The Federal Reserve, often referred to simply as “the Fed,” acts as the central bank of the United States. Perhaps its most powerful tool for influencing the economy is the setting of the federal funds rate. When you see headlines asking “what is the current Fed interest rate,” they are referring to the target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. While this might sound like a technicality of the banking system, it is the heartbeat of the American economy, dictating the cost of everything from a mortgage on a new home to the interest earned on a humble savings account.

As of the current economic cycle, the Federal Reserve has maintained a stance focused on balancing the twin goals of price stability and maximum employment. Following a period of aggressive rate hikes designed to curb post-pandemic inflation, the current rate environment represents a pivotal moment for investors, homeowners, and business owners alike.

The Mechanics of the Federal Funds Rate

To understand where the interest rate stands today, one must understand how it is determined and why it fluctuates. The decision-making power lies with the Federal Open Market Committee (FOMC), a group of twelve members who meet eight times a year to review economic data and decide whether to raise, lower, or maintain the target rate range.

How the FOMC Sets the Target Range

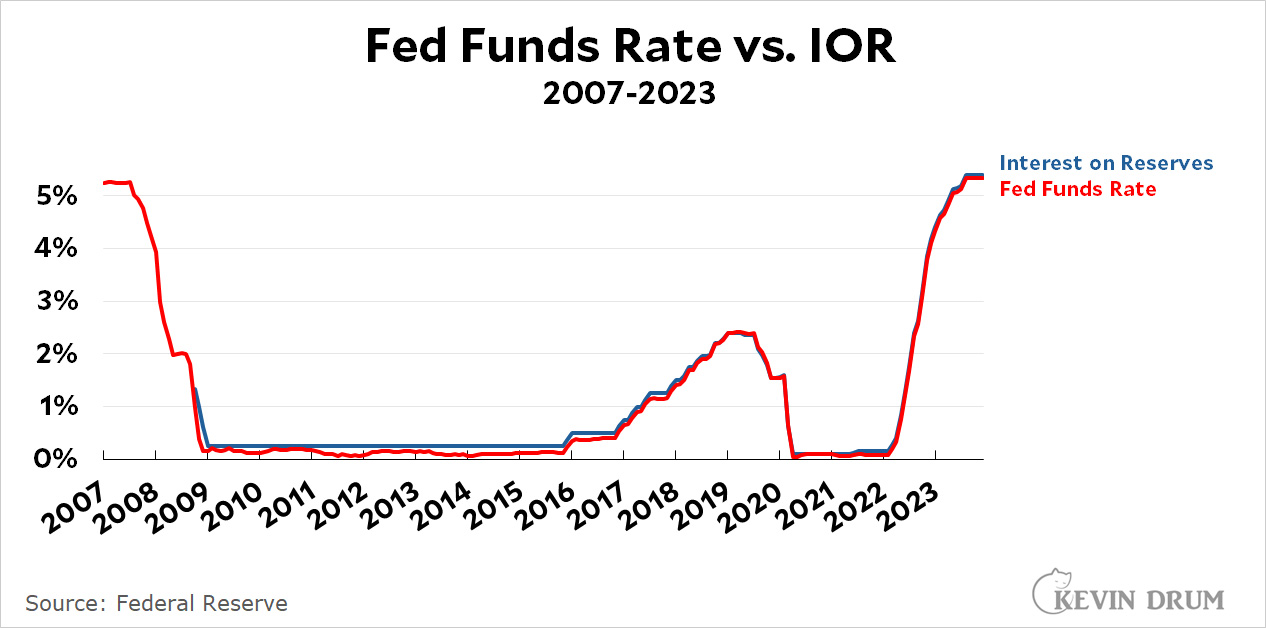

The Fed does not set a single, fixed interest rate. Instead, it establishes a “target range”—for example, 5.25% to 5.50%. The “Effective Federal Funds Rate” is the actual volume-weighted median of overnight rates within that range. By adjusting this range, the Fed influences the “price” of money. When the economy is overheating and inflation is high, the Fed raises rates to make borrowing more expensive, thereby slowing down spending. Conversely, when the economy is sluggish, the Fed lowers rates to encourage borrowing and investment.

The Role of Inflation and the “Dual Mandate”

The Fed operates under a “dual mandate” assigned by Congress: to promote maximum employment and stable prices. Typically, the Fed targets a 2% inflation rate. If the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE) price index shows inflation rising significantly above that target, the Fed will likely keep interest rates higher for longer. The current environment is a direct result of this battle against inflation, as the committee weighs the risks of a recession against the necessity of cooling price growth.

The Impact of “Dot Plots” and Forward Guidance

Investors don’t just look at the current rate; they look at where the Fed thinks rates will be in the future. Through a tool called the “Dot Plot,” FOMC members provide anonymous projections of future interest rates. This “forward guidance” is crucial for financial markets, as it allows banks and investors to price in future changes long before they actually happen.

Direct Impact on Personal Finance and Consumer Debt

The federal funds rate is the “base rate” from which almost all other consumer interest rates are derived. When the Fed moves its target range, the “Prime Rate”—the interest rate banks charge their most creditworthy corporate customers—moves in lockstep.

Mortgages and the Housing Market

While mortgage rates are more closely tied to the yield on the 10-year Treasury note than the Fed funds rate itself, they are heavily influenced by the Fed’s trajectory. In a high-rate environment, the cost of a 30-year fixed-rate mortgage increases significantly. This reduces the purchasing power of homebuyers, often leading to a cooling of the real estate market. For those with existing Adjustable-Rate Mortgages (ARMs), a rising Fed rate can lead to higher monthly payments, putting a strain on household budgets.

Credit Cards and Variable Interest Debt

Most credit cards have variable Annual Percentage Rates (APRs) tied to the Prime Rate. When the Fed raises interest rates, credit card interest rates usually go up within one or two billing cycles. In the current high-rate climate, carrying a balance on a credit card has become increasingly expensive, making debt transition strategies—such as balance transfers or debt consolidation loans—essential for financial health.

The Silver Lining: Savings and Certificates of Deposit (CDs)

High interest rates are a double-edged sword. While they make borrowing expensive, they reward savers. After years of near-zero interest on savings accounts, the current Fed rate has pushed yields on High-Yield Savings Accounts (HYSAs), Money Market Accounts, and Certificates of Deposit (CDs) to their highest levels in over a decade. For conservative investors and those building an emergency fund, this environment provides a rare opportunity to earn a meaningful return on cash without market risk.

Investing Strategies in a Shifting Rate Environment

The stock and bond markets react sharply to Fed interest rate decisions. Understanding these dynamics is key to maintaining a resilient investment portfolio.

The Inverse Relationship of Bonds

One of the fundamental rules of finance is that when interest rates rise, bond prices fall. This is because new bonds are issued with higher coupon rates, making existing bonds with lower rates less attractive. However, for new investors, higher rates mean higher “yield to maturity.” Navigating the current rate environment requires a strategic approach to “duration”—the sensitivity of a bond’s price to interest rate changes.

Equity Markets and Valuation

Higher interest rates generally put downward pressure on the stock market, particularly for “growth” stocks. This happens for two reasons. First, companies face higher borrowing costs, which can eat into profit margins. Second, when valuing a company, analysts discount future cash flows back to the present. A higher interest rate (the discount rate) results in a lower present value for those future earnings. Conversely, “value” sectors like banking often perform well when rates are higher, as they can expand their net interest margins.

Diversification and Real Assets

In times of interest rate uncertainty, diversification becomes paramount. Investors often look toward real assets, such as commodities or real estate investment trusts (REITs), though the latter can be sensitive to borrowing costs. The current environment encourages a “balanced” approach, where investors hold a mix of equities, fixed income, and cash equivalents to hedge against the volatility sparked by FOMC announcements.

The Broader Economic Ripple Effect

Beyond your personal bank account, the Fed interest rate shapes the very structure of the global economy.

Corporate Borrowing and Business Expansion

For businesses, the Fed rate determines the cost of capital. When rates are low, companies are more likely to take out loans to build new factories, hire more staff, or invest in research and development. When the current rate is high, businesses often adopt a “wait and see” approach, slowing down capital expenditures. This slowdown is exactly what the Fed intends when it tries to cool an overheating economy.

The Strength of the U.S. Dollar

The federal funds rate also affects the value of the U.S. dollar relative to other currencies. When the Fed maintains higher rates than other central banks (like the ECB or the Bank of Japan), the dollar tends to strengthen as global investors seek the higher yields offered by U.S. Treasuries. A strong dollar makes imports cheaper for Americans but makes U.S. exports more expensive for the rest of the world, impacting the trade deficit.

Avoiding a “Hard Landing”

The ultimate goal of the Fed’s current interest rate policy is to achieve a “soft landing”—a scenario where inflation returns to 2% without triggering a major recession or a spike in unemployment. The current “higher for longer” narrative suggests that the Fed is cautious about cutting rates too soon, fearing that inflation might reignite, while also remaining wary of keeping rates so high that the economy grinds to a halt.

Strategic Financial Planning for the Future

Given the current state of the Fed interest rate, how should individuals and businesses plan for the months ahead?

When to Lock in Rates

If you are considering a major purchase that requires financing, timing is everything. While it is impossible to “time the market” perfectly, monitoring the Fed’s language can provide clues. If the FOMC signals that they have reached the “terminal rate” (the peak of the hiking cycle), it may be an opportune time to lock in a fixed-rate loan before any potential volatility. Conversely, for savers, locking in a long-term CD while rates are at their peak can provide guaranteed income for years to come.

Monitoring Key Economic Indicators

To anticipate the next move in the Fed interest rate, keep an eye on three specific indicators:

- The Consumer Price Index (CPI): This measures inflation. If it falls, the Fed is more likely to cut rates.

- The Non-Farm Payrolls Report: This measures job growth. If the labor market stays too “hot,” the Fed may keep rates high to prevent wage-push inflation.

- GDP Growth: If the economy shows signs of significant contraction, the Fed will face pressure to lower rates to stimulate growth.

Conclusion: Staying Informed in a Dynamic Economy

The question of “what is the current Fed interest rate” is more than just a data point; it is a reflection of the health and direction of the global economy. By understanding the mechanics behind these rates and their far-reaching impacts on debt, savings, and investments, you can make more informed financial decisions. Whether you are a first-time homebuyer, a seasoned investor, or someone simply looking to maximize their savings, staying attuned to the Federal Reserve’s policy shifts is an essential component of modern financial literacy. As the Fed continues to navigate the complexities of the 21st-century economy, your ability to adapt your financial strategy to the prevailing rate environment will be a key driver of your long-term success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.