In the intricate global economy, financial institutions serve as indispensable conduits, facilitating the flow of capital, managing risk, and enabling countless transactions that underpin daily life and business operations. From the local credit union to multinational investment banks, these entities are the bedrock of modern finance, connecting savers with borrowers and shaping the economic landscape. Understanding what constitutes a financial institution, the myriad forms they take, and their overarching significance is crucial for anyone navigating the complexities of personal finance, business strategy, or macroeconomic policy.

The query “what is financial institution name” often precedes a deeper dive into understanding these crucial entities. While the names themselves vary widely—from “Bank of America” to “Prudential Financial” to “Fidelity Investments”—the underlying principles of their operations and their essential roles remain consistent: they are intermediaries in the financial system. This article will explore the core definition of financial institutions, delineate their diverse types, elaborate on their critical functions, and provide insight into how individuals and businesses can make informed choices about partnering with them.

What Exactly is a Financial Institution?

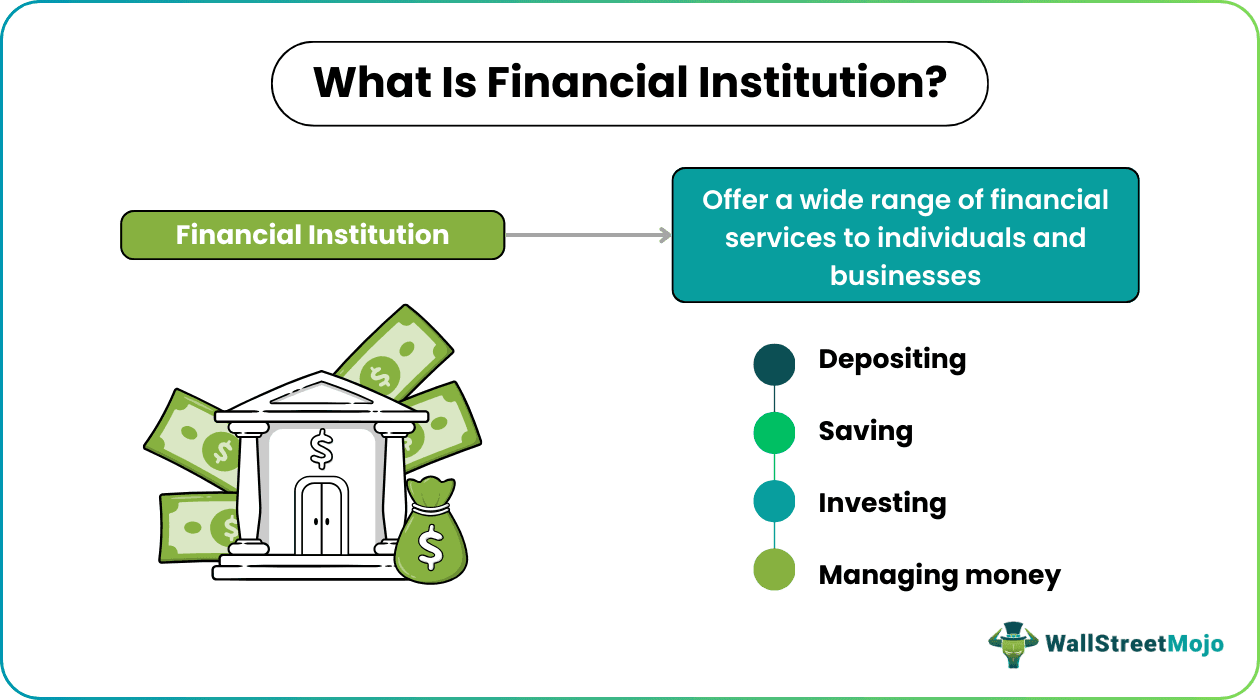

At its core, a financial institution is an enterprise that deals with financial and monetary transactions, such as deposits, loans, investments, and currency exchange. They essentially act as intermediaries between those who have capital (savers/investors) and those who require capital (borrowers/companies). Their primary function is to mobilize savings and channel them into productive investments, thereby fostering economic growth.

Defining the Core Concept

A financial institution aggregates funds from a large number of individuals and organizations and then lends those funds out to other individuals, businesses, or governments. This process involves a transformation of financial assets—taking short-term deposits and converting them into long-term loans, for example, or pooling small investments into diversified portfolios. They generate revenue through interest rate differentials (charging borrowers a higher interest rate than they pay depositors), fees for services, and investment returns. Crucially, they are entrusted with the safekeeping and management of vast sums of money, making their stability and integrity paramount.

The Regulatory Framework

Given their central role and the systemic risks associated with their potential failure, financial institutions are among the most heavily regulated entities in the world. Regulators, such as central banks (e.g., the Federal Reserve in the U.S.), government agencies (e.g., the FDIC, SEC), and international bodies, impose strict rules regarding capital adequacy, liquidity, risk management, and consumer protection. This stringent oversight aims to ensure the stability of the financial system, prevent fraud, protect depositors and investors, and maintain public confidence. Adherence to these regulations is a defining characteristic of legitimate financial institutions, distinguishing them from less formal financial intermediaries.

Diverse Landscape: Key Types of Financial Institutions

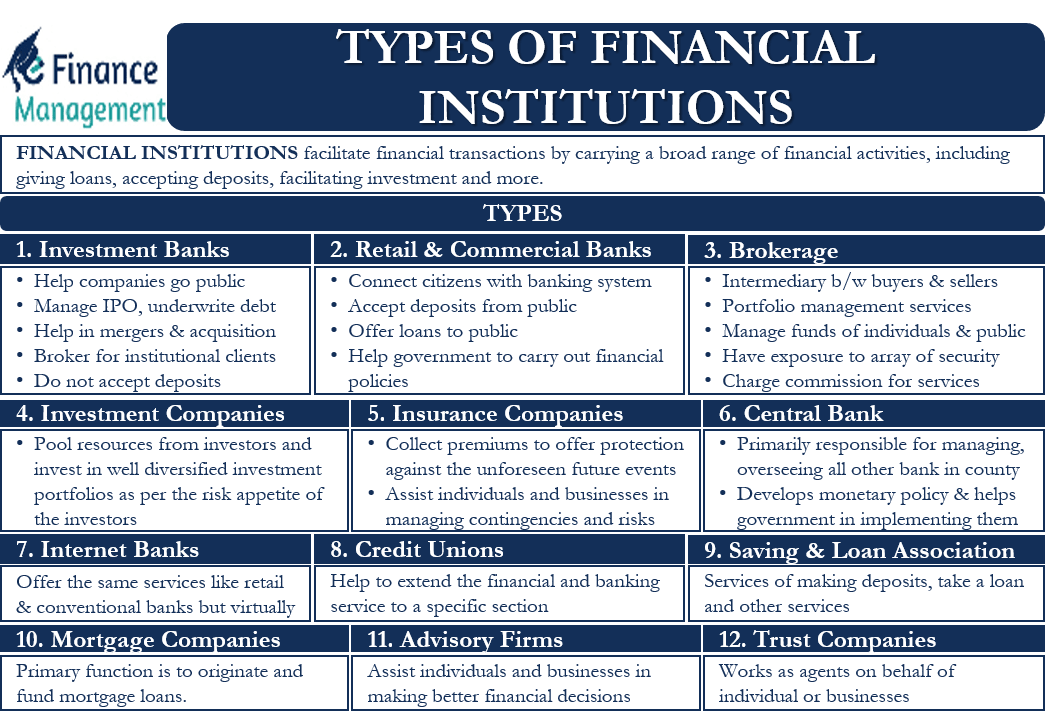

The financial sector is remarkably diverse, populated by various types of institutions, each specializing in different aspects of financial services. While they all serve as intermediaries, their specific functions, clienteles, and operational models can vary significantly.

Depository Institutions: Banks and Credit Unions

These are perhaps the most common and recognizable financial institutions. They accept deposits from individuals and businesses and provide loans.

- Commercial Banks: The largest and most numerous, offering a wide range of services including checking and savings accounts, personal and business loans, mortgages, credit cards, and often wealth management and investment banking services. Examples include JPMorgan Chase, Bank of America, Wells Fargo.

- Credit Unions: Member-owned cooperative financial institutions. They offer similar services to banks but are generally non-profit and often provide more favorable interest rates on loans and deposits due to their structure. Membership is typically based on a common bond, such as employment, geographical location, or association.

Contractual Institutions: Insurance Companies and Pension Funds

These institutions obtain funds through contractual agreements and make payments under specific circumstances. They are characterized by long-term liabilities and thus tend to invest in long-term assets.

- Insurance Companies: Collect premiums from policyholders and provide protection against financial losses from various risks (e.g., life, health, property, casualty). They invest these premiums to generate returns, ensuring they can pay out claims.

- Pension Funds: Manage retirement savings for employees, pooling contributions from individuals and employers. They invest these funds over long periods to provide a steady income stream to retirees.

Investment Institutions: Investment Banks, Brokerage Firms, and Mutual Funds

These institutions primarily facilitate capital market activities, helping businesses raise capital and individuals invest.

- Investment Banks: Serve corporations and governments by underwriting new stock and bond issues, advising on mergers and acquisitions, and providing financial advisory services. They do not typically accept deposits from the general public. Examples include Goldman Sachs, Morgan Stanley.

- Brokerage Firms: Facilitate the buying and selling of stocks, bonds, mutual funds, and other securities for individual and institutional investors. They charge commissions for their services. E*TRADE and Charles Schwab are well-known examples.

- Mutual Funds: Investment vehicles that pool money from multiple investors to invest in a diversified portfolio of securities (stocks, bonds, money market instruments). They are managed by professional fund managers and offer investors a convenient way to diversify their holdings.

Other Specialized Institutions: Mortgage Lenders and Fintech Companies

The financial landscape also includes specialized entities addressing niche needs or leveraging new technologies.

- Mortgage Lenders: Institutions solely focused on originating and servicing mortgage loans. While often part of larger banks, many independent mortgage companies specialize in this area.

- Fintech Companies: Technology-driven firms that offer innovative financial products and services, often disrupting traditional models. This can range from online payment platforms (e.g., PayPal, Square) and digital-only banks to robo-advisors and peer-to-peer lending platforms. They represent a significant evolution in how financial services are delivered.

The Indispensable Role of Financial Institutions in the Economy

The presence and efficient operation of financial institutions are not merely convenient; they are fundamental to the health and growth of any modern economy. Their roles extend far beyond simple money handling, touching every aspect of economic activity.

Facilitating Capital Allocation

One of the most critical roles of financial institutions is to efficiently allocate capital. They gather scattered savings, transform them into larger sums, and direct these funds towards productive uses—such as financing business expansion, infrastructure projects, innovation, and housing. This process is essential for economic dynamism, ensuring that resources flow to where they can generate the most value. Without this intermediation, individuals with surplus funds would struggle to find reliable borrowers, and businesses with viable projects would find it difficult to secure funding, stifling growth.

Managing Risk and Providing Security

Financial institutions play a vital role in managing and mitigating various financial risks. Insurance companies, for instance, pool risks, protecting individuals and businesses from unforeseen losses. Banks assess credit risk, diversifying their loan portfolios to reduce the impact of individual defaults. They also provide secure platforms for storing funds, processing payments, and conducting transactions, offering a level of safety and reliability that individuals and small businesses would find challenging to achieve independently. The regulatory environment further reinforces this security, aiming to prevent systemic failures.

Supporting Economic Growth and Stability

By fostering savings, facilitating investment, and providing efficient payment systems, financial institutions are direct drivers of economic growth. They enable consumer spending, business investment, and international trade. Moreover, they contribute to economic stability by providing liquidity to markets, managing monetary policy (in collaboration with central banks), and offering mechanisms for individuals and businesses to smooth consumption and investment over time. A robust and stable financial sector is a prerequisite for sustained economic prosperity.

Impact on Individuals and Businesses

For individuals, financial institutions offer essential services like savings accounts, mortgages, car loans, credit cards, and retirement planning, enabling them to manage their finances, achieve life goals, and navigate financial challenges. For businesses, they provide critical funding for operations, expansion, and innovation, alongside services like payment processing, treasury management, and foreign exchange. They are partners in growth, offering expertise and resources that are vital for both startups and established corporations.

Navigating Your Choices: Selecting the Right Financial Partner

Given the diversity of financial institutions and services, choosing the right partner is a critical decision for both individuals and businesses. This choice significantly impacts financial health, convenience, and goal attainment.

Factors to Consider for Personal Finance

When selecting a bank, credit union, or investment firm, individuals should consider several factors:

- Fees and Rates: Compare interest rates on savings accounts and loans, as well as monthly maintenance fees, ATM fees, and transaction charges.

- Services Offered: Ensure the institution provides the specific services you need, such as online banking, mobile apps, bill pay, wealth management, or specific loan products.

- Accessibility: Consider branch locations, ATM networks, and the quality of digital banking platforms.

- Customer Service: Research reviews and assess the responsiveness and helpfulness of their customer support.

- Security and Insurance: Confirm that deposits are insured by relevant government bodies (e.g., FDIC in the U.S. for banks, NCUA for credit unions).

Considerations for Businesses

Businesses have additional layers of complexity when choosing financial partners:

- Business Banking Services: Look for specialized accounts, lines of credit, payroll services, merchant services for processing payments, and commercial lending options.

- Scalability: Can the institution support your business as it grows, offering more complex financial products and larger credit lines?

- Industry Expertise: Some financial institutions specialize in particular industries and may offer more tailored solutions or a deeper understanding of specific business challenges.

- International Capabilities: For businesses involved in global trade, the ability to handle foreign exchange, international wire transfers, and trade finance is crucial.

The Rise of Digital and Fintech Solutions

The advent of digital-only banks, robo-advisors, and various fintech platforms has expanded the options available, particularly for those comfortable with technology. These platforms often offer lower fees, higher interest rates, and highly intuitive user experiences. However, it’s essential to research their regulatory compliance, security measures, and customer support infrastructure, as some newer entrants might not have the same long-standing track record as traditional institutions. Hybrid models, combining digital convenience with limited physical presence, are also becoming increasingly common.

The Future of Financial Institutions: Trends and Transformations

The financial services industry is in a constant state of evolution, driven by technological innovation, shifting consumer expectations, and evolving regulatory landscapes. Understanding these trends provides insight into the future direction of financial institutions.

Digitalization and Customer Experience

The digital transformation is perhaps the most profound trend. Financial institutions are investing heavily in AI, machine learning, blockchain, and cloud computing to enhance operational efficiency, personalize customer experiences, and bolster security. Mobile banking apps are becoming central hubs for financial management, offering everything from budgeting tools to investment platforms. The focus is increasingly on providing seamless, instant, and intuitive digital interactions.

Regulatory Evolution

As technology advances and new financial products emerge, regulators are continuously adapting their frameworks. There’s a growing emphasis on data privacy (e.g., GDPR, CCPA), cybersecurity, and ensuring fair practices in algorithmic lending and investment. The balance between fostering innovation and maintaining financial stability remains a core challenge for policymakers globally.

Emerging Business Models

The competitive landscape is being reshaped by fintechs, challenger banks, and even big tech companies entering financial services. This pressure is forcing traditional institutions to innovate, partner with technology firms, or acquire them. We are seeing a move towards more modular, API-driven banking, allowing for greater integration of services and personalized product offerings. The concept of “embedded finance,” where financial services are seamlessly integrated into non-financial platforms (e.g., buying insurance when purchasing a car online), is also gaining traction, blurring the lines between traditional sectors.

In conclusion, financial institutions, regardless of their specific names or niche, remain central pillars of the global economy. They are dynamic entities, constantly adapting to serve the evolving financial needs of individuals and businesses. A comprehensive understanding of their functions, types, and the trends shaping their future is invaluable for anyone seeking to navigate the modern financial world effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.