses if an event must be canceled or postponed due to unforeseen circumstances.

- Flood Insurance: Specifically covers damage from flooding, which is often excluded from standard homeowners policies.

The fundamental purpose of all these insurance products remains the same: to transfer risk from an individual or entity to an insurance company, thereby providing financial security and peace of mind.

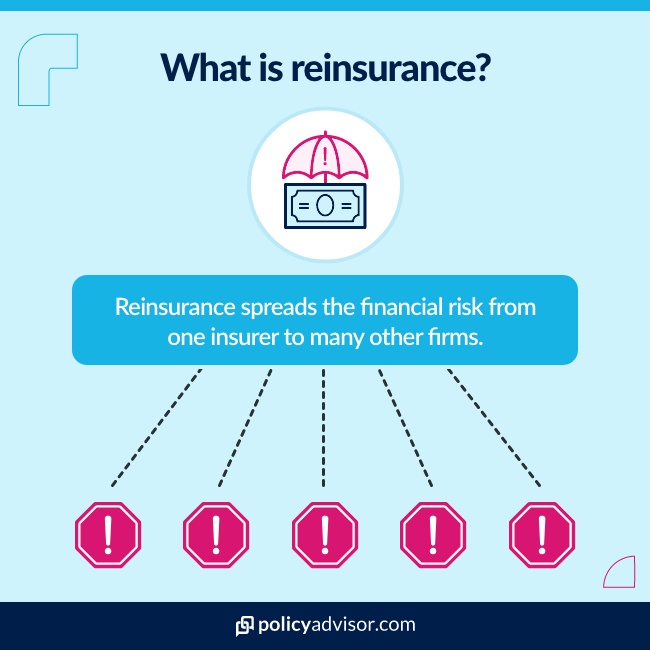

Reinsurance: Insurance for Insurers

While insurance allows individuals and businesses to transfer their risks, insurance companies themselves are exposed to significant risks. A single catastrophic event, such as a major hurricane, earthquake, or a widespread pandemic, could result in claims that overwhelm an insurer’s financial capacity. This is where reinsurance comes into play.

Reinsurance is essentially “insurance for insurance companies.” A primary insurer transfers a portion of its risk portfolio to a reinsurer in exchange for a portion of the premium. This process allows insurers to:

- Increase Capacity: By sharing risk, an insurer can underwrite larger policies or cover more risks than it could on its own. This is particularly important for large infrastructure projects, major corporations, or high-value assets.

- Stabilize Earnings: Reinsurance smooths out the impact of large or unexpected claims, preventing extreme volatility in an insurer’s financial results.

- Reduce Capital Requirements: By transferring some of its risk, an insurer may be able to reduce the amount of capital it needs to hold in reserve, freeing up capital for other investments or growth initiatives.

- Gain Expertise: Reinsurers often possess specialized knowledge and analytical capabilities that can benefit the primary insurer, particularly in understanding and managing complex risks.

The Mechanics of Reinsurance

Reinsurance contracts, known as treaties, can be structured in several ways:

Treaty Reinsurance

In treaty reinsurance, the reinsurer agrees to accept a certain portion of a specific class of risks written by the ceding insurer (the primary insurer) over a defined period. This provides automatic coverage for all risks falling within the treaty’s scope.

-

Proportional Reinsurance: In this type of treaty, the reinsurer shares both the premiums and the losses in agreed-upon proportions.

- Quota Share Treaty: The reinsurer accepts a fixed percentage of every risk within the treaty. For example, the insurer might cede 30% of all its auto insurance policies to a reinsurer. The reinsurer receives 30% of the premiums and pays 30% of the claims.

- Surplus Share Treaty: The insurer retains a certain amount of risk (its “net retention”) for each policy and reinsures the excess, up to a specified limit. This allows the insurer to write larger policies by sharing the amount exceeding its retention.

-

Non-Proportional Reinsurance: In this type, the reinsurer only pays when losses exceed a predetermined threshold. The premium paid to the reinsurer is typically a flat fee, not directly tied to the proportion of premiums ceded.

- Excess of Loss (XOL) Treaty: The reinsurer agrees to pay all losses that exceed a specified amount per occurrence or per event. For instance, an insurer might have an XOL treaty that covers all losses above $5 million from a single event.

- Stop-Loss Treaty: This protects the insurer from an accumulation of losses over a period, rather than individual large claims. The reinsurer pays losses that exceed a certain percentage of the insurer’s total premium income during the contract term.

Facultative Reinsurance

Facultative reinsurance is negotiated on a case-by-case basis. When a primary insurer has a risk that is too large, unusual, or complex to fit within its existing treaties, it can seek facultative reinsurance from one or more reinsurers. This allows for greater flexibility but is generally more time-consuming and expensive than treaty reinsurance.

The reinsurer has the option (faculty) to accept or reject each individual risk submitted by the ceding insurer. This is often used for unique or high-value risks, such as insuring a specific skyscraper, a major sporting event, or a unique industrial facility.

The reinsurance market is a global one, with highly specialized reinsurers playing a critical role in the stability and capacity of the global insurance industry. They act as a vital backstop, absorbing risks that would otherwise be too concentrated for primary insurers to handle alone.

The Interplay Between Insurance and Reinsurance

The relationship between insurance and reinsurance is symbiotic. Without insurance, individuals and businesses would be vulnerable to financial ruin from unforeseen events. Without reinsurance, the insurance industry itself would be unable to bear the full weight of potential catastrophes, limiting its capacity and ultimately its ability to serve its societal function.

Economic and Societal Impact

The combined force of insurance and reinsurance contributes significantly to economic stability and growth.

- Facilitating Business Investment: By providing protection against property damage, business interruption, and liability, insurance enables businesses to undertake investments and operations that would otherwise be too risky. This fosters innovation, job creation, and economic development.

- Promoting Risk Mitigation: The availability of insurance incentivizes individuals and businesses to adopt risk mitigation strategies. For example, fire insurance encourages the installation of smoke detectors and sprinkler systems, while auto insurance encourages safer driving practices.

- Disaster Recovery: In the aftermath of natural disasters, insurance payouts play a crucial role in helping individuals and communities rebuild. Reinsurance ensures that even in widespread catastrophic events, the insurance industry has the capacity to meet these massive claims.

- Financial Market Stability: The insurance and reinsurance sectors are significant participants in global financial markets, investing premiums in a diverse range of assets. Their stability contributes to the overall health of the financial system.

Challenges and Evolution

Both insurance and reinsurance are dynamic industries constantly evolving to meet new challenges and opportunities.

- Emerging Risks: The rise of new risks, such as climate change (leading to more frequent and severe weather events), pandemics, and cyber threats, requires insurers and reinsurers to develop new products, models, and underwriting capabilities.

- Technological Advancements: Technology is transforming the insurance landscape. Insurtech companies are leveraging data analytics, artificial intelligence, and blockchain to improve underwriting, claims processing, customer experience, and fraud detection. Reinsurers are also adopting these technologies to enhance their risk assessment and management capabilities.

- Regulatory Landscape: The insurance and reinsurance industries are heavily regulated to ensure solvency and protect policyholders. Navigating complex and evolving regulatory frameworks is a constant challenge.

- Capital Markets Integration: There is an increasing convergence between the insurance and capital markets, with alternative capital providers (like pension funds and hedge funds) entering the reinsurance market through instruments such as catastrophe bonds. This provides additional capacity and can offer different risk-return profiles.

In conclusion, insurance and reinsurance are indispensable tools for managing risk and fostering financial security. Insurance empowers individuals and businesses to protect themselves against specific losses, while reinsurance acts as a critical safety net for the insurers themselves, enabling them to take on greater risks and operate with greater stability. Together, they form a robust framework that underpins economic activity, promotes resilience, and provides a vital buffer against the unpredictable nature of the world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.