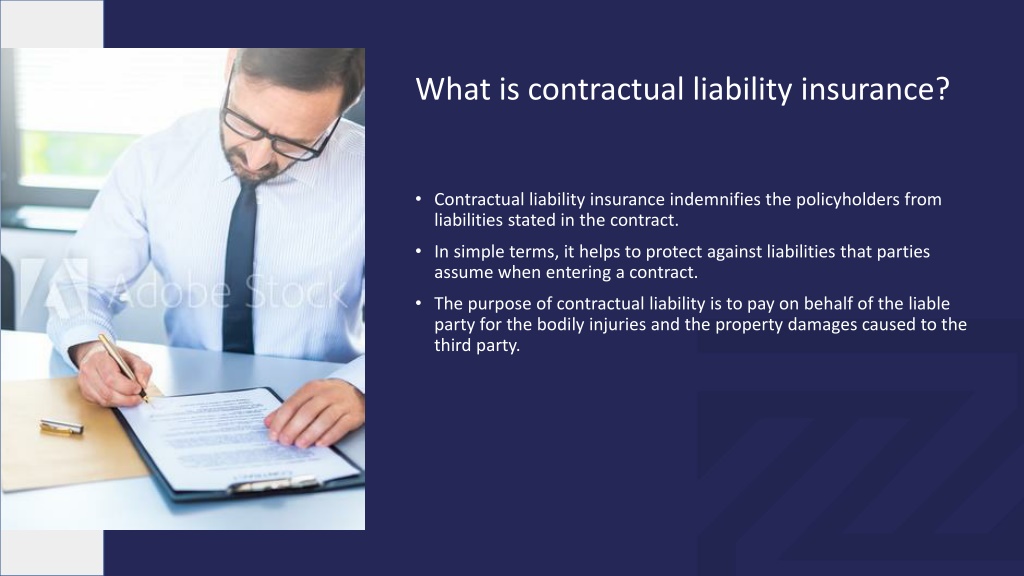

In the complex ecosystem of modern business finance, contracts serve as the foundational architecture for growth, collaboration, and service delivery. However, every agreement signed—whether with a vendor, a client, or a landlord—carries a hidden weight of financial risk. This is where contractual liability insurance becomes an essential instrument in a company’s financial toolkit. At its core, contractual liability insurance is a specialized form of coverage designed to protect a business against the financial fallout of liabilities it has voluntarily assumed through a legal contract.

For business owners, financial controllers, and investors, understanding the nuances of this insurance is not merely a legal checkbox; it is a vital component of strategic risk management. Without it, a single “hold harmless” clause in a standard service agreement could expose a firm’s entire balance sheet to catastrophic loss.

Understanding the Fundamentals of Contractual Liability Insurance

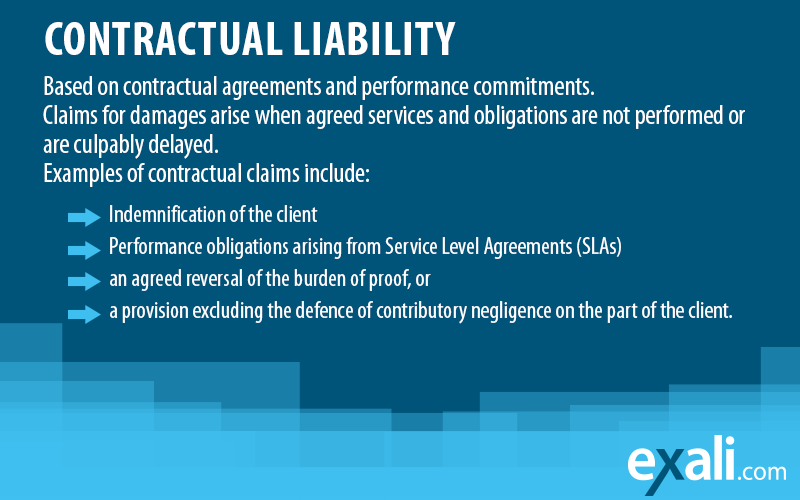

To grasp the importance of contractual liability insurance, one must first understand how liability functions in the commercial world. Typically, a business is liable for its own negligence. If a customer slips and falls on your premises, your general liability insurance responds. However, contractual liability is different because it involves “assumed” liability—meaning you have agreed to take on the legal and financial responsibility for someone else’s mistakes or accidents.

Definition and Core Purpose

Contractual liability insurance provides coverage for the financial obligations a business assumes when it enters into a contract. Specifically, it protects the policyholder in instances where they have agreed to indemnify or “hold harmless” another party. If a lawsuit arises and the contract stipulates that your business must pay for the legal fees or damages incurred by the other party, this insurance steps in to cover those costs, preserving your liquid capital and assets.

How it Differs from Standard General Liability

Many business owners mistakenly believe that a standard Commercial General Liability (CGL) policy covers all contractual obligations. In reality, most CGL policies contain an explicit exclusion for contractual liability. However, there is a significant “carve-back” within these policies for what are known as “insured contracts.” Understanding the boundary between what is automatically covered and what requires a specific endorsement is a critical task for any financial officer managing a company’s risk profile.

The Role of Indemnity Agreements

Indemnity is the heartbeat of contractual liability. An indemnity agreement is a promise by one party to compensate another for a loss. For example, a construction firm might sign a contract with a developer agreeing to indemnify the developer if a third party is injured on the job site. Even if the developer is partially at fault, the construction firm’s contractual liability coverage may be triggered to pay the settlement, protecting the developer’s financial interests as per the agreement.

Why Every Business Needs Contractual Risk Mitigation

From a business finance perspective, risk mitigation is about predictability. Unexpected legal judgments can derail a company’s cash flow and long-term investment strategies. Contractual liability insurance acts as a buffer, ensuring that the promises made in the boardroom do not lead to insolvency in the courtroom.

Protecting Assets in Third-Party Agreements

Whenever a business interacts with third parties—be they landlords, suppliers, or independent contractors—there is a transfer of risk. Landlords often require tenants to assume liability for any incidents occurring within a leased space. If a pipe bursts and damages a neighboring unit, the lease might dictate that the tenant pays. Without contractual liability insurance, those repair costs and potential lawsuits come directly out of the business’s operating budget, potentially depleting reserves intended for expansion or R&D.

Industries Where it is Non-Negotiable

While almost every sector benefits from this coverage, certain industries find it indispensable. In construction, manufacturing, and logistics, the “web of contracts” is dense. A manufacturer using a third-party distributor will likely have contracts that dictate who pays if a product fails. In these high-stakes environments, having robust insurance ensures that a business can fulfill its contractual promises without risking its fundamental solvency.

Navigating “Hold Harmless” Clauses

A “hold harmless” clause is a legal provision stating that one party will not hold the other responsible for certain risks. While these are standard in many industries, they represent a significant financial commitment. Contractual liability insurance is the mechanism that funds that commitment. By effectively “insuring” these clauses, a business can sign more ambitious contracts and partner with larger entities that demand high levels of risk assumption from their vendors.

Key Components and Coverage Limits

Not all insurance policies are created equal. For a business to be truly protected, the policy must align with the specific risks present in its unique contracts. This requires a deep dive into the policy’s structure and the limits of its coverage.

Blanket vs. Specific Contract Endorsements

Businesses generally have two options for structuring their coverage. A “Blanket” contractual liability endorsement covers all contracts that fall under the policy’s definition of an “insured contract” automatically. This is the preferred route for businesses that sign numerous standard agreements throughout the year. On the other hand, “Specific” endorsements are used for high-value or high-risk contracts that fall outside the standard definitions. For the financially savvy business leader, the choice between these depends on the volume and complexity of the firm’s contractual landscape.

Common Exclusions to Watch For

It is a financial mistake to assume that “contractual liability” covers every breach of contract. Generally, these policies do not cover a business’s failure to perform the work promised. For example, if you are contracted to build a software platform and fail to deliver it on time, contractual liability insurance will not pay the resulting late fees or lost profits. It is strictly limited to bodily injury or property damage claims arising from the contract. Distinguishing between professional errors and liability claims is essential for accurate financial planning.

Determining Appropriate Coverage Limits

How much coverage is enough? This is a question of capital allocation. Business leaders must evaluate the maximum potential loss associated with their largest contracts. If a company is working on a $10 million infrastructure project, a $1 million liability limit is woefully inadequate. Coverage limits should be scaled based on the value of the contracts held and the potential severity of risks involved in the specific industry.

Integrating Insurance into Your Business Finance Strategy

Insurance should not be viewed as a standalone expense but as a strategic asset. When integrated properly into the broader financial strategy, contractual liability insurance enables a company to take calculated risks that lead to higher returns.

Cost-Benefit Analysis of Premium vs. Potential Loss

Every dollar spent on an insurance premium is a dollar not spent on growth. However, a cost-benefit analysis usually reveals that the “cost of risk” (the premium) is far lower than the “cost of loss” (a lawsuit). By paying a predictable monthly or annual premium, a business replaces a massive, unpredictable financial volatility with a fixed operating expense. This stability is highly favored by lenders and investors, who want to see that a business is protected against “black swan” legal events.

The Impact on Long-term Financial Stability

Long-term stability is built on the ability to survive litigation. Even a frivolous lawsuit can cost tens of thousands of dollars in legal fees. Contractual liability insurance typically covers the cost of defense, which is often as valuable as the coverage for the settlement itself. By protecting the cash reserves of the company from being drained by legal battles, the business can maintain its credit rating and continue its long-term investment cycles uninterrupted.

Working with Financial Advisors and Brokers

Navigating the intersection of law, finance, and insurance requires professional expertise. Business owners should work closely with their financial advisors and insurance brokers to audit their existing contracts. This ensures that the language in the contracts matches the language in the insurance policy. A “gap” between what a contract promises and what a policy covers is a financial liability that can lead to significant out-of-pocket expenses.

Conclusion

In the modern financial landscape, contractual liability insurance is an essential safeguard. It bridge the gap between the legal promises a business makes and its physical ability to pay if things go wrong. By understanding the mechanics of indemnity, the necessity of risk mitigation, and the strategic importance of coverage limits, business leaders can protect their assets and ensure their company’s longevity.

Ultimately, money management is as much about protecting what you have as it is about earning more. Contractual liability insurance provides the peace of mind necessary to sign the next big deal, knowing that the company’s financial foundation is secure against the unpredictable tides of legal liability. Whether you are a small startup or a large corporation, mastering this aspect of business finance is a non-negotiable step toward sustainable success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.