In the intricate landscape of automotive finance, the acquisition of a new or used vehicle often involves securing a loan. While the excitement of a new set of wheels is palpable, the financial realities of car ownership, particularly the rapid depreciation of an asset, can present significant risks. This is precisely where Gap (Guaranteed Asset Protection) coverage emerges as a critical financial tool, safeguarding consumers from a potentially devastating financial shortfall in the event of a total loss. Understanding gap coverage is not merely about an insurance product; it’s about shrewd personal finance management and mitigating unforeseen debt.

Understanding the Depreciation Dilemma: Why Gap Coverage Exists

The moment a new car drives off the lot, its value typically depreciates significantly. This immediate and ongoing loss of value creates a fundamental financial vulnerability for car owners who finance their purchases. Unlike real estate, which can often appreciate or hold its value over time, vehicles are generally depreciating assets. This rapid decline in market value often outpaces the rate at which a loan balance is paid down, leading to a precarious financial situation if the vehicle is totaled or stolen.

The “Gap” Explained: Loan-to-Value Discrepancy

At the heart of the need for gap coverage is the loan-to-value (LTV) discrepancy. When a vehicle is purchased with a loan, the principal amount financed often exceeds the car’s actual cash value (ACV) from day one, especially after factoring in taxes, registration fees, and other upfront costs that are rolled into the loan. Traditional auto insurance policies are designed to cover the vehicle’s ACV at the time of loss, not the outstanding loan balance.

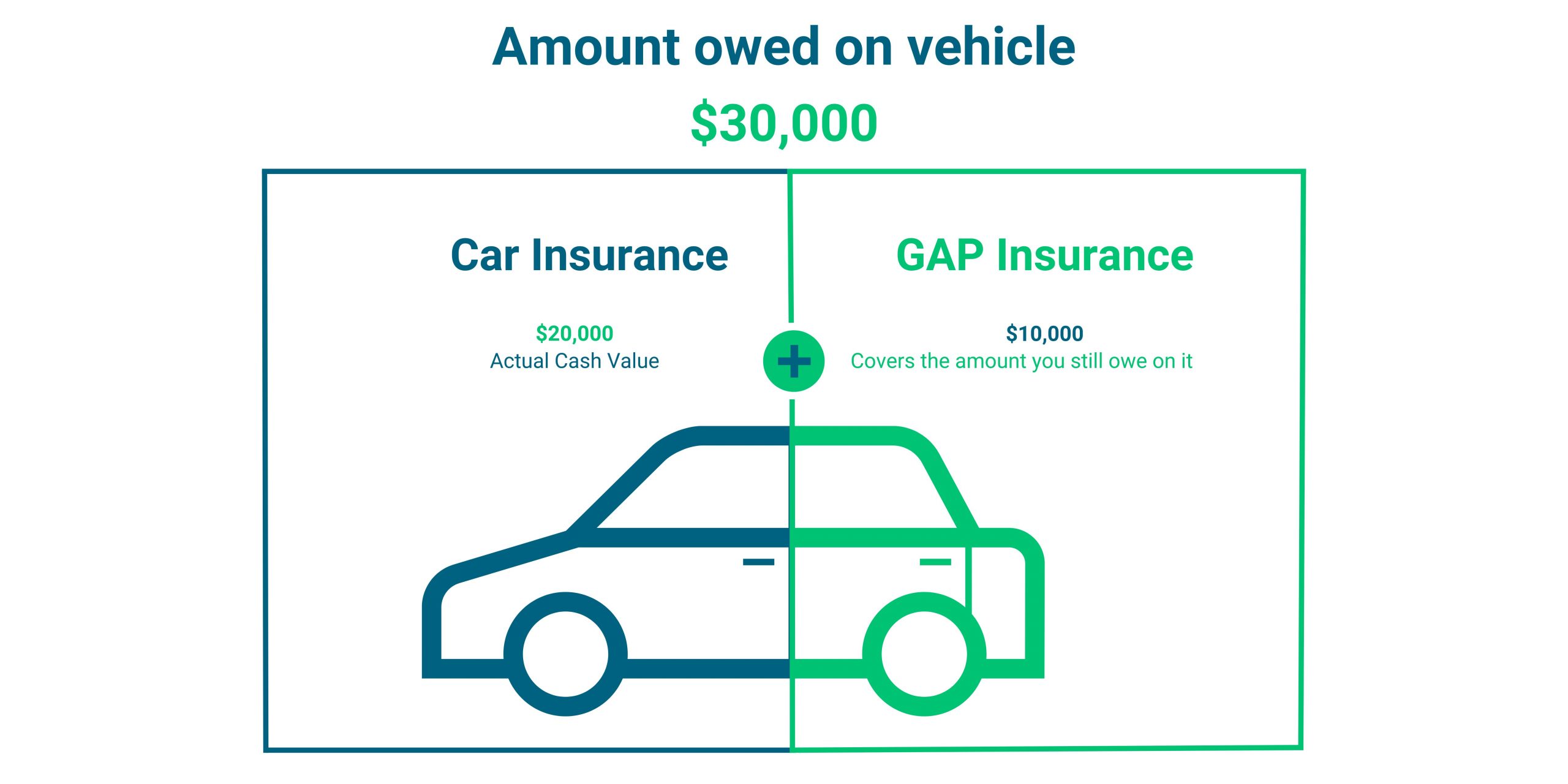

Consider this scenario: You purchase a car for $30,000 with a minimal down payment, financing $28,000. Within the first year, the car’s ACV might drop to $22,000 due to depreciation, while your loan balance, after interest and principal payments, might still be $25,000. If your car is declared a total loss, your standard insurer would pay out $22,000. This leaves a “gap” of $3,000 ($25,000 loan balance – $22,000 insurance payout) that you, the owner, are still legally obligated to pay to your lender, despite no longer having the vehicle. This is the financial risk gap coverage is designed to eliminate.

Total Loss Scenarios: When it Matters Most

Gap coverage becomes indispensable in total loss scenarios. A total loss typically occurs when a vehicle is so severely damaged in an accident that the cost of repairs exceeds a certain percentage of its ACV, or when it is stolen and not recovered. Without gap coverage, the financial burden of repaying a loan on a vehicle that no longer exists can be substantial. This can lead to significant financial strain, potentially forcing individuals into debt or delaying the purchase of a replacement vehicle, creating further logistical and financial challenges. The peace of mind offered by knowing this financial risk is mitigated is a significant benefit to responsible financial planning.

How Gap Coverage Works: Mechanics and Benefits

Gap coverage acts as a financial bridge, connecting the valuation provided by your primary auto insurer with the remaining balance of your vehicle loan. It’s a supplementary form of insurance, typically distinct from your comprehensive or collision policies, specifically designed to address the unique financial challenge of negative equity in a total loss event.

Bridging the Financial Divide

When a covered vehicle is declared a total loss, your primary auto insurance policy will pay out its actual cash value (ACV). If this ACV is less than your outstanding loan or lease balance, gap coverage steps in to pay the difference. For example, if your primary insurer pays $20,000 for a totaled vehicle, but you still owe $24,000 on your loan, gap coverage would pay the remaining $4,000. This direct payment to the lender ensures that you are no longer financially obligated for a vehicle you no longer possess. It effectively zeroes out your debt on that specific asset, preventing a situation where you’re making payments on a phantom car.

Who Benefits Most from Gap Coverage?

While gap coverage can be a prudent financial decision for many car owners, certain circumstances make it particularly valuable:

- Minimal or No Down Payment: A small down payment means a larger initial loan balance, exacerbating the LTV discrepancy from the outset.

- Long Loan Terms (e.g., 60 months or more): Extended loan terms slow down the rate at which principal is repaid, keeping the loan balance higher for longer and increasing the risk of negative equity.

- High-Depreciation Vehicles: Some vehicles, particularly new luxury cars or models that undergo frequent redesigns, depreciate more rapidly than others.

- Rolling Over Negative Equity: If you rolled negative equity from a previous car loan into your current financing, your starting loan balance is already inflated, making gap coverage almost essential.

- Leased Vehicles: Many lease agreements automatically include some form of gap protection, as lessees are typically responsible for any shortfall between the vehicle’s value and the remaining lease payments in a total loss scenario. However, it’s crucial to confirm this is included and understand its specifics.

For these individuals, gap coverage isn’t just an option; it’s a vital component of a sound financial strategy, protecting against significant unrecoverable debt.

Types of Vehicles Covered

Gap coverage is generally available for new and used cars, light trucks, and SUVs. Most policies require the vehicle to be no more than a few years old (typically under 7-10 years) and have relatively low mileage at the time of purchase. Commercial vehicles, motorcycles, or recreational vehicles might have different or specialized gap products, or may not be eligible under standard auto gap policies. Always confirm eligibility with the provider based on your specific vehicle and usage.

Key Considerations Before Purchasing: Is it Right for You?

Deciding whether to purchase gap coverage requires a careful financial assessment. It’s an investment in risk mitigation, and like all financial products, its value depends on your specific circumstances and risk profile.

Loan-to-Value Ratio: The Crucial Metric

The single most important factor in determining the need for gap coverage is your loan-to-value (LTV) ratio. If your loan amount significantly exceeds the vehicle’s market value, your risk is high. This often occurs when:

- You make a down payment of less than 20%.

- Your loan term is unusually long (e.g., 72 or 84 months).

- Your vehicle is known for rapid depreciation.

- You’ve financed additional costs (e.g., extended warranties, service contracts, negative equity from a trade-in) into your loan.

A simple calculation of your current loan balance versus your vehicle’s estimated actual cash value (using resources like Kelley Blue Book or Edmunds) can reveal your exposure.

Down Payments and Loan Terms

A substantial down payment (20% or more) immediately reduces the LTV discrepancy and speeds up the equity build-up in your vehicle. Shorter loan terms also contribute to faster principal reduction. If you made a significant down payment and opted for a short loan term, you might find that you quickly achieve positive equity, meaning your car’s value exceeds your loan balance. In such cases, the financial benefit of gap coverage diminishes over time and might become unnecessary relatively quickly.

Vehicle Depreciation Rates

Researching the depreciation rate of your specific vehicle make and model can provide valuable insight. Some vehicles hold their value exceptionally well, while others plummet in value rapidly. A car with a historically high depreciation rate would inherently present a greater “gap” risk, making gap coverage a more financially sound decision.

Cost-Benefit Analysis

Gap coverage is not free. Its cost can vary from a few hundred dollars as a one-time fee to a few dollars per month added to your insurance premium. Compare this cost against the potential financial loss you might incur without it. If the potential gap is substantial (e.g., several thousand dollars) and your budget would be severely strained by having to pay that difference out-of-pocket, then the cost of gap coverage is a reasonable investment in financial security. However, if your LTV ratio is favorable and the potential gap is minimal, the expense might outweigh the benefit.

Where to Acquire Gap Coverage: Options and Providers

The market offers several avenues for purchasing gap coverage, each with its own advantages and financial implications. Understanding these options allows you to make an informed decision that aligns with your financial planning.

Dealerships: Convenience vs. Cost

Many car dealerships offer gap coverage as an add-on during the vehicle purchase process. The primary advantage here is convenience; it’s often rolled directly into your car loan, meaning no separate monthly payments. However, this convenience often comes at a higher price. When gap coverage is financed into the loan, you end up paying interest on the gap coverage premium itself, increasing its total cost. Dealerships typically mark up the price of gap policies significantly, making it potentially the most expensive option.

Insurance Companies: Often More Affordable

Your existing auto insurance provider is often the most cost-effective source for gap coverage. Many major insurers offer it as an endorsement or rider to your standard policy. When purchased this way, it’s usually added as a small monthly or semi-annual fee to your regular premium, often totaling less than a few dollars per month. Because it’s not financed and generally has lower administrative costs, this route typically provides the best value. Contact your current insurer for a quote to compare.

Credit Unions and Banks: Another Avenue

If you finance your car through a credit union or bank, they may also offer gap coverage as part of their loan packages. Similar to dealerships, it might be bundled into your loan, but often at a more competitive rate than a dealership would offer. It’s always wise to inquire about their gap options and compare them against quotes from your auto insurance provider.

Independent Providers

There are also third-party companies specializing in gap insurance. These providers can sometimes offer competitive rates, especially for specific vehicle types or higher-risk profiles. However, always exercise due diligence when considering independent providers: check their ratings, reviews, and ensure they are reputable and properly licensed.

Understanding the Fine Print: Exclusions and Limitations

While gap coverage offers substantial financial protection, it’s crucial to understand its limitations and exclusions to avoid unexpected financial surprises. Like any financial product, knowing the specifics of your policy is key to effective risk management.

Deductibles and Payout Limits

Some gap policies may have a deductible, meaning you’re responsible for a portion of the gap amount before the policy pays out. More commonly, gap coverage will cover your primary insurer’s deductible as part of the total payout. For instance, if your primary insurer pays $20,000, and your loan is $24,000, leaving a $4,000 gap, the gap policy might state it covers the $4,000 plus your $500 comprehensive/collision deductible, effectively paying $4,500. Conversely, policies often have a payout limit, typically expressed as a percentage of the vehicle’s ACV (e.g., up to 125% or 150% of ACV). This means there’s a cap on how much the gap policy will pay, which could be relevant if you have an extremely large amount of negative equity.

Negative Equity Rollover

A common exclusion in many gap policies is coverage for negative equity rolled over from a previous car loan. If you traded in a car and owed more on it than it was worth, and that deficit was added to your new car loan, some gap policies may not cover the portion of your loan attributable to that rolled-over negative equity. It’s imperative to clarify this specific clause with your provider.

Pre-existing Damage and Usage

Gap coverage typically only applies to a total loss event as defined by your primary insurer. It does not cover pre-existing damage, mechanical breakdowns, or vehicles used for commercial purposes without a specific commercial gap policy. Furthermore, some policies may have exclusions related to reckless driving, driving under the influence, or vehicles being used in races or competitions.

When Gap Coverage Isn’t Needed

Finally, it’s important to recognize when gap coverage is no longer a financially sound investment. If you’ve paid down your loan significantly and your vehicle’s market value now exceeds your outstanding loan balance (i.e., you have positive equity), gap coverage becomes redundant. Many policies allow you to cancel at any time and receive a prorated refund if you paid upfront. Regularly review your LTV ratio to determine if continuing gap coverage aligns with your financial interests. This proactive approach ensures you’re not paying for protection you no longer need.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.