Interest rates are often described as the “price of money.” They represent the cost of borrowing and the reward for saving, serving as the primary lever by which global economies are balanced. In the current economic climate, understanding the current rate of interest is not merely a matter of academic curiosity; it is a vital necessity for anyone looking to purchase a home, grow a business, or protect their personal savings. As we navigate a period of significant transition in monetary policy, the fluctuations in these rates dictate the flow of capital across the globe, influencing everything from the strength of the dollar to the monthly payments on a standard credit card.

The Foundations of Interest Rates and Central Bank Policy

To understand why the current rate of interest sits where it does today, one must first look toward the central banks, specifically the Federal Reserve in the United States. Central banks are tasked with a “dual mandate”: maintaining price stability (controlling inflation) and promoting maximum sustainable employment. When inflation rises above the target 2% threshold, central banks typically raise the “federal funds rate”—the interest rate at which commercial banks borrow and lend to each other overnight.

The Role of the Federal Reserve and Inflation Control

Over the past twenty-four months, the financial world has witnessed one of the most aggressive “tightening” cycles in modern history. To combat the inflationary pressures that emerged post-pandemic, the Federal Reserve raised benchmark rates from near zero to a range exceeding 5%. This move was designed to cool an overheated economy by making it more expensive for businesses to expand and for consumers to spend. The current rate of interest reflects this restrictive stance, as the Fed maintains a “higher for longer” philosophy to ensure inflation returns to its long-term target.

How Benchmark Rates Trickle Down to Consumers

The federal funds rate is the “base” of the financial pyramid. While most consumers do not borrow directly at this rate, it serves as the foundation for the Prime Rate—the base interest rate that commercial banks charge their most creditworthy corporate customers. When the Fed raises its benchmark, the Prime Rate follows suit almost instantly. This, in turn, impacts the interest rates on variable-rate products such as Home Equity Lines of Credit (HELOCs), credit cards, and adjustable-rate mortgages. Understanding this ripple effect is essential for predicting how personal debt obligations will change in response to central bank announcements.

Navigating the Lending Market: Mortgages and Personal Loans

For the average individual, the most tangible impact of the current rate of interest is felt when applying for a loan. The lending market has undergone a paradigm shift, moving away from the era of “easy money” that defined the 2010s into a period of more traditional, higher-cost borrowing.

The 30-Year Fixed Mortgage Reality

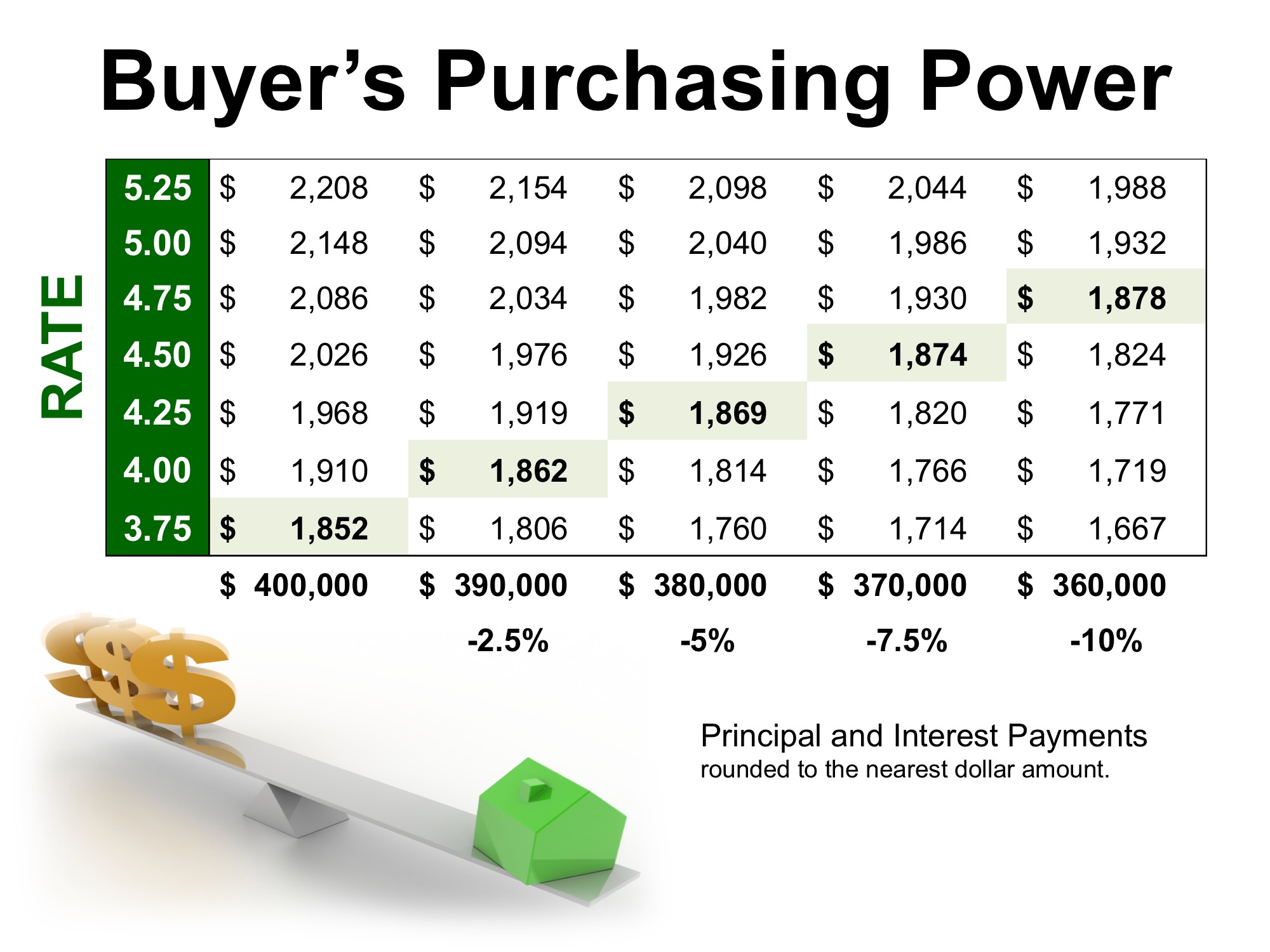

Mortgage rates do not track the federal funds rate perfectly; instead, they are closely tied to the yield on the 10-year Treasury note. Because investors view mortgages as long-term commitments, they demand a premium over government bonds. In the current environment, 30-year fixed mortgage rates have fluctuated significantly, often hovering between 6% and 7.5%. This is a stark contrast to the 3% rates seen in 2021. For a homebuyer, this difference can mean hundreds, if not thousands, of dollars in additional monthly interest payments, significantly impacting “affordability” and cooling the broader housing market.

Auto Loans and Personal Credit Trends

Beyond housing, the current rate of interest has permeated the automotive and personal loan sectors. Financing a vehicle has become considerably more expensive, with average new-car loan rates climbing well above 7% for those with excellent credit, and significantly higher for subprime borrowers. Personal loans, often used for debt consolidation or home improvement, have seen similar spikes. Lenders have also become more discerning, tightening their credit standards as the cost of capital rises, meaning that “the current rate” is often only available to those with the highest credit scores.

The Silver Lining: High-Yield Savings and Fixed-Income Investing

While high interest rates present a challenge for borrowers, they offer a significant boon for savers and conservative investors. For over a decade, keeping money in a traditional bank account yielded essentially zero return. The current rate environment has fundamentally changed the math of personal savings.

The Rise of High-Yield Savings Accounts (HYSA) and CDs

Today, many online banks and credit unions offer High-Yield Savings Accounts with interest rates exceeding 4% or even 5%. This allows individuals to earn a meaningful return on their emergency funds without taking on market risk. Similarly, Certificates of Deposit (CDs) have regained popularity. By “locking in” the current rate of interest for a period of six months to two years, savers can guarantee a fixed return even if the Federal Reserve decides to cut rates in the near future. This has made “cash” a viable asset class for the first time in a generation.

Bonds and the Inverted Yield Curve

The current rate of interest also dictates the performance of the bond market. When new bonds are issued at higher rates, the value of existing bonds with lower rates typically falls. However, for new investors, current yields on Treasury bonds and corporate bonds are the most attractive they have been in years. We are also currently witnessing an “inverted yield curve,” where short-term interest rates are higher than long-term rates. Historically, this has been a signal of an impending economic slowdown, but for the modern investor, it offers a unique opportunity to capture high yields in short-term government securities.

Strategic Financial Management in a High-Rate Environment

In a world where the current rate of interest remains elevated, financial strategies must evolve. The “playbook” that worked in 2019—leveraging cheap debt to invest in growth—is no longer the most efficient path to wealth creation.

Prioritizing High-Interest Debt Liquidation

When interest rates are high, the most effective “investment” one can make is often paying down debt. Credit card interest rates frequently exceed 20% in the current market. Because these rates are variable, they rise in lockstep with the Fed. Paying off a balance with a 22% APR provides a “guaranteed return” of 22%—a figure that is almost impossible to match in the stock market or any other investment vehicle. Households are increasingly focusing on “debt avalanches” (paying off the highest interest rate first) to preserve their monthly cash flow.

Rethinking Capital Allocation and Business Finance

For entrepreneurs and business owners, the current rate of interest changes the “hurdle rate” for new projects. When the cost of borrowing is 8%, a business expansion must generate a significantly higher return to be considered profitable than it would if the cost of borrowing were 3%. This leads to a more disciplined approach to capital allocation. Businesses are currently focusing on efficiency, organic growth, and maintaining strong balance sheets rather than relying on aggressive debt-fueled acquisitions.

Long-Term Wealth Planning and Flexibility

The most important takeaway regarding the current rate of interest is that it is never static. Economic cycles move from expansion to contraction and back again. The current period of high rates may eventually give way to a “neutral” period as inflation stabilizes. Therefore, financial flexibility is key. This involves maintaining a diversified portfolio that includes both equities (which can hedge against inflation) and fixed income (which benefits from high current rates). By staying informed on the direction of interest rates, investors can pivot their strategies—refinancing debt when rates drop and locking in yields when rates peak—to ensure long-term financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.