Understanding the distinctions between CONUS (Continental United States) and OCONUS (Outside Continental United States) is crucial for anyone navigating personal finance, investing, business operations, or employment that spans these geographical boundaries. These terms, while seemingly simple geographical descriptors, carry significant financial implications for individuals and businesses alike, influencing everything from taxation and cost of living to investment strategies and access to financial services.

Defining the Geographic and Financial Scope

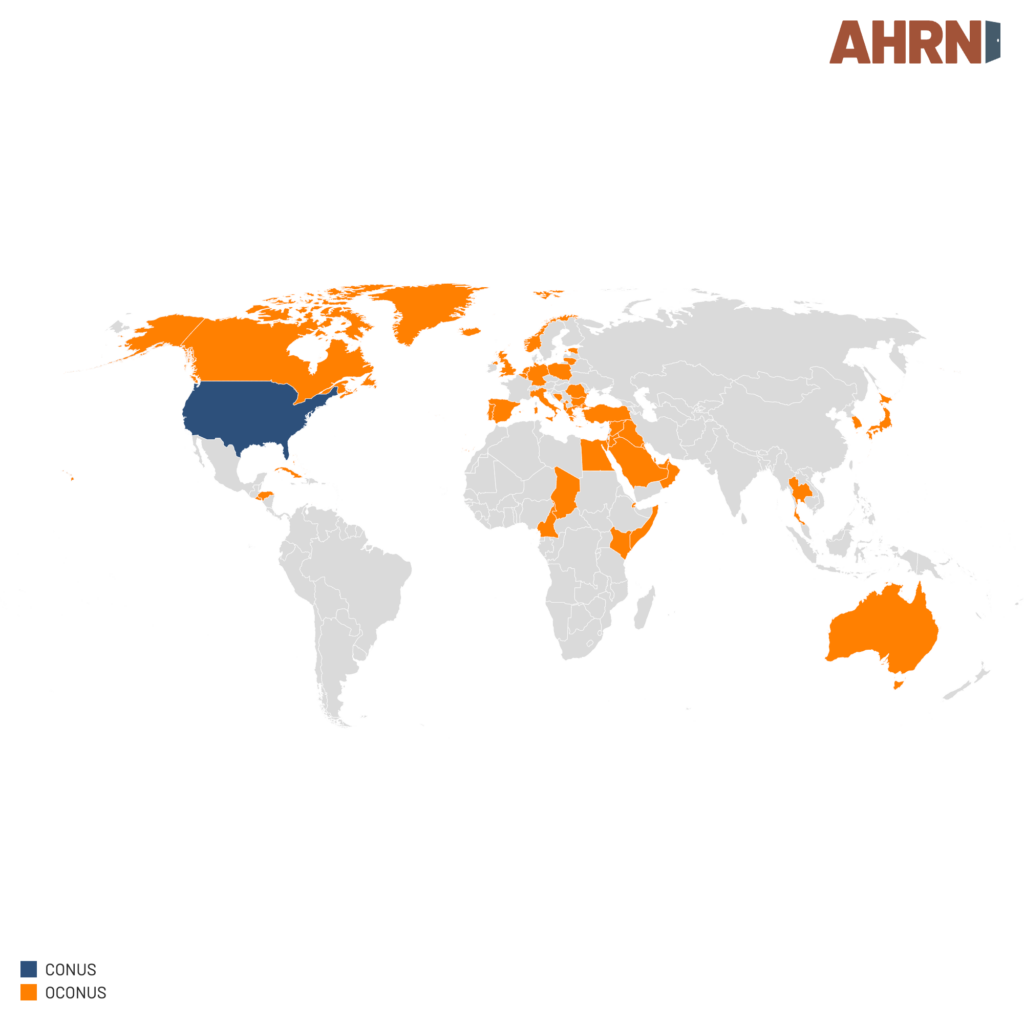

At its core, CONUS refers to the 48 contiguous states of the United States, along with the District of Columbia. OCONUS, by contrast, encompasses Alaska, Hawaii, and all U.S. territories and possessions (such as Puerto Rico, Guam, and the U.S. Virgin Islands), as well as foreign countries. For financial planning purposes, recognizing these delineations is the first step toward optimizing one’s fiscal strategy.

Understanding CONUS: The Domestic Financial Landscape

Within CONUS, the financial environment is largely homogenous in terms of federal regulations, banking systems, and market access. Individuals and businesses operate under a consistent set of federal tax laws, though state and local taxes can vary widely. Investment opportunities are readily accessible through major U.S. exchanges, and financial tools are generally standardized across state lines.

- Taxation: Income earned within CONUS is subject to federal income tax, state income tax (in most states), and local taxes where applicable. Property taxes, sales taxes, and other levies contribute to the overall tax burden, which can differ significantly from one state to another. Understanding these variations is key for budgeting and tax planning.

- Banking and Credit: The U.S. banking system provides a wide array of services, including checking and savings accounts, credit cards, mortgages, and loans, with established credit reporting agencies (Experian, Equifax, TransUnion) providing comprehensive credit scores. Access to credit is generally straightforward for residents with a financial history within the U.S.

- Investment Access: U.S. citizens and residents within CONUS have direct access to a robust array of investment vehicles, including stocks, bonds, mutual funds, ETFs, and real estate, typically through domestic brokerage firms and financial advisors. Retirement accounts like 401(k)s and IRAs are standard tools for long-term wealth accumulation.

- Cost of Living: While varying by state and city, cost of living within CONUS is typically benchmarked against a national average. Factors like housing, transportation, healthcare, and groceries contribute to the overall expenses, which directly impact budgeting and savings goals.

Decoding OCONUS: The International Financial Dimension

Operating or living OCONUS introduces a much more complex financial landscape. While U.S. citizens retain their federal tax obligations, the practicalities of earning, spending, and saving money are heavily influenced by the local economy, legal framework, and currency of the host location. This requires a sophisticated approach to financial management, often necessitating specialized knowledge or professional guidance.

- Taxation: U.S. citizens working abroad are still subject to U.S. federal income tax on their worldwide income. However, they may qualify for exclusions or credits, such as the Foreign Earned Income Exclusion (FEIE) or the Foreign Tax Credit, which can significantly reduce or eliminate U.S. tax liability on foreign earnings. Understanding residency rules and tax treaties is paramount to avoid double taxation and ensure compliance. State tax obligations may also vary depending on one’s domicile.

- Currency and Banking: Living OCONUS almost invariably involves dealing with foreign currencies, necessitating strategies for exchange rates, international transfers, and local banking. While some U.S. banks have international branches, opening local accounts and navigating foreign banking regulations can be challenging.

- Investment Access: Investing while OCONUS can be more complicated. Access to U.S. brokerage firms might be restricted based on residency, and navigating foreign investment markets carries additional risks related to currency fluctuations, political instability, and differing regulatory environments. Strategies often involve maintaining U.S.-based accounts or exploring internationally compliant investment platforms.

- Cost of Living and Allowances: The cost of living OCONUS can vary dramatically. In some locations, it may be significantly higher than in CONUS, while in others, it could be lower. For military personnel, government employees, and some private sector expatriates, various allowances (e.g., Cost of Living Allowance – COLA, Overseas Housing Allowance – OHA) are provided to offset the increased expenses associated with living abroad.

Financial Implications of CONUS vs. OCONUS Living

The choice or necessity of living CONUS or OCONUS profoundly impacts an individual’s financial strategy. From the intricacies of tax compliance to the practicalities of daily budgeting, each geographical context presents unique financial opportunities and challenges.

Taxation: Navigating IRS Rules and Foreign Tax Considerations

For U.S. citizens, the most significant financial differentiator between CONUS and OCONUS living is often taxation. While CONUS residents primarily deal with federal, state, and local taxes, OCONUS residents face the added complexity of foreign tax laws and their interplay with U.S. obligations.

- U.S. Federal Tax Obligation: The U.S. is one of the few countries that taxes its citizens on worldwide income, regardless of where they reside. This means an American earning income in Japan, for example, is still required to file a U.S. tax return.

- Foreign Earned Income Exclusion (FEIE): This allows qualifying individuals to exclude a significant portion of their foreign earned income from U.S. taxation (up to an inflation-adjusted amount). To qualify, one must meet either the Bona Fide Residence Test or the Physical Presence Test.

- Foreign Tax Credit: For income not covered by the FEIE or for income from non-employment sources, the Foreign Tax Credit allows taxpayers to reduce their U.S. tax liability dollar-for-dollar by the amount of income taxes paid to a foreign country.

- State Tax Domicile: Even while living OCONUS, an individual might maintain a state tax domicile, meaning they could still owe state income taxes depending on the state’s rules regarding residency and domicile. This requires careful planning, sometimes involving establishing domicile in a state with no income tax.

- Reporting Requirements: OCONUS residents face additional reporting requirements, such as the Report of Foreign Bank and Financial Accounts (FBAR) for accounts exceeding certain thresholds, and possibly Form 8938 (Statement of Specified Foreign Financial Assets). Non-compliance can lead to severe penalties.

Cost of Living and Compensation Adjustments

The financial reality of day-to-day living varies dramatically based on location. Compensation structures often reflect these differences.

- Cost of Living Allowances (COLA): For military members and some government employees, COLA is an additional allowance designed to offset the higher cost of goods and services in specific OCONUS locations compared to the CONUS average. This allowance is typically tax-free.

- Overseas Housing Allowance (OHA): This allowance assists OCONUS personnel in meeting housing costs that often exceed CONUS norms. Like COLA, OHA is generally tax-free.

- Private Sector Compensation: Private sector companies often offer expatriate packages that include salary enhancements, housing allowances, education benefits for dependents, and relocation assistance to compensate for the challenges and higher costs of living abroad.

- Purchasing Power: Understanding the local purchasing power of one’s income is critical for effective budgeting. Currency exchange rates constantly fluctuate, impacting the real value of U.S. dollar-denominated income in a foreign market.

Housing, Utilities, and Infrastructure Differences

Beyond direct costs, the availability and quality of housing, utilities, and infrastructure can significantly impact an OCONUS resident’s financial planning.

- Housing Market Dynamics: OCONUS housing markets can be vastly different from those in CONUS, with varying rental costs, property ownership regulations, and lease terms. Some locations may have limited housing options or require significant upfront costs.

- Utility Costs: Electricity, water, gas, and internet services can be more expensive, less reliable, or less accessible in some OCONUS locations. These variables must be factored into monthly budgets.

- Infrastructure and Services: Access to reliable transportation, healthcare facilities, and financial services infrastructure can impact daily expenses and overall quality of life, requiring potentially higher insurance costs or personal transportation investments.

Financial Planning Strategies for CONUS and OCONUS

Effective financial planning requires a tailored approach that accounts for the specific challenges and opportunities presented by CONUS or OCONUS living.

Budgeting for Geographical Realities

Creating a realistic budget is paramount. For OCONUS residents, this means incorporating variable costs like currency exchange fees, international call plans, potential travel expenses back to CONUS, and understanding local pricing for goods and services. Tools that track expenses in multiple currencies can be invaluable. CONUS residents, while facing fewer international complexities, still need to account for significant regional variations in housing, transportation, and state/local tax burdens.

Investment Considerations: Market Access and Currency Risk

- Maintaining U.S. Accounts: Many OCONUS residents find it beneficial to maintain U.S.-based brokerage accounts and retirement plans (401k, IRA) for easier management and access to familiar investment products, assuming their broker allows it based on their overseas address.

- Currency Diversification: Investing in assets denominated in various currencies can hedge against currency risk, particularly important for those whose income or expenses are primarily in a foreign currency but whose investments are in USD, or vice-versa.

- Local Investments: Exploring local investment opportunities in OCONUS countries might offer diversification and potential tax advantages, but requires thorough research into local regulations, market liquidity, and political stability.

- Estate Planning: Cross-border estate planning is complex, involving the laws of multiple jurisdictions and potential international tax treaties. Specialized legal and financial advice is often required to ensure assets are distributed according to one’s wishes.

Insurance and Healthcare: Protecting Your Assets and Well-being

- Health Insurance: While CONUS residents typically rely on employer-sponsored plans, Medicare, or ACA marketplaces, OCONUS residents may need international health insurance plans. Military and government personnel often have access to TRICARE or other federal programs. Understanding coverage limitations and local healthcare systems is critical.

- Life and Disability Insurance: These policies are just as crucial OCONUS as they are CONUS. Reviewing existing policies to ensure they provide adequate coverage regardless of residency is important.

- Property and Casualty Insurance: Homeowner’s or renter’s insurance in an OCONUS location might be sourced from local providers, requiring an understanding of local laws and coverage options. Vehicle insurance will certainly be country-specific.

Employment and Business Opportunities Across Borders

The distinction between CONUS and OCONUS significantly shapes employment prospects and business ventures.

Government and Military Careers

The U.S. government and military are primary employers that frequently necessitate OCONUS assignments. Personnel are subject to specific financial regulations, allowances, and benefits packages designed to mitigate the unique financial burdens of living abroad. Understanding these programs is vital for career and financial planning within these sectors.

Private Sector and Entrepreneurial Ventures

For the private sector, OCONUS assignments often come with expatriate packages, which are crucial for attracting talent globally. Entrepreneurs considering OCONUS operations must navigate international business laws, foreign exchange risks, and differing market dynamics. Online income opportunities, while location-independent in nature, still require an understanding of tax implications based on an individual’s tax residency.

Remittance and International Money Transfers

Sending money across borders, whether to support family, pay bills, or transfer savings, is a common financial activity for OCONUS residents. Choosing efficient and cost-effective methods for international money transfers (wire transfers, online services, cryptocurrency) is an important financial consideration. Fees, exchange rates, and transfer limits vary widely among providers.

Leveraging Financial Tools for Cross-Border Living

Modern financial tools can significantly simplify the complexities of managing money across CONUS and OCONUS boundaries.

Banking and Credit Management

- Global Banks: Utilizing banks with an international presence can streamline account management and transfers between countries.

- Multi-Currency Accounts: Some fintech platforms offer multi-currency accounts, allowing users to hold, send, and receive funds in various currencies, reducing exchange rate volatility and transfer fees.

- Credit History: Maintaining a good U.S. credit history, even while OCONUS, is important for future financial endeavors back in CONUS, such as mortgages or loans. Using U.S. credit cards with international usage in mind can help.

Tax Software and Professional Advice

Given the intricacies of international tax law, leveraging specialized tax software or, more commonly, consulting with a tax professional experienced in international taxation is highly recommended for OCONUS residents. These experts can help optimize tax strategies, ensure compliance, and navigate complex reporting requirements. CONUS residents also benefit from professional advice when dealing with state-specific tax nuances or complex investment income.

Relocation Assistance and Financial Advising

Many organizations offer relocation assistance for OCONUS moves, which can include financial planning support, assistance with banking, and guidance on local cost of living. Independent financial advisors specializing in expatriate finance can provide tailored advice on investments, retirement planning, and wealth management, specifically addressing the unique challenges faced by those living outside the Continental United States.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.